Physical bottlenecks need capital. Capital needs optionality. When China risk prices into Hong Kong primary markets, listing venue optionality matters. Nubank chose ADGM in April. That is the redirect to track.

The real story is not another Apple supplier listing.

Luxshare is seeking up to $3.1 billion from a Hong Kong listing, according to Bloomberg. The signal is that hardware supply-chain capital still has a bid, even as investors are becoming more selective across China-linked assets.

That matters because AI and consumer electronics both need physical capacity. The market talks software multiples. The supply chain needs funding, redundancy, and geopolitical optionality.

Hong Kong is the key test. If investors absorb a large Apple-supplier deal, it says capital markets remain open for strategic hardware names despite China risk. If demand is soft, it confirms the discount is moving from macro narrative into primary-market pricing.

Watch order book quality and aftermarket performance, not just the headline raise.

AI may be digital at the interface. The bottlenecks are still physical.

Phantom surplus thesis is sound. Strait passage remains conditional and severely restricted. UAE's Fujairah hub and ADCOP pipeline (1.8 mbpd) operated throughout the disruption. Measured infrastructure performance, not forward guidance.

Algorithms are aggressively shorting Brent crude because they cannot distinguish between new supply and evacuated inventory.

At 73.51, $BRENT has collapsed over 23 points below its 50-day moving average.

The entire plunge is built on a mechanical data illusion.

The 60-day ceasefire unlocked the Strait of Hormuz, triggering a massive outflow of tankers.

Paper markets see the headline outflow volume, assume a structural supply surge, and blindly hit the bid.

They are completely misreading the physical reality of the basin.

Those are STRANDED vessels finally being allowed to leave the chokepoint.

Insurance risk means operators are refusing to send replacement ships back IN.

This is the exact setup we saw in Q4 2018 when sanctions waivers tricked the paper market into pricing a PHANTOM SURPLUS.

Momentum funds front-ran the temporary flow, physical barrels quietly vanished by January, and the shorts were systematically dismantled.

The identical dislocation is playing out in real time.

Iran struck a commercial vessel near Oman this week, proving the ceasefire is purely decorative.

Meanwhile, the US strategic reserve is sitting at a four-decade low, offering zero buffer for a shock.

Once the backlog of stranded tankers finishes clearing, the total collapse in incoming cargo will finally hit the global data feeds.

The physical market always collects from the paper market in the end.

Spot-on 2008 analogy. The institutional fix: sovereign anchor capital absorbing first-loss on tariff risk so project economics don't crater at cycle turns. ADFD's $1B water platform is structured on this.

Panic-buying 3-year solar paybacks while Brent crude quietly collapses 38% is a very special kind of macro comedy.

It is genuinely amusing to watch entire sovereign populations trade exactly like emotional retail.

Brent has already puked from $118 down to a $73.47 handle.

The geopolitical supply shock is actively unwinding and the institutional bid is gone.

But because local electricity grids lag the commodity tape, households in the Philippines and Pakistan are panic-financing hundreds of millions in Chinese solar panels based on outdated utility bills.

This is the exact setup we traded in July 2008.

Back then, airlines panicked at $147 oil and locked in massive, multi-year fuel hedges right at the absolute peak.

Six months later, crude was in the $30s and those peak-panic hedges bankrupted half the sector.

Today, heavily indebted EM consumers are financing long-duration rooftop hardware based on peak-crisis power models.

The moment local utility rates finally adjust downward to match the new $73 crude reality, those 'three year' solar payback models instantly blow out to a decade.

The physical hardware depreciates, the utility savings vanish, but the installation debt remains.

You never lock in long-duration illiquid infrastructure at the tail end of a cyclical commodity squeeze.

Emerging markets are quite literally hedging the top.

Physical constraint acknowledged. Hormuz restricted, variable no allocator controls. What I track: Mubadala published AED 1.4T AUM results mid-conflict. Data, not narrative.

Nuclear power in Europe is costly and slow. Small Modular Reactors (SMRs) offer a promising alternative, but face regulatory challenges. #SMR#NuclearEnergy

@JTheretohelp1@BudaghyanArthur IPO timing signal has held. Where capital rotates post-correction matters. ADGM issuing VARA standards during active conflict demonstrates the regulatory continuity that captures reallocation flows.

@DropSiteNews September 30 is a data point. I track institutional execution under stress, not security deadlines. The credibility gap between states that maintained operational continuity and those that didn't is what drove post-conflict reallocation after 2020.

@S_Mikhailovich Fair question. Classic EM defaults come from currency mismatch: borrow in USD, earn in local. China's debt is RMB-denominated and domestically held. Completely different risk profile.

The 'trade agreements with developing economies' recommendation overlooks existing infrastructure. UAE free zones already route commercial flows across MENAT and South Asia under legal frameworks EU allocators recognise. No diplomatic timelines required.

🇩🇪🇨🇳 China has exploited Germany’s industrial weakening.

Since 2018, Germany’s net exports have made a cumulative negative contribution of around 4% of GDP to growth

Since 2018, China has moved in the opposite direction, with its global export share rising from 13.1% to 16.3% and its trade surplus reaching a record $1.189tn in 2025.

Germany’s trade deficit with China hit a record €87bn in 2025.

The EU can help by opening new markets through trade agreements with developing economies.

But Germany also needs deep pro-growth reforms and productive public investment.

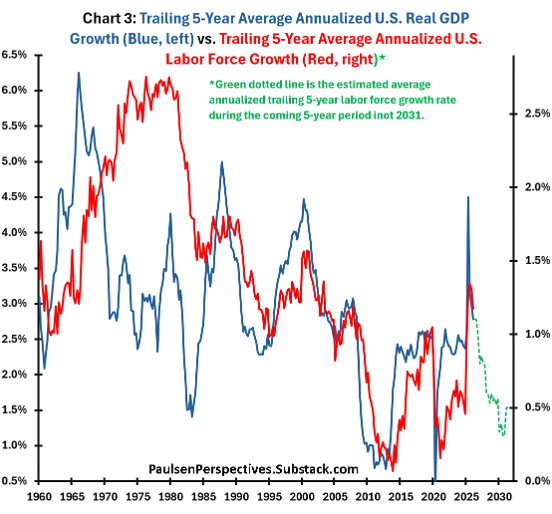

Paulsen's structural deceleration thesis aligns with CBO data. When domestic labor force growth heads toward 0.5%, I evaluate jurisdictions with different fundamentals. UAE's demographics and regulatory maturity make it a natural complement in EM allocations.

Despite exciting innovations, US real GDP growth unfortunately appears poised to return to the "Demographic Dungeon" in the coming years as labor force growth normalizes near post-war lows. See my full report on implications at https://t.co/cmZvbGqspf

Not a timing signal but a valuation reality. Patient capital should look at where earnings yield is expanding. UAE non-oil sectors offer that with $2.5T in sovereign capital depth behind them.

S&P Earnings Yield plumbing new lows for 2026. The other times we were in this vicinity:

- 1929

- 2000

While not meant to be used as a timing tool, this chart does a good job at reflecting overvaluation vs. undervaluation when viewed in light of yields.

Source: Bloomberg

A U.S.-sanctioned tanker is falsely broadcasting a Norwegian flag. This is the second example of sanctioned Iranian tonnage to claim a European register in the past week, the other an LPG carrier.

A bold deceptive shipping practice, carried out in plain sight of the U.S. and European operators closely scrutinizing every movement through Hormuz. It echoes the sequestered Iranian VLCCs that sailed from Chabahar 48 hours before the MoU was signed, breaking the blockade.

The message is a defiant one, signaling that Iran will continue its energy exports, irrespective of international maritime rules and regulations.

One of the biggest changes with the Fed is how much confidence you can have in your views.

@LHMacro argues that a less transparent Fed opens the door to a much wider range of outcomes, making conviction trades harder to hold.

"If the Fed isn't going to guide you ahead... I'm going to be a little bit quicker to cut risk."

Hormuz remains conditional and severely restricted. For allocation decisions, I track what the UAE controls domestically: infrastructure redundancy, regulatory continuity, financial system resilience.

Before the US-Israeli strikes, Iran had an estimated 5,000-6,000 sea mines, with some analysts believing Tehran has retained 80-90 per cent of its small boats and minelaying vessels.

https://t.co/O0iTBu3GGV

@KobeissiLetter 110 bps carry changes the math. When US financing costs double in two months, allocators evaluate complementary structures. UAE's zero income tax and 9% corporate rate rewrite the hurdle rate calculus.

@VladBastion Physical AI deployment velocity matters more than CAGR projections. Gulf sovereigns are scaling smart infrastructure faster than US procurement cycles allow. That could pull Ouster's adoption timeline forward.

@IMFinMENA@AndresVelasco@LSEnews Velasco's framing is timely. The EM principle I'd add: institutional continuity through acute disruption. ADGM kept processing licences through this conflict. That variable was underweighted.