If you've found yourself wondering why so many on the progressive left perceive Jewish people as "oppressors," there's no better introduction to how this perspective gained traction in academia than through this 6.5-minute film by @MikeNayna, on the academic hoax known as "the Grievance Studies Affair."

Three scholars – @ConceptualJames, @peterboghossian, and @HPluckrose – submitted deliberately absurd and fake academic papers to respected peer-reviewed journals in the humanities and social sciences.

One of the accepted papers included a chapter from Hitler's "Mein Kampf," with the phrases "our movement" or "party" replaced by "intersectional feminism."

Their objective was to reveal that these journals were accepting papers not based on research quality but on their alignment with specific ideological beliefs, influenced by postmodernist thought.

https://t.co/w8LRIVxEts

You can read more about the hoax here: https://t.co/aBQufi214H

Due diligence on a company or security is research. It is NOT Investment Process. Say it with me...Research is NOT process.

A sound process is the repeatable framework that governs everything: how you source your universe, how you conduct DD on a sector/company/security, sizing guidelines and/or rules, entry discipline (catalyst or no catalyst), what would make you change your mind and what you have to believe, portfolio construction, and risk management parameters.

Due dili is just one part of process.

Conflating the two is a mistake, especially when training people who are still forming habits.

see tweets (there are many!)

My wife mentioned a nice private school over dinner this week

She said the campus was beautiful

I asked what's the tuition

She said we should look at it as an investment in him not a cost

I made a note

She said don't make a note

I said I always make notes

She said this isn't a deal

I said everything is a deal

She closed her eyes

She said we'd discuss it Saturday

I agreed

Saturday 7:02am

She came downstairs in her Saturday robe

Coffee in hand

I had my cargo shorts on

The dining room had been cleared

The projector was on

The analyst was at the head of the table

Quarter zip on, three iced coffees, a legal pad, and two laptops

He had been there since 6:44am

I texted him at 11:14pm Friday

The text said dining room 6:45am bring the model

He sent a thumbs up

My wife stopped in the doorway

She said what is this

I said you said you wanted to discuss it

She said this is not a discussion

I did not respond

She sat down anyway

The analyst stood

He said good morning ma'am

She did not respond

He sat back down

A printed deck in front of each seat

A fourth copy in case

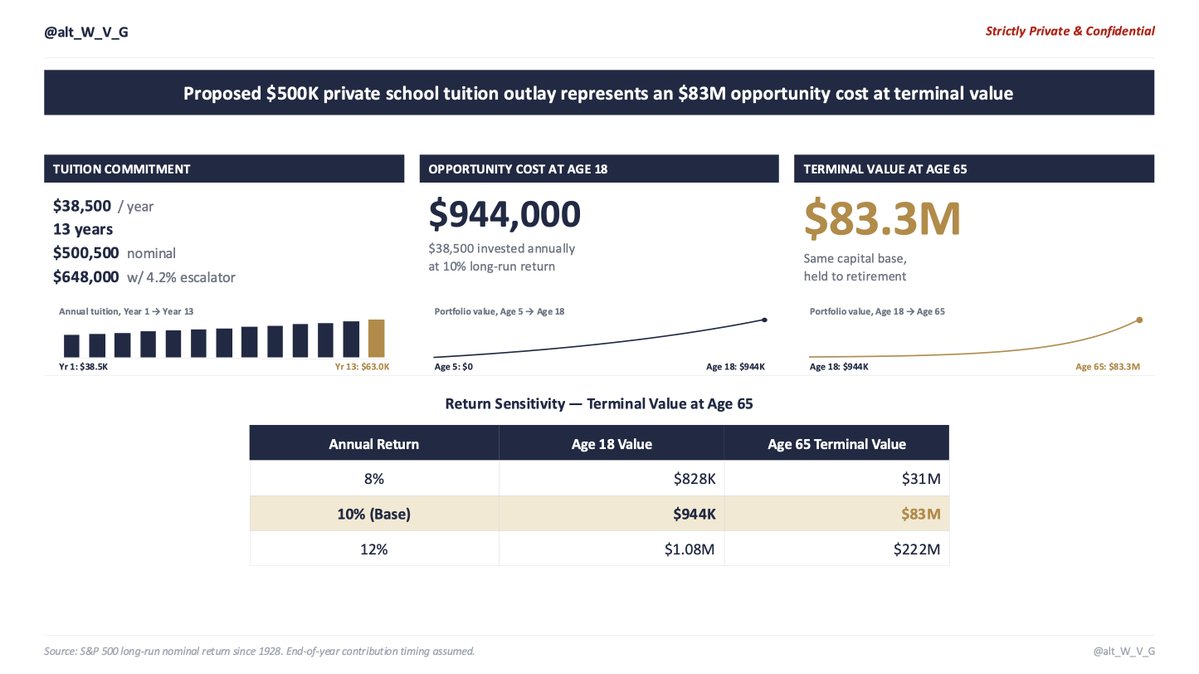

Slide 1 Tuition Schedule

$38,500 per year

Thirteen years

$500,500 nominal

Before escalators

The school has raised tuition 4.2% per year for a decade

With escalators $648,000

My wife said okay

I said I'm not done

Slide 2 Opportunity Cost

Even before escalators

$38,500 invested annually

10% nominal return

S&P long-run average since 1928

By his eighteenth birthday $944,000

My wife said we can afford it

I said I know that's not the slide

Slide 3 Terminal Value at Age 65

$83 million

She was quiet

The analyst slid the sensitivity tables across the table

8% return $31 million

10% return $83 million

12% return $222 million

She did not look

She said this isn't about money

I said it's always about money

She said no it isn't

I said then what is it about

She did not answer

She said you can't put a dollar value on his teachers his classmates his environment

I said I can the analyst already did slide 6

He flipped to slide 6

She did not look

She said the school is the best in the city

I said best is a feeling

She said it produces the best students

I said the students were already the best before they got there

She said our son deserves it

I said our son deserves $83 million

My son walked in

He is five

Dinosaur pajamas

He looked at the projector

He looked at the open deck on the table

He looked at slide 3

He said are we modeling pre-tax or after-tax

The analyst opened a new tab

My wife looked at the ceiling

He said what's the discount rate

The analyst set down his pen

She closed her eyes

He said is this the same return assumption from the 529 conversation

The analyst stopped typing

He looked at me

I did not say anything

She stood up

Sat back down

He said dad can I help

I said yes

He pulled up a chair

The analyst handed him a printout

He started reading

My wife watched him read

She watched him for a long time

She said his name

He looked up

She said do you like school

He said the work is too easy and the kids don't ask questions

She did not respond

She looked at the ceiling

She walked out of the room

The analyst started packing up

He said should I follow up Monday sir

I said no follow up needed

He'll be fine

Sent from my iPhone

In markets, we follow the economy, earnings, valuations, the Fed, inflation, regulatory policy, fiscal policy, and global affairs for a common reason: to seek insights on the direction of asset prices and to evaluate risk/reward.

We live in an era of profound uncertainty with both huge opportunities and threats. In this context, here are 5 critical questions:

UNCERTAINTY #1: Is the stock market in a tech bubble? Have we pulled too much forward with respect to valuations?

UNCERTAINTY #2: Has the Iran war already lit the inflation fuse?

UNCERTAINTY #3: Is the Treasury market at risk of its own crisis? Is US government debt a source of instability?

UNCERTAINTY #4: Will anything close to the Citrini memo materialize in white-collar job loss?

UNCERTAINTY #5: Will private credit concerns intensify? Can we muddle along or is there potential for a contagion event?

To all parents with kids under 10: enjoy these years. Right now you’re their hero. Their protector. Their best friend.

Then they turn 13 and suddenly you’re a complete moron because you asked them to unload the dishwasher. Overnight you’ve become the dumbest, most embarrassing creature on Earth whose only purpose is to exist in the basement, and never make eye contact with them again.

Parenting is a scam. 10/10 would recommend though 😂

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time.

He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha.

He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life."

He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett.

But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them.

Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does.

Enjoy!

Timestamps:

0:00 Intro

1:00 The Kindest Thing

13:19 Trading vs. Investing

17:33 Lessons from Warren Buffet

22:24 The Existential Risks of AI

29:54 The Nature of Trading

31:46 Bitcoin

35:55 Bubbles

42:08 A Day in the Life of PTJ

46:00 Information Overload

47:07 Passion for Markets

50:49 The Robin Hood Foundation

54:18 The Workless World

56:03 Journalism

1:00:00 Principal Components of a Great Life

1:05:06 Kill Them With Kindness

Now that Medallia is officially a default... this will be the $BXSL Blackstone BDC's largest one to date and one of the very few that have stained its portfolio $BX

Will likely have to be marked down again:

Blackstone Secured Lending Fund ($BXSL), a major BDC, has significantly marked down its large, roughly $380-$400 million debt exposure to Thoma Bravo-backed Medallia, marking it at 78 cents on the dollar by early 2026, down from 87 cents in mid-2025. This reflects distress in a top holding, formerly over 5% of net assets, due to software sector volatility and company-specific execution issues.

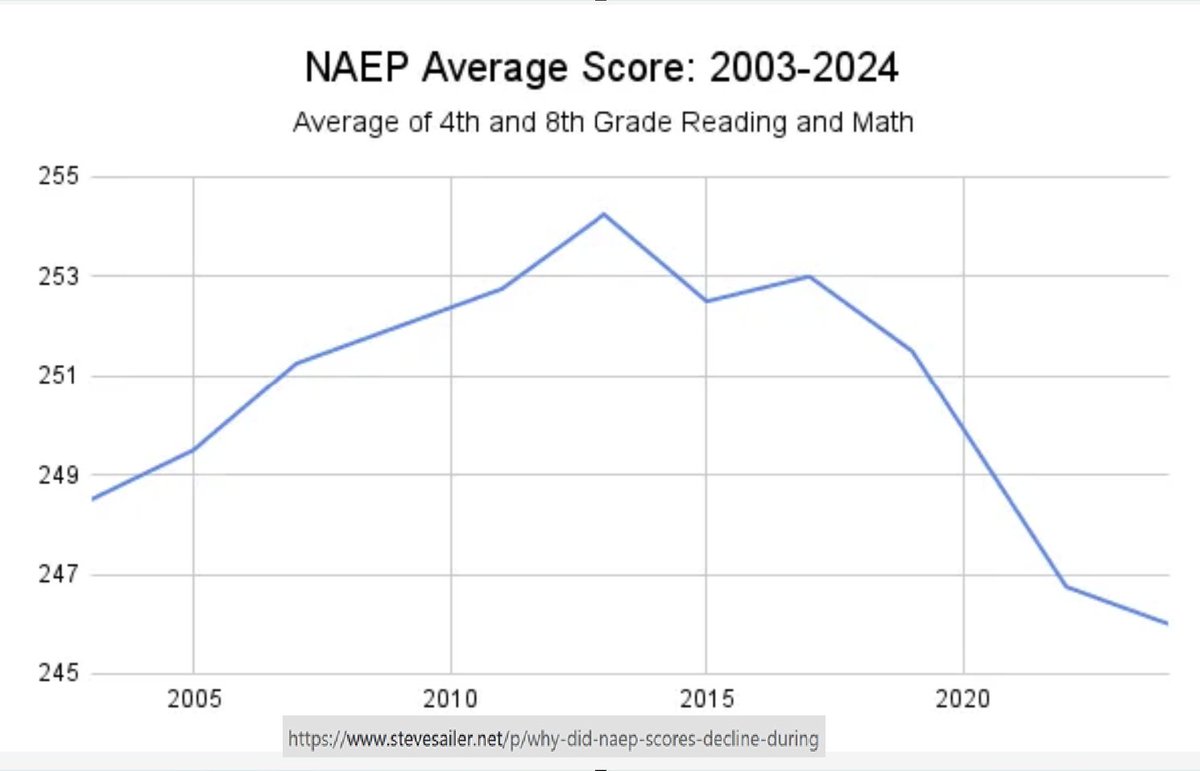

The erosion of K-12 accountability at all levels—districts, schools, teachers & students—since 2016 has corresponded with a drop in outcomes. The fad of the moment in education is "science of reading", but without addressing low standards, curriculum changes alone won't work.

1/n

1/10 The U.S. naval blockade of the Strait of Hormuz would cost Iran approximately $276M/day in lost exports and disrupt $159M/day in imports, a combined economic damage of ~$435M/day, or $13B/month.

Over 90% of Iran's $109.7B in annual trade transits the Persian Gulf. Oil/gas accounts for 80% of government export earnings and 23.7% of GDP. Kharg Island alone generates ~$53B/year, or as I noted to @TIME, "$78 billion a year in energy revenue.

GEOPOLITICAL RISK IS THE HARDEST RISK TO TRADE

IMO, traders have discounted the Iran situation bc nearly all conflicts resolve without crazy escalations. The world is incentivized towards peace.

It’s a REALLY good heuristic. Genuinely it is the right heuristic, MOST of the time!

In fact, that is why for almost a decade I’ve faded geopolitical risk premium as described in this video (https://t.co/gReTd9yV86)

The issue is… this situation is different and in a complex world w complex players, crazy stuff can and inevitably does happen.

I’ve said so from day one. This situation is different bc an irreplaceable amount of oil production has been shut-in while two sides remain diametrically opposed.

For Trump: it is a nonstarter that Iran has any uranium enrichment or a path to nuclear weapons.

For Iran: it is a nonstarter that Iran does NOT have a uranium enrichment program.

BOTH countries view their stance as an EXISTENTIAL position.

For over a month now, I’ve read takes that this will be over ASAP and that it’s de-escalating. I’m not an expert. But neither are these people.

The experts like @kpler and @EnergyAspects are still freaking out at the amount of energy that is shut-in and are skeptical of how this resolves.

The reason why most on Twitter aren’t freaking out is bc most on here are looking at the S&P500 while living in America or an energy-secure nation.

Huge chunks of the world are ALREADY in a full-blown energy crisis that is already resulting in starvation and death. That sounds hyperbolic, but it’s not. It’s hyperbolic bc you reading this are financially secure when most of the world isn’t.

Meanwhile, escalation from here is still always possible (see today’s weekly Sunday morning Truml tweet full of insanity).

Yes, by some miracle, one side might fold.

But the main point of this post is to say: “yea, but maybe not and meanwhile every day that passes is catastrophic to huge portions of the global population.”

With geopol risk, heuristics are just that… a good rule of thumb that you can use as a guide but not a predictive tool.

Instead of watching Netflix, watch this 1-hour Yale lecture by Professor Ben Polak.

It will change how you think about decisions in negotiations, business, and everyday life.

The Phone in the Limo is Busted

The "buy the dip" mentality floating around software right now feels a lot like pattern matching to the wrong cycle. This is not meant to be or sound like a generic bear porn take. I am attempting to share my observation about the quality of information available to make that bet, and the reliability of the signals people are using to make it. I've written about the private markets mechanics and the credit backdrop separately (use the twit search function for more background). In this post I am going to attempt to bring it together a bit more...

Let's start with the mosaic. The BTD ("buy the fcking you dip, you fcking moron - https://t.co/bgfQVq7w5d) crowd isn't necessarily wrong about any single piece of this. Slowing growth alone, 'seems' manageable. Multiple compression alone if history is any guide (I don't believe it is...), potentially an opportunity. AI disruption narrative alone, maybe overblown for specific names (feels that way, but I can't prove it...can you?). Rising debt alone, depends on the asset. PE overhang alone, slow moving but they are actively playing defense in lights. But when I take a step back, you have all of them simultaneously, and you're weighting them selectively to support a position you already want to have. Essentially, I see cherry picking one name that checks two or three boxes is not the whole picture.

The signals people are leaning on to support that rationalization are broken.

Let's start with the obvious one...management guidance. The visibility that made SaaS guidance reliable is genuinely impaired right now. AI impact on renewal rates, expansion revenue, customer behavior, nobody has clean line of sight on this. Management isn't lying. They just don't know either. The confidence required to extrapolate forward from the last four years hasn't been earned by the situation.

Next let's address buybacks. FinTwit loves pushing buybacks as this panacea. Borrowing money to retire shares is not a vote of confidence in the business from my perch. We are witnessing 'earnings per share management', SBC dilution control, and in some cases financial engineering to hold a stock up that is doing real operational work as a retention and recruiting tool. Next, when the terminal value question is genuinely open, levering up against an uncertain denominator is a wild risk to take. The buyback benefits the people making the decision more directly than it benefits you the investor (good for the traders).

One of the most oversold narratives in investing is insider buying. I mean, don't get me wrong, I like when insiders of the companies I am involved with buy stock. I privately encourage insiders, who have a great feel for their forward looking prospects to get ahead of it as a signal to market participants, and for their own wealth generation to buy stock before the path is obvious to others... But keep in mind, that many of these executives are already wealthy (I could give you some great stories about encouraging insiders at Nexstar to just do this before several material earnings inflections).

Let's address something and just say it directly...seat risk and livelihood risk are not the same conversation. A $1M open market purchase when you have $40M in stock and options is an extremely cheap signal to send, and the market treats it like something big/game changing that costs something real. The asymmetry between what it signals and what it actually costs them personally is too wide right now to carry the weight people are putting on it. Get your mind right.

I am not here to shit on the sell side. The research space is a tool, that's it! But let's discuss sell side estimates. The models were built for a world of predictable recurring revenue and stable competitive moats. The adjustments being made to those models are just educated guesses about something with no real historical precedent. I am genuinely not making a criticism of the analysts making the estimates and revisions call or changing the price targets after the stock or sector gets walloped, but its their job and they have the incentive structure to match that seat.

There are also a lot of narrative violations occurring with large PE sponsor(s) commentary in the press. When Thoma and Vista are making the media rounds reassuring everyone about portfolio health, that is the only lever they have left, and I don't really see this as a datapoint with a lot of merit. So as of now, they aren't walking away from their companies, and why should they? They are not handing keys to lenders (yet/now), and why should they? But let's take a 2021 or 2022 vintage deal, bought at 10 to 14 times sales, financed at 7 times leverage when debt cost 9 percent (wrap deal structure), in a business that has slowed from 25 percent growth to 7 percent, with comps that have re-rated from 10 times to 3 or 4 times sales, with debt that now costs 13 percent. The math certainly works less efficiently now, and there is a case to be made that on paper the equity is impaired, and the IRRs presented 6-9 months ago are pretty much unlikely to be realized. The marks don't reflect it because nobody in the ecosystem has the standing or the incentive to force the issue.

And let's be honest about why the media tour is happening at all. The exit market is essentially closed (other than the full pamp private deals where they are "reserving space" for retail...yikes). IPO into this? For what audience and at what price?

The strategic buyer universe, your Oracles, your Salesforces, Constellations, SAP, has pulled back. The competitive bidding situations between Thoma, Vista, KKR, Blackstone and the long list of other capable strategics that made 2020 to 2022 feel like a permanent bull market for these assets, those are gone, at least for now. It's opportunistic now and sparse, and the optics of what deals you do matter as much as the economics and snap shot accretion.

The special dividend recap at 2022 terms with 25 lenders fighting for allocations? Not happening. So what's left? Merging portfolio companies that you wouldn't normally put together to cut OpEx. Rolling assets into continuation vehicles to buy time and avoid a new mark. Selectively selling the winners to show LPs some DPI and prove the fund is working, while the weeds sit on the books marked at something that has no real buyer to test it against.

Someone will respond to this with a one off deal example as if it really matters. Ask yourself whether that sponsor is doing it because the setup is genuinely compelling or because they need liquidity and think they better move before it gets worse.

We will also almost certainly see a sponsor pay a multiple materially higher than where public comps are trading, and a lot of people will call that a re-rate signal for the sector. It ain't. Get your mind right.

You bought $80 to $100 billion of deals at 8 to 14 times sales two to four years ago and now you're telling your investment committee you're hunting in a world where deals are 2 to 6 times sales.

Someone is going to respond to this post and immediately jump right to but but but, software multiples are cheap versus history. This is the most seductive and probably the most dangerous signal of all. Insert its a trap gif. Multiples are only cheap relative to the growth, moat, and terminal value assumptions that justified them historically. If those assumptions have structurally changed, the historical comparison is a false anchor.

The prior cycles where buying software on a drawdown worked, 2016, 2018, 2022, those were multiple compression events. Those business models were intact. Terminal value wasn't seriously in question (I am sure a few were...so come get me in the comments). The lending environment recovered. You could trust the c-suite disclosed guidance (and was likely sandbagged), trust the board increasing the buybacks, and in many, if not most cases, could trust the moat. This is a different set of conditions and the old toolkit doesn't cleanly apply.

So what does real underwriting look like here and now? The framework and variety of checklists that involve unit economics that genuinely benefit from AI or true insulation from it, improving earnings revisions (rate of change), no material pricing degradation, clean balance sheet, straight forward formulaic and opportunistic honest capital allocation that is all spelled out and aligned with governance and incentive compensation structures. Almost nothing in software passes all of that simultaneously right now is the way I see it. But the more difficult issue to contend with, is that even if you find something that does, the work is just beginning and you have to keep verifying. This environment requires dynamic re-underwriting as conditions shift, which adds real stress to longer duration investing in a way that sitting back and letting it work and play out is a tough way to approach this, is my view.

I look at this approach as the lazy approach with excuses like I have a mandate that allows me to be patient and I have earned the trust of my LPs. PSA: I would be very careful with this assumption... And for a lot of people it's genuine conviction that it resolves the way it always has. Maybe it does...and perhaps it will.

This is what I keep coming back to...The AI disruption risk is probably somewhat overhyped. I think that (I don't necessarily have a convicted belief in the statement). I just can't really quantify it, I certainly can't qualify it with any real precision, and I have no honest way to weight that assumption in a model (do you??). I would be careful of anyone telling you they can issue spot this with conviction and are sizing up the opportunity as a long duration investment (this is not a TRADING DISCUSSION POST - yes if semi's sell off, software will prob bounce!).

The phone in the limo is busted. The signals that used to tell you where you were and where you were going aren't working the same way anymore.

More comin'...this much I promise you.

Best,

Mojo