$ROK.V: a mysterious South Africa-born Israeli-resident oil & gas investor with a Russian-sounding name fails to pay for an acquisition of a Canadian oil company in time. Not stereotyping, but in fact it was never actually confirmed he had the funds available.

@toy59496 Yeah, this is one of the cases where multiples/comps don't work (if they ever do). Really need a scenario-based approach, as in the expert report - even though that turned out to be too optimistic, too.

@thewritser I'm reading it the same way at first glance, even if it's an indirect acquisition. But curious why there is no mention of that in the press releases.

@ACapitalLP Some even charge for promoting frauds like $INT.ST 😤 But solid, human research (not just rehashing corporate propaganda with AI) should be worth more.

@alvarogomezolea So you're saying they're getting €1.8bn while not giving up anything? I find that hard to believe.

I'd rather compare to the actual current valuations like TEF.

@InvestSpecial Not sure how non-binding is an "excuse", it actually means they had no obligation to sign anything and could walk away from the bid for any reason.

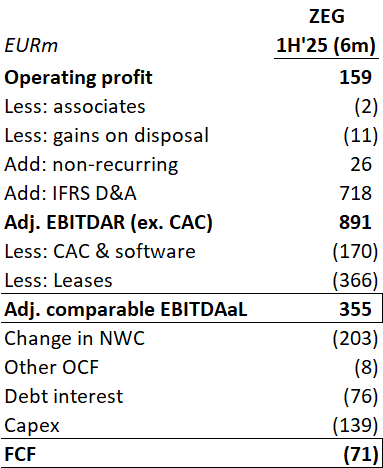

@alvarogomezolea Aren't you forgetting customer acquisition costs and loss of EBITDA to fibercos? I think their comparable EBITDAaL is more like €700m, perhaps lower PF for full fiberco divestment.

@fabreres@kingfishcap Agree, but I don’t read it this broadly. As mentioned in the TP decision, the concern was about that particular site only and about the intentions of this particular buyer (which as we have seen, has been slippery indeed).

@jupiters_string@ToffCap By looking for situations with catalysts (e.g. spin-off in the above case) and understanding valuation.

Here's Greenlight's presentation for $SOLB.BR (interestingly, they went for the basic, cyclical RemainCo instead of the speciality SpinCo): https://t.co/CSPbVTn4rz

@finphysnerd@SharogradskyM Agree with you on accountability, but 'the CEO duped us' is not an excuse in this case, even if he did - not for professional fund managers or semi-pro influencers with ks of followers. And it didn't just happen, questions were being raised already 2 years ago.

@finphysnerd@SharogradskyM It is totally wrong, this is not a mistake that can simply happen. It takes a lack of financial analysis skills, common sense and integrity.

@pradeeepk@MikeFritzell Yeah, that’s pretty much a collapsed DCF, but then FCF is affected by WC swings and lumpy capex, so need to normalise - so could just use EV/EBIT as a reasonable shortcut.