Blockchain adoption is broken. It’s time for a new model.

@santiagoroel is launching a custom Avalanche L1 to bring businesses on-chain—not through speculation, but through acquisition & transformation.

Here’s how @Inversion_Cap is making it happen👇

https://t.co/PUjEcbASqR

@vaneckpk@fundstrat Yep, just finished and had the same thought. My first initial thought is memcoins are about to become an even larger portion of the asset class

Weird, you can't seem to access your own assets to sell them or to buy more of them.

If only there was a solution to this that didn't require trusting a 3rd party...

https://t.co/q13sOgjhZd

We've raised our 2030 ETH price target to $22K, influenced by ether ETF news, scaling progress, and our read of onchain data. Additionally, we've analyzed how ETH and BTC perform in both traditional and crypto-only portfolios for optimal returns. @Matthew_Sigel@Patrick_Bush_VE

🔗 https://t.co/PUlnat5Agz

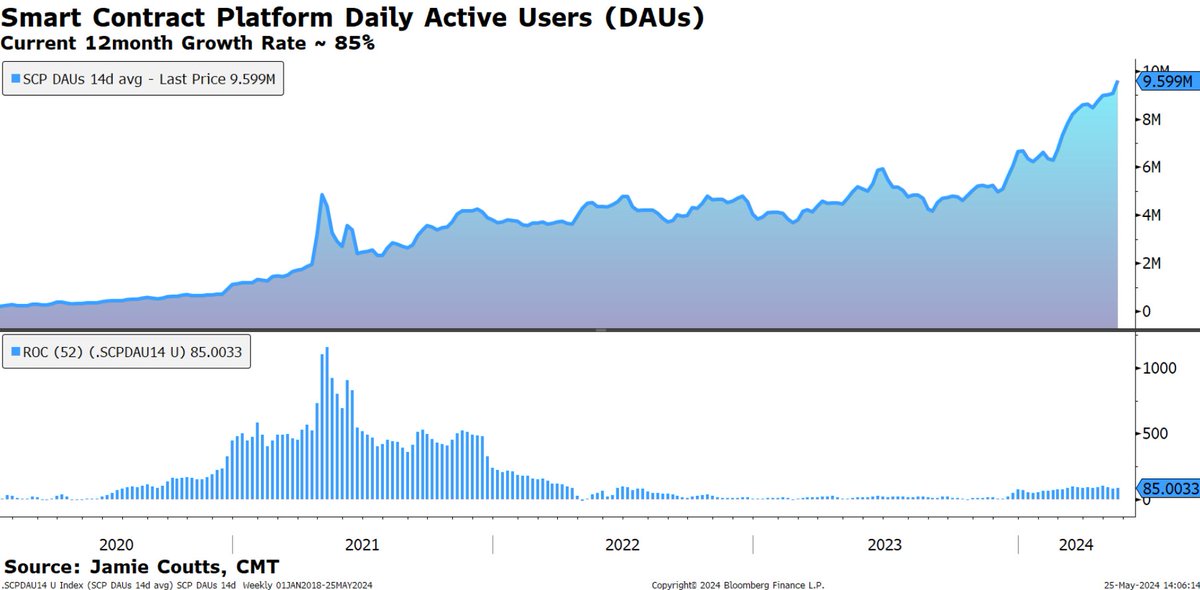

Interesting observation from a pioneer OG #crypto analyst/investor @cburniske on the dApp pipeline. By my estimation, Daily active addresses should reach 20-30 million in 12 months time based on current growth rates. This implies 200-300 million MAUs and potentially 1 billion in total wallet addresses.

If it wasn’t clear before, AI is the single biggest revenue driver in cloud.

Microsoft’s Azure is winning share directly from Amazon. In Feburary, Microsoft grew 2% & Amazon lost 2%. Google is also taking share - 1% in the last year. A one percentage point share shift represents about $750 million of spend or about $5b in market cap.

“We’re fundamentally a share taker there because if you look at it from our perspective, at this point, Azure has become a port of call for pretty much anybody who is doing an AI project”

“More than 65% of the Fortune 500 now use Azure OpenAI service.”

Much of the AI spend is at the enterprise, where a 50% reduction in customer support cost or a 75% increase in engineering capacity filters billions to the bottom line.

“The number of $100 million-plus Azure deals increased over 80% year-over-year, while the number of $10 million-plus deals more than doubled. "

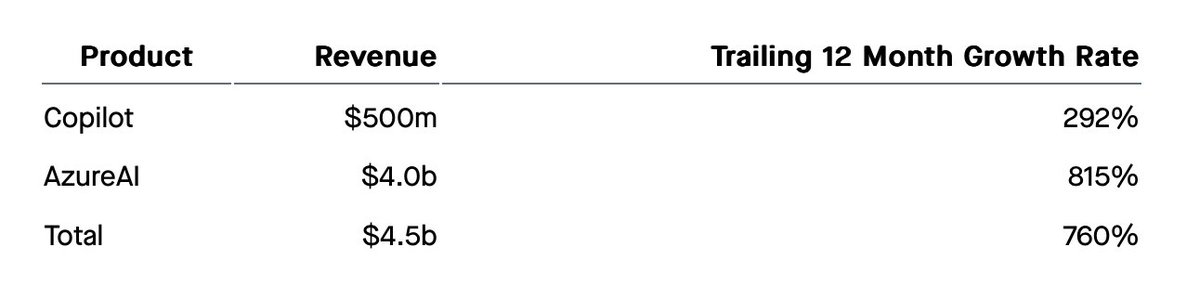

Copilot growth implies about a $500 million ARR product growing 35% QoQ - tripling annually.

“We now have 1.8 million paid subscribers with growth accelerating to over 35% quarter-over-quarter…more than 90% of the Fortune 100 are now GitHub customers, and revenue accelerated over 45% year-over-year. "

The rest of Azure is still growing in a nice clip of 24% annually. But AI added 7 percentage points or $4b to the revenue, a 31% growth rate for a $4b business means adding $1.2b of revenue in a year.

“7 point lift to Azure growth from AI”

Combined with the Copilot business, Microsoft has roughly $4.5b-5b AI product suite.

This trajectory shows no signs of slowing down. The company is investing $50b of capex this year into additional capacity because AI demand exceeds supply.

“Currently, near-term AI demand is a bit higher than our available capacity…In Azure, we expect Q4 revenue growth to be 30% to 31% in constant currency”

Even more impressive, if illusive to measure, is the cross-selling ability of AI across Microsoft customers. The net dollar retention figures must be world class because Microsoft is largely selling to existing customers. NDRs of 300-400% are not unlikely.

Vector databases :

“So AI projects obviously start with calls to AI models, but they also use a vector database. In fact, Azure Search, which is really used by even ChatGPT, is one of the fastest growing services for us. We have Fabric integration to Azure AI and so – Cosmos DB integration.”

The Fabric data platform :

“Fabric now has over 11,000 paid customers, including leaders in every industry from ABB, EDP, Energy Transfer to Equinor, Foot Locker, ITOCHU and Lumen; and we are seeing increased usage intensity.”

AI in other applications:

30,000 Organizations across every industry have used Copilot Studio to customize Copilot for Microsoft 365 or build their own, up 175% quarter-over-quarter.

There’s mention of more within the transcript, but I think the point comes across.

Within the Google transcripts, One of the more interesting data points is that generated search actually increases search volumes :

Most notably, based on our testing, we are encouraged that we are seeing an increase in search usage among people who use the new AI overviews as well as increased user satisfaction with the results.

Also, the company’s reach across consumers is staggering :

We have 6 products with more than 2 billion monthly users, including 3 billion Android devices. 15 products have 0.5 billion users

AI is accelerating growth in a $75b market, 20 year old market. If these growth rates aren’t a sign of anything to come, the amount of market cap creation in front of us will a garguantuan figure.

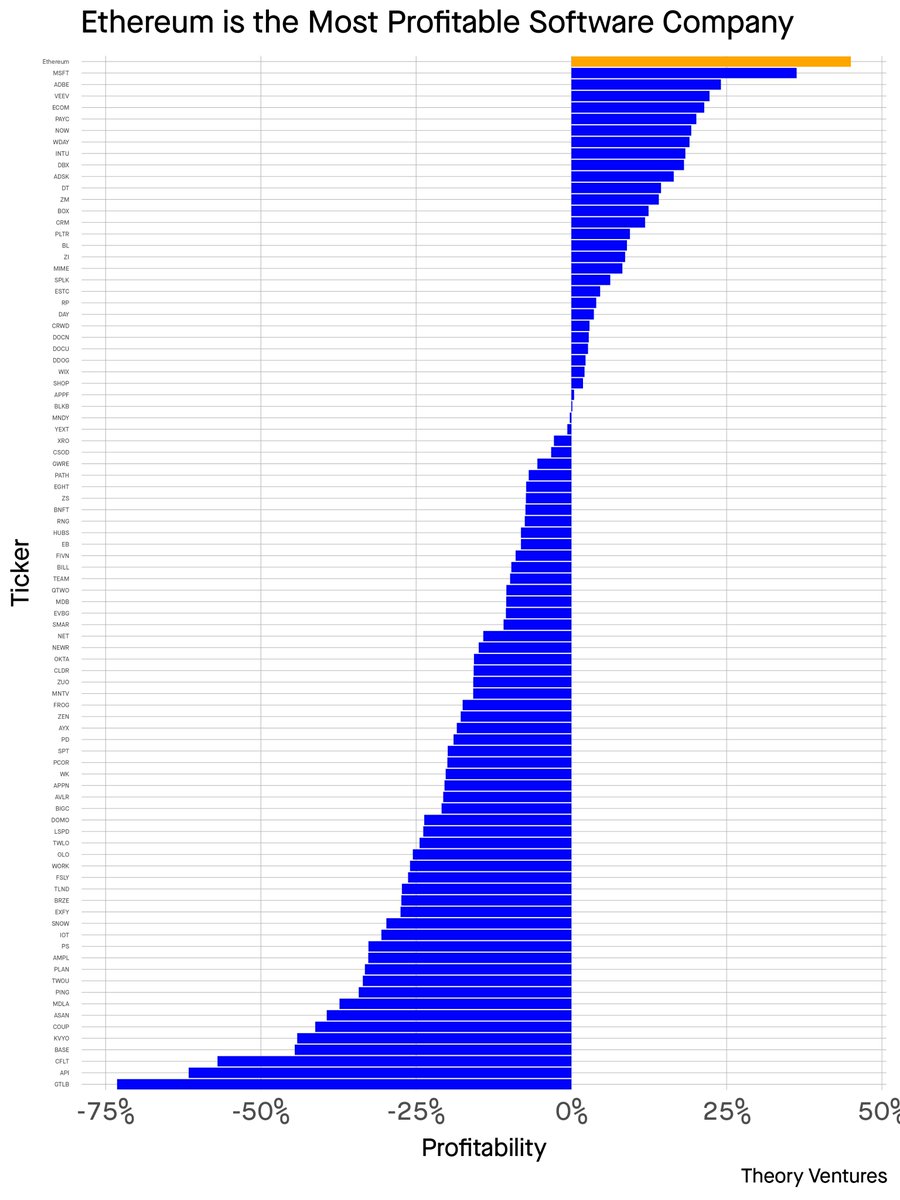

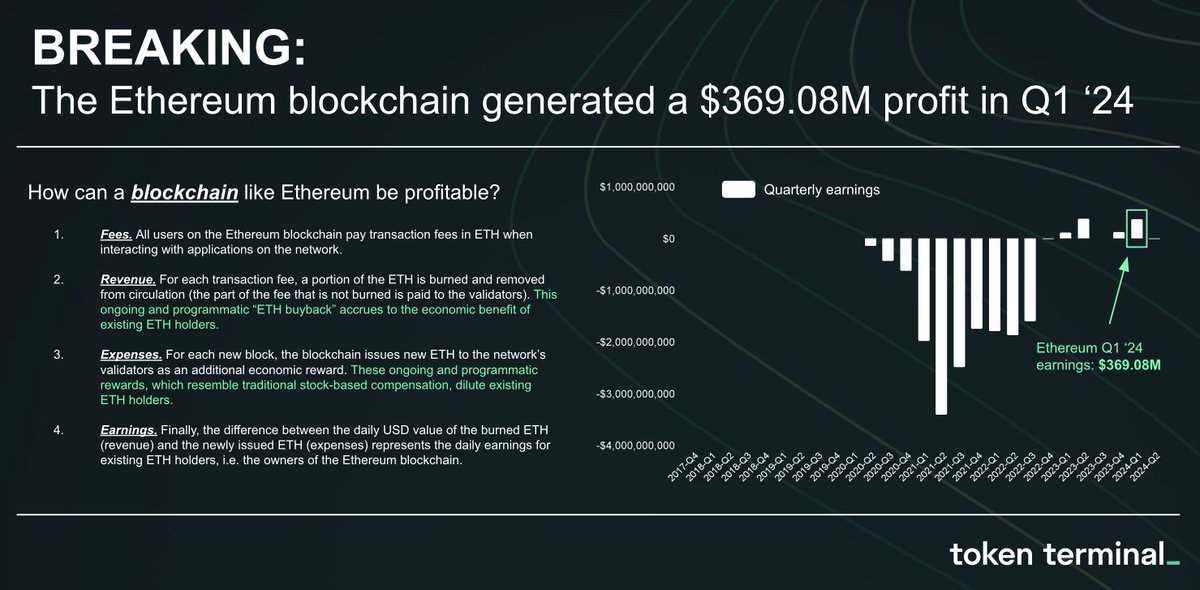

What was the most profitable software company in Q1 2024?

Ethereum.

Ethereum generated $370m in profit on $825m in revenue for about a 45% net income margin.

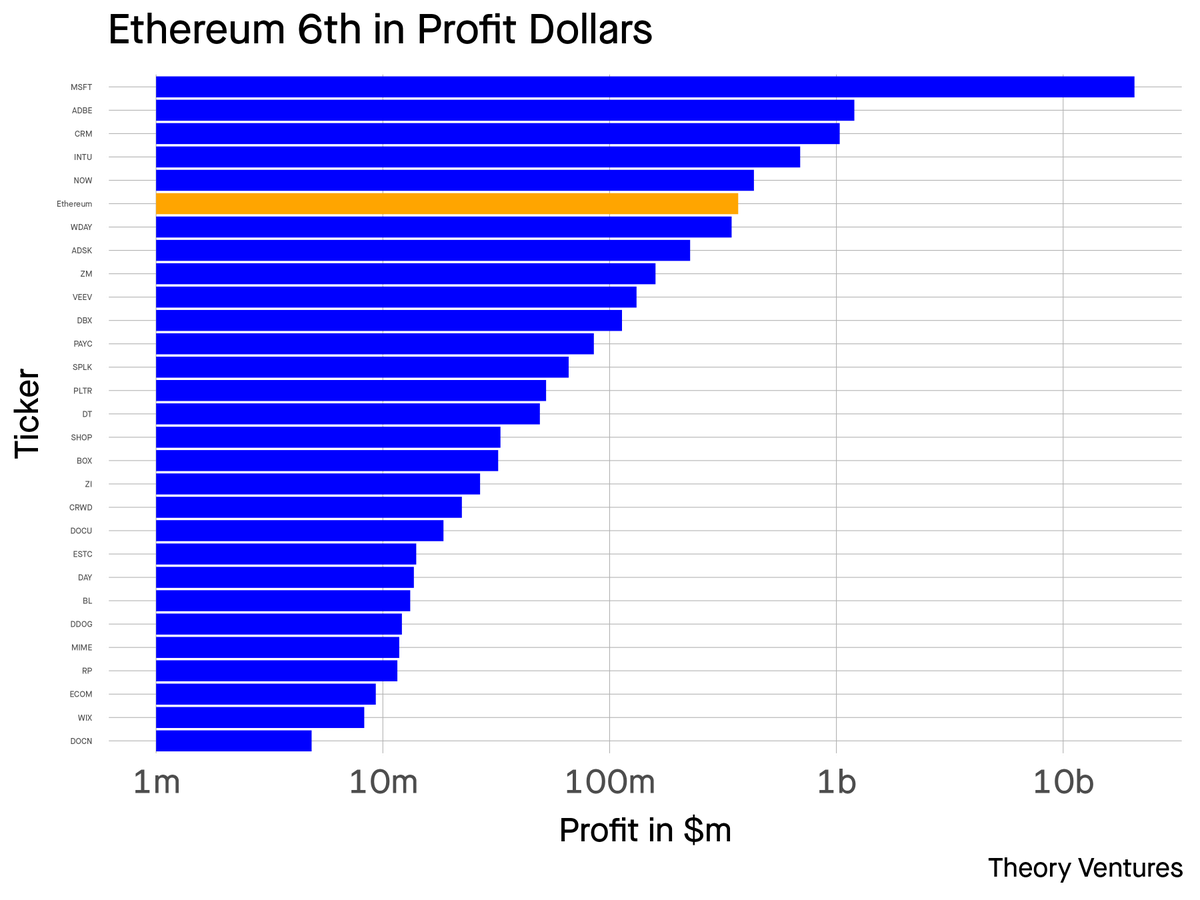

The chart above shows both the historical performance & also explains how web3 blockchains like Ethereum generate revenue & profits.

How does Ethereum compare to other software companies?

If Ethereum were to trade on the New York Stock Exchange or the NASDAQ, it would top the net income margin (%) charts, with Microsoft, Adobe and Veeva thereafter.

In terms of aggregate dollars across all publicly traded software companies, the Ethereum would be sixth. Note the profit scale in the chart above is logarithmic.

Ethereum’s market cap is roughly $350b today, which is on par with Salesforce & worth 7 Snowflakes.

There are many important caveats here. Ethereum’s historical profitability hasn’t been nearly this strong. The second is Ethereum isn’t organized as a corporation akin to others in this peer set. The third is the Ethereum token is both utility & “equity.” Last, Ethereum trades at 100x revenue compared to 7-17x for Salesforce & Snowflake.

But Ethereum demonstrates the compelling value that web3 blockchains can create.

First DePin project on Artemis: @akashnet 👀

- Fees: $85.5k in March '24 (~$1m fees run rate)

- Revenue: $2.9k in March '24 (~$35k rev run rate)

What other DePin metrics and projects do you want?

2x better response times than leading provider, Infura, with 0% failed calls.

THIS is why you should under-dePIN your RPC service with POKT Network.

Thanks for the s/o @hmalviya9 !

The State of RPCs (Based on Last Week Data)

- @QuickNode is the fastest RPC Provider with an average response time of 107 ms.

- @POKTnetwork have 2x better response time than leading provider @infura_io with 0% failed calls.

- @BlockdaemonHQ is the worst performer right now.