(Public) Primer On Investing In The Cyclical Chemical Sector

The piece is a compilation of all the chemical-sector write-ups we published since October 2025.

By: @Jon_Costello_

https://t.co/GBBbbUlZFI

Hyperscale GW forecast by Wells Fargo.

Does $META really need ~21GW by '28 when its core business is using only ~8GW?

Anthropic and Open AI had ~5GW of combined compute earlier this year. Will METAs nascent AI business really need ~2.5x that in two years?

$GOOG $AMZN $META $MSFT $ORCL

Regarding the $META BBG article: note they are NOT currently selling compute. This isn’t a Neo deal announcement and two months ago META expanded deals w/ $CRWV and $NBIUS.

My view: this is $META giving themselves optionality around 2027 capex.

Depending on how successful their upcoming AI models and agentic/AI products are, META may find themselves still compute constrained in 2027, or with significant excess. They are planning for both outcomes.

META has outlined their AI / Agent product strategy (my thread on that below), they’ve demonstrated promising results at small scale w/ Muse Spark, now they are going to scale that model to the frontier.

Twice (GPT4 & Opus 4.6/Claude Code) we have seen how easy it is to be short inference capacity when AI products breakout.

If the model performs as they hope, it’s possible METAs new agent and subscription products see explosive growth. That’s why META has assembled enormous compute for 2H26 and 2027.

If Muse models cannot catch the frontier or agent products don’t catch on, META will have significantly overbought and will sell capacity back into the market like $SPCX did.

If you are long $META, you have more upside if AI products work, but leasing excess capacity could still lead to a big increase in earnings above consensus.

If you are long AI bottlenecks (memory, etc), you should really hope META products work. Bc if they sublease capacity back into the market that has already been built in 2026, while also stepping back themselves in 2H27/2028+, it would send shocks to both the demand and supply side of AI bottlenecks, faster than bulls anticipate is possible.

Honeywell spin-off: first day of trading yesterday for $HON $HONA with both tickers selling off into the close (higher pressure on RemainCo interestingly)

Implied creation values look interesting for both at current levels. While Aero is considered the premium asset, Automation's growing installed base + software monetisation strategy is under appreciated and may get the steeper re-rate overtime.

B2Gold trades at 8 times forward earnings.

The gold mining industry average: 15 times.

A company trading at nearly half the sector multiple — with earnings growing 161% over the next 3 years.

Here is the full Q1 2026 picture:

Production: 237,763 ounces — ahead of plan.

Cash: $479 million.

Revolving credit facility: fully repaid April 24.

Asset sale to Agnico Eagle: $325 million cash received.

Q2 2026 dividend: $0.02 per share — payable June 23.

2026 production guidance: 820,000 to 970,000 ounces.

New CEO Mike Cinnamond took over June 4 — fresh leadership with a mandate to unlock value.

9 analysts cover the stock. Consensus: Buy.

At 8x forward earnings with 161% EPS growth forecast — the math does not add up to the current price.

$BTG on NYSE American. $BTO on TSX.

Oil's war premium has round-tripped: WTI back to a $69 handle, pre-war lows, as Hormuz reopens. The tape that matters isn't the barrel - it's what a cheaper barrel funds. Airlines at new highs, the long end softening, small-caps broadening. Crude is now oversold.

We've seen an implosion in the financial demand for oil and the 50:1 ratio of financial:physical is likely distorting price relative to medium-term fundamentals. Inventories will continue to fall, rigs will soon start to stack, physical demand metrics like refining margins remain strong, floating/unsanctioned Iranian barrels will soon be absorbed, Iran will likely remain in control of the Strait, and China will at some point return to the market. What then???

FT article on this. As Christophe notes:

"The BIS has just reminded us that AI is probably a major economic revolution but the current investment boom is also starting to become a source of financial fragility... The problem is that the market is already pricing in an almost perfect scenario with rapid adoption, massive productivity gains, high margins and sustained earnings growth. It is possible but not guaranteed... The BIS also highlights the opaque financing of the entire AI ecosystem with cross-shareholdings, long-term contracts, data centers built by third parties and leased back to tech giants, private debt, off-balance-sheet commitments, and so on."

From the FT article:

“Disappointment in returns could trigger a sudden pullback in financing and turn the capex [capital expenditure] boom into a protracted investment bust, with potential knock-on effects on financial conditions,” the BIS said.

The report acknowledged it was possible that AI could raise productivity “significantly” over the coming decade, given the efficiency gains it can provide to companies... But it said that historical episodes of investment booms provide “instructive parallels” — among them the expansion of canals in the 1830s, railways in Britain in the 1840s and the dotcom boom of the late 1990s.

These all had one key feature in common, said the BIS, “a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify”.

A major equity market correction associated with AI could have broader implications today than in the past, the BIS said, because households have greater exposure to shares relative to their wealth and income. Financial stability could also be endangered, given the volumes of debt being sold by AI companies to finance their investment, it warned.

“Perils have grown with pressure points around risks of persistent inflation, the sustainability of AI-related investments, growing financial vulnerabilities and weakening fiscal positions,” it said.

🚨 The BIS has just reminded us that AI is probably a major economic revolution but the current investment boom is also starting to become a source of financial fragility.

➡️ We should not confuse AI’s technological potential with the immediate financial profitability of every investment made in the name of AI. AI can generate significant productivity gains but turning these task-level gains into a lasting increase in productivity across the whole economy is much more complicated. Companies need to redesign processes, train teams, integrate tools, adapt systems and rethink business models. Historically, this kind of transformation takes time.

📊 The problem is that the market is already pricing in an almost perfect scenario with rapid adoption, massive productivity gains, high margins and sustained earnings growth. It is possible but not guaranteed. AI may well be a real revolution but that does not mean every investment being made today will be profitable, nor that all current valuations are justified.

📚 The major hyperscalers are investing enormous amounts in data centers, semiconductors, energy, cloud infrastructure and computing power. However, this race is also defensive as everyone is investing aggressively out of fear of missing the wave. Individually, that is rational but collectively it can create overcapacity. A classic pattern in major technological revolutions where a technology can be revolutionary while capital can still be misallocated.

⚠️ The BIS also highlights the opaque financing of the entire AI ecosystem with cross-shareholdings, long-term contracts, data centers built by third parties and leased back to tech giants, private debt, off-balance-sheet commitments, and so on. If the investment cycle slows abruptly, the shock will not only affect a few technology stocks, but it could spread to suppliers, data center developers, utilities, private credit funds and, more broadly, financial conditions.

*Link: https://t.co/1YeEQ0uChH

What we've learned from this era is that:

You can fool some people all of the time.

And you can fool all people some of the time.

And you can fool all fools EVERY time.

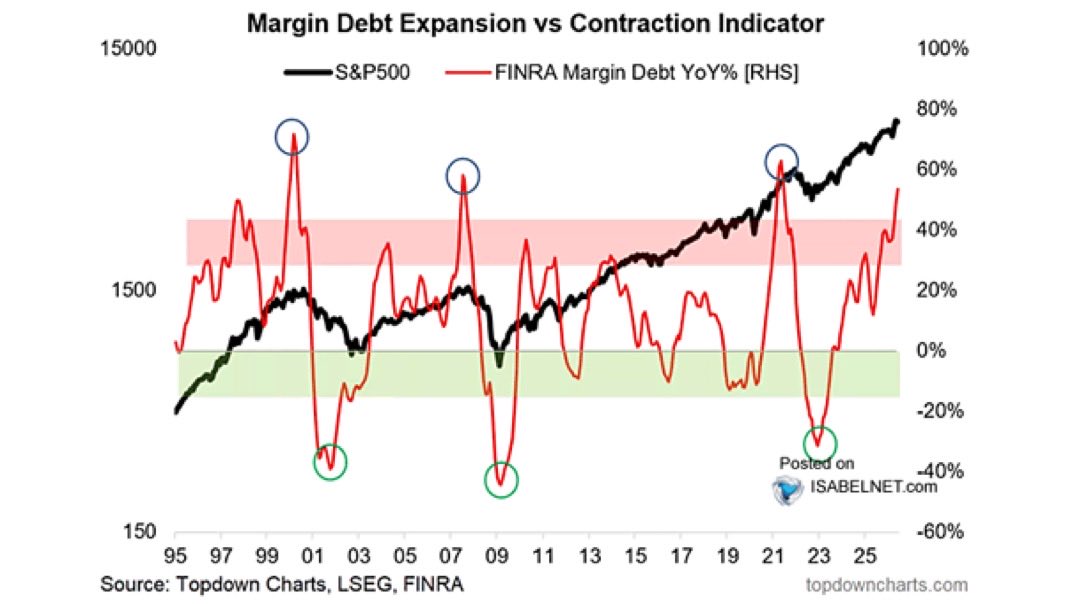

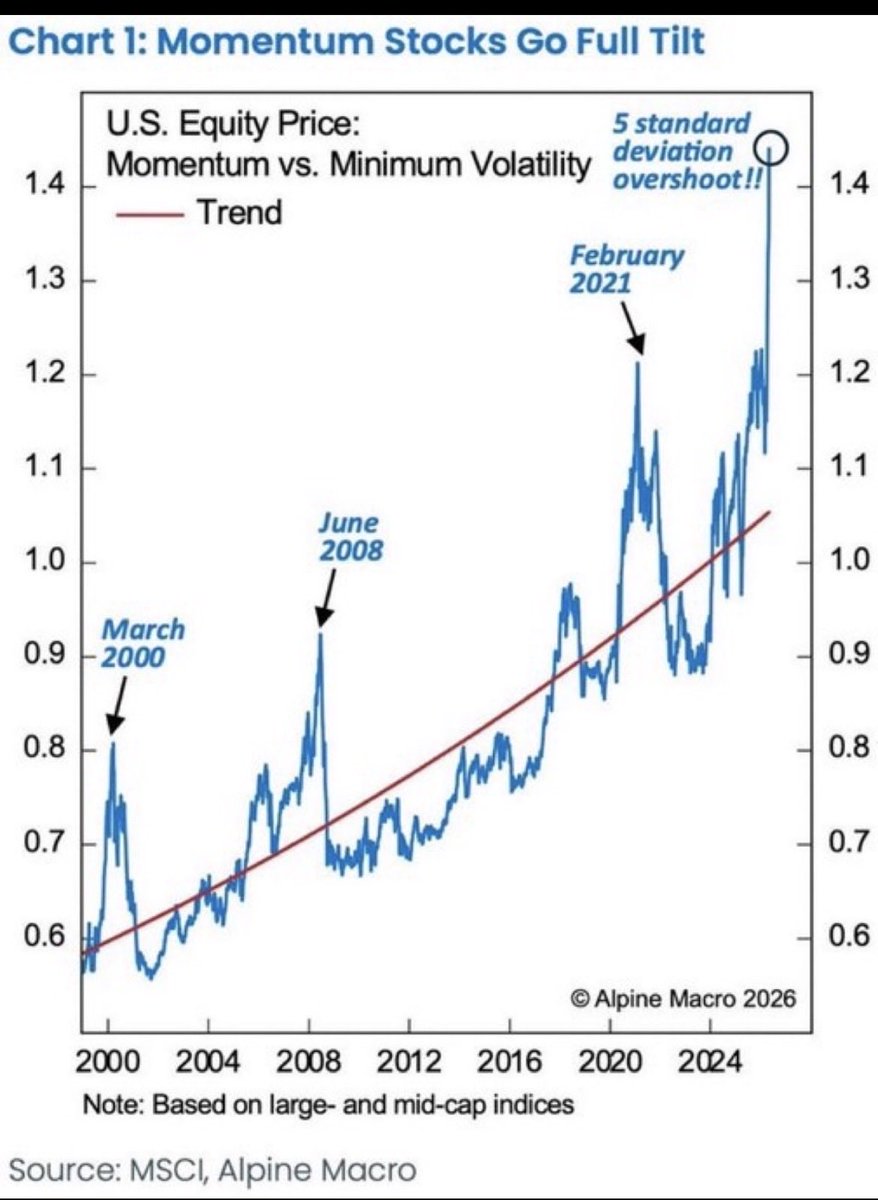

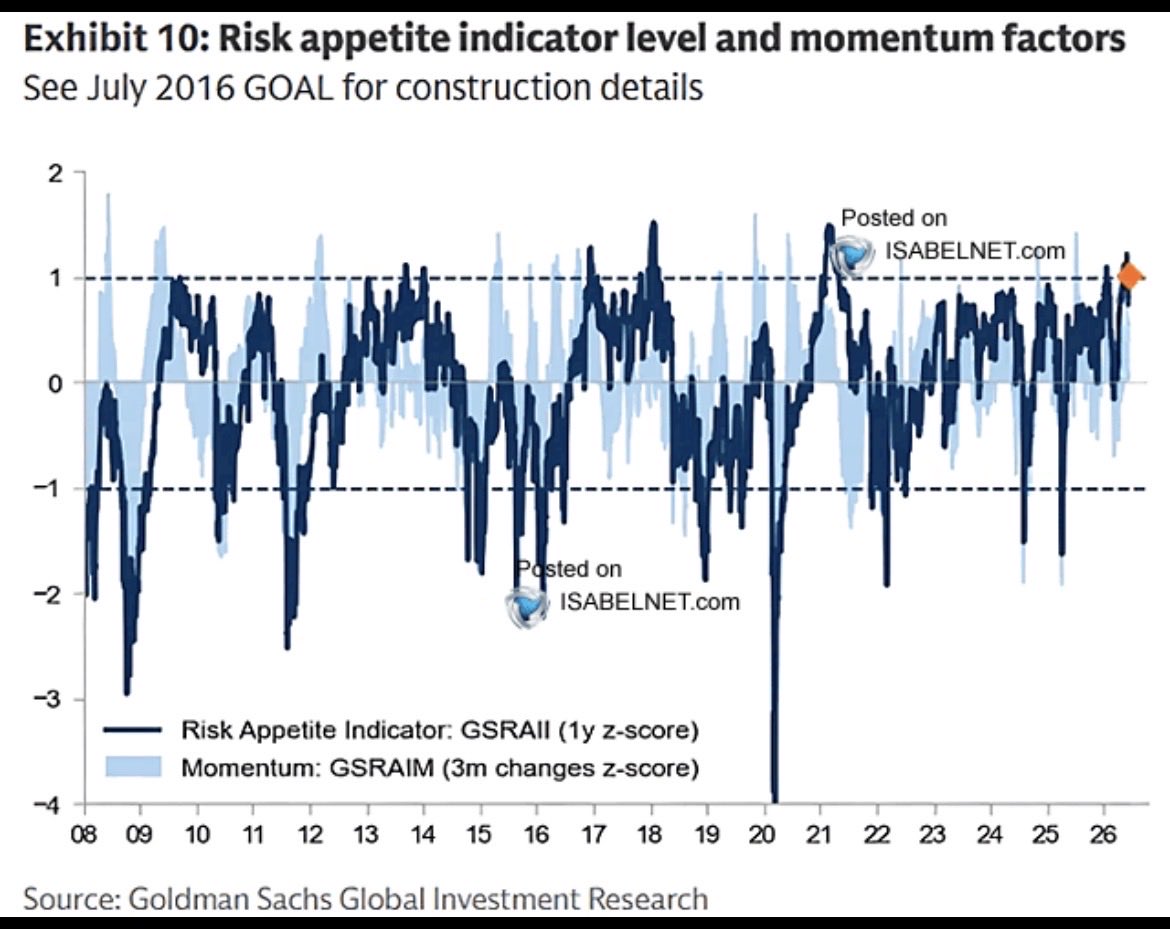

No matter which indicator you look at, every one is screaming peak valuations.

Similar valuations were reached during the dot‑com bubble… after the crash it took the S&P 13 yrs to break even.

What keeps me awake at night?

This.

One of the oldest froth gauges on Wall Street: the year-over-year change in margin debt. How fast investors are borrowing money to buy stocks.

May 2026 reading: 53.7%. A new record high in absolute terms, $1.42 trillion borrowed against portfolios.

Look at the chart. Every blue circle is a major top. 2000. 2007. 2021. The pattern is always the same. The line climbs into the danger zone, rolls over, and the rollover is the signal. Not the peak itself. The turn down from it.

That's the part most people get wrong. They wait for a number. A line in the sand at 55%, or 60%, or wherever. But the market doesn't ring a bell at a level. The tell is direction.

While margin debt is rising, leverage is being added. Genius on the way up. It amplifies every gain and makes the bulls look like prophets.

When it turns down, the machine runs in reverse. Borrowed money gets called back. A normal 10% dip triggers margin calls. Forced selling begets forced selling. The leverage that built the top accelerates the fall.

So here's what I'm watching now. Not whether we hit a magic number. Whether this line stops climbing and starts to fall.

The peak in margin debt growth has marked the edge of every major top for two generations. We're sitting at the second-highest reading in years, still rising.

The day it rolls over is the day to pay attention.

Up is the party. Down is the bill.

The TRUTH about Jeremy Grantham

Let's set the record straight.

You saw the video with Joe Kernen, here are the facts:

1. Jeremy Grantham called the dotcom bubble 5 years too early.

2. He was eventually vindicated... but the 2002 trough was 39% higher than when he turned bearish in 1995.

3. He nailed the housing market bubble, and he nailed the recovery perfectly, going long at the absolute bottom in 2009.

4. He called for a market melt-up in 2018, and was right, but...

5. Ever since 2021 he's been a bear...

the market is up 97% since then.

So what's the lesson? There is a Peter Lynch quote that fits perfectly:

"Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

$QQQ ~ How the 2020’s “AI boom” compares with boom-bust cycles of past major innovations. Railway mania, Dotcom boom, Roaring late 1920s mania, Canal mania. Notice that almost all prior booms lasted about 5 years. AI boom started in Q4 2022 so we good until Q4 2027?. $SOXX $SMH

![neilsethinew's tweet photo. FT article on this. As Christophe notes:

"The BIS has just reminded us that AI is probably a major economic revolution but the current investment boom is also starting to become a source of financial fragility... The problem is that the market is already pricing in an almost perfect scenario with rapid adoption, massive productivity gains, high margins and sustained earnings growth. It is possible but not guaranteed... The BIS also highlights the opaque financing of the entire AI ecosystem with cross-shareholdings, long-term contracts, data centers built by third parties and leased back to tech giants, private debt, off-balance-sheet commitments, and so on."

From the FT article:

“Disappointment in returns could trigger a sudden pullback in financing and turn the capex [capital expenditure] boom into a protracted investment bust, with potential knock-on effects on financial conditions,” the BIS said.

The report acknowledged it was possible that AI could raise productivity “significantly” over the coming decade, given the efficiency gains it can provide to companies... But it said that historical episodes of investment booms provide “instructive parallels” — among them the expansion of canals in the 1830s, railways in Britain in the 1840s and the dotcom boom of the late 1990s.

These all had one key feature in common, said the BIS, “a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify”.

A major equity market correction associated with AI could have broader implications today than in the past, the BIS said, because households have greater exposure to shares relative to their wealth and income. Financial stability could also be endangered, given the volumes of debt being sold by AI companies to finance their investment, it warned.

“Perils have grown with pressure points around risks of persistent inflation, the sustainability of AI-related investments, growing financial vulnerabilities and weakening fiscal positions,” it said.](https://pbs.twimg.com/media/HL_IHQTWcAAeEfg.png)

![neilsethinew's tweet photo. FT article on this. As Christophe notes:

"The BIS has just reminded us that AI is probably a major economic revolution but the current investment boom is also starting to become a source of financial fragility... The problem is that the market is already pricing in an almost perfect scenario with rapid adoption, massive productivity gains, high margins and sustained earnings growth. It is possible but not guaranteed... The BIS also highlights the opaque financing of the entire AI ecosystem with cross-shareholdings, long-term contracts, data centers built by third parties and leased back to tech giants, private debt, off-balance-sheet commitments, and so on."

From the FT article:

“Disappointment in returns could trigger a sudden pullback in financing and turn the capex [capital expenditure] boom into a protracted investment bust, with potential knock-on effects on financial conditions,” the BIS said.

The report acknowledged it was possible that AI could raise productivity “significantly” over the coming decade, given the efficiency gains it can provide to companies... But it said that historical episodes of investment booms provide “instructive parallels” — among them the expansion of canals in the 1830s, railways in Britain in the 1840s and the dotcom boom of the late 1990s.

These all had one key feature in common, said the BIS, “a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify”.

A major equity market correction associated with AI could have broader implications today than in the past, the BIS said, because households have greater exposure to shares relative to their wealth and income. Financial stability could also be endangered, given the volumes of debt being sold by AI companies to finance their investment, it warned.

“Perils have grown with pressure points around risks of persistent inflation, the sustainability of AI-related investments, growing financial vulnerabilities and weakening fiscal positions,” it said.](https://pbs.twimg.com/media/HL_IjCEWsAAZu8W.png)