In significant Clare Capital news – Alex Gordon (@alx7000) has joined the ownership group of the firm and is now officially a Partner. Alex joined Clare Capital back in early-2018, soon after his return to New Zealand from working in the US for @PwC 1/4

Ken Griffin is brilliant because he updates his worldview when the facts change, even when it contradicts his past views.

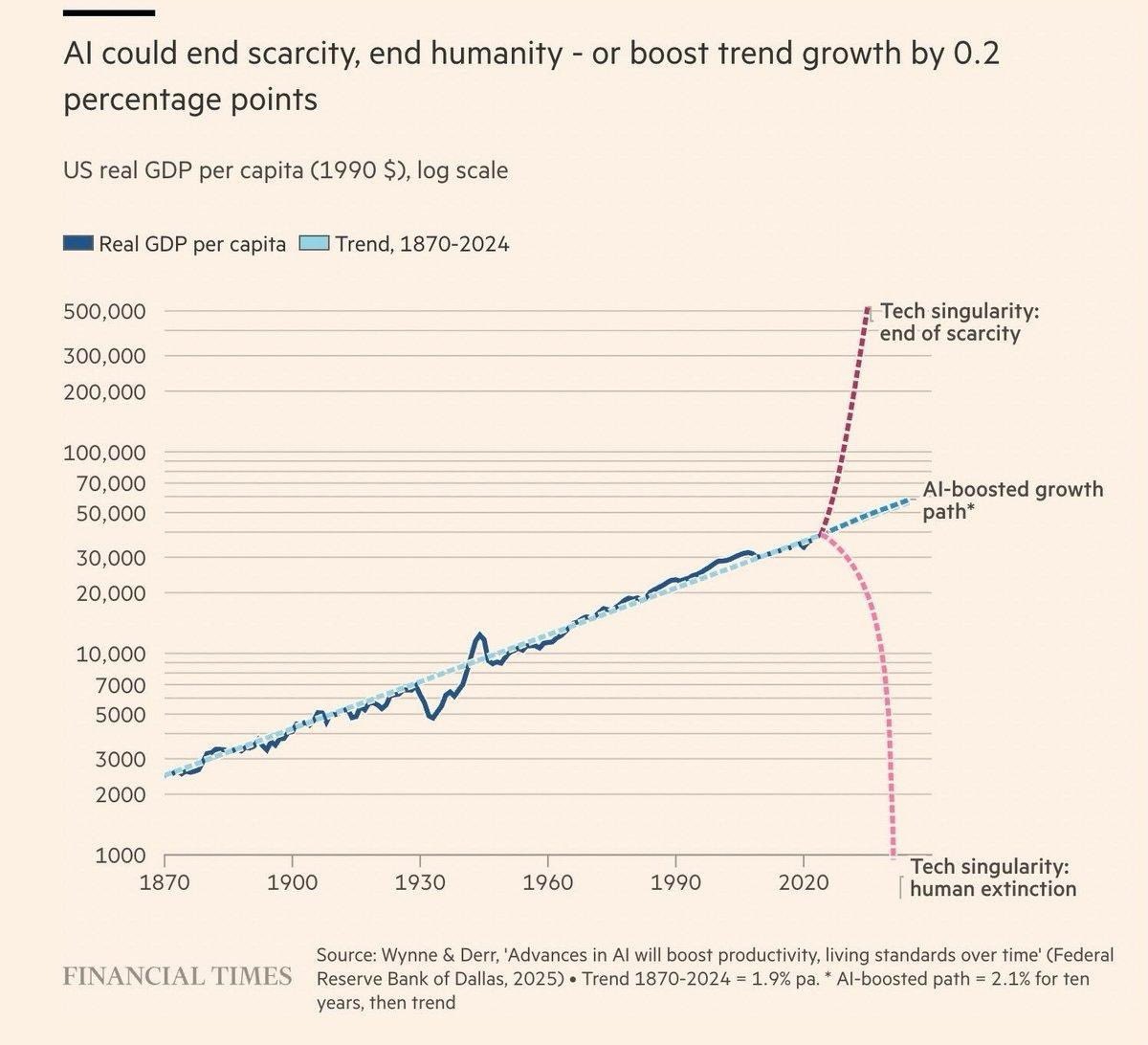

Most people still underestimate AI because humans struggle to intuitively grasp exponential progress. We experience linearity in daily life. Like I have seen a big dog, but never one the size of an airplane. I have seen tall trees, but never one reaching outer space.

AI does not scale linearly. It scales exponentially so the gap between today’s AI and AI from just a few months ago is already enormous.

Elon Musk avait dit un truc qui m'avait marqué sur l'allocation de ressources. En substance : passé un certain niveau de richesse, l'argent n'est plus de la consommation, c'est de l'allocation de capital.

Cette phrase change tout.

L'économie, dans le fond, c'est juste un problème d'allocation. Tu as des ressources finies et des usages infinis. Qui décide où va quoi ?

Imagine une cour de récré. 100 enfants, des paquets de cartes Pokémon distribués au hasard. Tu laisses faire. Très vite, un ordre émerge. Les bons joueurs accumulent les cartes rares, les collectionneurs trient, les négociateurs trouvent des deals. Personne n'a planifié. Et pourtant chaque carte finit dans les mains de celui qui en tire le plus de valeur. Le système maximise le bonheur total de la cour. C'est ça, la main invisible.

Maintenant fais entrer la maîtresse. Elle trouve ça injuste. Léo a 50 cartes, Tom en a 3. Elle confisque, redistribue, impose l'égalité. Trois effets immédiats. Les bons joueurs arrêtent de jouer, à quoi bon. Les mauvais n'ont plus de raison de progresser, ils auront leur part. Les échanges s'effondrent. La cour est égale, et morte. Elle a maximisé l'égalité, elle a détruit le bonheur.

Le problème de la maîtresse, c'est qu'elle ne peut pas avoir l'information que la cour avait collectivement. C'est le problème du calcul économique de Mises, formulé en 1920. L'URSS a essayé de le résoudre pendant 70 ans avec le Gosplan. Résultat : pénuries, queues, effondrement. Pas parce que les Soviétiques étaient bêtes, parce que le problème est mathématiquement insoluble en mode centralisé.

Quand Musk a 200 milliards, il ne les consomme pas, il les alloue. SpaceX, Starlink, Neuralink, xAI. Chaque dollar est un pari sur le futur. Et lui a un track record. PayPal, Tesla, SpaceX. Il a démontré qu'il sait identifier des problèmes immenses et y allouer des ressources avec un rendement spectaculaire.

L'État aussi a un track record. Hôpitaux qui s'effondrent, éducation qui décline, dette qui explose, services publics qui se dégradent malgré des budgets en hausse constante. Le marché identifie les bons allocateurs, la politique identifie les bons communicants.

Le profit n'est pas une finalité, c'est un signal. Il dit : tu as alloué des ressources rares vers un usage que les gens valorisent suffisamment pour payer. Plus le profit est gros, plus la création de valeur est grande. Quand Starlink est rentable, ça veut dire que des millions de gens dans des zones rurales ont enfin internet. Quand un ministère est en déficit, ça veut dire qu'il consomme plus qu'il ne produit. L'un crée, l'autre détruit, et on appelle ça redistribution.

Dans nos sociétés il y a deux catégories d'acteurs. Les entrepreneurs et les bureaucrates. L'entrepreneur prend un risque personnel pour identifier un problème, mobiliser des ressources, créer une solution. S'il se trompe il perd. S'il a raison, ses clients gagnent, ses employés gagnent, ses fournisseurs gagnent, l'État collecte des impôts. Il est la cellule de base du progrès humain.

Le bureaucrate ne prend aucun risque personnel. Son salaire est garanti. Au mieux il maintient une rente existante. Au pire il la détruit par excès de réglementation, mauvaise allocation forcée, incitations perverses qui découragent ceux qui produisent. Mais dans aucun cas il ne crée.

Regarde les 50 dernières années. iPhone, internet civil, SpaceX, Tesla, Google, Amazon, Stripe, mRNA, ChatGPT. Toutes des inventions privées, portées par des entrepreneurs, financées par du capital risque. Pas un seul ministère n'a inventé quoi que ce soit qui ait changé ta vie au quotidien.

La France est devenue le laboratoire mondial de la dérive bureaucratique. 57% du PIB en dépenses publiques, record absolu. Une administration tentaculaire, une fiscalité qui pénalise la création de richesse. Résultat : décrochage face aux États-Unis, à l'Allemagne, à la Suisse. Fuite des cerveaux. Désindustrialisation. Dette qui explose.

Et le pire c'est que la mauvaise allocation s'auto-renforce. Plus l'État prélève, moins les entrepreneurs créent. Moins ils créent, moins il y a de base fiscale. Plus l'État s'endette et taxe. Boucle de rétroaction négative parfaite. La maîtresse pense qu'elle aide, et chaque année la cour produit moins.

Dans nos sociétés, ce sont les entrepreneurs, toujours, qui font avancer la civilisation. Les bureaucrates au mieux maintiennent une rente, au pire la détruisent. Aucune société n'a jamais progressé en taxant ses créateurs pour subventionner ses gestionnaires.

La question n'est jamais qui a combien. C'est qui alloue le mieux la prochaine unité de ressource pour maximiser le futur de l'humanité. La réponse depuis 200 ans n'a jamais changé. Ce ne sont pas les fonctionnaires.

Was at the WH Correspondents dinner last night, a rare DC trip for me without a subpoena. On the positive side—was exciting, no one was killed, and ended early. I noted a new litmus for status among the gov’t elite—whether you were whisked away by secret service, or left to fend.

The 30 most in-demand startup secondary shares in Q1 '26 (per Setter Capital):

- Anthropic hits #1, bumping out SpaceX as the most desired shares on the list.

- Five of the top six companies are big IPO candidates in the next 12-18 months. They've been absorbing a lot of investor interest and capital over the past few quarters, it will be interesting to see what happens as they list.

- Prediction markets are still hot! Polymarket and Kalshi are two of the fastest risers. Anything crypto that hasn't rebranded as prediction markets continues softening.

- Replit and Shield AI are the two other fastest risers on the list. Lovable and Cursor also move up a few spots.

- ElevenLabs debuts at #9, tied (with Shield AI) for the highest ever. OpenEvidence and Saronic also make what I think is their first ever appearance on the list.

- Perplexity, Crusoe, and Figure both sliding significantly. Anecdotally feels like I haven't seen them discussed as much recently.

One notable data point, the average last round valuation of companies on the list was $120B (up 122% YoY). This compares to the average S&P 500 company valuation of $122B. Insane how big the private markets have gotten.

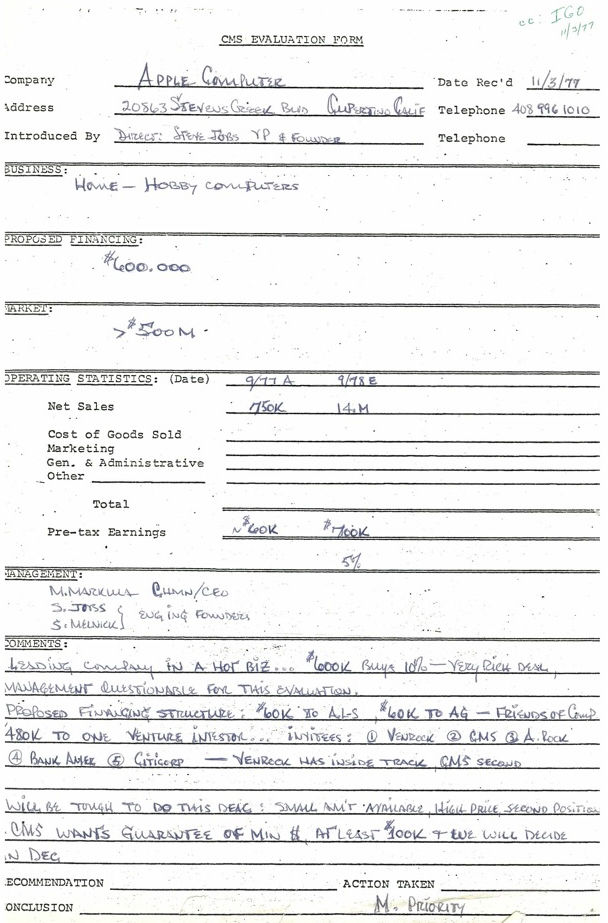

This is brilliant, on many levels. Apple's original deal memo from 1977. "$600k buys 10% - very rich deal". Current $APPL market cap $3.76 trillion. Handwritten with not a lot of detail at all. Very very cool.

In honor of 50 years of Apple, we're sharing - for the first time ever - Don Valentine's original 1977 memo for Sequoia's investment into Apple Computer. #Apple50

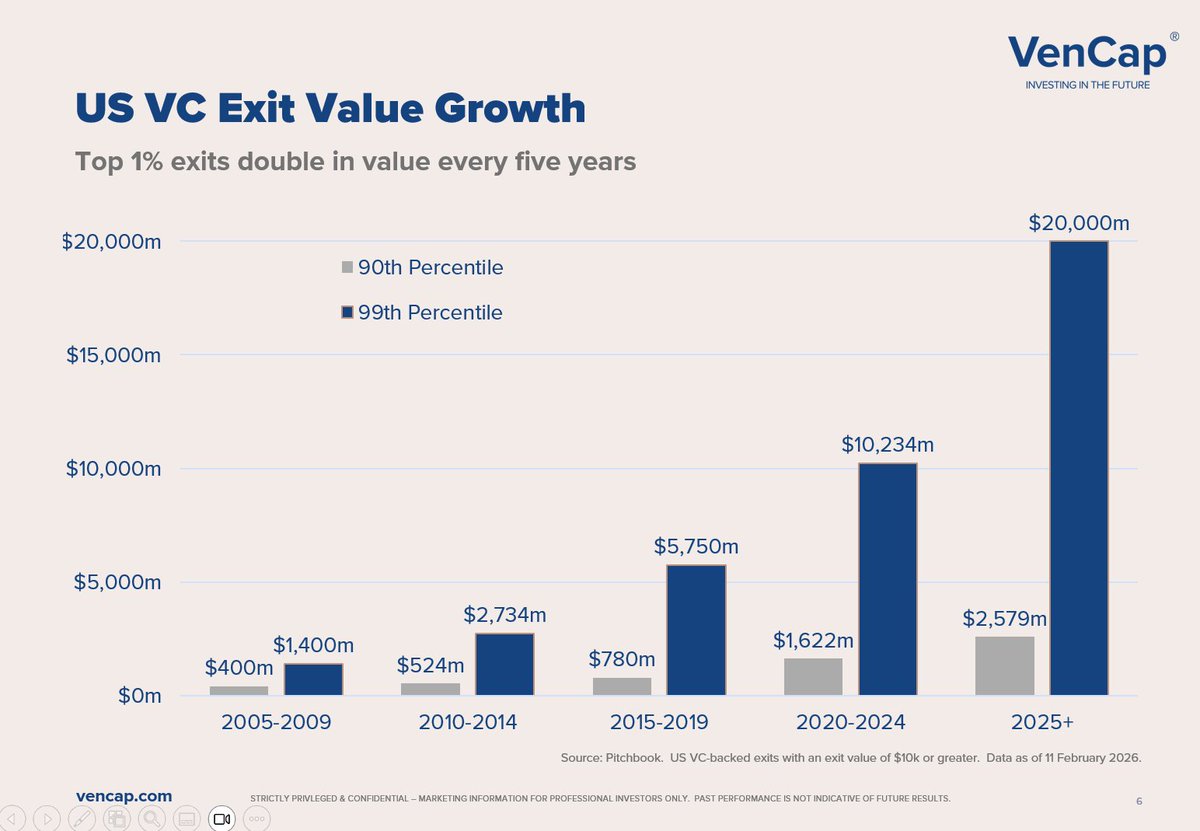

For the first time in venture history, three distinct channels share the liquidity burden roughly equally.

A decade ago, secondaries barely registered. They accounted for roughly 3% of exit value in 2015. Today they claim 31% : nearly $95b in the trailing twelve months.

The shift accelerated after 2021’s IPO bonanza. When public markets closed their doors in 2022, investors found alternative routes. Secondaries absorbed demand that would have flowed to traditional exits. When Goldman Sachs acquired Industry Ventures, the transaction signaled secondaries have arrived. Morgan Stanley followed with EquityZen, then Charles Schwab announced its acquisition of Forge Global. Wall Street recognized the structural change before most of venture did.

This matters for founders & investors. When IPOs dominated exits, fund models assumed a small number of public offerings would generate the bulk of returns.

Now liquidity arrives through multiple doors. A founder might sell secondary shares to patient capital while the company remains private. A GP might move positions through continuation vehicles. An LP might trade fund stakes on an increasingly liquid secondary market.

The 830 unicorns holding $3.9t in aggregate post-money valuation cannot all exit through IPOs. The math doesn’t work. At 2025’s pace of 48 VC-backed IPOs, clearing the unicorn backlog would take seventeen years. Secondaries provide a release valve that traditional exits cannot.

Companies like OpenAI have embraced this reality, running employee tender offers while voiding unauthorized secondary transfers. The largest private companies now manage their own liquidity programs rather than waiting for public markets.

Today, secondary liquidity concentrates in the top 20 names. SpaceX, Stripe, OpenAI. For the founder of company #50, the secondary market remains largely theoretical. For secondaries to succeed as a broad asset class, buyers must underwrite positions in companies without household recognition. As the market grows, this coverage gap becomes opportunity.

For LPs starved of distributions since 2022, the expansion of secondary channels offers hope. The $169b in cumulative negative net cash flows needs somewhere to go. More exit paths mean more opportunities to return capital.

When a Series B employee asks about liquidity today, the answer isn’t “wait for the IPO.” It’s “we’re planning a tender offer next year.”

A decade ago, secondaries were a footnote. Now they’re infrastructure. Liquidity flows where it can, not where tradition suggests it should.

https://t.co/vzmd8Nv1Vb

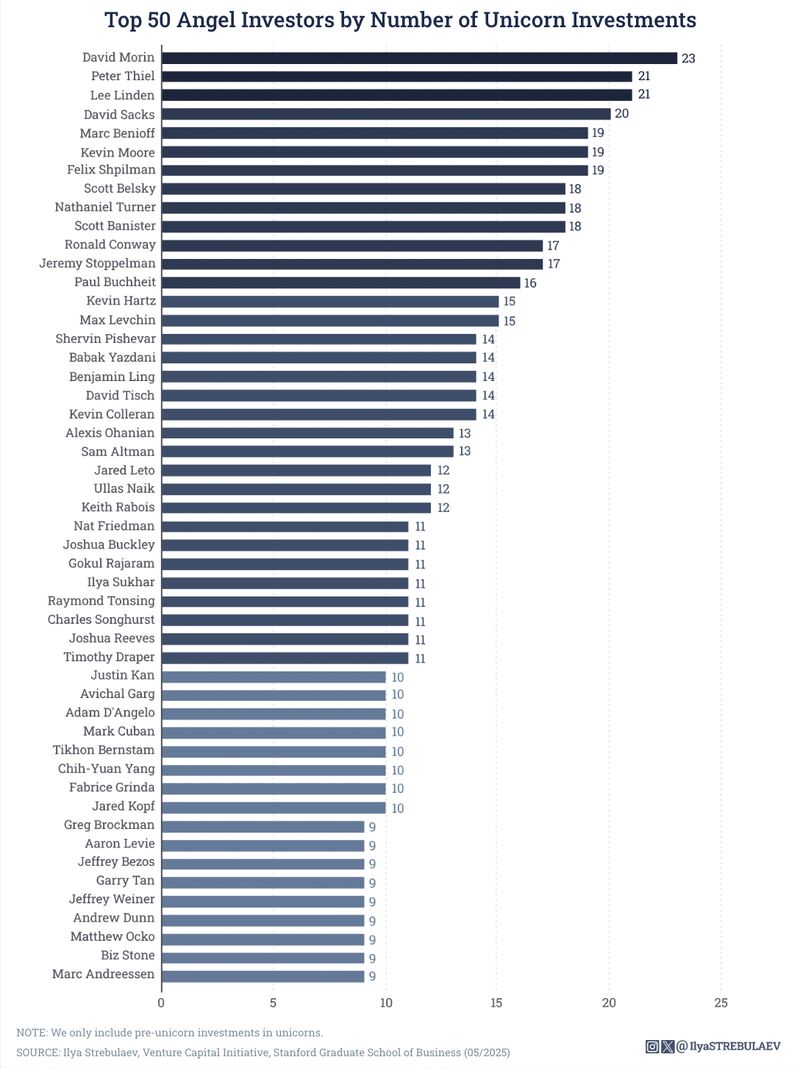

A Stanford professor analyzed 1,000's of angel investments to find out who's had the MOST unicorns.

The results are fascinating.

- David Morin tops the list with 23 unicorns

- Peter Thiel and Lee Linden follow with 21 each

- David Sacks at 20

- Marc Benioff at 19

A few things that stand out:

1) Almost every top angel was a founder or exec at a large tech company first. The clear signal here - they were mostly operators who earned their access.

2) Many co-invested together repeatedly. Thiel, Sacks, and Levchin all overlapped at PayPal and went on to back the same unicorns (Facebook, Airbnb, Palantir Technologies, SpaceX).

3) No women appear in the top 50. Sad.

4) The entry threshold to make this list is 9 unicorns (nuts!). The average unicorns across the top 50 is 13 (more nuts!).

I share this for folks to have inspiration to angel invest themselves!

There has NEVER been a better time - we are at a major tech inflection point.

If you're thinking about angel investing and forming angel syndicates, you should check out Verivend. Automated capital calls, one-click funding for co-investors, real-time visibility into who's in. Seamless software with a great team to hold your hand through it.

Try it yourself: https://t.co/qZ4U3OB2AY

Full credit to Ilya Strebulaev and his team at the Stanford for this research.

a16z: The Power Brokers

There is this story about Marc Andreessen that I think perfectly captures a16z.

in 2015, when New Yorker writer Tad Friend sat down to breakfast with Marc Andreessen while writing Tomorrow’s Advance Man.

Friend had just heard from a rival VC who wanted to get a word in: that a16z’s funds were so large, and ownership percentages so small1, that to get 5-10x aggregate returns across its first four funds, they’d need their aggregate portfolio to be worth $240-480 billion.

“When I started to check the math with Andreessen,” Friend writes, “He made a jerking-off motion and said ‘Blah-blah-blah. We have all the models—we’re elephant hunting, going after big game!’”

The aggregate portfolio did not end up being worth $240-480 billion. a16z Funds 1-4 had a total enterprise value of $853 billion at distribution or latest post-money valuation. Since distribution, Facebook alone has added $1.5 trillion in market cap.

Some form of this pattern keeps playing out: a16z makes a crazy bet on the future. Those in the know say it’s stupid. Wait some years. Turns out it’s not stupid!

Which is why, as a16z announces $15 billion in fresh funds, it is probably a mistake to dismiss them as greedy or stupid.

It's probably worth understanding just exactly what IT'S TRYING TO BUILD.

That's what I do in today's not boring deep dive:

a16z: The Power Brokers

Sequoia distributed over $50B while Roelof was the steward running Sequoia US since 2017

One of the first things @roelofbotha coached me on when I joined Sequoia was to look at each fund’s “write off rate”

Any fund with a write off rate below 40% wasn’t taking enough risk

Any time someone looks closely at airline economics, there is ALWAYS some crazy insight. Making money flying passengers is a hard business. You gotta be getting creative to turn a dime...

🧵 The wild story of NFDG: How two Silicon Valley legends built a $1.1B fund, 4X'd it in 2 years, then abandoned it all for Meta this week.

Nat Friedman (ex-GitHub CEO) + Daniel Gross (ex-YC partner) launched NFDG in 2023 with $1.1B focused on AI investments.

Their crown jewel? Safe Superintelligence (co-founded by Gross himself) - went from $5B to $30B valuation. Portfolio also included ElevenLabs, Granola, and Basis.

With only ~50% deployed, they hit 4X returns (~$550M → $2.2B portfolio value).

Advisory board: Stripe's John Collison + Paradigm's Matt Huang.

Then everything changed in ONE WEEK:

• June 29: Gross leaves Safe Superintelligence • This week: Zuckerberg announces Friedman leading Meta AI • Thursday: Friedman confirms he's started at Meta

• Sunday: Meta offers tender for up to 49% of fund

• Today: NFDG website is down

The twist? LPs can cash out at FULL NAV (not the typical discount). Meta gets the talent + deal flow without governance headaches.

This mirrors Garry Tan leaving Initialized for Y Combinator.

The lesson: In the Age of AI, even quadrupling $1B in 2 years may be less lucrative than being an operator in the revolution itself.

When the smartest VCs become operators, you know we're living through the most important tech transition of our lifetimes. 🚀

Today is the 30-year anniversary of my venture capital career.

My younger self would have found that hard to fathom.

Reflecting back, there was a simple algorithm embedded in my investment strategy that has made it all the more exciting and engaging over time — I look for startups that are unlike anything I have seen before, yet adjacent.

This novelty-seeking algorithm leads me and my partner Maryanna to explore numerous expanding frontiers of technology advancement and coincides with the innervation of ever more industries. The software-centric transformation we saw in automotive and aerospace is underway in manufacturing, construction, energy and agriculture. I know that I will be investing in new sectors five years from now that I could not name today, just as I would never imagined investing in Tesla or SpaceX twenty years ago. It’s a perpetual driver for lifelong learning.

But it arose from a simple boredom. At DFJ, we were the most active VC firm in Internet startups in 1995-1996, but by 1999, all of the B2C and B2B businesses were looking like variants on the same idea, sometimes to absurd extremes. I transitioned to deep tech semiconductor and materials science startups out of some instinct to seek less competitive domains and try something completely different.

I had not lost faith in the economic transformation that the Internet would still bring — far from it — but I exited the sector as all the companies I saw in 1999 looked the same. Interestingly, this had me exiting the Internet sector for new investments prior to the dot com crash. The same thing happened with cleantech investing, where we were one of the most active investors in the early years, but we stopped before the 2008 downturn. In both cases, the rush of fast followers and arbitrage-seeking opportunists preceded the crash. We did not predict the crash; we naturally moved on from when the novelty was gone.

From our simple rule, various emergent properties become evident on different time scales. In the near term, we gained portfolio diversification (obviously). In the medium term, we exited sectors when it was emotionally least likely (peak boom times) but prior to a major correction. It also lets us become early leaders in new sectors (Internet in 1995, then cleantech and syn bio, then AI in 2014) since we don’t have fixed sectors of focus, but we try to follow a thread of predicate technologies opening new opportunities.

But the most rewarding result has been the lesson learned over decades — that this investment strategy affords a lifetime of learning and dynamic adjustment to new areas of growth. Colleagues who have a fixed sector focus, in contrast, have a short-term competency dynamo (being the most experienced in a sector or niche), but ultimately, they seem unhappy 20 years later, retiring from venture regardless of their level of business success. Looking back over the past 30 years, my most important decision was to leave the competency trap of sticking with a single sector of focus.

Huge congrats @AucklandCity_FC, fantastic result. I (Mark Clare) played at the level @AucklandCity_FC do in the @NZ_Football pyramid back in the 1990s. A lot of proud @NZ_Football players, current and former, out here today.

Kalshi hired me to make the most unhinged NBA Finals commercial possible.

Network TV actually approved this GTA-style madness 🤣

High-dopamine Veo 3 videos will be the ad trend of 2025.

Here’s how I made it in just TWO DAYS 👇🏼 (Prompt included)

Really really good thread. We operate (and negotiate) in a small market (New Zealand and with international parties). There is a reason why our firm strategy is "long-term games with long-term people". We are paid to get outcomes, but we typically will see counterparties again...

Some notes on Negotiations

1/ When you finish any complex deal you will feel fatigued and worn out. It sometimes feels hard to celebrate. The best deals feel this way. Complex negotiations require compromises. When both (or all) parties make concessions nobody feels great. Everybody felt like they gave more than they wanted. And all wish the other party would have folded easier. That’s the definition of a good negotiation