Much better EMIB-T visualization. Will tell you a lot about how $INTC advanced packaging works.

If you read my report on EMIB, and then refer to the visualizer, you could yourself figure out the opportunity for Intel right now.

Link: https://t.co/kKuOi1fyh1

$nbis, $meta, $crwv, $orcl Mstanley out tonight w/ clarifying comments re: bb report. Tldr: If meta does sell compute, it will be as a bare-metal offering of spare internal 1P capacity (not 3rd party-leased) to serve as an "eps bridge" while they develop their core products.

What's key is ms doesn't believe meta can or wants to compete as a full-service stack, since their models are limited & they don't have the expertise, software, or salespeople to service specialized, high-touch enterprise inference markets (precisely the markets $nbis, for instance, seeks to serve). MS suggests meta is not contractually-allowed to resell any of their 3P leased raw silicon from nbis, crwv, orcl, etc., Believes they will save their cutting-edge contracted capacity (e.g., the nebius 12B Vera Rubin order), for internal use.

Net/net: If meta does enter the compute market it will be as a stopgap, and in the bare-metal, older chip market. A minor supply addition, at best; least threatening, arguably, to nebius of all the neo's; and all this only assuming a backdrop where the compute supply were to materially loosen.

KOSPI is in a choppy uptrend as well and just hit the lower boundary of the uprising channel. Lots of the weakness recently is due to the fund flow(the negative narrative is not the root cause):

1. Chinese fund selling to buy CXMT IPO

2. Other foreign funds selling to buy SK Hynix ADR in US

3. KR’s pension funds keeps selling to rebalance.

This is an important channel to defend. Let's wait and see.

They don't need permits to build substation, so they will build it and get grid power: https://t.co/OOwCZ9rHci "Birmingham city officials concluded that Nebius did not need the city’s approval to build a switching station and a substation to distribute power to a 300-megawatt data center at the Oxmoor Corporate Park, dubbed BHM01. Neither meets the city’s definition of a “utility substation,” according to City Attorney Nicole King."

$NBIS: Multiple people have asked me recently about buying $NBIS at $200+. They have, obviously, read the multiple bull cases, but from me, they are looking to get an alternative point of view for balance. I'll layout the risks in a public post for transparency.

In all fairness, if you are reading this for the first time and want the bull case, these accounts have done a great job laying out the $NBIS bull case:

1. @daniel_koss

2. @itsalasdairmann

3. @MB_Hogan

4. @babyfolio

5. @EndicottInvests

I don't own any $NBIS but some $IREN whales do own a fair amount of $NBIS and have done well with $IREN in 2025 and $NBIS in 2026.

There's no doubt that in H1 2026, $NBIS has had the best stock performance among publicly traded Neoclouds, with concrete deliverables in 399m Q1 revenue on 82% QoQ growth (1) and 40% downpayment from MSFT (2). At 11-15m/MW-yr, 399m quarterly revenue equates to 106MW-145MW of build out depending on blend GPUs and IaaS-PaaS-SaaS. This buildout is still early and not bottlenecked by power. However, hot stock performance for one time frame doesn't determine the whole trajectory; an example is $SMCI vs $DELL and $HPE. What will de-risk $NBIS for me is completion of their Vineland, NJ datacenter in 2026 or early 2027.

I will go over two main topics: Power and Software.

1. Power

Nebius has more than 4GWs of secured power with a strategy of diversifying between colocation and self-owned over many sites to manage risk. Nebius refers to secure and contracted power as either PPA from the energy producer or interconnection agreement (IA) which is final approval needed for grid buildout. Nebius' BTM sites like Vineland, NJ do not need IA and also bypass the grid buildout time.

Not all Nebius sites are equal so I'll go through starting from the ones that are the best in terms of time to power without delays.

Mäntsälä

Nebius's Mäntsälä site is 75MW of active power (11). This datacenter from Nebius's Yandex days is grid connected, greenfield, and self-owned (11). The Finland datacenter boast a PUE of 1.13 (11) comparable with IREN's Prince George datacenter at 1.1 PUE (12), both taking advantage of the climate.

Iceland

10MW of colocation lock and loaded (26).

Kansas City, Missouri

5GW of Colocation from Patmos lock and loaded, potential expansion to 40MW (29).

Israel

Israel my favorite $NBIS site in terms of guaranteed path to power with no delays. Nebius signed a datacenter lease for 80MW in Modi'in in the Masmiyya and Beit Shemesh districts with expansion to 286MW (23). Some of the clusters will be used for Israel's national super computer (24) and Beit Shemesh is an important military district, previously target of Iran's military strikes but now de-risked as the Iran Wwar has ended (25).

Independence

Of Nebius's large sites in North America, I like the potential of Independence the best. It cleverly uses reopening an old power plant built in 1958 and closed in 2020 near by to provide power. The natural gas-fueled Blue Valley Power Plant is very close by Nebius' designated site so grid buildout requires less high voltage components.

This is similar to Elon's colossus site which uses a mix of reopened power plant and importing gas turbines from deconstruction power plants from abroad (22).

UK

Ark Data Centres colocation, 16MW agreed with expansion plans to 52MW (30).

Vineland

Nebius current active buildout is a Colcoation site in Vineland, NJ with "Nebius, becoming a DataOne tenant for the next 10 years" (7). From Nebius' 20-F at the end of 2024 (9) and F-3 mid 2025 (10), "The New Jersey site is a phased development scalable up to 300 MW, with initial capacity expected to be available in the second half of 2025." However, we are entering into the second half of 2026 and Vineland has just switched out their power supply from Bergen cruiseship engines with Skylea carbon capture (13) to $BE fuel cells (14).

Nebius is paying 2.6B for 328MW of $BE Fuel Cells as a Service for 10 years with 250MW of guaranteed capacity and 78MW of installed system capacity (14). Like all BTM power sources, redundancy factor is needed which is the 78MW and only 250MW goes to the GPU and Aux Loads. This is 10.4m/MW for 10 years or 1.04m/MW-yr and doesn't even include the natural gas (17). To put in perspective, the entire datacenter cost buildout 15m/MW for 20 years with 3-4m retorfit cost if a site has grid connected power.

There is a concern whether or not Nebius will get the $BE fuel cells this year as they are sold out for 2026 (16). This is not a concern and the fuel cells themselves will be delivered this year because Oracle encountered a delay for their NM site and $BE is rerouting the fuel cells from Oracle to Nebius (15).

As stated in the 6-K, Nebius may provide "alternative capacity" (31) for it's Microsoft contract while Vineland is under construction. This will work for several tranches but will not work forever as Vineland is 3.48B ARR and almost half of $NBIS 7-9B 2026 ARR guidance.

Lappeenranta

Nebius has labled Lappeenranta, Finland as a 310MW greenfield site. Lappeenaranta is a greenfield site belonging to Polarnode and Nebius is renting it as Colocation (18). @TheUglyBuckling has full details on this site: https://t.co/nt73cfjvUY

Bethune, France

@InvestNorthwise does a good job of covering this one here: https://t.co/UAedUzMXM4.

Birmingham, Alabama

300MW of brownfield development that got permitted right before the city passed it's datacenter moratorium. This site has broken ground and has a decent chance to completion as a BTM site despite lawsuit from two homeowners who are within 1000ft of the datacenter (27).

The major blocker from Birmingham succeeding as a grid connected site is that the permit to build a substation and switching station was denied and final (28). The workaround to this is obviously just like Vineland $BE fuel cells. This is why I see Vineland, NJ as a pivotal site for Nebius as alot of their sites' contingency plan is $BE fuel cells so Vineland is the litmus test for their ability to execute on $BE fuel cell BTM sites.

Pennsylvania

Nebius most recent site announcement is their 1.2GW Pennsylvania site which they revealed to Analyst is Pennsylvania is grid connected (3). By end of 2027, Pennsylvania will have 250MW-350MW with each year adding 300MW (5). From cross referencing total capacity, power ramp, and acreage of site, Nebius's Pennsylvania site is most likely Lower Mount Bethel Technology Center” in Northampton County (6). If so, Nebius has secured the power purchase agreement and still needs to get the interconnection agreement which can be delayed based on time to build transmission, substations, and grid. Regulations and local anti-datacenter activism is dealt with in parallel to optimize time to power.

Good news is PJM is reforming it's interconnection queue to be first-come first-serve (19). Bad news is despite that, PJM is one of the most congested buildouts from a supply chain perspective and "PJM Interconnection data – but the biggest delays are no longer occurring within the interconnection queue" (20).

"The bottleneck has shifted downstream. Transmission buildouts, substation capacity, and strained supply chains are now the primary obstacles to energizing projects. According to PJM, projects spent an average of more than three years reaching an interconnection service agreement, and another four years waiting to come online after approval" (20).

2. Software

A large part of Nebius market cap is attributed software. Although Nebius is way ahead of IREN in software, I believe market is rewarding Nebius by using Databricks as a valuation comparison but this is misconstrued.

The similarities the market sees is that both companies have a full inference stack with Databrick provides LLM inference through API by the token through Databricks Mosaic (32, 33) and with Databricks currently at 6.9B ARR (34) and Nebius targetting a 7B-9B ARR by EOY. The big mistake here is that NBIS revenue is for SaaS plus infrastructure while Databricks is SaaS without infrastructure.

Databricks does not need to own GPUs, power contracts, or data centers to recognize their revenue. Databrick's 74% gross margin (34) is even better than Anthropic's 80% gross margins because Databricks doesn't have to pay for model training like Nebius because it uses Open Source Model. At the same time it's compute cost is like Anthropic's: accounted for in the gross margins and not subtract off afterwards as depreciation.

Of course Databricks does more than Managed Inference for Open Source and has Lakehouse as well. Databricks is also one step ahead with Managed Agentic Agents (36).

Competitors

There are way more Neoclouds than finX is aware of because many successful companies stay private nowadays longer and the field of AI Platforms is still young. Notable competitors are hyperscalers, Cerebras, FireworksAI, SambaNova, FireworksAI, TogetherAI, Baseten, Modal, Databricks, Coreweave and weaker competitors like Cloudflare, Novita, DeepInfra, Parasail, Scaleway, Lambda, Mistral, Cohere, AI21 Labs, OctoAI.

Every Neocloud likes to cherry-pick benchmarks for best inference speeds that make them look the best but we should select open source (OS) model first and then look at results. The models we select are:

1. GLM-5.2 Max - the most powerful OS model today.

2. DeepSeek V4 Pro - the most deployed in production usage near-frontier OS model model today.

3. gpt-oss-120b - the OS model with most benchmark submissions

The results are pictured in the same order as I listed them above and Nebius is below average.

https://t.co/TrbDvJruao

https://t.co/tDkyc6nGPq

https://t.co/CPeujKNpTP

Granted Nebius acquired EigenAI and Clarifai which look good on certain 1 dimensional benchmarks. These startups are optimizing latency benchmarks for buyouts and not real economics. For startups not serving large number of customers, they can juice their benchmark numbers by reducing batch size, over provisioning GPUs, keep KV cache longer in HBM, increase decoding budget, tune for latency over GPU utilization.

Moving Fast

Fireworks came out the other day with Managed Model Tuning of Open Source Models called Fireworks RFT (38). Basically for those familiar with Nebius lingo, it's Token Factory but Model Factory.

I expect Nebius to follow suit in 6-12 months. But by that time, other AI Platforms Databricks, Coreweave will have already released through developer documentation instead of marketing fanfare.

Obviously then there are obvious risks of OpenAI and Anthropic dominating and SpaceX DCs which might be cost competitive with $BE fuel cell sites.

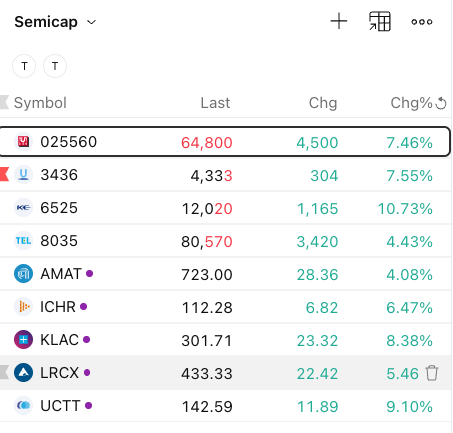

just another boring up day.

So regret that I bought the same size of memory vs memory semicap names....should be 1:2 or 1:3

The thesis of semicap was already well explained in

https://t.co/PoHZ2NdJAm

and https://t.co/LOc6Z4kMI3 on June 11.

Just some of the more interesting news I came across recently:

1. MS: Revised China humanoid shipments to reach 50,000 in 2026 from 14,000u and 28,000u earlier this year.

2. MS: Probe cards and test sockets likely to be priced hike (precious metal hikes + severe shortage of test pin capacity)

3. Capacitor price hikes: MLCC, aluminum electrolytic, tantalum, polymer aluminum, film, and super capacitors from Yageo.

4. $META Vistara architecture: Older DDR4 Memory with CXL as memory expansion

5. OpenAI achieved inference optimization breakthrough that halves costs and reduces GPU requirements.

6. LTAs are being signed with MLCC after Samsung signed LTA with US big tech customer

7. Grid power bottlenecks triggered 5x increase ($25B) in Brookfield's financing for $BE fuel cells.

8. Taiwan's chip packaging and testing supply chain includes major OSAT providers such as $ASX, Powertech, Winstek Semiconductor, Chipbond, ChipMOS, and ShunSin.

Dedicated testing companies include KYEC, Ardentec, and Sigurd Microelectronics, while testing interface suppliers include WinWay, MPI, Keystone Microtech, Chunghwa Precision, and Hermes Testing Solutions.

Leadframe makers include Jih Lin Tech, SDI, and CWTC, while major IC substrate suppliers include Unimicron, Kinsus, Nan Ya PCB, and Zhen Ding Tech. (Digitimes)

- Taiwan-based OSAT providers are raising prices

- Memory and IC packaging and testing capacity have both become bottlenecks in the semiconductor supply chain