This map shows the infrastructure Britain could have, without spending an extra penny, if our infrastructure cost as much as it does in Europe.

NEW RESEARCH from @BritishProgress & @BritainRemade finds that *the UK faces an investment cost premium of 65%* compared to other OECD countries, and therefore delivers less infrastructure for similar levels of investment.

Want better rail in Manchester? A tram for Leeds? More electrified railways? Better road upgrades?

All without raising taxes?

Then Britain has to fix the cost of building.

We look at case studies including the Edinburgh tram, Lower Thames Crossing and HS2, and find that, for the same amount of money, we get less back. The reasons are:

👑 Centralisation of power prevents mayoral & local authorities from funding & building new projects

🏛️ A lack of state capacity, particularly in procurement and engineering, means more gets outsourced

🏗️ Planning dysfunction adds uncertainty, delays and costs to new projects

⚖️ Our legal & regulatory system can add inappropriate requirements to projects, making investments more costly and even unviable.

In a weird way, this is good news. Why? Because it means that the UK can dramatically improve its infrastructure, and the effectiveness of our investment, without spending an extra penny. At a time of constrained public finances, this is welcome.

However, it is also a warning. Unless we fix Britain’s investment premium, every extra £ spent on transport, energy or other infrastructure will deliver less than it could.

Read the full paper from me, @pdmsero, @Sam_Dumitriu & @Michael_J_Hil here: https://t.co/2yjj1HNt8k

Scroll down for key graphs and charts…

Another absurd intervention by Burnham. The triple lock should never have been in Labour’s manifesto and ought to be broken. And if pensioners receive taxable income in excess of the personal allowance, they should of course pay tax on it. Why load the burden on younger people?

@BenRamanauskas Again, I didn’t say Polanski was right. Merely pointing out the DM is selective about who it thinks gilt markets should enforce budget constraints on.

@BenRamanauskas No - I was pointing out the hypocrisy of the Daily Mail, who have gone from complaining about woke gilt traders to cheerleading the discipline they provide.

@techie_fan@Cern_IXXI@Notnow1982@PhillipsPOBrien Relative to GDP Ireland is near the bottom of the support table. Sorry but Ireland is one of the biggest free-riders in the world when it comes to bilateral aid and communal defence.

1. In the long run, business rates depress rents. A business rate cut will increase rent. The benefit will go to landlords.

2. A business rate cut for small business is bad policy. It distorts decisions, will incentivise small businesses to stay small, and -> avoidance/evasion

UK tax has gone up significantly over the last 25 years

But the tax paid by the average UK worker has not

This apparent miracle was achieved by taxing “other people”: higher earners, capital, property, banks, etc

The strategy has run out of road

A 🧵 on what happens next.

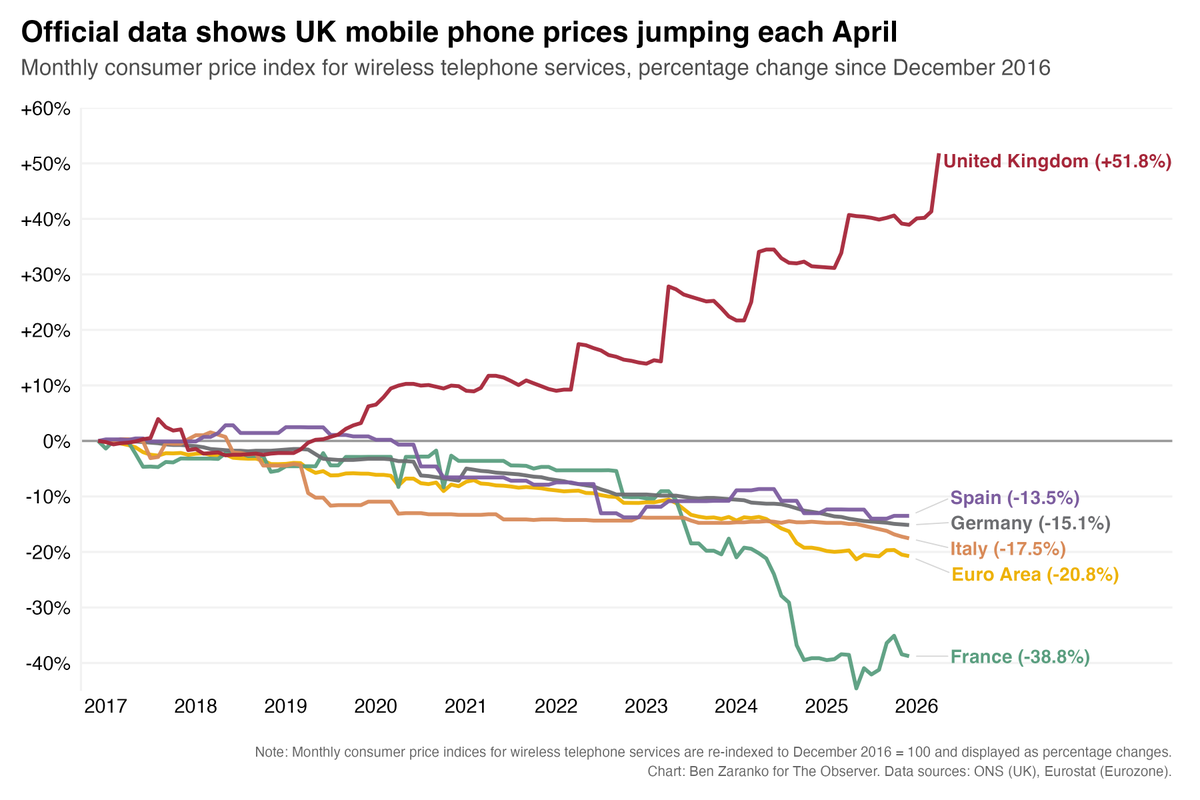

This chart is bonkers.

I think there's two possible explanations for why the UK runs so far ahead of other European countries – neither of them good. And the annual April jump speaks to a wider issue. For more detail, see my column in this weekend's Observer (link below).

"Challenging Inequalities". Do buy it! @williamnhutton has just called it "one of the great works of social science this century". It is also according to @matthewsyed a "wonderfully clear and readable little book". Paul Collier: "a superb critique of British public policy"

This is of course why Starmer’s failure (and Sunak’s before him) to deliver modest welfare reform has been such a disaster. Johnson and May’s Brexit and Cameron’s triple lock put the UK on an unsustainable fiscal path but subsequent PM’s have failed to correct this.

#r4today

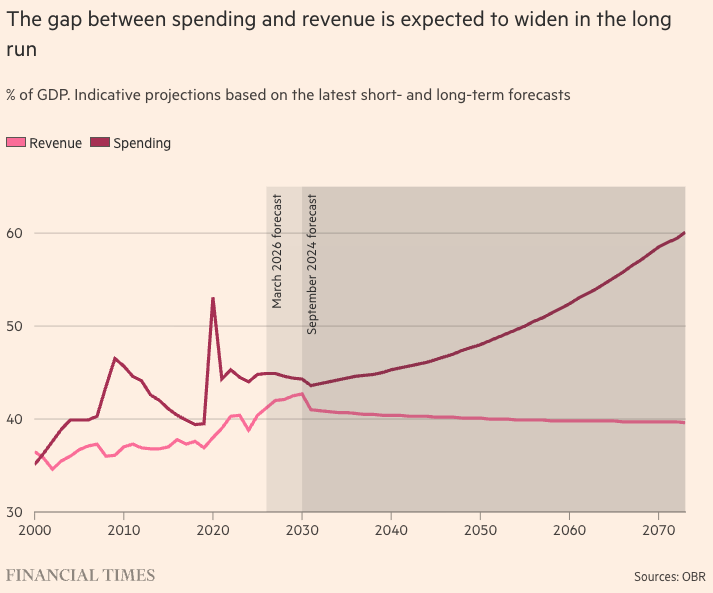

Anyone who thinks there is room for a new Chancellor to spend more liberally should take a long hard look at this graph.

Britain's borrowing costs are soaring because spending is projected to far outpace revenue from 2030.

A few implications:

1. The triple lock will have to go. An ageing population + inflation means we can't afford it.

2. Bond markets will not respond well to a new government (Labour or otherwise) that tries to suddenly boost spending, cut taxes or damage growth.

3. The only long run solution is growth. Even just 1% more per year would make a huge difference to this graph, raising revenue projections substantially, and reducing fiscal liabilities in a few key areas.

Article from @tejparikh90@FinancialTimes https://t.co/Yz3yCyp8LG

@PeterMatza@CeeMacBee What makes you say that? Peter, you give the impression of someone who doesn’t actually know what econometrics is? I am still waiting for the list of econometrics papers she has authored?