$ADBE is weighing David Wadhwani and Anil Chakravarthy as leading internal CEO candidates, per Bloomberg.

Adobe also hired Heidrick & Struggles to search externally for AI product leaders as it faces pressure from AI-native creative tools.

I don't know who needs to hear this but AGI is already here.

$FDS just made unstructured data available via MCP and I asked it to read four transcripts for $VEEV, update me on what's going on, tell me if the story is getting better or worse, and whether numbers are going up or down.

If this response isn't AGI, I don't know what is.

Claude costs $240 / year. $FDS MCP costs $1,500-2,500 / year.

Claude has serious COGS underneath that $240. $FDS MCP has de minimis incremental COGS.

And people are bearish on important SaaS with critical data?

Now I wonder if semis third deriv just turned negative... If all the big LLMs hit AGI within the next 12 months, the focus might shift to efficiency pretty hard.

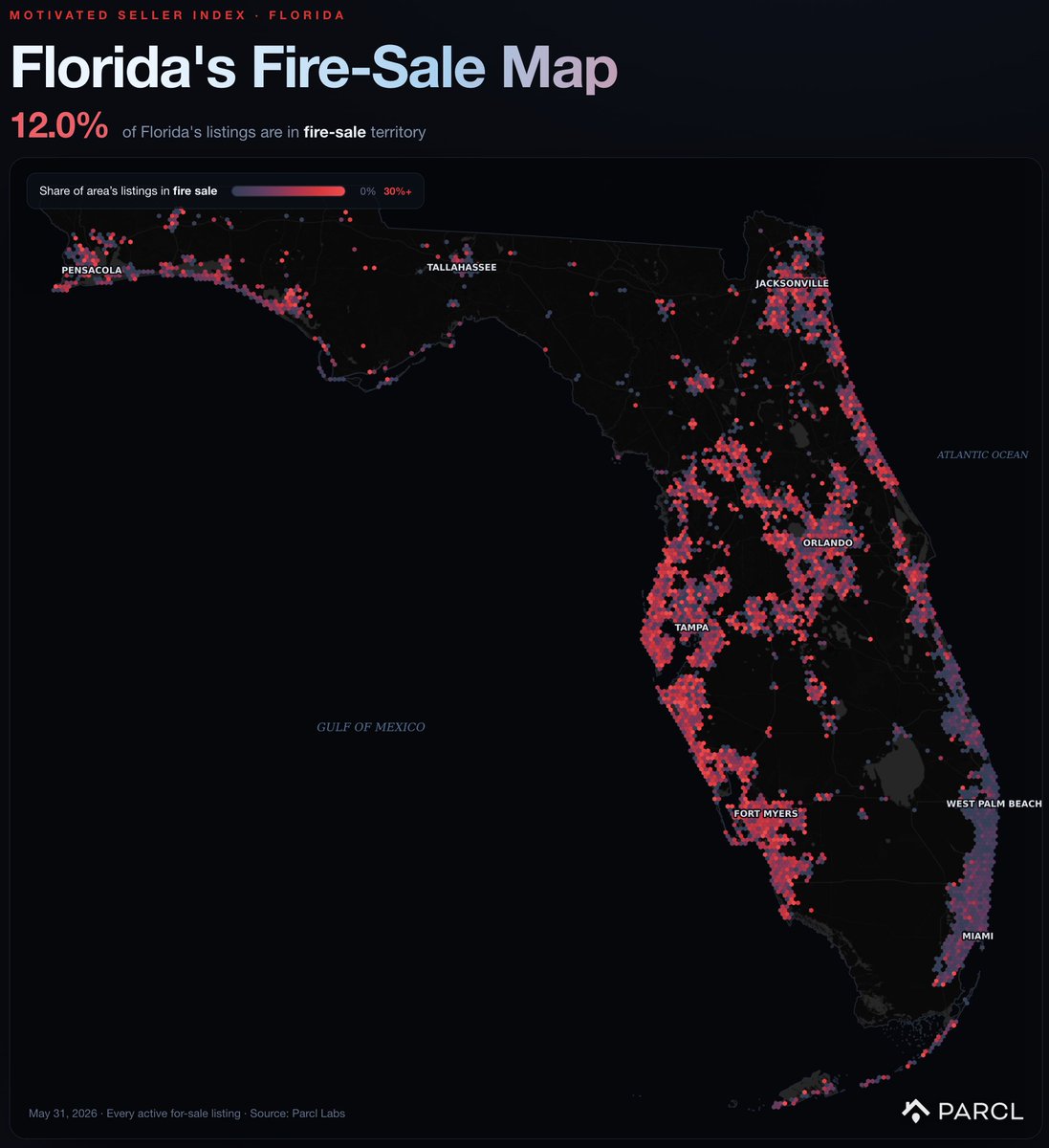

BREAKING - as of this morning, 12% of Florida's for sale homes are in active fire sale territory.

This means they have been sitting on market, the seller is actively cutting prices and increasing the frequency of those price cuts.

The pressure is mainly concentrated in Tampa and Fort Myers, where fire sales now top 30% of listings in some submarkets.

This means sellers cannot find buyers even though they want to.

🚨Michael Burry just said Elon Musk and Nvidia's deal is built on fake numbers.

Burry published a detailed breakdown calling the entire structure "Fugazi", his word for fake.

He is alleging that billions of dollars in Nvidia chips are being hidden off balance sheets, and that American retirees are unknowingly funding the whole thing.

Nvidia, the world's largest AI chip company sold $5.4 billion worth of its most advanced GPUs, the GB200, to a company called Valor.

Valor is not a real operating business. It is a special purpose vehicle, a shell company created specifically to hold these chips and nothing else. Nvidia also invested $1.9 billion of its own money directly into Valor on top of the sale.

Those 100,000+ chips are now physically inside xAI's data center. xAI is Elon Musk's artificial intelligence company, the one that builds Grok. xAI is using every single one of those chips right now to run its AI models.

But here is what Burry is flagging.

Neither Nvidia nor xAI owns those chips on paper. Valor, the shell company holds legal title. That means $5.4 billion in GPU assets do not show up on Nvidia's balance sheet as inventory.

They do not show up on xAI's balance sheet as assets. They are legally invisible to both companies.

Nvidia gets to book the $5.4 billion as a completed sale and record it as revenue. xAI gets full use of the chips without owning them. And the risk disappears into a shell company in the middle.

Now here is where American retirees enter the picture.

Valor needed $3.5 billion in debt to fund this structure. Apollo provided it. Apollo is one of the largest asset managers on earth with $1.03 trillion under management and $834 billion specifically in private credit.

Apollo raised the $3.5 billion, packaged it into debt securities, and sold those securities to Athene.

Athene is Apollo's own insurance company. It sells fixed and indexed annuities, retirement savings products, to ordinary Americans.

When a retiree buys an Athene annuity, they believe their money is sitting in safe, stable investments. That money is now inside a structure funding Elon Musk's AI data center.

The numbers inside Athene are most alarming.

Athene holds $74.2 billion in reserves. It has moved $217 billion in assets into a captive insurer based in Bermuda, meaning those assets sit outside normal US insurance regulation and oversight.

Of the entire portfolio, 34.7%, equal to $103 billion, is classified as Level 3 assets.

Level 3 is an accounting classification that means there is no observable market price for these assets. No outside party can independently verify what they are actually worth.

The leverage sitting on top of those unpriced assets is 16 times.

Burry's says:

Every step of this structure is technically legal and publicly disclosed. But the entire thing was deliberately engineered across 8 to 12 steps to move credit risk off balance sheets and away from any market pricing.

- Nvidia books the revenue.

- Apollo collects the fees.

- xAI gets the computing power.

- And retirees sitting at the bottom of a 16x leveraged Bermuda insurance structure, holding $103 billion in assets with no market price carry the risk without knowing it exists.

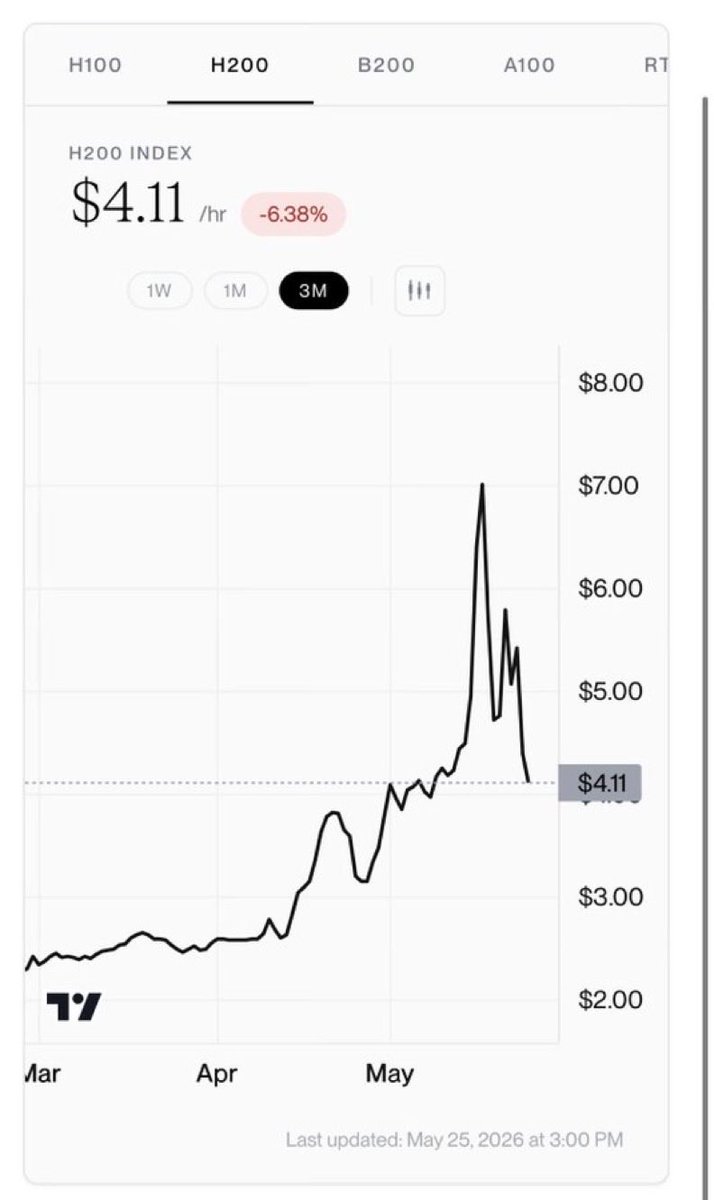

The price to rent an Nvidia H200 just collapsed from $7/hr to $4/hr in three weeks.

A -40% drop in the cost of the single most strategic asset in tech.

When the underlying commodity that powers your entire thesis loses 40% of its value in a month, that usually means one of two things: supply finally caught up, or demand was never as deep as the headlines said.

Either way, somebody is selling.

So why is the AI trade still pricing in scarcity?

BREAKING: "The U.S. and Iran are expected to announce the finalization of a draft proposal of a peace deal to end the fighting on all fronts by Sunday afternoon, a source close to the negotiations told The Washington Times"

Really enjoyed the deck @loganbartlett and team just shared on the state of Software, wanted to pull out a few things that caught my eye:

1. AI-native companies are growing faster AND more efficiently

The growth rates are really staggering. And they’re doing it with very few people. The demand for AI is insatiable, like nothing we have ever seen, and is diverting budget away from traditional software. This is an existential moment for the incumbents. I’ve been saying Accelerate or Die for months. The accelerating is unprecedented, and the growth is coming at the expense of SaaS 2.0. Only death can pay for life

2. They’re doing it without going head-to-head with incumbents

This is probably the most interesting slide to me. These AI-native businesses are growing so fast by using two approaches:

A) Finding a wedge into the enterprise, scaling quickly, then trying to expand

B) Building AI-native Systems of Record from below. @arampell calls this “Greenfield Bingo.” New businesses/SMB have zero/low switching costs, so AI-native CRM/HR/ERP companies can take share and march upmarket from below

Both of these are particularly tricky for incumbents to defend against. They simply aren’t able to move quickly enough to build compelling AI point solutions, and they’re struggling to defend downmarket while also defending the enterprise (bimodal go-to-market and running multiple service models in one company is incredibly difficult)

3. Incumbents scale by throwing people at the problem

This has been the dirty little secret of SaaS for 15 years. It’s basically impossible to grow revenue faster than headcount. Some companies like Shopify did it by layering on payments. Consumption-based companies have been doing it. The AI native companies have this figured out. The incumbent, seat-based, companies simply have never been able to decouple revenue from headcount. They will have to learn or die

4. Incumbents have the right to win but they are failing to capture the moment

As I’ve said before, the CIO wants to stick with their current vendors. They WANT to buy AI solutions from the incumbents. The problem is their solutions suck. @jasonlk has been all over this. These incumbents have a shrinking window of time where they have the advantage, but that window is shrinking. Rapidly.

And this headline is going to give tons of ammo to the Fed hawks, who are arguing that that the accumulation of "one off" shocks is causing inflation expectations to unmoor

*MICHIGAN 5-10 YR INFL EXPECTATIONS AT 3.9% VS PRELIM. 3.4%

MICROSOFT CANCELED CLAUDE CODE!

IT COST TOO MUCH.

Major tech companies are confronting the steep reality of AI inference costs as the era of heavy subsidies appears to be ending.

Microsoft is canceling most internal licenses for Anthropic’s popular Claude Code tool by June 30, 2026 less than six months after rolling it out broadly to engineers primarily due to escalating token-based expenses, while shifting teams toward its own GitHub Copilot CLI.

This mirrors broader pressures: Uber’s CTO revealed the company had already exhausted its entire 2026 AI budget in just four months thanks to heavy Claude usage among thousands of engineers (with individual monthly costs often hitting $500–$2,000), and GitHub is transitioning Copilot to usage-based billing with higher per-token rates starting June 1st.

The reality is good enough AI will expand and constantly get better removing the oxygen of the most expensive.

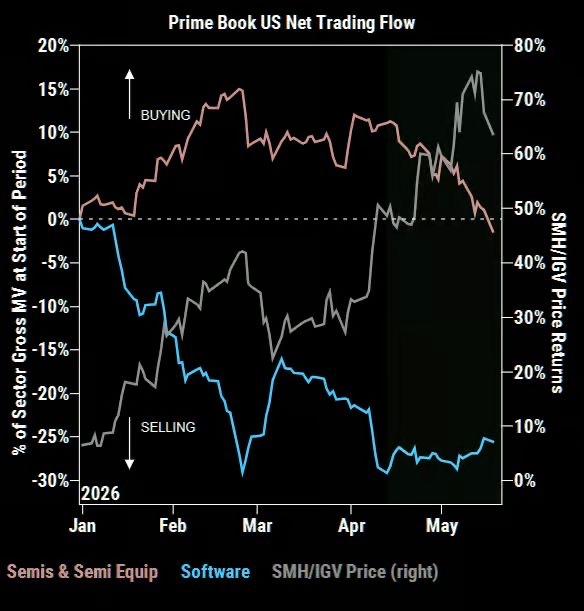

$IGV Software Squeeze Is Loading 🚨

• Mutual funds sitting at their LOWEST Software exposure since 2012 while Semis overweight hit +49bp — the coil is tight

• $IGV pressing the $94/$95 breakout level with a fresh bullish 21/100-day crossover just triggered — last time this setup fired, the move accelerated hard

• Hedge funds already quietly rotating INTO Software while cutting Semis — smart money is front-running the mutual fund chase before it starts

JPM flagged IGV June 95/102 call spreads at ~4x max payout for a reason

The trend line break is the trigger. Watch $94/$95 closely

#Software #IGV #Equities #Tech #Trading

Gavin's takes on Microsoft, Google, Meta, & Amazon:

Microsoft ($MSFT): "I like Satya, I admire him. He's an exceptional CEO, and I give him a lot of credit for the decisions he's made.

But he did go from, "We're going to make Google dance," to being the product manager of Copilot in 3 years.

The decision Satya is making now, which the market has punished him for, but I think is the right decision — who knows how fast Azure could be growing if they were willing to just sell GPUs to OpenAI.

'We're going to use our compute internally to make our own products better.' One reason Copilot was so bad, or has been so bad, is that there wasn't enough compute available. They're fixing that.

He's making good decisions that are risky decisions, to position Microsoft for this world where frontier models are no longer API-accessible.

It's a really courageous decision that I give him a lot of credit for.

Microsoft probably would be an $800 stock today if they were using their GPUs to serve solely OpenAI and Anthropic's capacity instead of using them for their own products."

Google ($GOOG): "Google was incredible last year because they had that TPU advantage, which is now gone.

The reason I think they're still in a great position is they have the most compute of everyone.

We talked about the value of installed bases being higher as a result of shortages — they have the biggest installed base of compute.

Google I/O is this week. If they don't release something that even slightly leapfrogs OpenAI and/or Claude, that's interesting.

It's not a disaster for Google, it's just interesting.

Between the amount of data they have, the YouTube data, the amount of compute, the search business — Google's never not going to be in a good position. You see that with GCP going crazy."

Meta ($META): "You've got to give Zuckerberg immense credit, for what he's done in terms of making Meta an AI-first company internally.

He is the only one of those true internet giants to have done that. I give him a lot of credit for paying up when he did for contracts, that talent.

And Muse was a really big upside surprise. It was the first model from MSL, and it's not on the Pareto frontier with xAI, Google's one entrant, OpenAI and Claude, but it's pretty close. That was very impressive to me. So Meta is in a better position — still not as strong of an absolute position as Google, but a better position."

Amazon ($AMZN): "Amazon is in a really strong position because of Trainium.

You're going to see real P&L efficiencies from robotics over the next 18 months in their retail business.

I actually think Nova — their internal models are not where Muse is, but they're better than they get credit for.

The two companies who are the most deeply engaged with startups are Amazon and Nvidia by a mile.

It's going to end up being a pretty big advantage for Nvidia and Amazon — with Google right behind them — to have this engagement that you just don't see from these other hyperscalers."

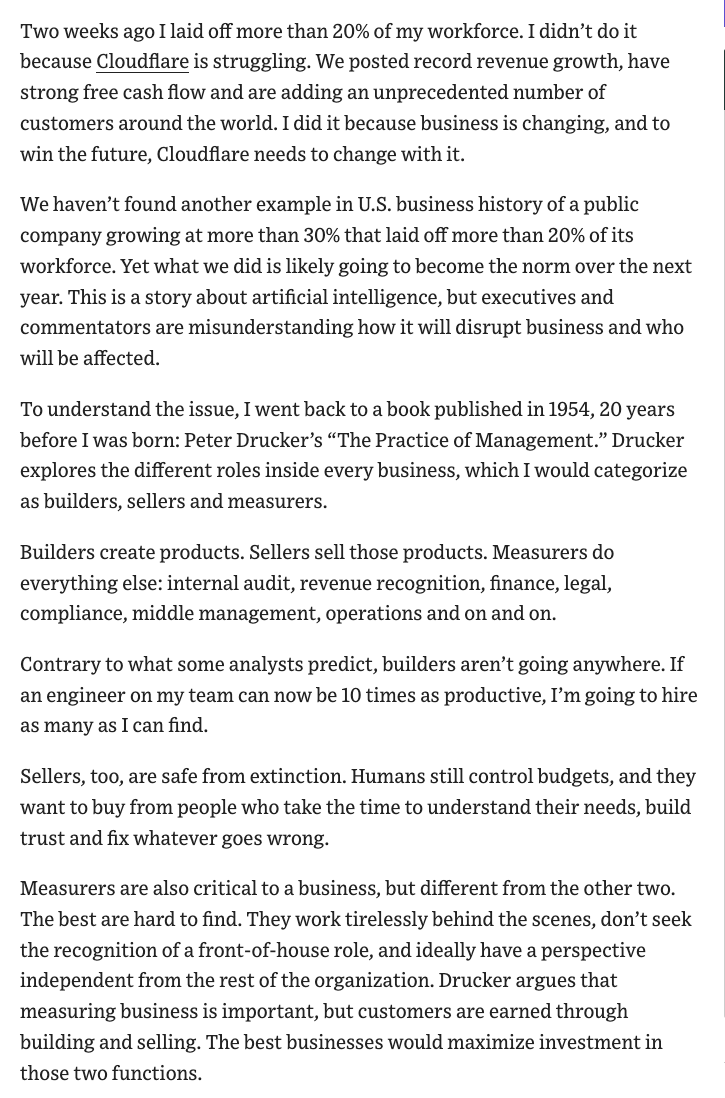

Cloudflare CEO Prince on how AI changes who gets laid off first:

Two weeks ago I laid off more than 20% of my workforce. I didn’t do it because Cloudflare is struggling. We posted record revenue growth, have strong free cash flow and are adding an unprecedented number of customers around the world. I did it because business is changing, and to win the future, Cloudflare needs to change with it.

We haven’t found another example in U.S. business history of a public company growing at more than 30% that laid off more than 20% of its workforce. Yet what we did is likely going to become the norm over the next year. This is a story about artificial intelligence, but executives and commentators are misunderstanding how it will disrupt business and who will be affected.

AI isn’t coming for builders or sellers, but it is coming for measurers. Tireless, independent, efficient and available, AI systems can now measure an organization with a level of objective detail and precision that was previously impossible even for the best employees.

For Cloudflare, internal audit previously picked a handful of business risk areas to scrutinize each quarter. Now we’re moving to a system in which every business risk is audited continuously. We’re closing our books faster. We’re making fewer mistakes and catching the ones we do more reliably. And, as CEO, I’ve never had better tools to measure exactly how the business is performing, including identifying our rising stars.

The vast majority of those we laid off last week were measurers. We cut middle managers across the organization because AI allows us to have more direct reports per manager while still measuring and mentoring our teams effectively.

We consolidated our operations functions into a single group that can support teams across the business, using AI to gain specific expertise when needed. We significantly reduced our marketing team, which, like in most companies, was teeming with measurers. Across our finance team, we found opportunities to consolidate and automate.

We received almost a million applicants for 1,111 paid internships this summer. The interns we hired are extremely qualified and AI-native. They’re all builders or sellers, and we expect that the majority will get full-time offers.