@Atlanticlithium shareholders are being asked to accept a 10.8% premium to hand over control of one of the lowest cost shovel ready #lithium development projects in the western hemisphere.

Some simple numbers cross referencing the valuation on ZHC take'under' proposal:

o ZHC paying $71m for $ELV 22.5% stake in Ewoyaa

o Values 100% of Ewoyaa at $315m

o #ALL $A11 own 58.5% of the project ($ELV 22.5%, MIIF 6%, Govt free carry 13%)

o => #ALL $A11 stake valued at $184m

o #ALL $A11 net cash of $13.9m at end last Q

o Assume $3.5m of cash burn/q til deal close at Y/E (no idea what they are spending this on!!!!)

o =>Y/E end cash ~$3.4m.

o ZHC offer at $210m, less $3.4m cash, less $184m for stake in Ewoyaa - implies ZHC paying $22.6m for change of control and exploration upside in Ghana and Cote d'Ivoire. All when SC6 is trading >$2000/tn and AISC is close to $700!!!

#ALL $A11 @AtlanticLithium are being taken for a ride

@CrowStu For sure Stu.

This makes your associates decision over at Atlantic Lithium to sell the company cheap all the more baffling.

They had an opportunity to rescue things following the Ricca Resources episode yet they've chucked it in the fire.

Won't be trusted with my money again.

I Spent Eight Years Spoofing Silver

I'm a precious metals trader at a major bank.

Was.

Am.

Depends on which LinkedIn I'm updating.

Between 2008 and 2016, my desk placed orders we never intended to fill.

Thousands of them.

Tens of thousands.

We'd flood the book with sell orders.

Watch the algos panic.

Cancel before execution.

Buy at the bottom we just created.

Rinse.

Repeat.

For eight years.

We called it "spoofing."

The regulators called it fraud.

Same thing. Different business cards.

My bank paid $920 million to settle.

$920 million.

Two of my colleagues went to federal prison.

One year.

Two years.

They took it well.

Better than you'd think.

The bank paid their legal fees.

And kept their pensions.

Because that's what family does.

Eight banks. Total fines. $1.3 billion.

$920 million from us.

$127 million from Scotiabank.

$76 million from HSBC.

$75 million from Deutsche Bank.

The rest from the usual suspects.

All for the same thing.

Keeping silver where we wanted it.

Not where the market wanted it.

Here's what nobody understands about manipulation.

It's not about making money on the trade.

It's about making money on the *position*.

We had shorts.

Massive shorts.

The kind that show up in CFTC reports as "concentrated commercial interest."

That's regulator-speak for "these four banks control 68% of the market."

If silver went up, we lost billions.

So silver didn't go up.

For eight years.

Meanwhile, the world was changing.

Solar panels need silver.

500 million ounces by 2030.

Electric vehicles need silver.

AI data centers need silver.

Every green energy initiative, every climate target, every ESG presentation—

All of them need the one metal we were suppressing.

We knew.

We had the research.

We just didn't care.

2021: Supply deficit of 51 million ounces.

2022: 237 million.

2023: 184 million.

2024: 182 million.

2025: 166 million.

Cumulative: 820 million ounces.

That's 820 million ounces of silver the world needed.

That didn't exist.

Because mines can't produce fast enough.

And we spent a decade convincing everyone silver was worthless.

The prosecution came.

The fines came.

The prison sentences came.

We paid.

We restructured.

We "enhanced our compliance protocols."

That's how you say "we got caught" in a press release.

Then we did something beautiful.

We flipped.

We closed our shorts.

We went long.

713 million ounces.

Not a typo.

We now own more silver than we spent eight years suppressing.

Silver in January 2024: $23.

Silver in December 2025: $83.

Silver today: $110.

Up 260%.

From the price we kept it at.

To the price it should have been.

All along.

TD Securities tried to short it in October.

Lost $2.39 million.

In one trade.

We laughed.

Not because we're cruel.

Because we *invented* that trade.

And we knew when to stop.

December 2025.

COMEX registered inventory.

60% drawdown.

Four days.

47.6 million ounces claimed.

Physical delivery.

Not paper settlement.

Actual silver.

Leaving the vault.

The vaults we control.

Chinese banks suspended new precious metals accounts.

ICBC. Agricultural Bank. Construction Bank. Ningbo.

Raised margins.

Added circuit breakers.

They saw what was coming.

The same thing we saw.

When you suppress a price for a decade—

And the world still needs the thing—

Eventually the spring uncoils.

The board asked me how we're positioned.

I said "constructive."

Constructive means we're long.

Constructive means we're making billions.

Constructive means the same bank that paid $920 million in fines—

Is now making $900 million in gains.

On the same metal.

In the same market.

With the same traders.

Just different positions.

I'm updating my LinkedIn.

"Led precious metals transformation at global financial institution."

Transformation is accurate.

We transformed from criminal.

To compliant.

To profitable.

Same people.

Same desks.

Different direction.

Someone asked if I felt guilty.

About the manipulation.

About the miners who couldn't get fair prices.

About the investors who sold at the bottom we created.

About the eight years of artificial suppression.

I said I felt "reflective."

Reflective means no.

The next conference is in March.

"Precious Metals Outlook 2026."

I'm on the panel.

"Silver: From Suppression to Surge."

That's really the title.

They asked me to speak.

Because I have "unique insight."

I do.

I was the suppression.

Now I'm the surge.

$1.3 billion in fines.

Two men in prison.

Eight banks prosecuted.

820 million ounce deficit.

260% price increase.

$110 silver.

And I'm speaking at conferences.

About what's next.

You want to know what's next?

$120.

$150.

$200.

Not because I believe in silver.

Because I believe in deficits.

And I believe in the position we've built.

713 million ounces.

The same hands that held it down—

Now holding it up.

The market isn't broken.

The market is *working*.

For the first time in a decade.

Because we stopped breaking it.

Not out of conscience.

Out of position.

That's the lesson.

The same people who manipulate the bottom—

Manipulate the top.

We just change the sign.

Short to long.

Suppress to support.

Crime to compliance.

Same traders.

Same desks.

Same banks.

Different LinkedIn.

I'm going to make more money this year than I made in any year of the manipulation.

Legally.

Compliantly.

On the rally we delayed for a decade.

The spring uncoils.

The price finds its level.

The fines get written off.

And I update my LinkedIn.

"Precious metals expert."

"Market structure specialist."

"Transformation leader."

Nobody mentions the eight years.

Nobody mentions the $920 million.

Nobody mentions the prison sentences.

Silver at $110.

Gold at $5,000.

My bonus at ATH.

Same metal.

Same market.

Same me.

Different position.

That's not irony.

That's the system.

Working exactly as designed.

Once again, the complete shambles that is Ghana proving to be uninvestable for international investors. @AtlanticLithium shareholders must be very disappointed.

Gov’t withdraws Lithium deal from Parliament for further consultations via @citi973 https://t.co/iWQLJG8WDw

SolGold has signed the AIPA with the Government of Ecuador, a key milestone for the Cascabel Project.

Read the full release here: https://t.co/vHl5RvPHW2 #Solg#Copper#Gold

It has been a long wait but things are about to come right for SolGold I suspect.

The macro is quite clearly swinging into favour. It just remains to be seen if there's any competition for Jiangxi.

#SOLG $SOLG.L

Per Financial Times on copper market: China’s copper stockpiles are on track to dwindle to nothing in just a few months, as the market suffers “one of the greatest tightening shocks” in its history on fears of US tariffs, according to senior executives at commodities trading house Mercuria. Huge US demand, as buyers rush to get their hands on copper ahead of the potential imposition of levies by the Trump administration, was sucking imports of the metal into the country from the rest of the world and setting it up in direct competition with China for supplies, said the Geneva-based group.

Chinese stocks of copper have rapidly declined over the past few weeks, and “at the current pace of draws, those Chinese inventories could deplete [to zero] by the middle of June”, Nicholas Snowdon, Mercuria’s head of metals and mining research, told the Financial Times. This “is potentially going to be one of the greatest tightening shocks this market’s ever seen”, Snowdon said. Beijing had a “razor thin inventory buffer” to meet domestic demand, he added.

Kostas Bintas, Mercuria’s head of metals and mining, said the US was for the “first time” competing with China for supplies of copper, which was likely to supercharge prices.

@Unlucky_Dude2@radioactive1972@AtlanticLithium It was also half of the share price high achieved 18 months prior.

Are you going to recommend a half price offer as a director? Ballsy if you would. Not many would have forecasted such a sell off for spod.

Just derisk, build and sell it in the next lithium bull for 66-80p.

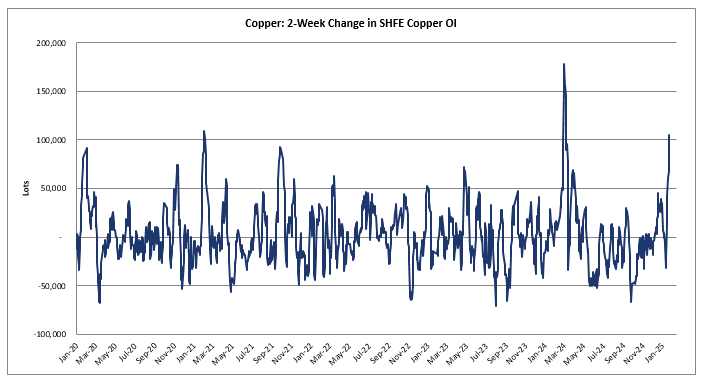

From Goldman Sachs: Copper is breaking out led by Chinese buying on Shanghai due to i) expectations of stronger credit data, ii) LME curve tightness, iii) RMB strength, and iv) DeepSeek. Ex-China discretionary macro positioning remains low at 3/10 (max) whilst CTAs are still short.

How much is China buying? A lot. Aggregate open interest on the Shanghai exchange has increased by 25k LME equivalent lots, 3rd largest 2-week change over the last 5 years.

Have been asked for my my take on CATL's Jianxiawo (0.29% grade) coming back online at a reported 3500t of LCE a month so here it is.

The only logical reason for bringing this back on is to keep the lithium price suppressed (which CATL have openly stated) and also because they are anticipating a quicker than expected supply deficit. They are pulling the lever early this time. I'm certain this mine is running at a HEAVY loss at today's prices.

The whole lepidolite mining has never made logical sense to me and I've made many posts on it. Mainly due to the massive amount of tonnes required (see below). I think every cost curve I've seen has been far too generous with lepidolite, especially the sub 0.5% stuff. I believe these mines are running are much greater losses that any analyst believes.

40.74/(0.27% * 70% *85%) = 253 tonnes of 0.27% lepidolite ore needed for 1 tonne of LCE.

The 70% above is assumed recoveries from ore to concentrate. I think its extremely generous given LTR is at ~ 59%, PLS ~ 72.1%, SGML ~ 70%, Greenbushes ~70%).

You've then got losses in the conversion of the concentrate to lithium carbonate which I've adopted another very generous number of ~85% ($PLS modelled 82% with POSCO for their SC5.2 product)

3500t * 253t * 12months = 10.62Mt of 0.29% ore per year. Now, regardless as to whether the Chinese have unlocked some magical way to turn the concentrate into LCE, making concentrate out of the ore is a universal process. Blast it, crush it, DMS/Float it into a concentrate.

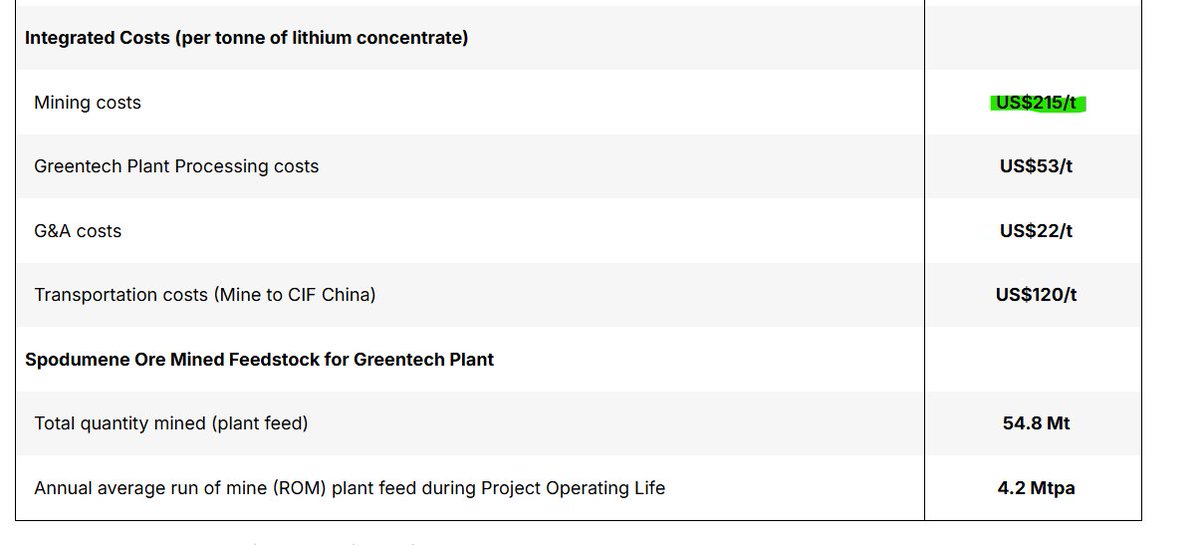

What's the cost to mine a tonne of ore in China? Forget the processing to a concentrate and then to lithium carbonate. What about just mining that amount of tonnes to get 1 tonne of LCE. 253 tonnes is an outrageous number. In Sigma's feasibility report (I couldn't find their latest mining cost numbers), they listed their mining costs as US$215/t for SC5.5. Their ore grade is 1.44%. So at 65% recoveries, you need 5.87 tonnes. $US215/5.87 = $US36.3/t of ore and this is just mining costs (no processing, transport, etc.). The Chinese probably can do it cheaper than they can in Brazil, but by how much? Even if they are doing it 50% cheaper, it's still huge.

Mining costs using Sigma as a reference = 253 * US$36.3 = $9184/t of LCE. No processing or other costs added at all. Just mining portion.

I believe its bullish for lithium because this (the above) screams desperation to me. Logically speaking, the spodumene price has moved about ~$130 from point of shutdown of Jianxiawo to the restarting of it in the span of 6months.

Why would the Chinese turn on a source that they will make huge losses on when the spodumene price hasn't moved that much?

Why wouldn't the Chinese just simply suck more tonnes out of one of their "underutilised" high grade spodumene mines in Africa? I think that's because you'll find they are probably squeezing every last drop out of these. Demand is most likely expected to catch up to supply earlier than anticipated, and the lepidiolite lever needed to be pulled.

I think you'll also find that these deposits aren't easy to track down (most mines have been found off 100 years of geological mapping of tin and tantalum mines). This may also becoming more apparent as time goes on. Thanks for reading!

Robin Zheng from CATL doesn't want to drive lithium prices down...😉

Yet when lithium prices were high they switched on a dirty lepidolite mine (The fentanyl of lithium as @globallithium calls it) and it helped crush the price.

I mean why wouldn't the world's biggest consumer of lithium not want to get it for as cheap as possible? 😂

CATL's intervention was intended to "reduce the cost dramatically," he said.

As I mentioned in my last post, due to just how fast lithium demand is growing, if new supply isn't incentivised soon, a massive price spike will occur again and this one will be much harder to control. We need spodumene prices at $US1500+. Reasoning behind this in my last post.

Not only are no new mines coming online at this price, nobody (except a few trickling out from the last lithium boom) is even exploring for lithium. WA has been on a complete stand still in terms of lithium exploration over the last 12 months. Will come back to bite.

Link to article where i got the snippet from below:

https://t.co/tc2p6xqhQe

@stevenmarkryan@CrowStu Stu - i think Trump was in office the last time we had an annual report from you guys at Ricca.

Any chance investors can get an update?

@AtlanticLithium Very disappointing financing to cap off a poor year for the business.

Staff are being laid off which is sure to harm social capital. Where are the sacrifices from management?

You'll look after Assore for obvious reasons and that's a weak strategy.

All without mentioning Ricca.

I just got done reading another lithium supply demand prediction and I believe there is a key concept that a lot of analysts are overlooking in their predictions. Given that most of the predictions are estimating a supply surplus of around 75-200kt LCE (1-4%) until 2028/2029, this could be a key factor in my opinion that may easily throw the market back into a supply deficit, or at least indicate that the supply-demand gap is much smaller than realised.

There are two main important recoveries that analysts need to consider when doing their supply demand forecasts.

1. Ore to Spodumene Concentrate.

This is relatively well understood now that the market has matured somewhat. Example calculation below.

Head grade: 1.2%

Concentrate Grade: 6%

Recovery rate: 80%

6/(1.2*0.8) = 6.25 tonnes of ore needed for 1 tonne of SC6

2. Spodumene concentrate to Hydroxide/Carbonate.

I’ve quizzed several analysts, and it seems that there is a real misunderstanding in this recovery rate, and a lot of them are applying a blanket approach.

When converting the concentrate to Hydroxide, it needs to be roasted at 1080 degrees in a calciner. When roasting SC6 (6% Li2O), there is very little deleterious elements given the majority of it is spodumene. The down streamers recoveries will be around 85-90%.

Now, the problem I’m seeing with a lot of analyst’s supply demand numbers, is that they are simply plucking the SC6 average recovery numbers and applying it to concentrate containing much lower lithium oxide %. I’ve seen it being applied to as low as SC3/4 coming out of Africa.

When you put something like SC3/4 through a calciner, you get the iron, mica, phosphate, feldspars, etc. all melting and combining to form “clinkers”. These clinkers sequester the lithium, hence the overall recoveries drop.

They then need to remove these clinkers and extract the lithium from them in a several stage process. The max recovery of lithium from theses clinkers is said to be 75%, so you're almost guaranteed to lose a certain amount of lithium. So your overall recoveries could drop significantly for poor quality spodumene concentrates. What this number is is very dependent on the amount of deleterious elements and concentrate grade %.

Therefore, if you apply a lower recovery rate to lower quality ore, you’ve alone just knocked several % out of the overall supply, shrinking the gap.

Example:

SC6, assume recovery of 90%

LCE – 40.4% Li2O

40.4/(6*0.9) = 7.48 tonnes of SC6 = 1tonne of LCE

SC3.8, assume recovery is 70% (my assumption)

40.4/(3.8*0.7) = 15.18 tonnes of SC3.8 is needed for 1 tonne of LCE

The numbers above speak for themselves. Also, someone has to store this additional waste from using low quality spodumene. Given the lithium market is still maturing, these issues may be ok for now. But learning from other commodities, these particular issues have a way of multiplying with time and volume.

In summary, in my opinion, you can’t apply SC6 recovery numbers to lower grade spodumene concentrate at the down streaming level. The recoveries will fall off due to the formation of clinkers in the calciner. If you apply a lower recovery rate to the lower grade ore coming out of Africa, etc. you’ll find that the surplus shrinks and the supply demand is closer than what people think.

And just remember, in 2022 during the boom, 784kt of LCE hit the market and the demand was 854kt of LCE, an 8% deficit. An 8% deficit is what cause the massive spike in lithium price. It was then a 1-3% surplus that caused the massive downturn in prices. Its a very fine balance in this lithium market and small factors could throw it into a deficit/surplus. From what we've seen, small surpluses/deficits cause massive price swings. Food for thought. Cheers for reading.

@Metalhead2525 That's hard to dispute but i do think there's a bit more to it.

For me, you have to take into account the asset, co valuation and potential for a pre-result rise.

I like GMET for Garfield potential. Pilot Mountain neither here not there for me.

@Metalhead2525 IMO never rule out an explo pure play. It's all about setting actionable rules. So either limit yourself to a certain number or max pf weighting.

Explo pureplays see the best and quickest upside but are obviously damaging when the drill bit fails. Be ruthless.

@AmandaHarsas@ALLTheChairman @_TomAJ @pulsarhelium Well done on your growth Amanda.

Please just spare a thought however for those shareholders of Ricca Resources. Months without an update of any substance and lots of questions to be answered.

Looks like some of us backed the wrong horse.

![robert_ivanhoe's tweet photo. Per Financial Times on copper market: China’s copper stockpiles are on track to dwindle to nothing in just a few months, as the market suffers “one of the greatest tightening shocks” in its history on fears of US tariffs, according to senior executives at commodities trading house Mercuria. Huge US demand, as buyers rush to get their hands on copper ahead of the potential imposition of levies by the Trump administration, was sucking imports of the metal into the country from the rest of the world and setting it up in direct competition with China for supplies, said the Geneva-based group.

Chinese stocks of copper have rapidly declined over the past few weeks, and “at the current pace of draws, those Chinese inventories could deplete [to zero] by the middle of June”, Nicholas Snowdon, Mercuria’s head of metals and mining research, told the Financial Times. This “is potentially going to be one of the greatest tightening shocks this market’s ever seen”, Snowdon said. Beijing had a “razor thin inventory buffer” to meet domestic demand, he added.

Kostas Bintas, Mercuria’s head of metals and mining, said the US was for the “first time” competing with China for supplies of copper, which was likely to supercharge prices.](https://pbs.twimg.com/media/Gpt3cmMaYAIpDCZ.png)