The semiconductor thesis may be broken, proceed with caution.

Based on a Semianalysis report.

> CPO and 800V will be delayed till 2028/29 a huge pushback in the system.

> 400V will ramp as planned.

> NPO potentially accelerating.

This is a big break in the thesis if true. They specifically name caution in investing in companies such as $LITE, $HIMX $NVTS $WOLF

Best 400V exposure

> $APH

> $VRT

> $MX

> $MPWR

Best NPO

> $SMTC

> $MTSI

> $AVGO

> $AAOI

Copper

> $CRDO

Interconnects you say?

IMO you only need two stocks: $CRDO and $AAOI.

$CRDO = king of the <30m layer

$AAOI = king of the >30m layer

That’s it. Full coverage.

A little list of interesting stocks that are getting hammered today:

$XFAB -15% and getting back to the pre @aleabitoreddit pump

$TRT -8% and down 55% from the highs. One of FinX favorites right now

$DGXX -7% one of the best dips out there imo

$IREN -8% we all know it, and it's one of $NVDA's favorite neo-clouds. Read @Agrippa_Inv reports if interested

$LPK -10% and not so far from buying territory

$DELL -6% Trump's favorite stock

$PENG -7% FinX pumped it too hard

$ALKAL -7% I seem to have sold at the exact top

$HIMX -11% far from a buying point

$SOI -10% same as above

$ADTN -9% another FinX favorite

$RPI -9% too high

$4X0 -6% and one of my worst calls, the stock just goes down but I think it's a great opportunity

$QCOM -8% Jensen's pump wasn't enough

Let me know if you found some good dips to buy today

2 politicians just bought a AI stock $LITE supplying data centre buildouts

- Cisneros oversees military intelligence; Lumentum supplies lasers to the U.S. military.

- Gottheimer supports AI chip export controls that affect Lumentum.

These 2 also bought $MU early… something’s cooking

Quietly, $SIVE just took a massive step forward.

Sivers Semiconductors just delivered the kind of real-world validation that turns patience into conviction.

They’ve locked in an $8.2 million production order from https://t.co/A7mlfHMHLp for advanced Ka-band beamforming ICs, real volume manufacturing through 2027 for next-gen tactical terminals that seamlessly handle LEO, MEO, and GEO orbits at once. This isn’t another prototype deal. This is the ramp kicking off!

Even better: https://t.co/A7mlfHMHLp is being acquired by York Space Systems ($YSS), a major US defense prime. Sivers’ chips are now embedding straight into critical national security programs — resilient multi-orbit comms that the US Army, Navy, and allies actually need.

One terminal can pack hundreds to over a thousand of these high-value chips. As volumes scale, this relationship alone can deliver tens of millions in annual revenue. With defense budgets surging, constellations exploding, and unbreakable connectivity in huge demand, the setup is incredibly strong.

After following this story closely, this feels like exactly the validation we’ve been waiting for. Beamforming is winning real high-stakes spots today, while photonics keeps them primed for the AI data center boom. A small-cap at the intersection of SATCOM, defense, and next-gen infra, this is asymmetric at its best.

What’s important to remember: almost everyone is hyper-focused on photonics (for good reason), but wireless has been the quiet but powerful growth engine laying the foundation all along. More than the order size, it’s the strong signal it sends. Leadership delivered exactly what the CEO flagged in Q1. Next, I expect photonics to fire with new design-ins and pre-production orders.

I’m more bullish than ever. Patience here is going to pay off big.

I'll keep talking about $OUST on every single red day unlike all FOMO chasers who only talk about it when they're up +10% on the day.

$OUST is at $2.3B MC / $2.1B EV today.

Here's where I get a +3-5x (minimum) from:

$900M * 10x sales multiple on 41% CAGR for 4 years gets you to $9B EV alone.

10x sales multiple essentially gets you over 4x from here.

As long as youre assumption is that $OUST trades above 5x sales on:

- Being one of the sole Western LiDAR plays

- Being one of the sole Western LiDAR plays in a +$70B TAM

- Being EBITDA and net profitable

- Growing above 40% CAGR

Then $OUST makes complete sense here.

Power & infrastructure is key for the AI build out and $AIPO etf holds the stocks doing that

$CCJ – Mines uranium; fuels nuclear reactors that power AI data centers.

$GEV – Makes gas turbines and grid equipment; keeps power flowing at scale.

$ETN – Builds electrical components (switchgear, transformers); manages power distribution infrastructure.

$VRT – Designs liquid cooling and power systems specifically for data center density.

$CEG – Operates nuclear plants; sells clean baseload electricity to hyperscalers directly.

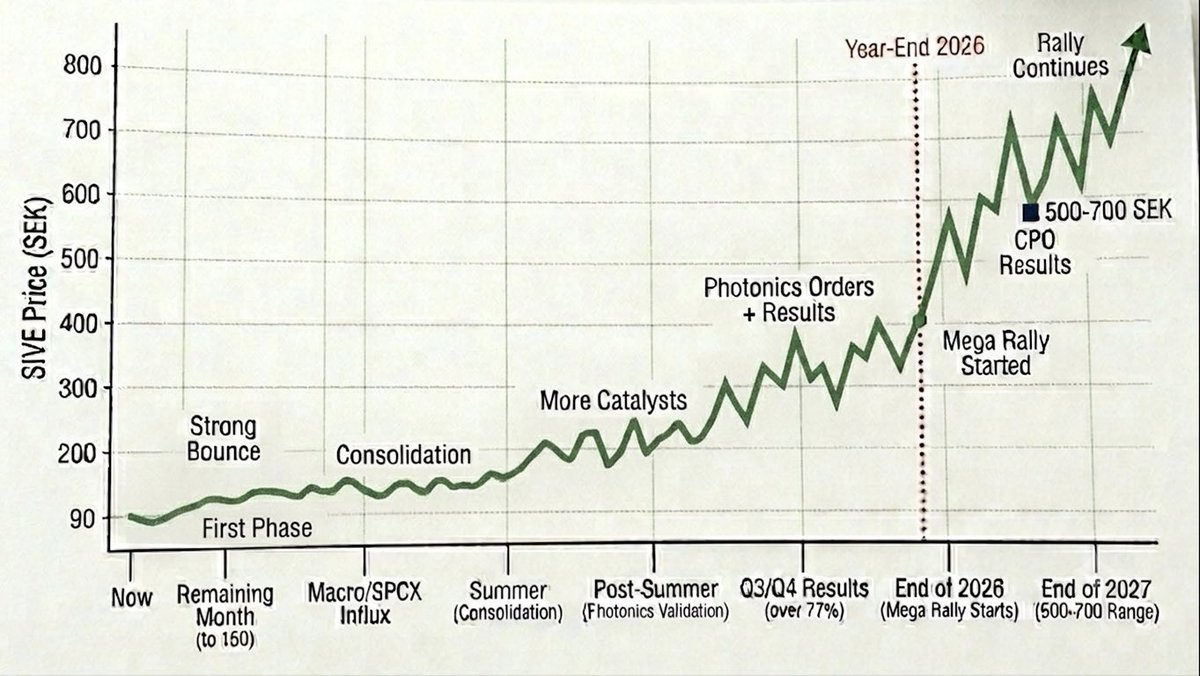

Let me speculate a bit on $SIVE

Based on my own assumptions, I’m going to map out a timeline for $SIVE

We are seeing upcoming catalysts and growing expectations:

- Ayar Labs integrating into the $NVDA ecosystem

- Partnership with $GFS

- Dual listing on the Nasdaq

But recently, we've also been seeing actual order confirmations

Even if these aren't in the photonics segment, they are hitting their other business units

This cleans up their financials and gives them the breathing room to smoothly develop the photonics and CPO branch

What I expect next:

Short-term: I see a strong rally through the rest of the month up to 150 SEK

Driven by a shift in macro market sentiment and capital inflows returning after the migration to $SPCX

Consolidation: After that, I expect a consolidation phase in the 150 SEK range, similar to what we are seeing right now

Summer Catalysts: More catalysts will keep rolling in throughout the summer, moving the price into the 200-250 SEK range

Post-Summer & Looking into 2027:

After the summer, I firmly believe the first orders from the photonics branch will start coming in

Nothing crazy, but they will serve as massive validation, alongside the upcoming quarterly results

For those quarters, I expect growth to surpass the 77% surge we saw in Q1

This should move us into the 300-400 SEK range

As we approach the end of 2026, we'll be right on the doorstep of CPO starting to show tangible results by early 2027

Larger photonics orders will kick in, and the second mega rally for $SIVE will begin

I foresee more catalysts dropping

While institutional investors finish locking down a massive piece of the pie

I see $SIVE wrapping up the year in the 500-700 SEK range

From there, the rally will continue into numbers I won't even try to guess

This timeline is based on recent developments, the company's execution, and price action

It is pure speculation on my part, but keeping it realistic

If the current catalysts start solidifying

Ultra bullish on $SIVE

The optical transceiver market triples to $36 billion this decade and $AAOI is the smallest cap name with arguably the most explosive upside in the entire space. Here is the math nobody is showing you.

Start with where we are. 800G is the workhorse today and it is exploding. Shipments doubled in 2025 to around 24 million units.

TrendForce sees 63 million units in 2026, a 2.6x jump in a single year. Zero demand softening.

Now the 1.6T ramp, which is the real story. Shipments crossed 1 million units in 2025 and are forecast to hit 5 plus million in 2026.

NVIDIA’s GB300 platform requires 162 of these 1.6T modules per server cabinet, so demand scales directly with every rack that ships.

Microsoft alone is deploying 2 million 1.6T transceivers, roughly $3 billion in procurement.

And 3.2T is absolutely coming. By 2027 most switch ports transition to 1.6T, and by 2030 most are expected to run 3.2T.

Every generation means more dollars per port, more modules per cabinet, and a brand new upgrade cycle. This is a staircase that climbs for the rest of the decade.

Now here is why $AAOI specifically.

It is the smallest cap of the major players, which means it has the most room to run if it executes. And it has one structural advantage almost nobody else has.

They make their own lasers in house. In a market where lasers are the single biggest supply bottleneck, while competitors wait in line for allocation, AAOI controls its own input.

That is exactly why two to three hyperscalers told them they would buy every transceiver they can produce.

Revenue already grew 83% to a record $456 million with guidance over $1.1 billion for 2026.

A confirmed order book stretching through 2027. And a market cap a fraction of $COHR, $LITE, or $CRDO

When you own the bottleneck input in a market tripling this decade, and you are the smallest name in the room, that is where the asymmetric upside lives.

$LWLG - The mainstream media is chasing overextended software applications, completely blind to the physical polymer bottleneck that next-gen AI supercomputers are slamming into.

Everyone is tracking traditional silicon photonics, while institutional smart money is quietly absorbing the float of Lightwave Logic.

Retail looks at backward-looking income statements and calls it a science project.

They completely fail to see that Nvidia’s CEO just explicitly endorsed the silicon photonics shift, sparking a massive wave of accumulation.

Lightwave's proprietary „Perkinamine“ polymers act as a high-performance pavement for internet data, doubling speed while slashing energy consumption by 50%. This is the Holy Grail for the 1.6-Terabit AI cluster expansion.

The herd will buy the commercial volume breakout at $20. Insiders are front-running them today.

Drop a #LWLG or Quote-RT this if you understand the optical bottleneck.

What is your #1 hidden semiconductor play for the rest of 2026? 👇

My favourite asymmetries right now:

> $AAOI - Raised FY26 guidance to $1.1B+ with demand outrunning supply into mid-2027 on the 800G and 1.6T ramp, then sold off 12% on the print. A raised guide into a sell-off is the setup.

> $MRVL - Jensen called it the next trillion dollar company at Computex. $2B Nvidia stake, NVLink Fusion, and a genuine moat in custom silicon and silicon photonics. You can overcomplicate it and pretend you know more than the Godfather of AI, or you can just buy.

> $KEEL - Amazon hiring in Moses Lake where Keel is building, first hyperscaler lease is the trigger. Panther Creek at 350MW is the real prize. This is just proof of execution.

> $AMPG - relaunched its website and listed $AMZN and $NVDA as customers for the first time. The Nvidia link traces to the AI-RAN work with Northeastern. Amazon is brand new. Management has already said new contracts are coming and would be announced soon.

> $NBIS - Do I really need to say anything