@TypicalMatt5 Top 10 holdings differences between AVLV and DFLV respectively. Avantis profitability filters harder on cash-based operating profit jointly with P/B. DFA screening seemingly a little more traditional value-like (e.g UNH)

“Value and momentum are negatively correlated” is a long/short result only for HML vs UMD, both market-neutral.

Strip out market beta and the styles move closer together. With long-only funds, the shared beta drags it back up.

Last 10 years: SPMO vs DFLVX 0.70. Never negative.

@IndepBets CTA is very diff relative to SG CTA index, since they only trade commodities and rates. I think they strip out equities and currencies. They were heavily positioned long Oil pre-and-post Iran Hormuz closure. Since then it’s reversed. At one point up +15% YTD but now -1% YTD.

@TypicalMatt5 If you’re strictly worried about US Large Cap Value relative outperformance, then $AVLV is the objective winner. But this is a short 3.5 year backtest since inception of AVLV. Hard to say if it’ll continue but I have faith in Avantis’ methodology. Both beat Vanguard Value ETF.

Imagine DIY retail investor in 2019 was told they should invest 100% to US Small Cap Value & NOT participate in the mega-cap tech & AI. That would be a no-go for many.

Yet in fact, $AVUV (a systematic multi-factor US SCV approach w/flexible trading) has matched or exceeded VOO.

@choffstein This could work… trading 25% SCV factor purity for R2K beta exposure is a reasonable price if allocators are capital constrained and would otherwise not access trend at all.

@the_green_lark How might it change with different Momentum implementations? 12mo-1mo, 6mo (including recent month), monthly reconstitution vs semi-annual vs annual? Quality filtered momentum, etc.

@jaykaeppel@SystematicIRE US stocks? Global stocks? International stocks? Small cap stocks? Value stocks? Momentum stocks? Low Vol/Low beta stocks? Quality stocks?

What is the benchmark? Money can be made relative to a flat benchmark depending on allocation. Bonds, gold, managed futures still exist too.

Underlying holdings are not traditional value names one would expect:

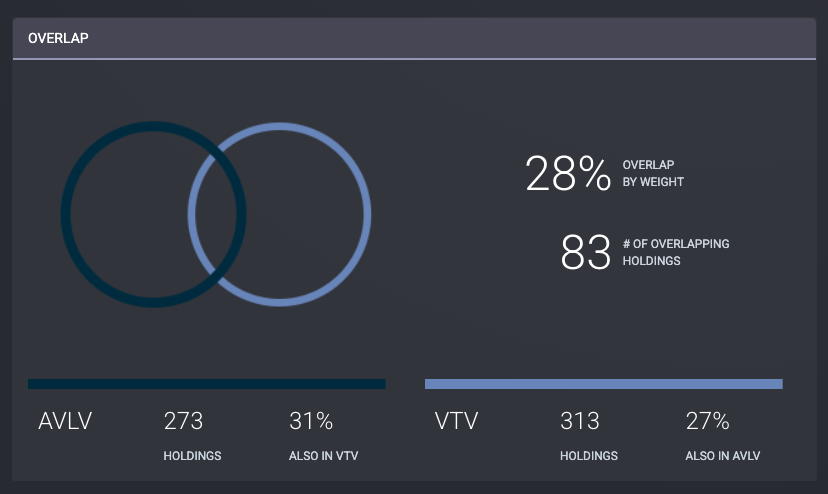

$AVLV has only a 28% overlap with $VTV.

Inside $AVLV are names like Micron, Apple, Amazon, Meta, Qualcomm, Lam Research, Caterpillar, Microsoft, Netflix.

This is a good reminder: despite the "Value" in Avantis US Large Cap Value ETF $AVLV, it's not a simple P/B or profitability sort. Weightings rise with a stock's expected return... cheap and profitable together. $AVLV has outperformed $VOO on a total return basis since inception.

Been loving the systematic process of $FMTM US Momentum ETF. 6-mo look back, reconstituted monthly, and a quality screened filter. It pairs exceptionally well with $SPMO for US Large Mo.

But I’m finding it hard to find a complement pair to $IDMO in developed ex-US. Any thoughts?

@jf10977@PFOInvestor And THIS is the exact reason one has to commit to holding systematic Small Cap Value (Avantis-style SCV) in their portfolio at all times if they want to harvest the premium. Because it is extremely hard to time that clustered outperformance

@PFOInvestor 1. $FMTM is much less mega-cap/tech overlap with SPMO. 6-mo lookback instead of 12mo-1mo. Equal-weight. Monthly rebalance.

2. $BSVO : Active manager diversifier for AVUV basically. Bridgeway similar philosophy but ~32% overlap with AVUV and also is even smaller cap / micro cap.

@PFOInvestor I have 50 US, 30 DM, 20 EM, and I aim ~30% momentum and ~70% value relative to each.

But Emerging Markets is the most challenging for me to allocate. I like 20% as an overweight, also $FRDM as a proxy equivalent of SPMO but in EM since it's 35% $TSM, Samsung, & SK Hynix.

@PFOInvestor I have tinkered lots, the best portfolio I can stick with is a global factor barbell of diversified value + momentum. I'm still in accumulation phase.

US:

$SPMO 10% $FMTM 10% $AVLV 10% $AVUV 10% $BSVO 10%

Developed ex-US:

$IDMO 10% $AVDV 20%

Emerging:

$FRDM 10% $AVES 10%

@PFOInvestor Actually R² of 97.7% on Avantis factor regression means it’s statistical proof that almost no idiosyncratic risk exists in this return stream. I agree DFA has a less than ideal go to market distribution strategy.

I’m also not a proponent for entirely SCV, I only hold 10%-20%