Just shipped: The Investing Tools Index → https://t.co/LNVz3opP1U

I’ve been building this for weeks — 265 tools and counting.

Organized by asset class + function + tool type (screeners, agents, Claude skills, APIs, etc.).

Here’s a sample of 50 AI-powered tools (full directory much bigger): Equities (27) • Multi-Asset (14) • Private Markets (5) + more

From @stockinsightsai to @kiyotaka_ai

v1 and growing fast.

What are you using or building? What should I add next?

Shoutout: @fiscal_ai@deepvest_ai@BollwerkAI

👇

My dad lost a small fortune betting on this man in the 90s.

In 1995, Seymour Cray’s company, Cray Computer Corp., filed for Chapter 11. A few weeks after the founder purchased ~6 million dollars worth of shares.

What’s interesting is that Cray wasn’t some overpromoting founder. He was arguably the greatest computer engineer of his generation and the father of supercomputing.

His bet was that the future belonged to increasingly powerful single machines.

One of his famous quotes:

“If you’re plowing a field, which would you rather use: two strong oxen or 1,024 chickens?”

The rest of the industry made the opposite bet.

Instead of building one incredibly powerful processor, companies increasingly connected thousands of cheaper processors together in parallel.

By the mid-1990s, commodity processors were improving so rapidly that the economics began to overwhelm the engineering elegance Cray was famous for.

Bulls like my dad were betting on -> legendary founder + huge vision + massive insider buy + revolutionary tech.

Unfortunately for the bulls, Cray was building better and better single machines while the industry was learning how to make thousands of cheaper machines work together.

Today, AI training, cloud computing, search engines, and hyperscale data centers are all descendants of the “1,024 chickens” approach.

One of my favourite Japanese ideas is Kitazato corp $368A. Founder led, Japanese company with a large (30% ex US) market share in IVF fertility treatment. Large tailwinds as popularity of IVF continues to grow. The co has been smashed down 25% from IPO last year. This isn't an

@romanp000 I like it. How much of current revenue will still be mission-critical to technicians five years from now as vehicle diagnostics become increasingly software-based and OEM-controlled?

I don't post much here but I spent years keeping a trading journal, not the kind with entry prices and stop losses, but the kind where you write things down at 2am after a bad week. Now I put it together for boom and bust traders.

Maybe it helps someone.

https://t.co/KVHRFY8j6o

I recently bought $DRX.TO - ADF Group, a Canadian fabricator of complex structural steel. They have 2 fabrication facilities in Quebec and 1 in Montana.

The stock recently sold off on near-term margin noise tied to steel tariffs and their LAR acquisition, creating what I think is a really good entry point

Why It's exciting:

1. Trades under 4x depressed EBITDA with a clean net cash balance sheet

2. Backlog has more than doubled in a year from $300m to $650M+, with strong bidding activity continuing.

3. Beneficiary of the "Build Canada" Thematic

4. A recent acquisition I believe will look like a no-brainer in hindsight

ADF is one of the best-positioned names to play the 'Build Canada' theme. They stand to benefit from a wave of infrastructure spend: airports, Ontario nuclear, hydro expansion in Quebec, BC, and Newfoundland, and energy/industrial buildout in the west. A "Buy Canadian" mandate further improves their competitive position and will spur industria/constructionl projects

Historically, they were 90% US, 10% Canada. However, with last year's tariffs, the company has aggressively pivoted its backlog which now sits at 60% Canadian and 40% US with a good chunk of the work segregated between the two countries. I expect Canada to make-up a bigger percentage of the mix overtime.

The most exciting part of the story is the LAR Group acquisition. Historically, ADF Group did primarily industrial & commercial projects. Think airports, warehouses, bridges and some industrial plants. LAR was a distressed, over-levered steel fabricator for the hydro sector. A specific contract blew them up and ADF stepped in as the white knight through a reverse vesting order approved by the government. It allowed them to acquire LAR's assets while having all liabilities extinguished, BUT keeping all certifications intact.

ADF is now certified to operate in both the hydro AND nuclear markets two of the most infrastructure-intensive sectors in Canada's near-term pipeline, in addition to potentially bidding for some of the big 'nation-building' projects the Canadian government has proposed.

The near-term overhang: LAR is working through a tail of low-margin legacy projects, which weighed on Q4 results. LAR currently runs ~10% gross margins vs. ADF's mid-20s. Management doesn't expect margins to deteriorate further from here, but the meaningful inflection only comes in H2 2026 and into 2027, as ADF deploys ~$35M to automate LAR's facilities. LAR is understood to be the preferred vendor for virtually all Hydro-Québec projects and so I expect more work to come their way. And let's not forget the government of Quebec approved the CCAA proceeding at record speed. Clearly Hydro-Quebec was pretty desperate to have ADF acquire LAR group as there aren't many companies capable of doing that type of work.

The second near-term overhang is the recent US steel tariff changes which puts a 10% tariff on the total value of steel transformed outside of US, but that uses US Steel. For some jobs, it made economical sense to ship US steel to Terrebonne and then ship it. It will impact their Q1/Q2 results, which caused last week's sell-off.

The market is focused on near-term headwinds but It's missing the forest for the trees.

Canada is entering one of the largest infrastructure build cycles in its history and ADF is one of a handful of Canadian companies capable of fabricating the complex steel structures these projects demand:

=> Hydro-Québec: $35–45B capex plan over the next decade

=> BC Hydro: $36B in regional investments over the next decade

=> Ontario & Atlantic provinces ramping hydro capacity

=> Ontario nuclear: plant refurbishments, SMRs, and Bruce Power expansion

And none of that includes the 15 'nation-building' projects the federal government has fast-tracked or the hundred of projects that will emerge from Canada's defense spend goal of 5% of GDP.

Despite the headwinds, the company expects to have stable gross margin, with a much bigger revenue number. There is a clear path here for the company to achieve 15% EBITDA margin on potentially over $500m of revenue which would get me to a target price of $17 at 6x EBITDA over the next 2-3 years.

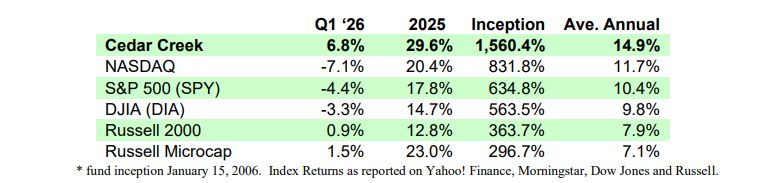

I believe @eriksen_tim is one of the goats in micro-cap investing. Not solely due to his continual outperformance over 20 years period, but he is also able to run the underlying business in which he has control in. Two skill sets. One man.

Remarkable.

10)

I think main takeaways are:

1) Do original stuff but do not worry to get inspired elsewhere.

2) Try not to sound smart. Look for easy things.

3) Be calm. You want to do this for decades. The burn-out is not worth it.

4) Don’t worry about people judging you. It kills.

I bought my first microcap stock at the end of 2021. I had no background in finance or investing, so I spent 2021 and 2022 learning the basics — mainly accounting.

By mid-2023, I started taking investing more seriously and began to understand what moves stocks and how to find ideas. That year I also laid the foundation for my investment style and had my first winners, like Deufol and later $CPH.TO.

In 2024, I leaned further into that, dedicating most of my time to generating ideas. And it bore fruit. I had my most successful year with multiple winners. By that point I felt confident in searching, identifying, and analyzing interesting setups. Most skills around “what to buy” were starting to click.

But 2025 taught me a valuable lesson. Knowing what to buy next doesn’t make you a good investor. What matters is how much you earn when you’re right and how much you lose when you’re wrong.

That year I learned — painfully — the importance of portfolio construction and how emotions interfere with it.

By the end of the year though, I had learned the most valuable lessons that books can’t teach. You have to experience them.

I’m sure this year I’ll continue to make mistakes and hopefully learn from them. But I feel much better prepared as an investor now than I was in 2024, even if I was an equally good (or bad) analyst back then.

The reason I’m writing this: don’t compare yourself to other investors. Everyone has their own timeline, and it takes years to learn just the basics (at least it did for me).

And you’ll never be “complete” as an

investor. The most complete you can be is good at managing your current sum of money because once that changes, you’ll need to develop new skills and adapt all over again.

Lion Rock https://t.co/b0g9xlURmJ is the first company that includes a formal tribute to David Webb in their results announcement. I will hold shares in this company forever. Lau Chuk Kin is one of the good guys.

https://t.co/aBHJXEfe8P

If you can trade on Cyprus exchange (me not) you may have a look on Vassiliko Cement works, running the only plant (cement, klinkers) in Cyprus means competitors have high transportation costs. Close to monopoly.

High profit margins

Growing (okay cyclical)

PER <10

Net cash

1/x