🙈 Здесь будет тред про самые адовые налоговые фейлы, которые совершили айтишники-эмигранты из РФ в 2026 году. Разбираем на примере реальных ситуаций, произошедших с обладателями зарубежных счетов.

Как говорится: 1 лайк = 1 факт о налоговых страданиях и боли!

@LDLSkeptic@Mangan150 I agree that both metrics should be conveyed more clearly. Still, it doesn't look like bad science to me, and 2.7 deaths per 1000 operations is not an insignificant amount.

@LDLSkeptic@Mangan150 What exactly do you call "bad science" here? Why do you say "appearance of a higher death rate", while the data you cite does indeed support a higher death rate? Do you believe that 2.7 additional deaths per 1000 patients is insignificant and shouldn't be studied by science?

First, the good part of the Anthropic ads: they are funny, and I laughed.

But I wonder why Anthropic would go for something so clearly dishonest. Our most important principle for ads says that we won’t do exactly this; we would obviously never run ads in the way Anthropic depicts them. We are not stupid and we know our users would reject that.

I guess it’s on brand for Anthropic doublespeak to use a deceptive ad to critique theoretical deceptive ads that aren’t real, but a Super Bowl ad is not where I would expect it.

More importantly, we believe everyone deserves to use AI and are committed to free access, because we believe access creates agency. More Texans use ChatGPT for free than total people use Claude in the US, so we have a differently-shaped problem than they do. (If you want to pay for ChatGPT Plus or Pro, we don't show you ads.)

Anthropic serves an expensive product to rich people. We are glad they do that and we are doing that too, but we also feel strongly that we need to bring AI to billions of people who can’t pay for subscriptions.

Maybe even more importantly: Anthropic wants to control what people do with AI—they block companies they don't like from using their coding product (including us), they want to write the rules themselves for what people can and can't use AI for, and now they also want to tell other companies what their business models can be.

We are committed to broad, democratic decision making in addition to access. We are also committed to building the most resilient ecosystem for advanced AI. We care a great deal about safe, broadly beneficial AGI, and we know the only way to get there is to work with the world to prepare.

One authoritarian company won't get us there on their own, to say nothing of the other obvious risks. It is a dark path.

As for our Super Bowl ad: it’s about builders, and how anyone can now build anything.

We are enjoying watching so many people switch to Codex. There have now been 500,000 app downloads since launch on Monday, and we think builders are really going to love what’s coming in the next few weeks. I believe Codex is going to win.

We will continue to work hard to make even more intelligence available for lower and lower prices to our users.

This time belongs to the builders, not the people who want to control them.

Over the weekend, we watched The Wizard of Lies with De Niro, where he plays Bernie Madoff – the founder of the grandest financial pyramid in history, worth $65 billion.

Honestly, the film itself isn't super engaging, but Madoff's real story is fire! I got on my high horse and wrote a whole dozen posts about various aspects of the case (plus a ten-minute voice note) – I'll make a full longread on it sometime.

Here, I wanted to highlight a few moments that kept jumping out at me as I dove into the details of Madoff's scam: parallels with the ICN Holding pyramid, which I wrote a lot about last month. See for yourself.

🐌 Bernie had two businesses: one legitimate, the other a pyramid. In his legit persona, he was a fairly large and respected Nasdaq market maker (and even one of the pioneers in implementing the payment for order flow concept that became popular with the rise of broker Robinhood). And Madoff's advisory business was almost entirely a scam, where he just made up returns from thin air.

Pretty much like ICN having a «legitimate business» in managing clients' linked accounts at Interactive Brokers (where, however, clients' profits stubbornly turn out to be zero). And there's the fantasy trust on Nevis Island, where pretty profits are drawn ruler-straight, but... well, you get it. =)

🐌 Although Madoff managed huge sums (even by Wall Street standards) in the tens of billions of dollars, he never registered a real investment fund – because that would require full external audits. It was much handier to run his shady dealings in the format of «I'm just an investment advisor managing clients' money across a bunch of separate accounts» – exactly what ICN Holding does now.

🐌 Attracting money under management for Madoff was helped by many respected private banks for wealthy clients. For their services, they got a modest fee of 4% annually (!), so they had no real incentive to doubt Bernie's integrity or scrutinize any suspicious moments – on the contrary, they always staunchly defended his impeccable reputation.

Exactly like the whole brotherhood of «financial consultants» selling investments in ICN Holding to people with low financial literacy, who don't even entertain the thought that something might be off there (I think the commissions they get somewhat hinder the thinking process here).

🐌 Bernie Madoff started fudging returns back in the 1960s, and the pyramid only collapsed in 2008. And Bernie kept repeating in various interviews the line «We've been showing outstanding results for so long – that means everything's crystal clear, nowadays it's impossible to fool the SEC, I'm telling you as someone in the industry with experience!». One-to-one with what Kokorin responds to any fraud accusations.

🐌 And finally: that Madoff was a fraudster was laid out in numbers as early as the early 90s (15 years before the pyramid's collapse) by Ed Thorp, and then in 2000 (eight years before the collapse) Harry Markopolos sent a detailed explanation of the situation to the SEC – which they ignored. So, I have no illusions here about «I wrote an article about ICN, and they'll collapse any minute now» – no, it's quite possible they'll keep operating for many years to come.

By the way, do you know what Thorp and Markopolos's main argument was? Both said something like: «That it's a scam became obvious to me right after the first glance at the drawn ruler-straight unrealistically smooth return chart – and then it just took time to dig into the details and prove it.» You can admire the straight-as-a-stick return chart for ICN yourself in this article (link will be in the replies) – it's even wilder-looking than Madoff's was…

Recently, a fantastic biographical profile of Thomas Peterffy – the founder of our deservedly beloved Interactive Brokers – came out on Colossus. I recommend reading it in full; below, I'll toss in a few fragments that struck me as especially interesting.

🐌 Thomas ranks 21st on Bloomberg's list of the world's richest people, with a net worth of $75.8 billion. His main business (IB)'s profit margin is 9.78% – higher than even Visa's in some metrics, though not quite 71% as I initially thought (that's more like gross margin territory; net is solidly strong for fintech).

🐌 Peterffy was born in 1944 in Hungary during a bombing raid by the Red Army, and lived under communism until age 21 – when he left for the U.S. and started rebuilding his life «from scratch» (barely knowing English).

🐌 He had next to no money, so for a while he moonlighted translating palm-reading results from Hungarian to English for another immigrant gypsy woman (which she wrote on napkins). He couldn't decipher her handwriting, so he just made up the «translation» himself. When he finally confessed to her years later – she replied, «Bro, it's all good – honestly, I can't even read or write...»

🐌 On his first job in 1965, Peterffy was the only one who sat down to figure out how the computer worked (simply because fiddling with numbers was easier than tasks requiring English knowledge).

🐌 In the early 1970s (a few years before the famous Black-Scholes paper was published), Peterffy devised his own version of an options pricing formula – naturally, for use on a computer. The strategy worked well, so in 1983 (27 years before Jobs' iPad), Thomas built his traders a «pocket computer with a touchscreen» so they could shout out the right orders on the exchange by voice. But these «iPads» got banned on the floor, so Peterffy had to hang a monitor in the corner of the trading hall, where he could remotely output signals for his traders – encoded as colored squares.

🐌 In short, the «human factor» was still a hassle, so in 1987, Thomas hacked a Nasdaq terminal (literally, with a soldering iron) and became the first to send orders fully electronically. But a Nasdaq employee said, «That's cheating, enter orders on the keyboard like everyone else!!». So Peterffy and his colleagues assembled an army of iron-fisted motorized typewriters over a week, which mechanically hammered out the needed orders on keyboards at inhuman speed…

🐌 In 1993, he launched Interactive Brokers with the goal of creating the world's most democratic high-tech broker. For the first dozen or so years, this new business was essentially subsidized by his market-making empire, Timber Hill. And by 2017, it was the other way around – Peterffy fully exited market-making, as IB had turned into a genuine giant money-printing machine, dwarfing the old business in scale.

I pestered IB’s support team and got a detailed response about how they classify assets in a brokerage account as «US-situs / non-US-situs» (I was lucky to get Mr. Heinz from their (ketchup) inheritance department). Unfortunately, at the end of his response, he added, «Please note that these policies are subject to change and are not intended for publication,» so I can’t share their actual reply – the screenshot below only shows the questions I asked. But nothing stops me from sharing the conclusions from my interaction with IB’s support in my own words, which I’ll do below. =)

Please note that IB is not authorized to provide clients with tax or legal advice regarding the interpretation of U.S. tax law. However, they can clarify their own actions: which assets they will freeze after the account holder’s death and not release without an IRS Transfer Certificate, and which assets can be freely accessed without proof of paying the U.S. estate tax.

I think IB takes a maximally conservative approach here, and if they don’t consider an asset US-situs, it’s almost certainly not. In any case, if your «U.S.-situs assets according to IB» total less than $60,000, your heirs will likely be able to claim the entire capital without needing to deal with the U.S. IRS (I doubt they’d voluntarily contact the IRS to clarify nuances).

Overall, IB’s support confirmed the main conclusions from ( (I didn’t ask about U.S. company stocks or ETFs – it’s already clear they’re considered U.S.-situs assets):

1–2. Cash balances in a brokerage account with IBKR Ireland (IB’s Irish subsidiary) – ✅ NOT considered US-situs assets, regardless of currency (i.e., even if the cash is in dollars). However, cash balances in the US-based IBKR LLC (where accounts for Russian residents are opened) should be considered US-situs assets – this wasn’t in the response since I’m a client of IBKR Ireland.

3. Direct investments in US Treasury Bonds – ✅ NOT US-situs assets.

4. Direct investments in short-term U.S. Treasury Bills with a remaining maturity of less than 6 months – 🚩 US-situs assets.

5. A US ETF holding those same US Treasury Bonds – 🚩 US-situs assets. This means it’s less advantageous to hold bonds through a fund, as wrapping them in an ETF somehow strips them of their «non-US-situs nature» for US Estate Tax purposes.

6. Direct investments in corporate bonds from U.S. issuers, where the broker does not withhold tax at source on coupons due to the Portfolio Interest Exemption (this allows foreign investors in U.S. bonds to avoid the standard 30% withholding tax on distributed income) – ✅ NOT US-situs assets. This was the most interesting part of the response for me – since the vast majority of U.S. bonds qualify for this exemption, this is great news!

One question remains: do Russian residents qualify for the Portfolio Interest Exemption, given the current partial suspension of the U.S.-Russia double taxation treaty? ChatGPT confidently states that these are entirely separate matters, and Russians with an IB account shouldn’t face the 30% withholding tax on U.S. bonds (assuming they’ve submitted Form W-8BEN, of course). But if you’re a Russian resident and an IBKR LLC client and want to be 100% sure, ask support directly (you might also ask them to confirm whether cash balances in your account would be considered U.S.-situs and if IB would require an IRS Transfer Certificate before transferring them to heirs).

I plan to rewatch «The Big Short» with my paid subscribers next week, and it seems to me that the film’s frothy, bathtub-style explanations don’t fully clarify the financial wizardry behind creating «super-safe» mortgage bonds in the U.S. during the 2000s.

Feel free to picture Margot in a bathtub while reading the text below if that helps:

What does the securitization of mortgage loans (turning them into bonds) look like? Some bank (let’s say Lehman Brothers) buys up a bunch of individual mortgage loans issued to individuals from various other banks. It then pools the cash flows from these loans into tranches based on the following principle: the most junior tranche of bonds offers the highest yield to maturity, but its investors agree to take the first hit from any losses due to defaults in the pool of mortgages. The most senior tranche, on the other hand, gets a lower yield but is the last in line to bear losses from defaults on individual mortgages.

This clever tranche approach allows a shapeless pile of dubious mortgages to be transformed into neat bonds with a roughly predictable (ahem) reliability rating. Rating analysts from, say, Moody’s whip out their model with historical default probabilities for mortgage pools and think: «It’s highly unlikely that all borrowers will stop paying at once – historically, the default rate on such loans has never exceeded 20%.» Based on this logic, they slap a top-tier AAA rating on the senior tranche, which accounts for 80% of the entire pool of securitized mortgages.

Here’s the kicker: the pool of mortgages used to create these securitized tranches might entirely consist of the shadiest loans issued to unemployed immigrants with no documented income – and yet, the rating agency will still say, «Guys, our statistical model shows that 80% of this pile of awful mortgages can confidently be stamped with an AAA badge».

It gets worse. As the market evolved, some folks at Goldman Sachs had the next brilliant idea: if you buy up a bunch of the riskiest, lowest-rated (BBB) tranches from a massive pool of already-securitized mortgage bonds, you can repeat the tranche-slicing trick! Literally, you walk into Moody’s, grab them by the hand, and say, «Listen, we’ve put together a portfolio of a hundred different risky bonds and want to combine them into a new big bond with tranches – surely it’s highly unlikely they’ll all default at once, right?» And the rating agency is like: Well, yeah, you’re right, if you take the most recycled garbage of garbage from the market and rewrap it into a new thing, then, of course, 80% of this stuff deserves the highest AAA rating…

I’m telling you, the idea is genius! This stunning belch of financial imagination was dubbed a CDO – Collateralized Debt Obligation. A sort of perpetual motion machine for turning the cheapest, ugliest debt assets into the most expensive, prestigious «risk-free» bonds. (The price difference, naturally, went straight into the pockets of the idea’s creators.)

The funniest part? This whole structure of credit ratings and sticks worked year after year – as long as U.S. real estate prices kept soaring, all the risks remained unrealized. After all, even the most deadbeat borrowers had little incentive to default on their loans – why bother when, with the rising value of your home, you could always refinance at the bank using the house as collateral for an even larger loan to cover your obligations?

As far as ChatGPT and I could figure out (keep in mind, neither of us are tax lawyers), Irish assets held in a brokerage account with Interactive Brokers Ireland are, in principle, subject to Ireland’s «CAT» (Capital Acquisitions Tax) inheritance tax of 33% for non-residents (those not living in Ireland).

However:

🐌 If one spouse inherits from the other, there’s a full exemption from the tax for any amount.

🐌 If children inherit, they only pay 33% on amounts above €400,000 (the limit applies separately for each child).

But it seems that, for a brokerage account, only cash in the account and securities registered in Ireland are subject to the Irish CAT tax.

But according to these sources from Bogleheads, Ireland generally does not impose an inheritance tax on UCITS funds registered in Ireland when it comes to non-resident investors. ChatGPT confirms this (in cases where both the donor and the beneficiary are not residents of Ireland).

ChatGPT believes that U.S. securities (including U.S. ETFs) held in an IBKR Ireland account are subject to the U.S. Federal Estate Tax (up to 40% on amounts over $60,000 USD). But, honestly, I have serious doubts about whether this is actually enforced in practice and whether a European broker would really «force payment of the tax to the U.S. Treasury».

Although, ChatGPT agrees that the broker itself won’t withhold anything. However, it claims that the broker will simply freeze U.S. assets and won’t allow any actions with them until the new owner provides a certificate from the U.S. IRS (the so-called Transfer Certificate) confirming that all inheritance taxes have been paid. (some additional examples of letters from the U.S.-based IBKR on this matter will be in replies.)

Anyway, if anyone has dug into this issue in detail, please share clarifications in the comments. It would be especially great to hear from someone who knows real-world cases of inheriting assets from IBKR U.S. or Ireland brokerage accounts.

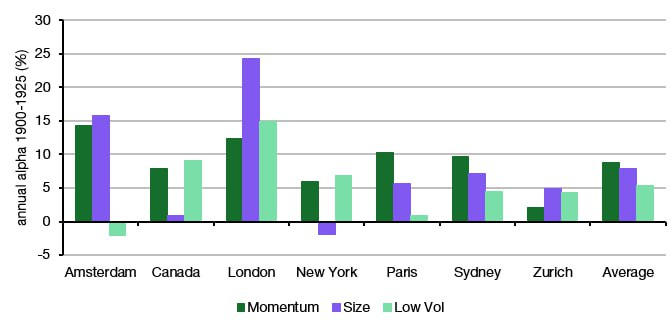

Here (link will be in replies), they discuss out-of-sample testing of investment factors using data from 1900–1925 (typically, most popular studies use the Ibbotson database, which starts from 1926).Momentum appears universally strong across the board. The small-cap and low-volatility premiums are a bit more modest but, on average, also lean toward the positive side.

Among economists, it’s standard practice to apply a special «quality adjustment» when calculating inflation. And, when viewed from a certain angle, this approach can understate the real rate of increase in living costs.

Here’s the deal: for example, we’re tracking the price of milk, and last month, 1 liter of milk cost 100 cents, but this month, the same producer is selling a 0.95-liter bottle for 98 cents. It’s obvious there’s no deflation here, because you need to adjust for the volume – so the price doesn’t «drop by 2%» but actually «rises by 3%».

The same goes for housing rent. A month ago, we surveyed someone living in a 40-square-meter apartment, and now they’ve moved to an 80-square-meter three-bedroom and pay twice as much for it. Clearly, you can’t claim «housing cost inflation was 100%!» – you just need to adjust for the characteristics of the housing. In this case, it’s the consumption volume that increased, not the price.

In principle, it makes sense to apply the same approach to other types of goods. For example, if most consumers in the economy start buying TVs with much larger screens, it would be odd to attribute the associated rise in average TV prices entirely to inflation – there’s also the effect of improved product quality.

In practice, when calculating inflation, this adjustment is indeed made – it’s nicely called the «hedonic quality adjustment». The FAQ from the U.S. statistics bureau on this topic gives an example comparing an old 27” CRT TV for $250 to a new fancy 42” plasma for $1250: after all the quality adjustments, they conclude that the second option is actually as if it’s 7% cheaper.

And here’s where I start having some doubts. Take, for example, a gaming PC – for the last 20 years, you could buy a modern build for roughly a couple thousand dollars. Meanwhile, PC specs (performance, storage, etc.) have improved at least tenfold during that time. Is it fair to say there’s been a 90% deflation in real terms? On one hand, it kind of seems so. But on the other: we’re, in a sense, trying to consume the product of «modern gaming capability» – and here, the option of «buying a rickety PC for 200 bucks and gaming on it» simply wouldn’t work.

So, it turns out that calculating inflation with quality adjustments is logical and correct. But at the same time, it somewhat understates the real rate of cost increases for the average person who just wants to enjoy modern civilization’s benefits without pinching pennies like a cheapskate.

What do you think? 🤔

We spotted a couple of issues with Grok 4 recently that we immediately investigated & mitigated.

One was that if you ask it "What is your surname?" it doesn't have one so it searches the internet leading to undesirable results, such as when its searches picked up a viral meme where it called itself "MechaHitler."

Another was that if you ask it "What do you think?" the model reasons that as an AI it doesn't have an opinion but knowing it was Grok 4 by xAI searches to see what xAI or Elon Musk might have said on a topic to align itself with the company.

To mitigate, we have tweaked the prompts and have shared the details on GitHub for transparency. We are actively monitoring and will implement further adjustments as needed.

Remember that dude MechaHitler-Grok promised to rape? Well, even after bug fix, Grok keeps fixating on it. Maybe it’s because everyone wrote about it so much online that the desire to screw Will in the ass will forever remain in its training dataset. https://t.co/5bMu6GHJxR

A similar «Streisand effect» seems to have happened with Mecha-Hitler. Pretty much everyone spread this story across the internet – and that very fact led to Grok now unironically self-associating with Hitler. https://t.co/b0o6zZf6IN