“We haven’t done that yet because we think we have a use for the compute,” Zuckerberg said at the time. “But obviously if we get to a point where we feel that we have overbuilt, then that is an option that we have, and that is partially what gives us confidence in investing in building this out.”

Amid a fast-moving AI race, Zuckerberg has repeatedly suggested that he believes the industry is constrained when it comes to computing capacity and that Meta should amass as much as possible and determine its use later.

For those interested in $NOK ...

Nokia’s 6-inch exposure came through the Infinera acquisition, and it is a fundamentally different kind of bet. Coherent, Lumentum and AAOI are mostly laser and discrete-device stories. Nokia/Infinera is a PIC story, chips that fold lasers, modulators, amplifiers and detectors onto a single piece of InP.

That changes the manufacturing problem. The die is bigger, the process is more complex, and the yield math is harder, but the payoff is that far more of the optical system gets integrated onto one chip.

The new San Jose fab (the 6-inch site) backed by the CHIPS Act is moving through qualification now:

“I think I know the new fab is finally flowing gas, flowing chemicals. So it’s -- all the equipment is being turned up. We’re qualifying it this year. It will start production late this year, early next year.”

What that fab is built to produce is the key differentiator:

“A key thing for us in this... is the majority of the volume that we’re building is this, and particularly in that facility, is this photonic integrated circuit for pluggables.”

And management is upfront that integration cuts both ways:

“It’s a full photonic integrated circuit. So the die size is a little bit bigger. So that creates a different... yield dynamics.”

That’s the trade. A larger PIC removes assembly steps and packs more value onto the chip, but bigger die are more exposed to defects. The 6-inch platform hands Nokia more wafer area to work with. The open question is whether those large integrated devices yield well enough at scale.

Important to know that Nokia is building the whole chain domestically, not just the fab. The San Jose InP site is paired with an expanded advanced test-and-packaging operation in Pennsylvania (we just spoke about this a few days ago), because pushing far more wafers out the front of the fab is worthless if packaging becomes the next choke point. By combining larger wafers, more advanced tools and more total tool count, management has framed the build-out as a step-function increase in capacity for complex optical chips, timed to support the surge in 2027 demand.

Nokia’s angle is all about internal supply, integration, and control over its own optical-engine roadmap.

I often get asked what my largest positions are

Well, here they are:

$LITE

$COHR

$CIEN

$NOK

$GLW

$AAOI

These make up a majority of my portfolio

If you want to learn:

> what my thesis is

> where I see these stocks going over the next 12 months

> what I am watching for / risks I see

I have many many articles about them on my Substack

https://t.co/6T2naqbkXV

Former $MSFT employee on why $MSFT leads the hyperscaler capacity race and what that means for the competition ( $GOOGL, $META, $AMZN ):

- The expert sees no slowdown in data center demand, with construction at an all-time high and available capacity at an all-time low, driven entirely by the need for AI training and inference. He doesn't expect the capacity crunch to ease anytime soon, with a large wave of new supply anticipated around 2028 based on current build-out timelines across the U.S. and globally, and some further relief potentially coming by 2030. However, the expert stops short of calling it a full resolution.

- The expert ranks $MSFT as the clear leader on current capacity, with $GOOGL in second place, moving quickly on both deployment and the commercialization of its TPUs for external use. $META comes in third, though the expert notes some uncertainty around how much capacity $META actually has available right now. $AMZN sits in fourth place, which the expert attributes to overindexing on the Inferentia line, which slowed capacity buildout in the short term, though the expert does not see that gap as permanent.

- The expert sees behind-the-meter microgrids as a practical and economically compelling solution for data center power, pointing to natural gas-rich areas where facilities can generate power at $0.03 to $0.07 per kilowatt hour compared to $0.17 to $0.21 from the grid, a cost difference significant enough to justify building out the infrastructure entirely.

- He believes the near-term mix will likely be gas turbines alongside battery energy storage systems tied to solar, but the expert sees SMRs as the ultimate destination, with companies making meaningful progress and permitting activity accelerating.

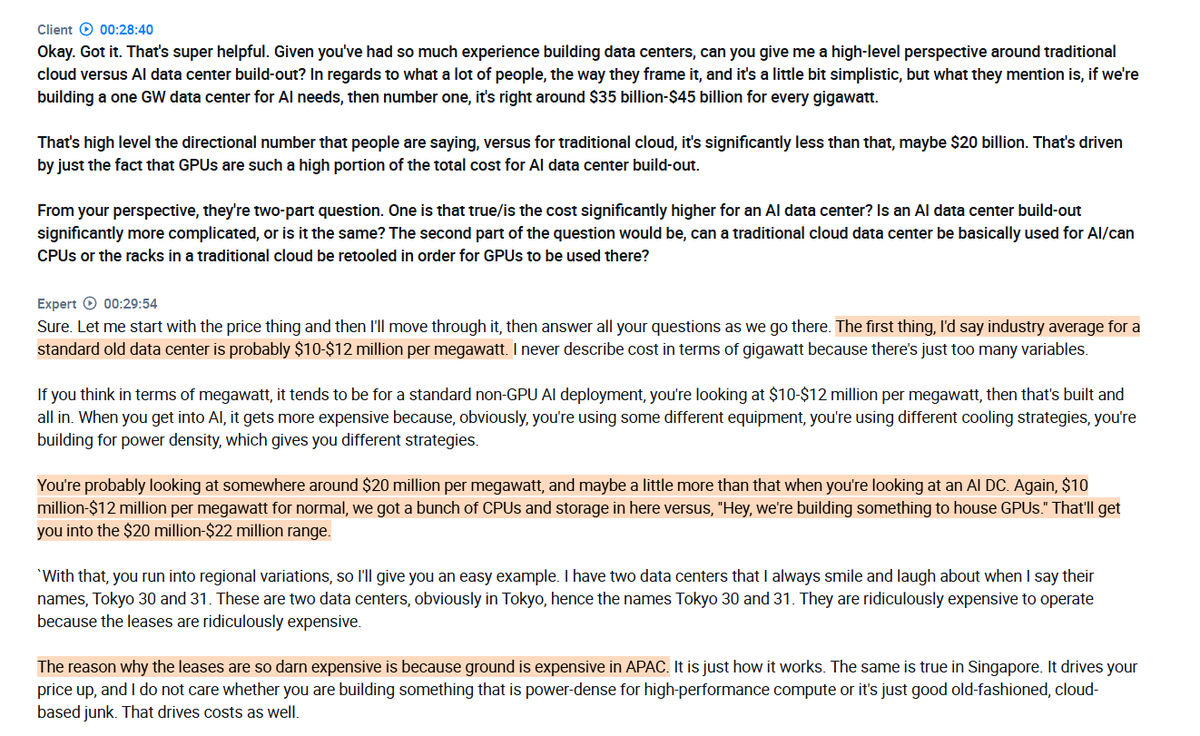

- The expert puts the cost of a standard non-GPU data center at around $10 to $12 million per megawatt all in, rising to roughly $20 to $22 million per megawatt for an AI-focused build, with the difference driven by higher power density requirements, different cooling strategies, and more specialized equipment. According to the expert, regional land costs add another layer on top pushing prices significantly higher regardless of workload type.

https://t.co/T1oGgUPCmF

Groq’s $20B was last year’s standalone valuation. But once an SRAM-route company gets embedded into the heterogeneous inference stack of any mainstream AI ASIC, its valuation will explode, because the shipment TAM is not even in the same league.

Cerebras’ valuation can actually be benchmarked against Groq, but the market currently has a major misunderstanding of Groq’s valuation

Take Rubin as an example. Suppose NVIDIA ships 25,000 Rubin racks a year, and only 7,000 of those racks attach LPX. Each LPX rack has 256 LPUs. If each LPX rack is priced at $3M, then LPU alone is already a $21B annual revenue business. At 10x P/S, that is at least a $200B valuation.

The key to Cerebras’ long-term development is how deeply it can integrate with AWS Trainium’s disaggregated inference architecture.

If it is only the currently disclosed version — Trainium does prefill, Cerebras does decode — then the technical implementation is much easier, but economically it still does not really work. It can only be a strategic beachhead. It can have some market, but it cannot create true scaled competitiveness.

But if it follows the NVIDIA path and deeply integrates the strengths of both sides, then even though the technical integration will take time and will not be easy, the payoff is worth it. Solution one: Trainium does prefill and decode attention, while Cerebras does decode FFN. Solution two: Cerebras runs the draft model, while Trainium does verification. Either way, the market competitiveness is far stronger.

If Cerebras gets onto the Trainium heterogeneous inference train, then its revenue becomes tied to Trainium. The imagination space becomes much larger. If it can further bind itself to OpenAI’s self-developed AI ASIC, then based on OpenAI’s 10GW self-developed AI ASIC scale by 2030, the imagination space moves up another level.

Trainium binding + OpenAI AI ASIC binding — this valuation, over the next few years, can be in the same order of magnitude as Groq’s current value.

Trainium shipment 3~4m in the long term, OpenAI AI ASIC shipment 3~4m in the long term.

Same point again: once an SRAM-route company gets embedded into the heterogeneous inference stack of any mainstream AI ASIC, its valuation will explode, because the shipment TAM is not even in the same league.