Our current thesis remains unchanged: PTFE is merely a secondary, non-mainstream solution that is highly unlikely to achieve commercial mass production. Instead, the M10Q configuration remains the clear preferred choice, primarily because it offers a broader pool of qualified suppliers and commands strong deployment support from tier-1 PCB fabricators.

every job will turn into explaining your intentions to ai

explaining what you want to ai is surpringly time consuming, coders already spend 80% of their time doing it, and this will be true for everyone

People -> Ideas -> Products -> Businesses - > Stocks - > Sectors -> Macro -> Markets

The skills most needed today to really make money in this mkt are towards the beginning and end of that flow diagram while ignoring the math you learned and clinged to from a book or in school in the middle of it.

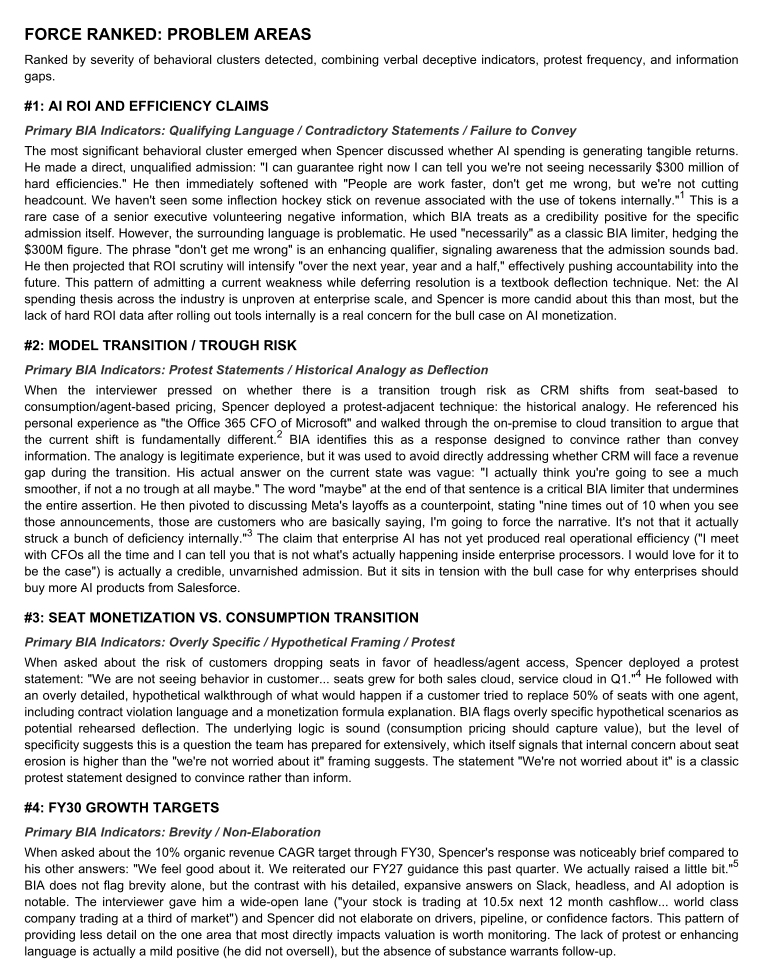

$CRM LANGUAGE ANALYSIS FROM YDAY IR PRESENTATION 1/2

The most significant behavioral cluster emerged when Spencer discussed whether AI spending is generating tangible returns. He made a direct, unqualified admission: "I can guarantee right now I can tell you we're not seeing necessarily $300 million of

hard efficiencies." He then immediately softened with "People are work faster, don't get me wrong, but we're not cutting headcount. We haven't seen some inflection hockey stick on revenue associated with the use of tokens internally." 1 This is a

rare case of a senior executive volunteering negative information, which BIA treats as a credibility positive for the specific admission itself. However, the surrounding language is problematic. He used "necessarily" as a classic BIA limiter, hedging the

$300M figure. The phrase "don't get me wrong" is an enhancing qualifier, signaling awareness that the admission sounds bad. He then projected that ROI scrutiny will intensify "over the next year, year and a half," effectively pushing accountability into the

future. This pattern of admitting a current weakness while deferring resolution is a textbook deflection technique. Net: the AI spending thesis across the industry is unproven at enterprise scale, and Spencer is more candid about this than most, but the

lack of hard ROI data after rolling out tools internally is a real concern for the bull case on AI monetization.

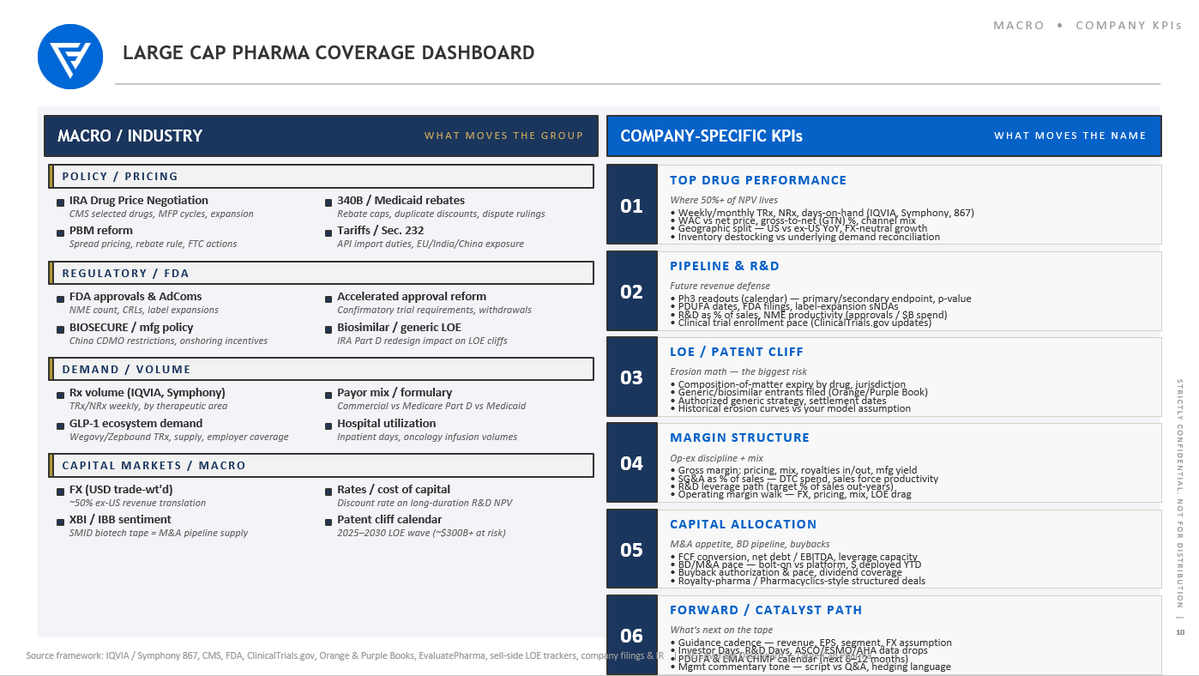

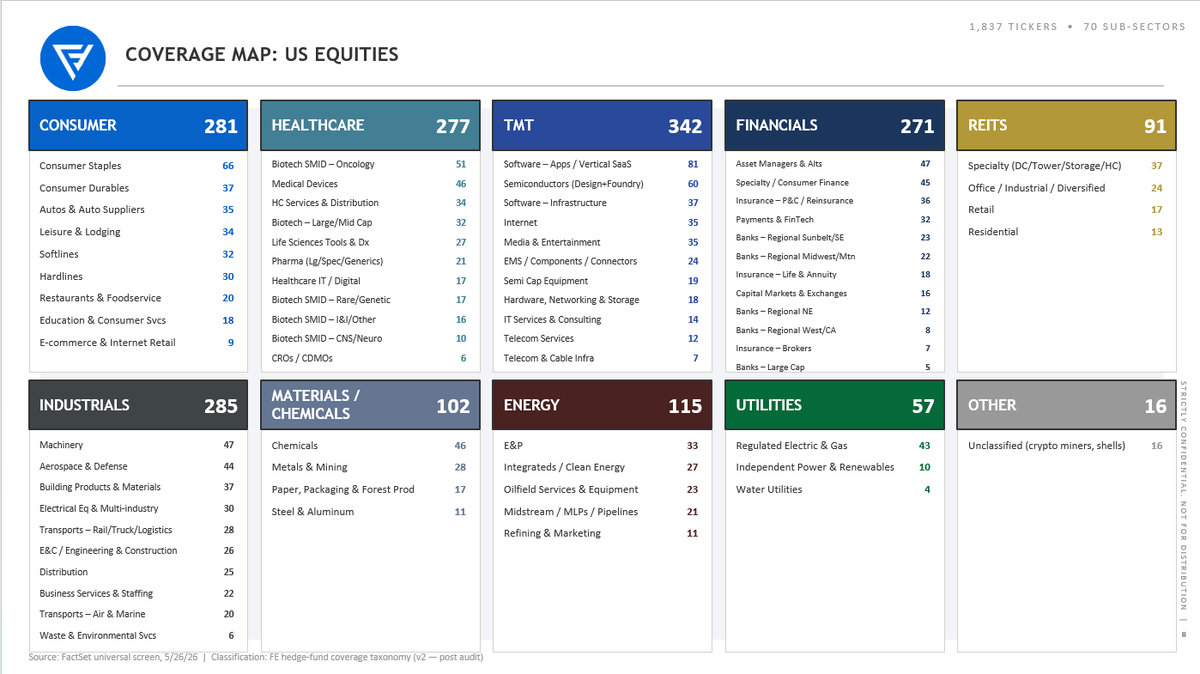

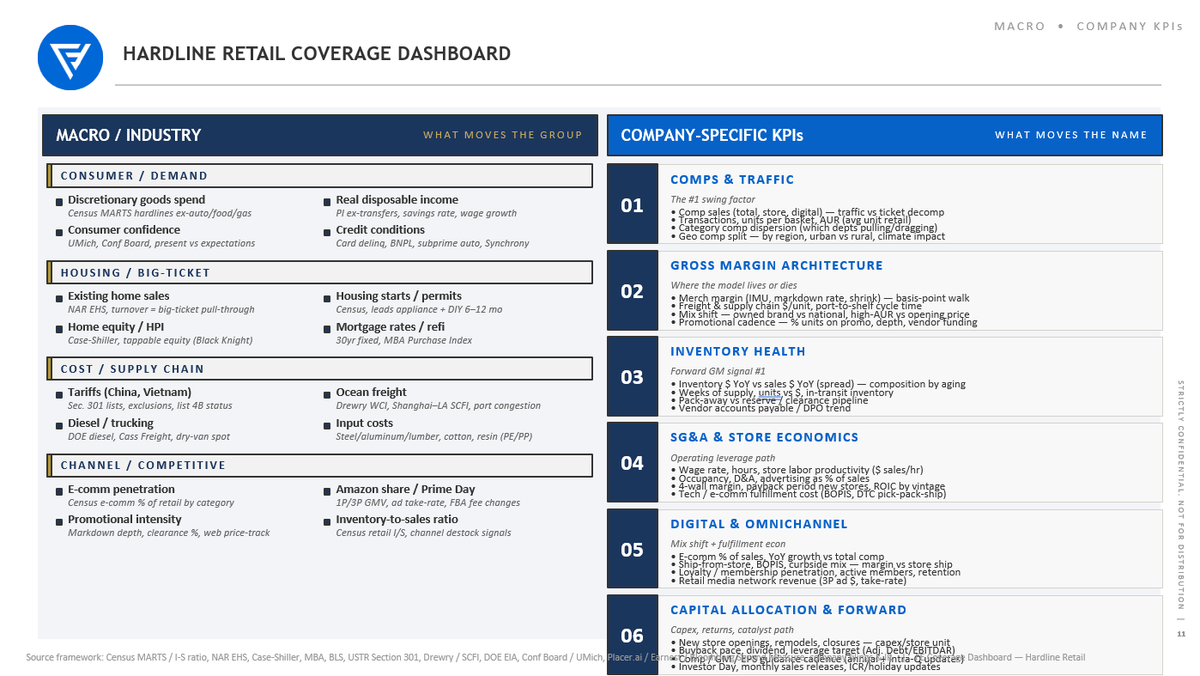

Sharing a few screenshots from one of the more ambitious projects I'm working on right now with respect to agents & investment process: creating coverage dashboard prototypes for all 70 US equity sub-sectors, breaking dashboards into "What Moves the Group" and "What Moves the Name".

I think most technologists don't quite comprehend the investment process differences between a SMID biotech pod analyst vs. a long only midstream MLP analyst vs. an Asian financials Tiger Cub analyst. Public equity investment process is highly heterogeneous and the combinatorial complexity (~a dozen different investors archetypes in ~70 different sub-sectors) hasn't lent itself to easy augmentation with chatbots. Mass customization from a pool of universal process primitives with Agents is a key unlock and I'm wondering how much pre-configuration will happen vs. a thousand flowers blooming from blank agentic workspaces...

My belief: if internal AI teams or vendors can pre-configure coverage dashboards to be immediately value added to the investment process, this forces the agentic "aha moment", accelerates diffusion of agents into investment process, and requires approximately zero time & focus from the investment team (the leverage happens on the back end). Also, if the user interface is configurable, the path to customization from this starting point is immensely easier than solving the blank page problem.

This is VERY conceptual on "what to build" and weak on "how to build", but I'm at the stage on some of this where I am beginning to explore both partnerships with builders and co-development with investment firms.

Please reach out via DM if this resonates.

This is an amazing video recommendation from Jukan about CPO.

_______________________________________________________

NPO is still 50% copper, 50% optics. The real CPO ramp is unlikely to begin until 2027 when 2.5D CPO will have 20% copper and 80% optics.

In 2030, the split will be 100% optics in 3D CPO (COUPE XPU)

The true hurdle is in maintenance for CPO in 2027 and 2030.

Pluggable/OBO/NPO (Green/Yellow): If an optical laser or engine fails, field technicians can easily hot-swap a pluggable module at the faceplate, or replace an NPO module on the board without tossing the expensive ASIC.

2.5D & 3D CPO (Red): Once the PIC and laser/optical components are physically bound inside the package or stacked directly under the ASIC, they can no longer be individually serviced. If a single optical component fails, the entire high-value compute engine (the XPU/Switch) is essentially bricked.

_______________________________________________________

CPO supply chain, per @semivision_tw:

1. CSP

Nvidia $NVDA

AWS $AMZN

Meta $META

ByteDance

Microsoft $MSFT

2. SOI Wafer

Soitec

ShinEtsu

SEMCO

IntelliEPI

3. Connector

Amphenol

Senko

US Conec

T&S Communications

Samtec

LightSense

Siemon

4. Testing

WinWay

MPI Co.

Hon Precision

Chroma

5. Fiber

Corning $GLW

YOFC

Sumitomo Electric

FiberHome

Prysmian

ZTT

Fujikura

Futong Group

Hengtong Fiber

6. ELS

Furukawa Electric

Broadcom

Lumentum

Sumitomo Electric

TE Connectivity

Coherent

O-Net Technologies

7. PIC Design & EDA

IBM $IBM

Intel $INTC

Sicoya

MACOM $MTSI

Juniper

Cisco $CSCO

SiFotonics

POET Technologies $POET

Ansys - part of Synopsys

Ayar Labs

Fujitsu

Marvell $MRVL

Lumentum $LITE

Infinera

Huawei

Ranovus

Cadence $CDNS

Skorpios

Synopsys $SNPS

OpenLight

8. Foundry

TSMC $TSM

Intel $INTC

Tower Semi $TSEM

Applied Optoelectronics $AOI

Silex

GlobalFoundries $GFS

Samsung

United Microelectronics $UMC

Acacia

STMicroelectronics $STM

9. EIC & DSP Design

Broadcom $AVGO

Coherent $COHR

Lumentum $LITE

Infinera

Ciena $CIEN

MACOM $MTSI

10. Light Source

LandMark Optoelectronics

Coherent $COHR

IntelliEPI

iQe

NICHIA

Sumitomo Electric

An interesting shift in data center architecture emerged from $NVDA ’s latest earnings. The company expects $20B in revenue this year from its Vera CPU infrastructure.

Meaning NVIDIA, in its very first year of selling CPUs, is already on track to become the world’s largest data center CPU vendor.

Went through $AMD's May 2026 deck this weekend and it nicely reframes the AI debate away from “is this a bubble?” and toward a better question:

How early are we in actual AI demand?

Big difference between employees using chatbots and enterprises rebuilding workflows around AI.

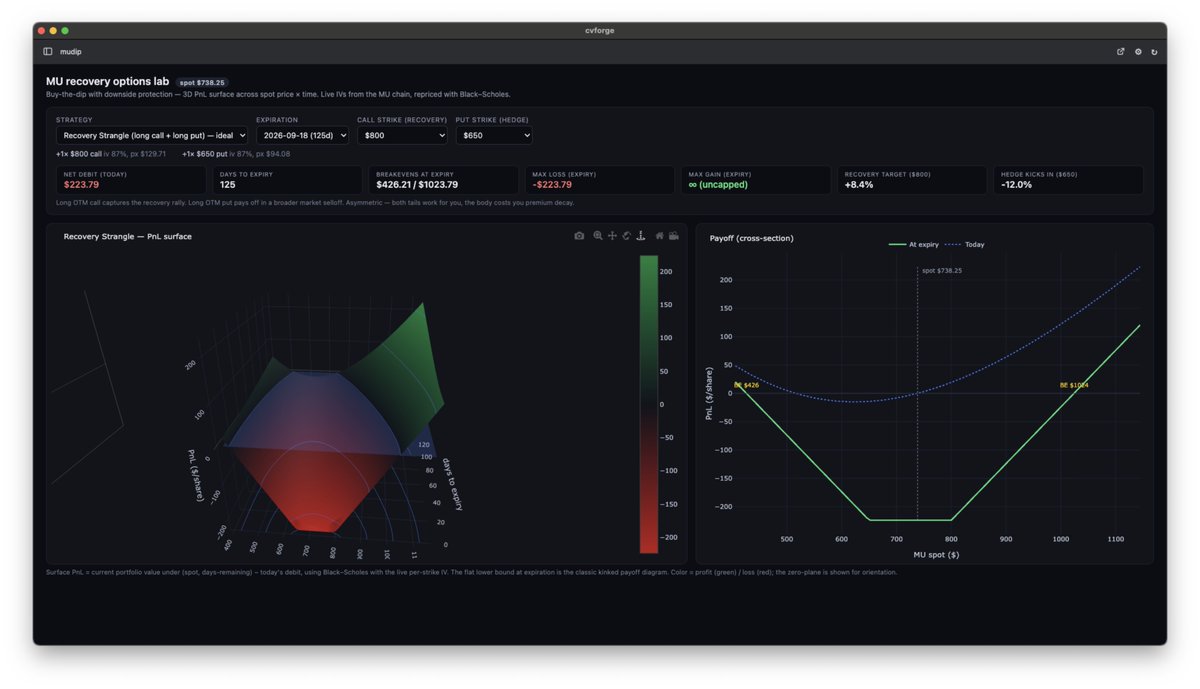

> "if I want to buy the dip on $MU and profit from a recovery to previous highs but also protect myself from a general market selloff - what is the ideal options strategy - give me a 3D PnL surface across spot price and time to better understand"

cvforge:

(this tool is free)

Monthly Wrap Up - May Edition: Sizzling but Safe

Tech rally continues (Nasdaq/SOX/Taiex at new highs) with little overheating sign thanks to strong AI fundamentals amid robust token usage/ARR/capex

Key Updates:

Big 5 CSP Capex:

•2026: +82% YoY (upward revisions for MSFT & META)

•2027: Expect ~+30% upside vs consensus +26%

Price Hike Themes:

•CPU: AMD, Intel, ZDT — another hike likely in late 3Q26

•Memory: MU, SNDK

•Mature Nodes: UMC, TXN

•Copper Foil: Co-Tech, KB, EMC

•Optical Laser: LITE (Buy)

AI Forecast Revisions:

•TSMC CoWoS capacity raised to 145K/175KPM by end-26/27

•Nvidia Rubin MP to Sept.

AI inference ramp. "assume 100M Agentic AI users, 10 agentic task drive 1B agentic execution task workloads, need for 500M CPU cores, at least 2-3M incremental server CPUs (industry ~12-14M server CPUs), underlined by $ARM, $AMD and $INTC ...weekly token generation now >26T"

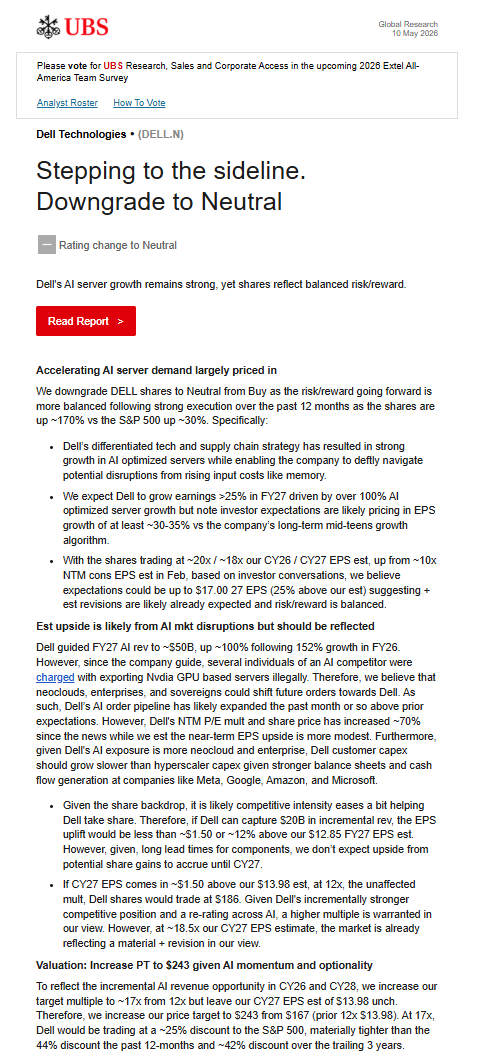

UBS d/g $DELL:

"given Dell's AI exposure is more neocloud and enterprise, Dell customer capex should grow slower than hyperscaler capex given stronger balance sheets and cash flow generation at companies like Meta, Google, Amazon, and Microsoft."

$SMCI, $TSSI