Every Breath Connects: The Atomic Components of the Human Body

With every breath I build millions of atoms into my body that already belonged to Aristotle, Gandhi, Goethe, Buddha, Graham, Buffett and YOU :-)

https://t.co/dwy0uIV5gO

Price-to-Sales Ratios of the Three Largest Global Companies (as of 03/11/2025):

📊 Apple: 8.8

📊 Microsoft: 10.8

📊 NVIDIA: 20.1

A timely reminder from Scott McNealy, former CEO of Sun Microsystems, who called out the absurdity of high valuation multiples back in 2002:

“Two years ago we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don't need any transparency. You don't need any footnotes. What were you thinking?“

Valuations don’t matter—until they do. 🚀

#Valuation #ContrarianInvesting #TechBubble

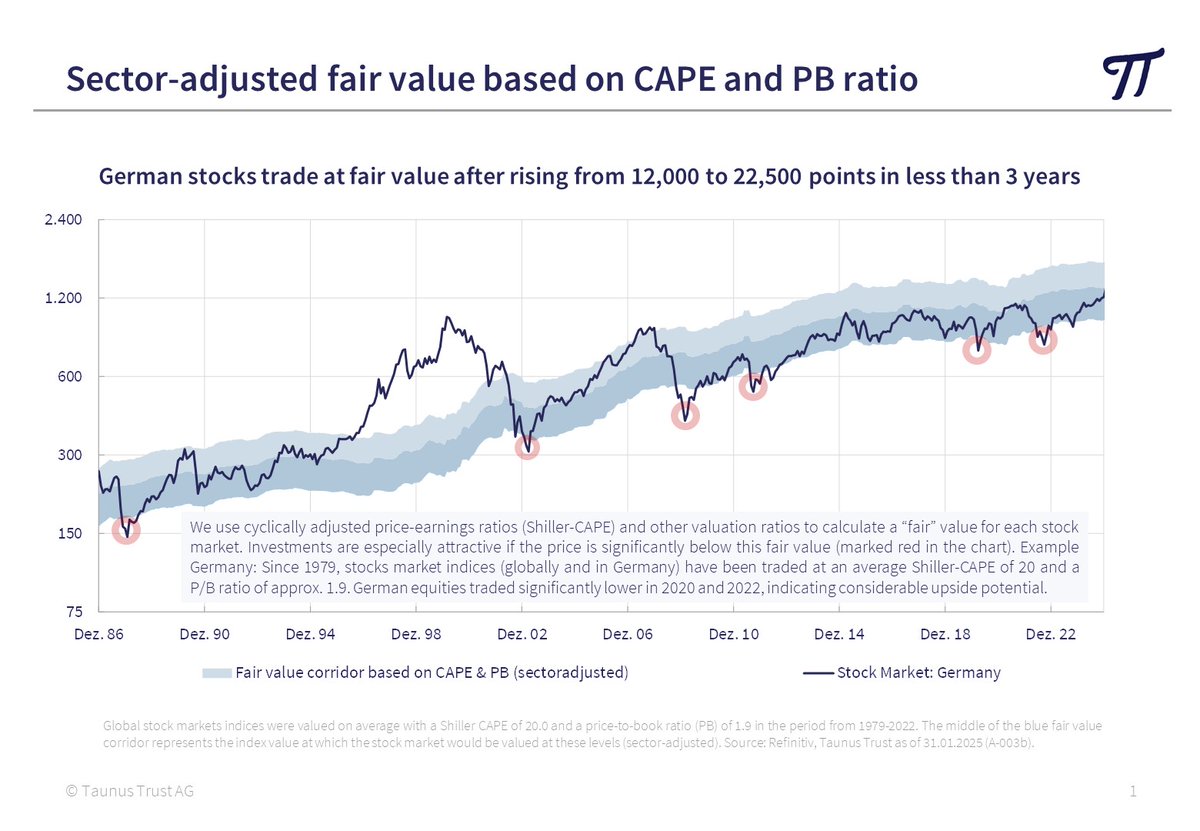

Sector-adjusted fair values based on CAPE and PB ratio

🔹 German stocks trade at fair value after rising from 12,000 to 22,500 points in less than 3 years

🔹 Emerging Asia is trading 20% below fair value and currently offers interesting opportunities

🔹 Expensive sector-adjusted valuation in the US stock market has now reached levels last seen during the New Economy bubble in 2000 – a clear warning signal.

📊 Background information on our valuation models, including sector adjustment, can be found in our article https://t.co/oK2Oe1tjAJ

#FairValue #CAPE #ContrarianInvesting #EmergingMarkets #DAX

Stock Market Update: Sector-Adjusted Country Valuation

Country valuations can be misleading due to differences in sector composition. For example:

○ Denmark: 70% consists of (always) expensive healthcare stocks

○ Taiwan: 80% is concentrated in IT sector (just 26% MSCI World)

🔎 Our approach: Adjusting valuations for different sector structures allows for better comparability and more accurate forecasts.

Sector-adjusted stock markets return forecasts (10-15 years):

Latin America & Emerging Asia: >7% p.a.

Developed Asia & Europe: 6% p.a.

USA: 0.8% p.a. (sector structure only accounts for ~10% of high valuation)

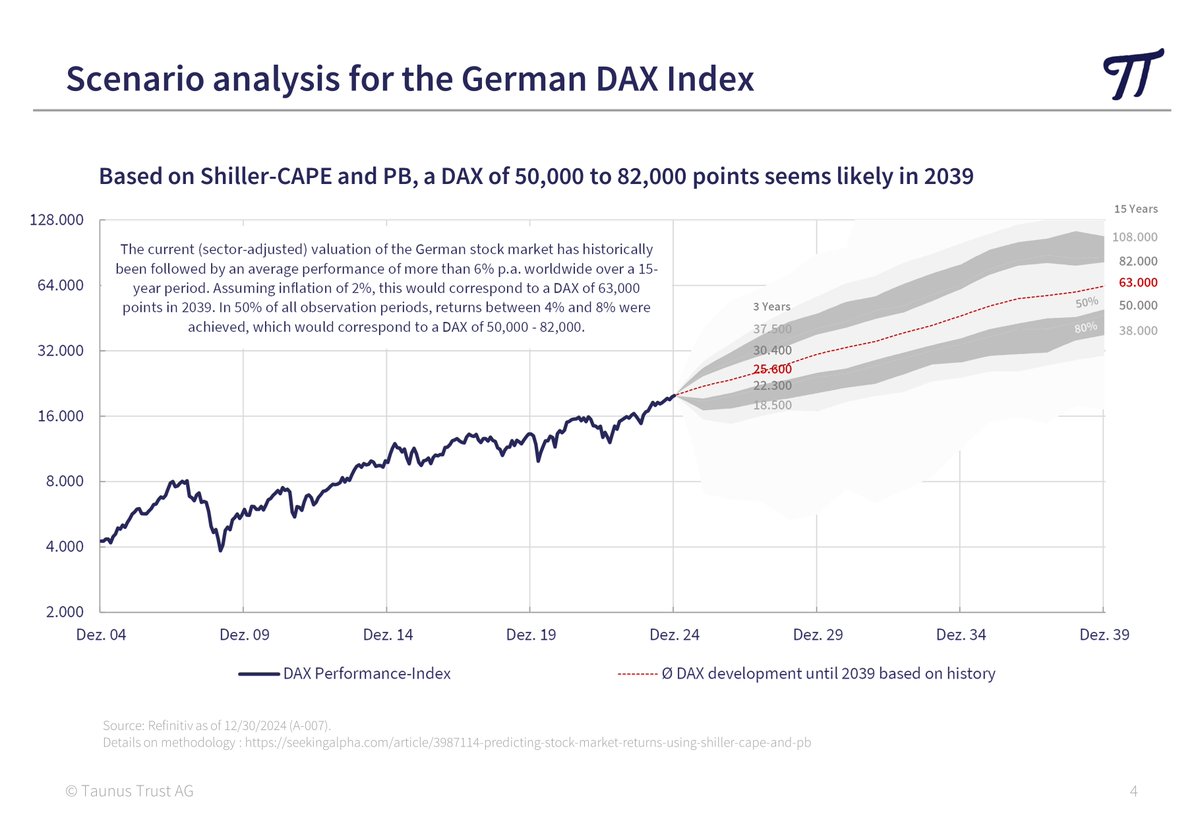

📈 Germany vs. USA – long-term scenario analysis for stock market returns

Germany: Sector-adjusted DAX valuation suggests 6.8% LT performance and a range of 50,000–82,000 points by 2039. From an empirical perspective, it seems unlikely that the DAX will be lower at the end of 2027 than it is today.

USA: High valuations imply low returns, with a 50% probability of the S&P 500 remaining below today’s level in 2039(!!)

📊 Further details in our current article https://t.co/XVRCiMNeVn

Webinar zu unserem Huber Portfolio SICAV mit Co-Fondsmanager Jan David Meyer, CFA startet in 30 Minuten. Interessenten können sich anmelden unter: https://t.co/Fbz0DvX6XX

Thema: "Der lange Atem der Antizyklik"

Wird spannend :-)

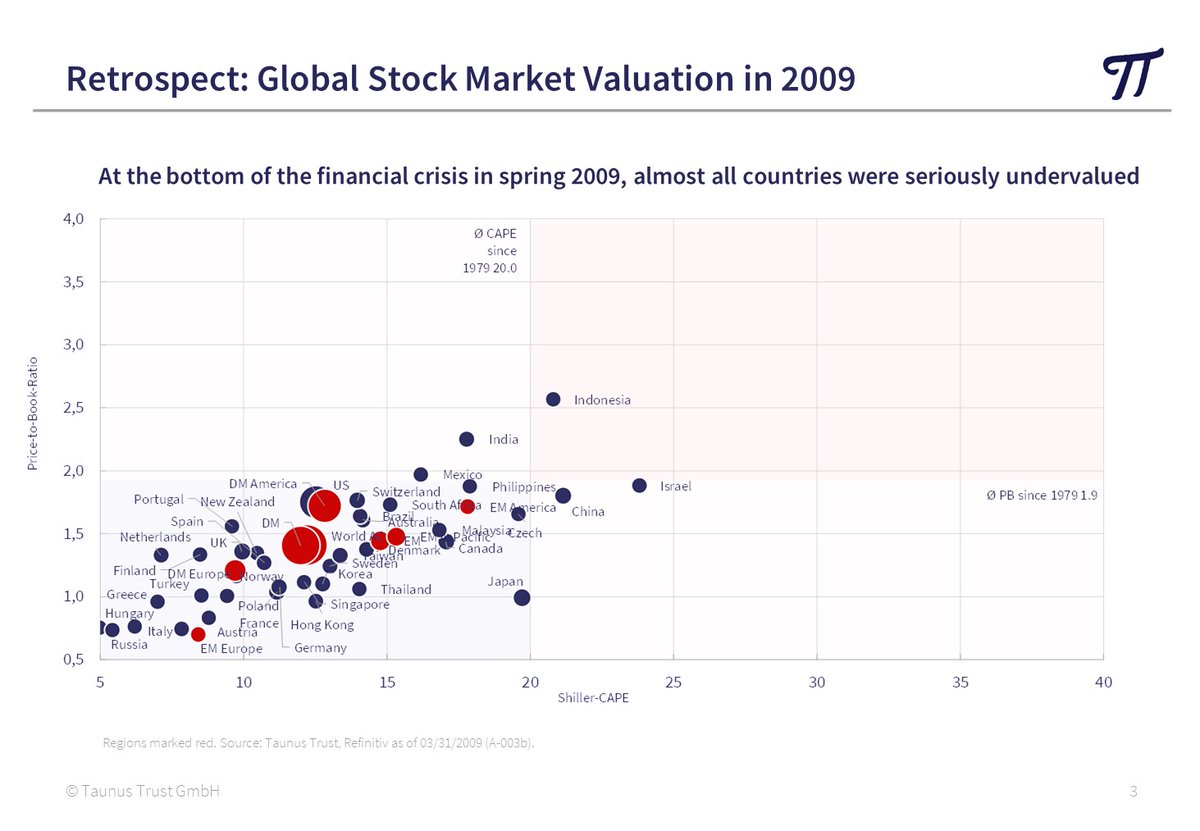

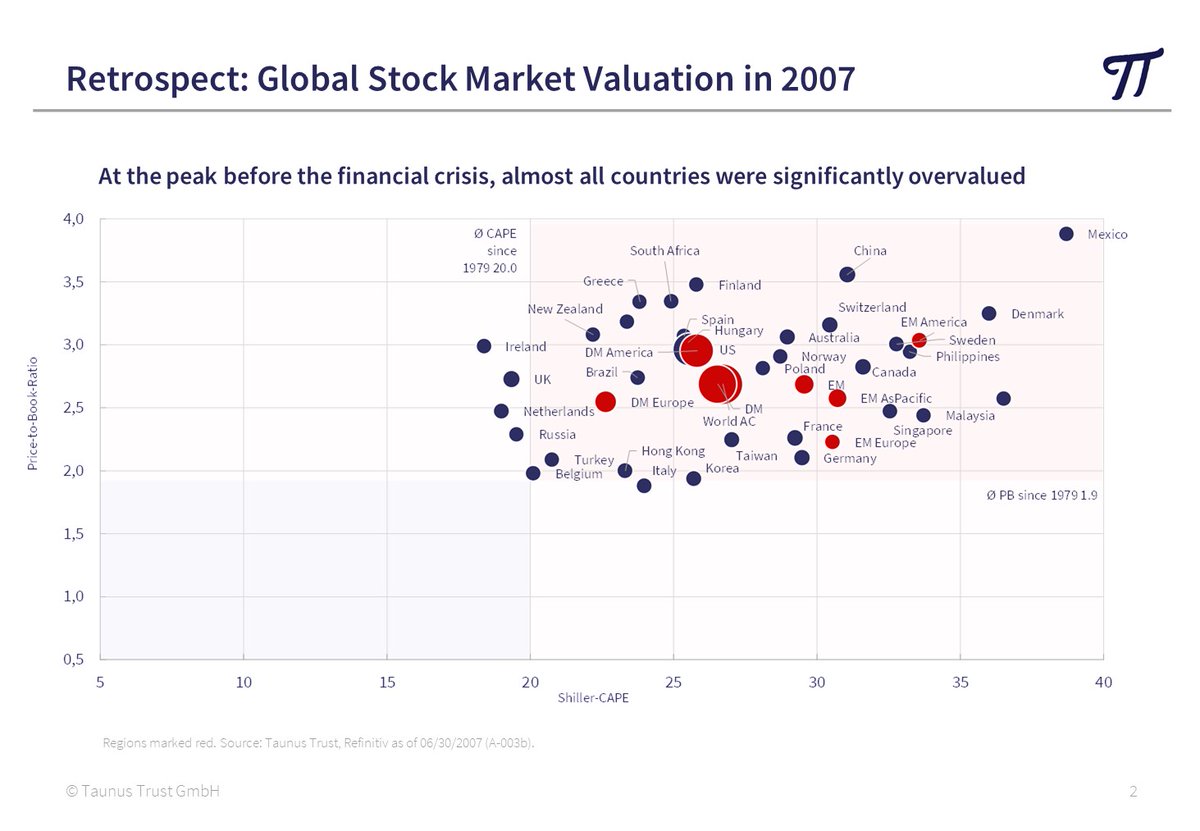

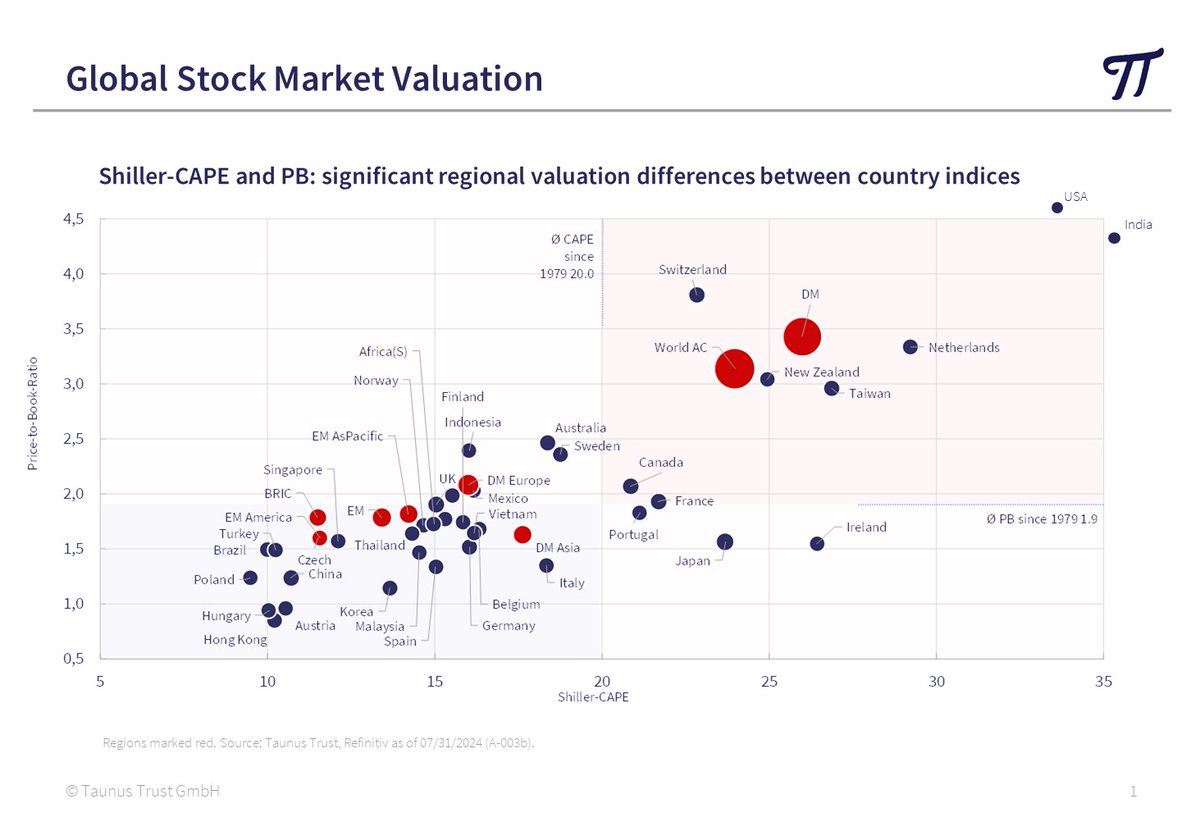

🌍 Global Stock Market Valuation Update as of 07/31/2024

As measured by the Shiller-CAPE and P/B ratio, only 13% of global equity market capitalization is undervalued today, while 76% is above long-term valuation averages. The valuation of USA and India is exceptionally high, even off the chart scale (Charts 1). Conversely, numerous stock markets in Emerging Asia and (Eastern) Europe are significantly undervalued.

➤ Current Valuation compared to historical extreme valuations (chart 2 & 3):

Today, we are far from either extreme in many markets, but the extremely high valuations of the index heavyweights could hold great potential for disappointment, especially for passive ETF investors who focus their investments there.

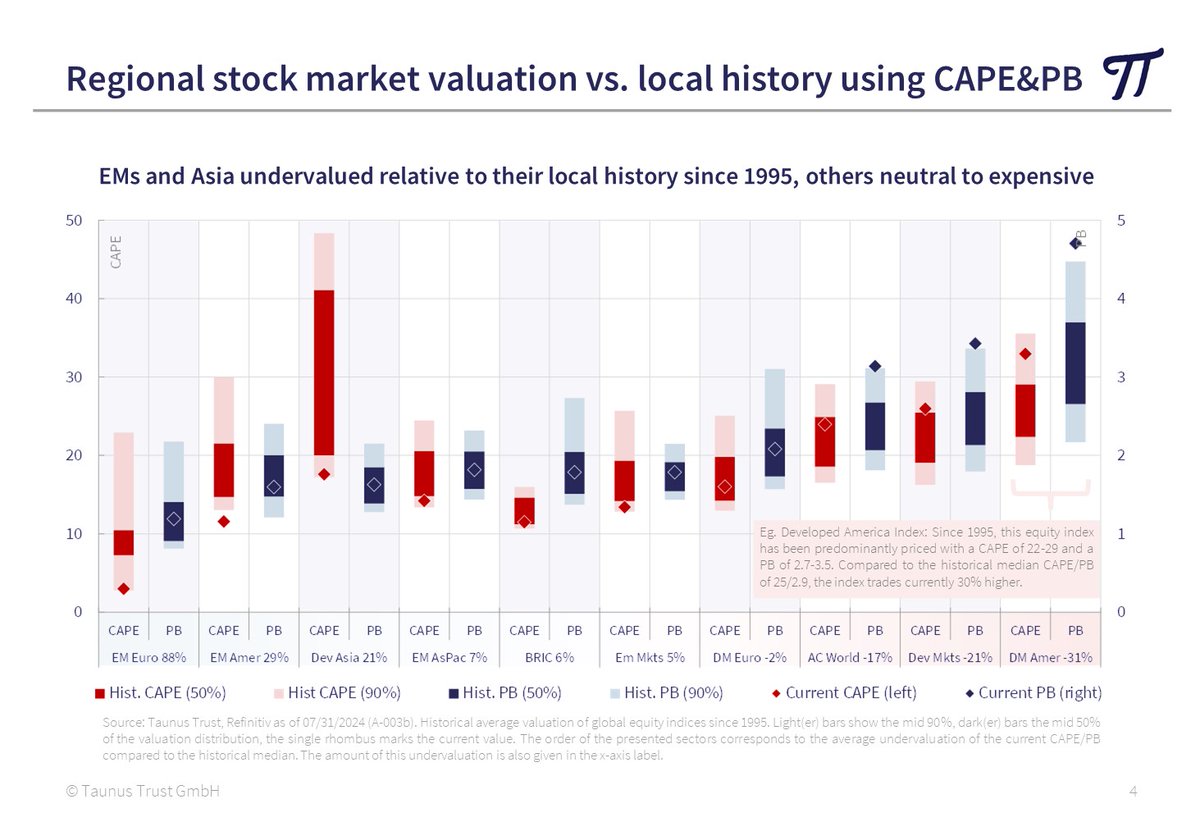

➤ How expensive is the stock market valuation compared to local history (chart 4)?

The US market is currently trading 31% higher than in the period 1995-2024. In contrast, Emerging America, Developed Asia and Emerging Asia are attractive, trading 29%, 21% and 7% below their historical valuation averages.

#StockMarketValuation #ValueInvesting #Stocks #CAPE

Wachstumsaktien haben die letzten 10 Jahre alles überflügelt, die Anleger sind bis zur Halskrause investiert und die Bewertungen teuer. Keine gute Kombination...

https://t.co/jSaCFz9B3W

Value & SmallCaps: Did the great rotation start in these quiet summer days?

In the last 10 days, global small caps were up 3%, while large caps were down 3%. Such a 6% spread has never been measured since at least 1993 (Chart 1)!

Value stocks have also gained in the last few days, while growth stocks have lost 6%. A 7% performance difference in just 10 days is also close to the historical extremes of 2000, 2009 and 2020 (Chart 2).

Whether the great rotation will start now is of course completely uncertain - even if it is overdue in view of the extreme overvaluation of growth stocks (Chart 3). But if it comes again in my lifetime 🎉 , the beginning could look exactly like this and it would surprise a large number of investors...

Überaus sehenswertes Interview mit vielen interessanten Gedankenanstößen von dem Wissenschaftler @MatthieuRicard, der Mönch wurde. Einige interessante Inhalte:

- Achtsamkeit in Unternehmen?

- achtsam tötende Soldaten

- Homo oeconomicus kann gravierende Probleme unserer Zeit schon auf Grund der Fristigkeit nicht lösen

- Karma - westliches Verständnis hiervon hat wenig gemein mit östlicher Theorie

https://t.co/JTavoNG7u4

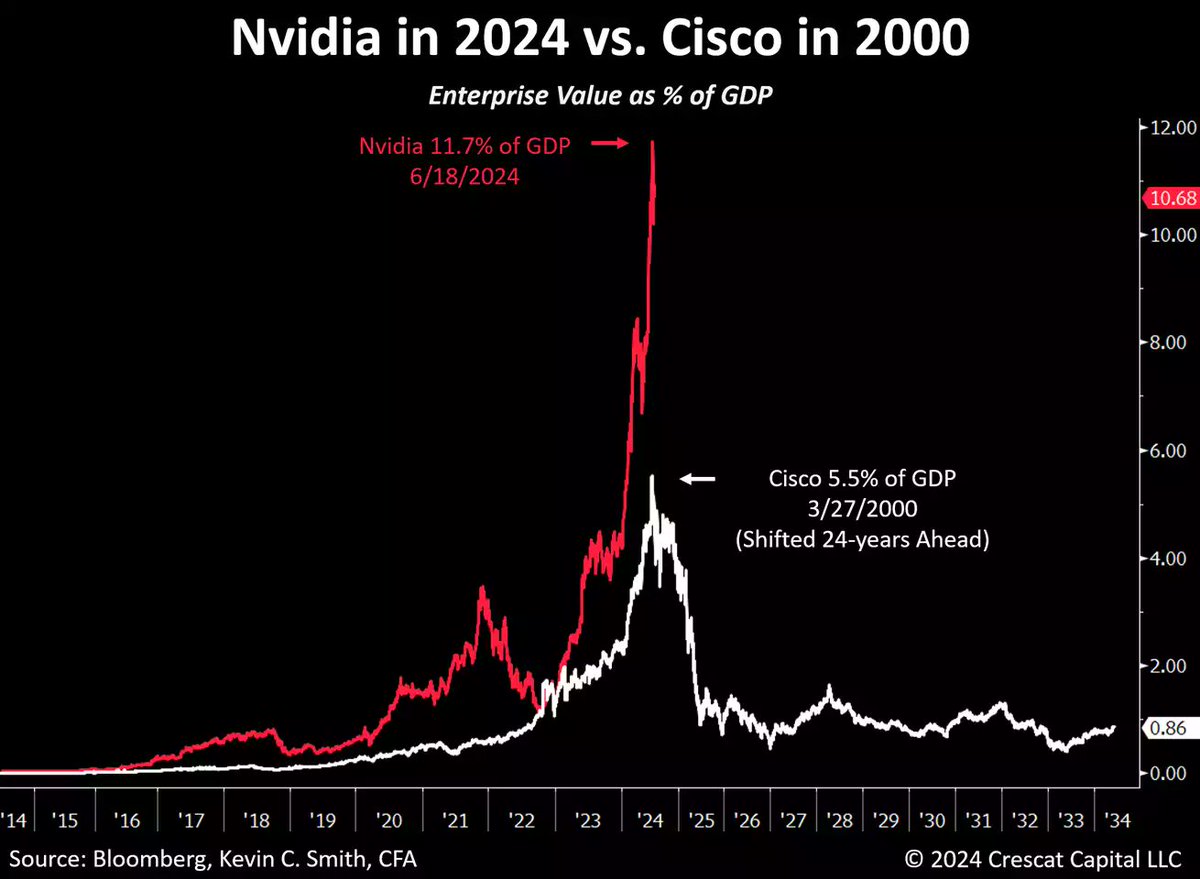

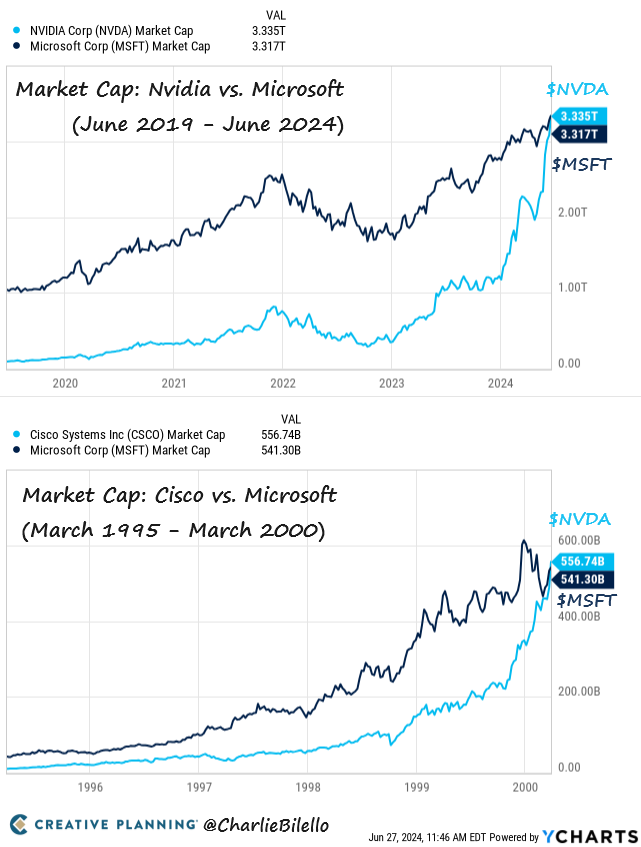

'Nvidia recently earned the most valuable company in the world status with an EV of $3.3 trillion, a record 11.7% of total US GDP at its recent peak on June 18, more than twice as high as Cisco's achievement in 2000.' https://t.co/9iRREyQ11a by @Crescat_Capital@TaviCosta

"Throughout history, certain companies have dominated the equity market, but the process of creative destruction makes staying on top for long periods of time very difficult. (..) Over long periods of time, almost all champions are dethroned."

https://t.co/yQYOZMbSba

good luck for the today's champions: #NVIDIA #alphabet #amazon #apple #meta #lilly #broadcom #jpm #tesla

At its peak in March 2000, Cisco briefly passed Microsoft to become the largest company in the world.

At its peak last week, Nvidia briefly passed Microsoft to become the largest company in the world.

$CSCO $NVDA $MSFT

https://t.co/l5IYmkeySJ

Wachstumsaktien haben die letzten 10 Jahre alles überflügelt, die Anleger sind bis zur Halskrause investiert und die Bewertungen teuer. Hat sich so ein Dreiklang schon jemals auf lange Sicht ausgezahlt? Meine Einschätzung aus antizyklischer und empirischer Sicht in 12 kurzen Minuten und mit zahlreichen Charts.

https://t.co/bVVhJOpQOf

Bei Interesse an den Vortragsfolien bitte per PN melden…

Das vollständige Interview unter der Moderation von Dirk Arning von Drescher & Cie sowie Wolfgang Fickus (Comgest) und Felix Schleicher (LF - MMT Value) steht unter https://t.co/C4hRNnuTqV zum Download bereit.

#Antizyklik #Technologieaktien #Value #TaunusTrust

Geoffrey Hinton, one of the pioneers of deep learning and AI: “How many examples can you tell me about where a more intelligent thing is controlled by a less intelligent thing?”

One of the best 14 minutes I've seen on the subject of AI. A really important must watch of the week!

“There is a 50-50 chance AI will get more intelligent than humans in the next 20 years. We’ve never had to deal with things more intelligent than us. And we should be very uncertain about what it will look like.”

~ Geoffrey Hinton

Seit 2023 haben Wachstumsaktien wieder die Nase vorn. Doch die aktuelle Marktlage könnte eine Aufholjagd der Value-Aktien begünstigen. Ich werde morgen am 21. Juni 2024 um 11 Uhr auf dieses Thema im Webinar näher eingehen. Mitdiskutieren werden Wolfgang Fickus (Comgest) und Felix Schleicher (LF - MMT Value) unter der Moderation von Dirk Arning von DRESCHER & CIE.

Melden Sie sich bei Interesse hier direkt zum Webinar an: https://t.co/PiybEfZSbl