Leaders from @skyBridge, @paypal, and @crowe take the stage with @zGuz@coinage_media to talk about the big picture as institutions are going all in on digital assets.

From portfolio construction to balance sheets and compliance frameworks - thank you, @JohnSvolos, Larry Wade, and @SKrople for sharing your expertise with our audience.

Innovation thrives when the rules are clear. Today, CTA urged the Senate to pass the CLARITY Act so America can lead the next generation of financial technology, strengthen consumer protections, and keep jobs and investment here at home. 🇺🇸 🚀

It's 2026, and every candidate has to take a stand on crypto.

@JessicaTaylor (@CookPolitical), @zakouts84 (Mercury), and Rebecca Shaw (@TeamAvoq) on what the crypto vote looks like heading into midterms, and which races it might move.

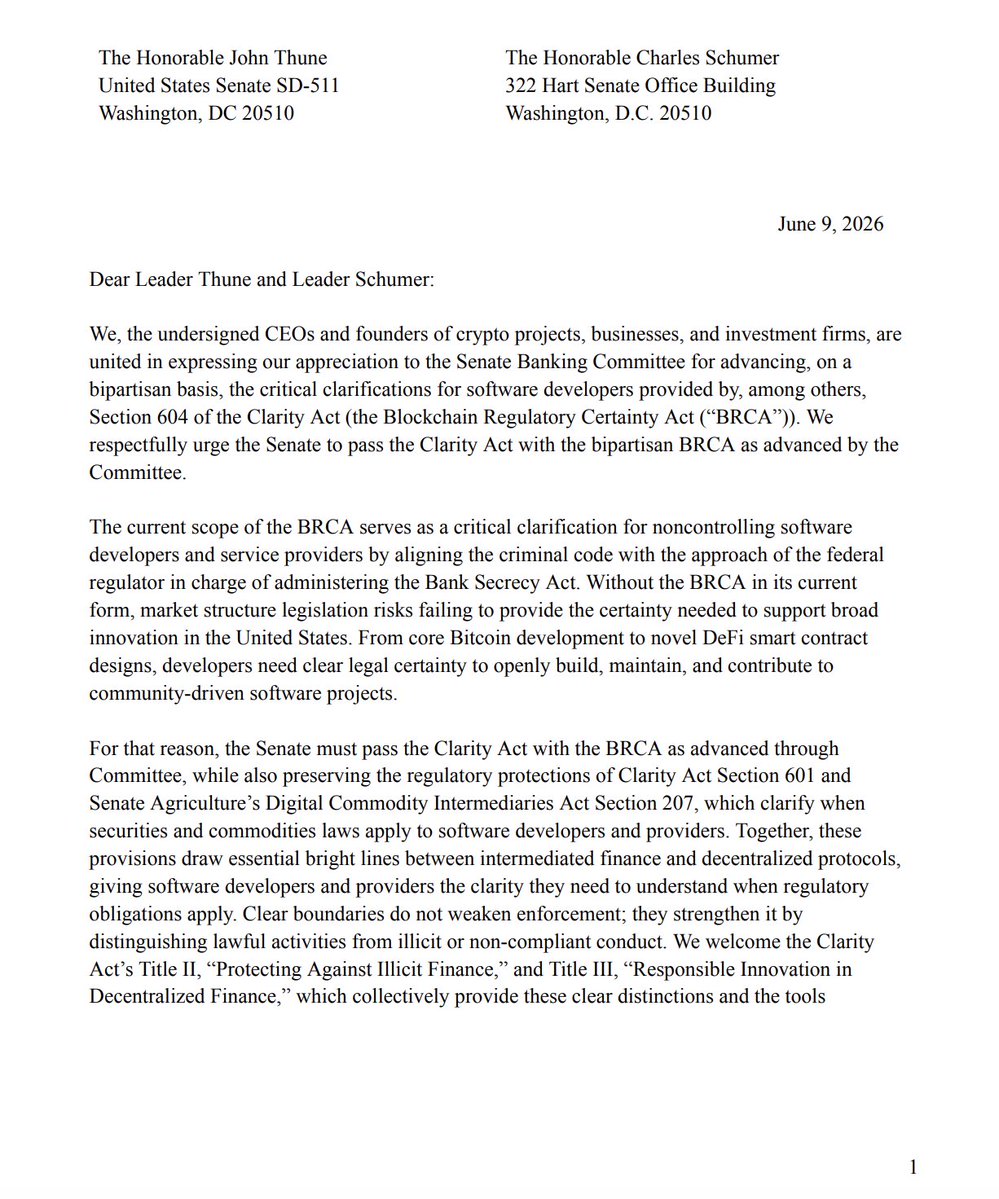

This industry takes care of its builders. Thank you to the 60+ CEOs and founders who sent a clear message to Senate leadership today: Pass the Clarity Act with developer protections and the BRCA intact.

Developers who do not control user funds are not money transmitters.

Read the full letter: https://t.co/HQFte9fSwT

On June 16, Solana Summit: Washington x Wall Street comes to Chicago 🏙️

Policymakers, regulators, institutional investors, and builders will explore how @solana serves as the foundation for modern finance + how the right policy enables broader institutional adoption.

Join us ➡️ https://t.co/OekcWvdeqV

Debate continues around the Clarity Act. But the conversation should be grounded in what the bill says rather than exaggerations of what people assume is in there without having read it.

The bill is designed to bring digital asset activity into a clearer regulatory framework. Clarity creates new obligations, supervisory hooks, and agency rulemakings while preserving the core authorities DOJ and federal agencies already use to pursue money laundering, sanctions evasion, fraud, and scams. The bill does not make it easier for criminals to use crypto to launder money.

Framing Clarity as “deregulation” is puzzling, to say the least. The bill includes hundreds of pages of new obligations, registration requirements, disclosures, rulemakings, and compliance undertakings that do not exist today.

The same is true for arguments that the bill lets banks put customer assets at risk. What the bill does is allow regulated financial institutions to responsibly innovate, including by using blockchain technology to perform functions they may otherwise already perform through other means, subject to applicable supervision and regulatory requirements. Banks are not going to be secretly converting customer deposits/assets into crypto because of this bill.

On illicit finance specifically, check out Title II and Title III of Clarity. Those sections cover new obligations relating to illicit finance, protocols, and front ends. And if you’re concerned that the Blockchain Regulatory Certainty Act (BRCA) or other developer protections in Clarity create a money laundering loophole, please point us to the language that does so. The BRCA aligns the scope of money transmission with the longstanding interpretation of the federal agency that administers the Bank Secrecy Act. It does not legalize money laundering, financing of terrorism, evading sanctions, or knowingly facilitating the movement of dirty money.

Clarity does not strip away the rules that apply to other types of investments. In fact, Clarity reflects a basic parity principle that a tokenized security is still a security. Tokenizing something does not magically remove it from the applicable regulations.

The claim that Clarity makes it far more difficult for regulators to crack down on fraud and scams is also impossible to reconcile with the text of the bill. Take Amendment 126, for example, adopted during the Banking markup on a bipartisan basis. That makes clear that unless explicitly addressed by Clarity, existing authorities for fraud, scams, deceptive practices, and similar misconduct remain fully intact and available to regulators. If someone commits fraud, this bill does not give them a free pass.

No part of Clarity authorizes taxpayer bailouts for crypto. The bill includes clarifications about issues like bankruptcy and customer property, but that is not the same thing as putting taxpayers on the hook for crypto bailouts.

There are fair debates around ethics provisions. Those provisions were not included in the Banking markup because of jurisdictional issues, but many remain at the table for ongoing negotiations around ethics language in any final bill.

And yes, crypto participates in politics. So do banks, unions, lawyers, energy companies, consumer groups, tech companies, and every other organized interest in America. Political advocacy does not prove that the underlying policy is wrong.

It is also insulting to suggest that a lawmaker's support for crypto legislation can only be explained by ignorance or corruption. Members and staff have spent years hearing from the industry, its critics, academics, regulators, and many others. Pretending support can only come from bad faith ignores the years of education and policy work that have gone into this debate.

The industry has not been hiding Clarity. We have been talking about this bill for months. Organizations like @BlockchainAssn, @crypto_council, @DigitalChamber, @fund_defi, @standwithcrypto, and so many others have been speaking publicly about the bill and urging people to contact their representatives to explain why regulatory clarity and other specific parts of the text matter. This debate has been happening in public. And it will continue.

This was Solana Summit: Washington x Wall Street in NYC.

If you missed the first one – good news. We're heading to Chicago on June 16. Registration is open.

https://t.co/Uwa5h9VQxM

SPI’s Head of Government Relations @thecolinmclaren has a new op-ed in @TaxNotes: the GENIUS Act was a win, but stablecoin payments can't scale if Americans are still required to report a gain on fractions of a penny every time they tap their wallet.

1/ PropAMMs and the Next Chapter of Permissionless Market Structure

For years, onchain trading won on access, lost on execution. Some feel better performance requires moving backwards to centralized systems

PropAMMs on @solana are proving permissionless can outcompete centralized

1/ 🚨JUST IN: The @SECGov has issued guidance that addresses one of the most persistent challenges in crypto: When are digital assets considered securities?

https://t.co/KTFhwUp5sh

America needs to be the crypto capital of the world.

Our tax code needs to reflect that priority, especially for crypto stakers and miners.

I discussed the future of crypto taxes with the @IRSnews CEO at a @WaysandMeansGOP Committee hearing today:

just read this article by joe biden's "economic advisers"

they make the following arguments for why crypto is useless:

- price is down

- giant tech companies aren't using it yet

- it's a slow and expensive database

- main use case is international crime because i) anonymous and ii) binance didn't stop funds to iran via crypto

wish we had better critics so I could learn from them and work on improving the systems.

sadly, this is just nonsense by two idiots with no coherent arguments or even a basic understanding of crypto

i) if price being down means a technology is useless, then airplanes that are used everyday are useless as the airline stock prices have gone down 10% since 2017 while everything else has gone up

it also means that american eagle jeans are now much more useful since sydney sweeney wore them and the stock mooned

ii) well one, giant tech companies ARE using it.

see robinhood, block, meta, google, aws, shopify, tesla, spacex, stripe — and even NYT via Polymarket lmao

second, there are several regulations barring them from participating in many activities due to your very own admin's posture towards crypto

iii) I don't have the time to teach engineering to a shriveled raisin like @econjared but i) you are referring to bitcoin, ii) systems like solana are infinitely more performant than your antiquated COBOL frames

source: I worked on both, instead of getting my 18 yo intern staffers to do an outdated google search

iv) the part about anonymity is particularly hilarious

crypto is actually less anonymous than even traditional banking and card systems YET ALONE cash, which is entirely undetectable without extremely specialized processes

you are actually lucky that we haven't made it more anonymous yet, but don't worry that is coming

Opinion: The "Promoting Innovation in Blockchain Development Act" is a bipartisan push to protect open-source developers from outdated criminal codes and keep tech innovation in America.

1/ The GENIUS Act created a clear framework for payment stablecoins as dollar-backed, regulated instruments. Huge win for U.S. leadership. 🇺🇸

But our tax code? It’s still stuck in the past.

Great resource from @ensdomains on deploying decentralized websites

ENS’s practical guide shows how ENS, IPFS, and Filecoin Onchain Cloud work together to deploy more resilient, decentralized sites.

The stack:

- ENS for naming

- IPFS for content addressing and distribution

- Filecoin Onchain Cloud for long-term persistence

- Safe for secure updates

Read the full guide:

https://t.co/GTr3TiOocc

[NEW] Today, the DEF team published a myth vs. fact resource on the Blockchain Regulatory Certainty Act

The BRCA is good policy, and its inclusion in market structure is a red line for the industry for good reason.

Below: we debunk common misconceptions about the BRCA. 👇

1/ @SolanaInstitute is proud to submit this comment to @FTC alongside @fund_defi, @BlockchainAssn, and @crypto_council.

We share the FTC’s consumer protection goals. But it is not a cybersecurity regulator and shouldn’t use “unfairness” to set engineering standards in crypto.

![fund_defi's tweet photo. [NEW] Today, the DEF team published a myth vs. fact resource on the Blockchain Regulatory Certainty Act

The BRCA is good policy, and its inclusion in market structure is a red line for the industry for good reason.

Below: we debunk common misconceptions about the BRCA. 👇 https://t.co/HxSariz2TG](https://pbs.twimg.com/media/G_OTQgDXIAAHEOx.jpg)