Into the 4.45/50 zone for us 10y to reload some medium term shorts again.

Think market is coming to realisation that neutral is somewhat higher than we all think…

many settled with a ~3.5 (even Powell!) as a decent mid…

but what if it’s more like 4-4.5%?

Belly vulnerable

Sometimes the chart voodoo works.

Sfrz7 bounced at 96.00.. US10y back flirting with the major trendline.

Lots of bad shorts at bad levels sets up squeeze potential. 4.45/50 area 10y might make sense to reload.

Destination still for higher rates imo, but we’ve moved fast.

Vibe shift in USD continuing, as US exceptionalism narratives take hold.

US now the clear country with the best growth fwd, and now the mkt has come to terms with a hike (u6 pricing 12.5!)

EURUSD vs 5y real rates shows a huge divergence.

It’s all driven by $ RY going up May

Sometimes the chart voodoo works.

Sfrz7 bounced at 96.00.. US10y back flirting with the major trendline.

Lots of bad shorts at bad levels sets up squeeze potential. 4.45/50 area 10y might make sense to reload.

Destination still for higher rates imo, but we’ve moved fast.

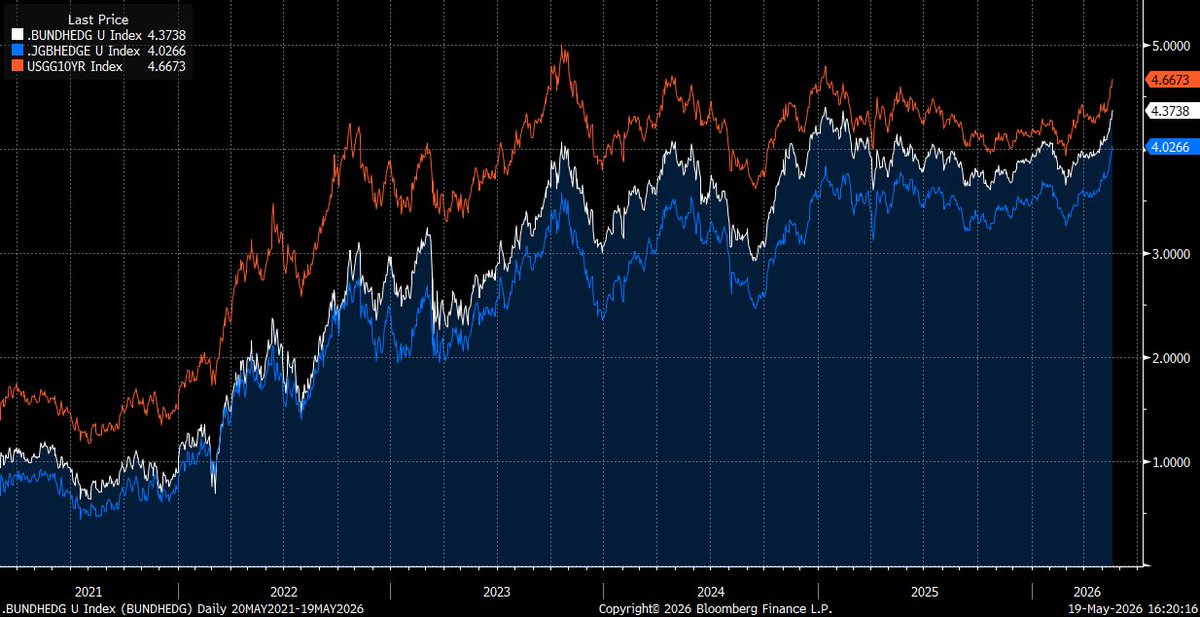

@sunchartist Got a bit busy this afternoon lol… have the bund and JGB hedged into USD handy, (vs UST10yr).. you can infer relative attractiveness for JPY domiciled from the 3 comparatively

I think under appreciated in JPY rates is the speed and direction of travel of Inflation swaps.

5y up to new highs today, up 70bps since the war, and 35bp this month!

BoJ falling further behind the curve. GDP overnight allays immediate concerns for June. But more is needed.

@cchengasaurus Yeh that’s the bit on the payoff matrix where you lose bad… For me it’s the least likely path of what can actually happen. But who knows!

I wouldn’t rec anywhere sofr personally.

Trade mostly pushed there is sep/oct/dec fomc fly.

Global rates pausing at the big trendlines..

so instead of focusing on outright delta, time to look around the edges for trades.

July MPC gap trades less than 1bp over July ECB gap.

Modal paths are for Jun+Sep from ECB, and a “not cycle” hike from BoE at July.

@Augustus_kaizer Sure, just subjective to the whims of the market on any given day and time…

What do you see as the modal path here?

Which is the bit you disagree with most?

@Augustus_kaizer This is twitter my guy. Gotta keep it simple…

In any case, wasn’t referring to market implied. But simply my own most likely path.. (And that of about 90% of people i speak too)

@PatrickBasiewic@pdegrauwe Agreed. Completely misses the point tho. UKT does not borrow at a higher rate than French treasury.

BoE sets a higher policy rate than ECB does.

The author almost gets there in the piece, but fumbles it at the line.

@JuliusProbst@pdegrauwe Yep exactly! I gave the author the benefit of the doubt that it was either a typo or English translation error… context of the blog was for yields, not burden, but yes, if referring to burdens then the analysis is even more wrong! Hilarious eh