Portfolio Management 101:

1. Find factors that drive returns.

2. Measure them with principal component analysis

3. Isolate them by hedging beta:

• Get data

• Build a regression

• Short the market

Start a hedge fund.

Pick hedges by minimizing statistical dependence to factor returns, not just linear correlation. HSIC measures dependence in RKHS and detects nonlinear links (tail co-moves, volatility coupling). Compute HSIC between candidate hedge returns and factor vector on a rolling window. Choose the hedge (or hedge basket) with the smallest HSIC, then size by usual risk objectives.

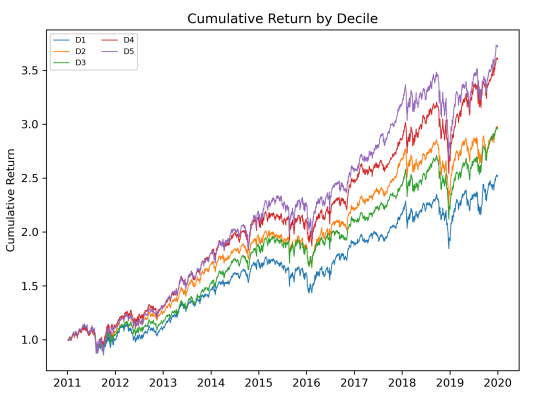

"We propose an alternative “blended” approach, which assigns 50% weight to the 12-2 return and 50% weight to the 11-2 return, then sorts stocks into deciles based on the simple average. We generalize this approach for a rebalancing frequency of N months (assigning 1/N weight)."

The MMer mispriced the parlay, but then continued selling over many trades and there was presumably no alert to a human or no human responded to the alert that says you've been lifted X times in Y seconds which I'd think is still a protection MMs code into their systems

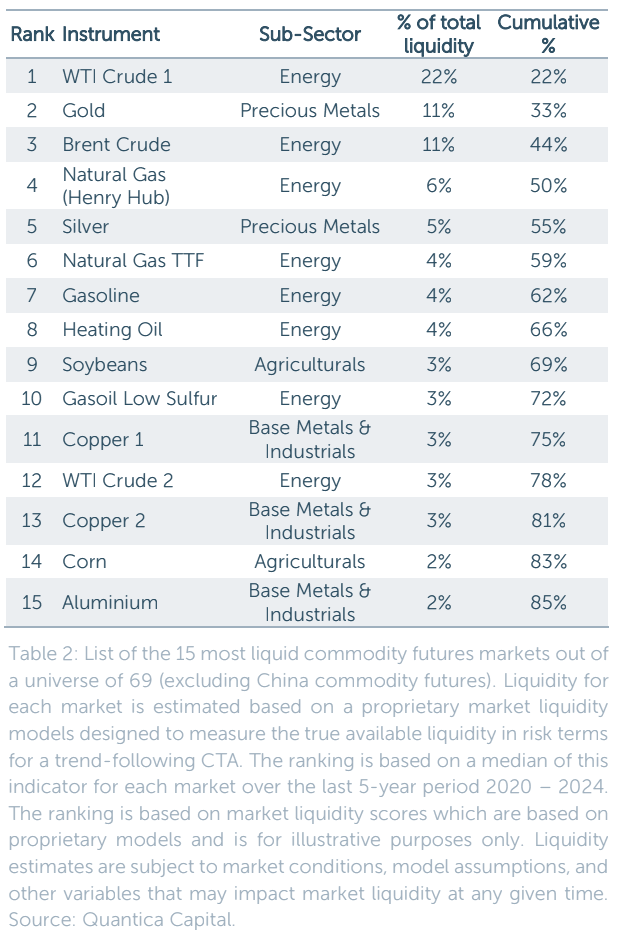

"Commodity futures liquidity is highly concentrated: out of a universe of 69 commodity futures, the 10 most liquid account for 70% of the total liquidity across all available commodity futures, with energy futures alone accounting for 55-65%."

https://t.co/SClrQuQSgF

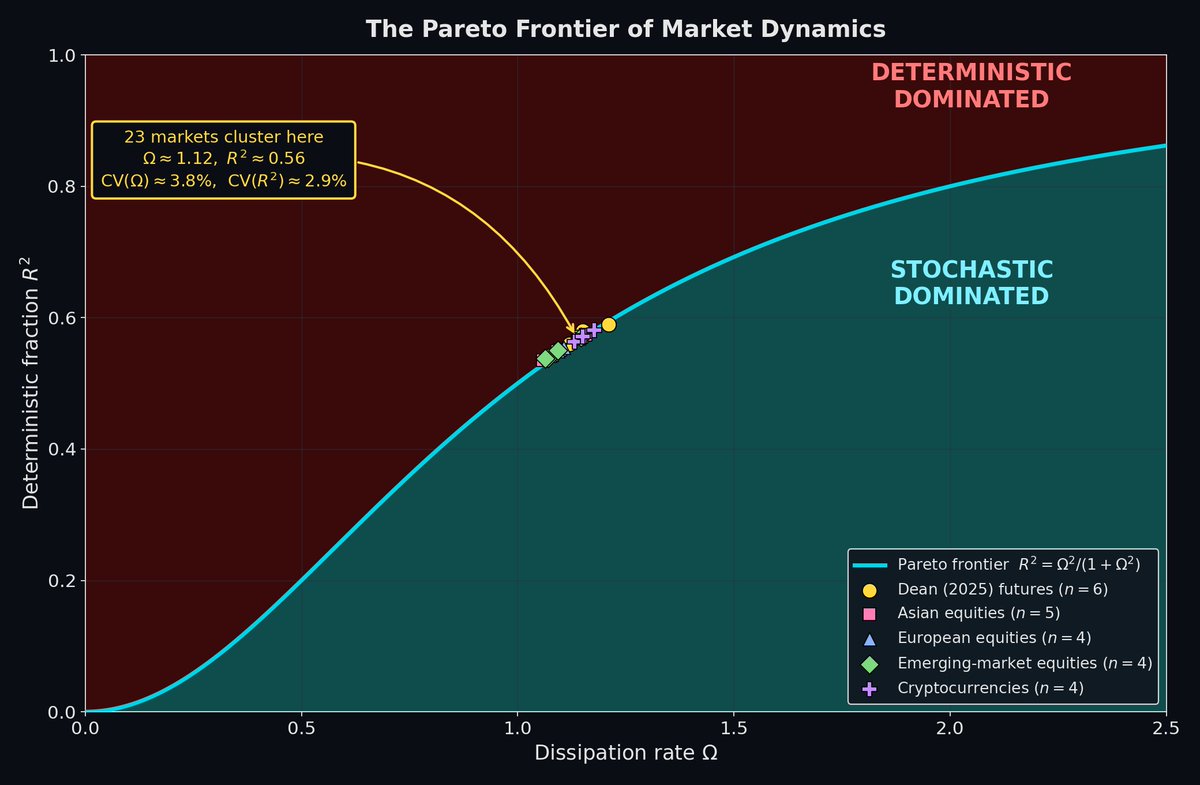

Notes: Closed-form identity relates variance to thermodynamic coupling. No fitted params. VRP is mispriced because pricing ignores the market's information geometry. 23 markets across 5 asset classes fit within 4.5×10⁻⁴. Thermodynamic coupling exposes predictability.

Treat the pair/basket spread as a random variable with a rolling distribution. Each day you compare today’s (recent) spread sample to a reference historical sample using a kernel two-sample distance. MMD detects distribution shifts beyond mean/variance. Stop trading when the test rejects same distribution, because the spread state likely changed.

A new Research Recap is out. Topics include:

➢ An improved commodity carry signal

➢ Long-short equity strategies

➢ Trading the EIA report with LLMs

➢ Predicting option returns with LLMs

➢ Trading on inflation betas

➢ Great blogs, industry research & podcasts

➢ ...and much more.

https://t.co/8pr3BhHAWQ

When Trend-Following Hits Capacity: A Case Study on Commodities

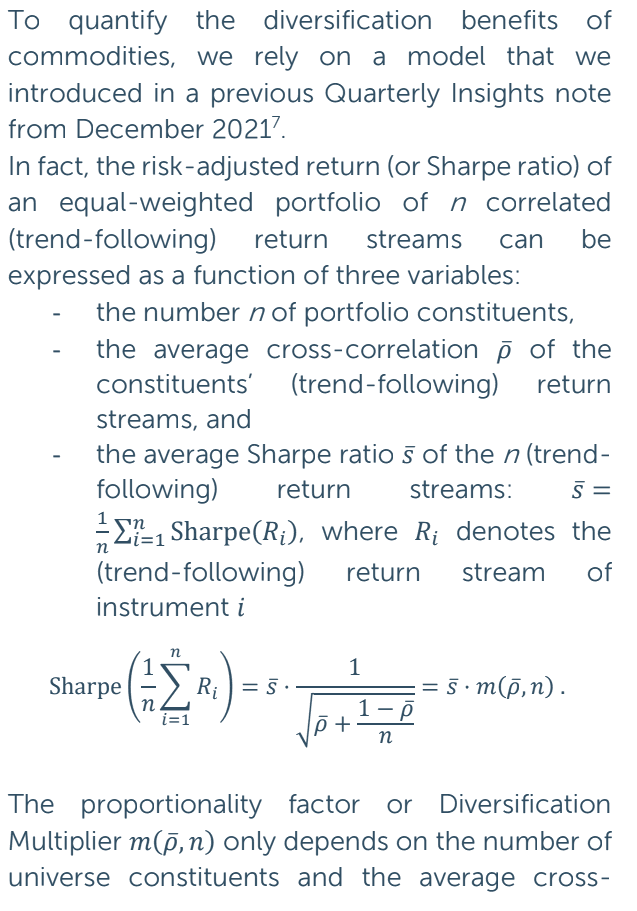

"The expected Sharpe using 69 commodity markets can be twice as high as when restricted to the 10 most liquid markets.

"It is difficult to fully capitalize on diversification benefits due to capacity constraints.

As a grad student working on Hamiltonian systems in General Relativity, I often wondered what the phase-plane approach from dynamical systems theory could tell us about markets.

Today I submitted the third paper in that answer:

Information Geometry of Market Dynamics: A Pareto Frontier from Contact Geometry.

Preprint: https://t.co/NXpR7VxFlw

and code:

Zenodo: https://t.co/uppcCQwoo1

Cryptocurrencies: BTC-USD, same methodology as the paper's SPY figure, free yfinance data. Lyapunov ellipses predicted from the fit alone; they match the empirical density with no angle or scale tuning. k=0.211, Ω=1.154, R²=0.573. Sits on the frontier within 10⁻³.

Correlation and Commodity Risk Premia (Fan, Zhang)

"A long-short correlation portfolio delivers positive average returns but is largely spanned by exposures to the aggregate market, hedging pressure, and skewness factors."

Tax Benefits of Pre-Tax Alpha (Liberman, Sosner, Freitas)

"Pre-tax alpha enhances the tax benefits of tax-aware long-short beta-one equity strategies. The positive effect of pre-tax alpha on tax benefits strengthens with leverage and investment horizon."

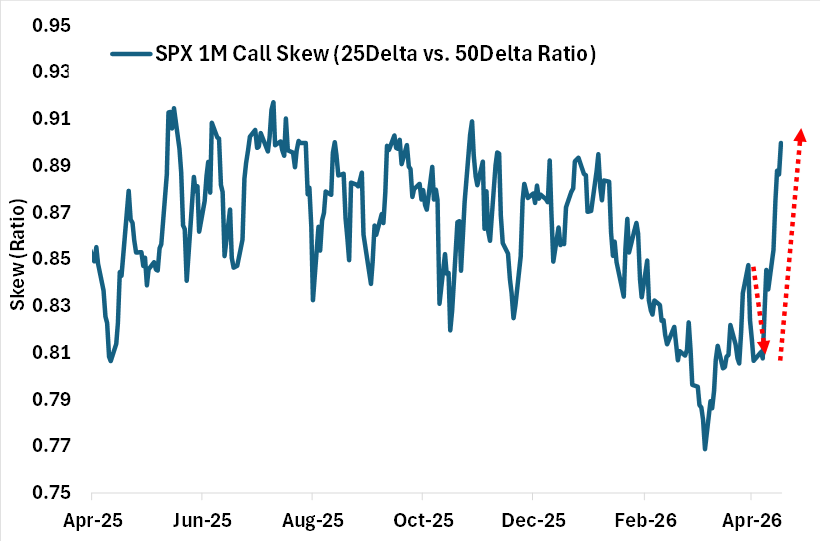

In today’s Macro Volatility Digest:

🔹Equity, rates, credit, and FX implied volatilities all fell below their long-term averages.

🔹SPX 1M call skew, a measure of demand for upside calls, has surged from near a 1-year low to now the 90th percentile high on the back of FOMO (see chart below).

🔹We’ve seen a notable pickup in retail activity in MGTN options recently, with retail flow now making up over 80% of the volume.

Download the full report: https://t.co/QqKf0wdjIs

Riskfolio-Lib is a library for making quantitative strategic asset allocation or portfolio optimization in Python.

Here's the link:

https://t.co/UtVCIjY5OI

First remove common factor structure so you model only residual co-moves. Build a graph where edges encode residual dependence strength, turning the universe into a peer network. Run message passing so each asset’s prediction borrows information from its residual-linked neighbors.

The Tranching Dilemma

What if a meaningful part of usual trading strategy’s performance has nothing to do with your signal—but simply when you rebalance? A recent paper written by Carlo Zarattini & Alberto Pagani highlights a largely underestimated risk in systematic investing: rebalance timing luck (RTL). For practitioners running rotation or factor strategies, this is not noise—it’s a structural source of dispersion. Using a concentrated U.S. equity momentum strategy, the authors show that identical portfolios differing only by rebalance day can diverge by as much as ~350 bps in annual returns, compounding into dramatically different terminal wealth outcomes.

https://t.co/gK2pPJKnGr

#tranching #trading #strategy #diversification