UBS says 60% of companies now watching AI budgets are moving to cheaper models and open-source Chinese models

The pressure is coming from extreme bills, including users spending up to $35K/month, teams exceeding quotas by 200%, and companies cutting internal AI tools from 5 to 2.

Companies are not abandoning AI, they are using model routing, which sends easy tasks to cheaper models and saves premium models for hard reasoning, code, and long-context work.

Chinese open-source models such as Qwen, DeepSeek, MiniMax, GLM, and Kimi now fit the enterprise cost curve because they can be run locally or used through cloud catalogs.

---

news .futunn.com/en/post/75068082/ubs-group-finds-60-have-already-started-curbing-ai-spending?level=2&data_ticket=1780870170397383

Copper just hit a fresh all-time record high, powered by surging AI data center demand. Citi says it’s time to chase the move higher.

The message hasn’t changed: copper is the fundamental metal of the global economy, and there simply isn’t enough of it. AI, electrification, and the broader energy transition are colliding with persistent supply constraints. Mines take decades to build, permitting remains broken, and existing operations face growing headwinds.

At @IvanhoeMines_ we’re proud to be delivering some of the world’s highest-grade copper from Kamoa-Kakula and advancing the next wave of projects.

The supercycle isn’t coming, it’s here.

Early innings still.

https://t.co/lkXrOpZOzw

Here's the pattern nobody talks about:

2010 -> Compute was scarce. Cloud won.

$AMZN $MSFT

2015 -> Phones and data exploded. Platforms won

$META $GOOG

2020+ -> AI compute was the bottleneck. Chip makers won

$NVDA $AMD

Bookmark.

Now, The bottleneck moved to :

• Photonics → $AAOI $AXTI $AEHR $LITE

• Space → $RKLB $ASTS $LUNR $PL

• AI Inference → $AMD $ARM $INTC $RMBS

• Power Semis → $VICR $NVTS $MPWR $ON

• AI Infra → $NBIS $VRT $IREN

• Energy → $CEG $VST $NEE

• Robotics → $VPG $SYM $OUST

• Defense → $ONDS $KTOS $AVEX

This is where capital is flowing next.

Capital flows to necessity.

Find the bottleneck.

Invest in what removes it.

Next Idea on: https://t.co/DGS6tWOxF9

Major Gold Miners and Royalty Giants - Valuations: At the current gold spot prices, the P/NAV and FCF/EV valuations are well below their historical highs for producers. Here's an interesting chart from RBC. 🪙👇

$GDX $NEM $AEM $B $WPM $FNV

The entire copper industry has just returned from last week’s leading copper conference in Chile (CESCO), with participants, including the world’s largest copper traders, even more bullish that all-time-high copper prices could be tested over the coming weeks.

It’s become crystal clear that both China and the US are frantically stockpiling despite industrial supply chain uncertainties related to the conflict in Middle East.

The rivalry between the two superpowers could easily pull the king of metals up to $15,000 per tonne quicker than we can imagine.

ITS A FULL ON GLOBAL TUG-OF-WAR

THE OPTICAL PHOTONICS BOTTLENECK

As AI clusters scale past copper’s physical limits, the bottleneck shifts to optical & these are the companies building that layer across the stack:

1. $AAOI building the transceiver layer of the AI network through vertically integrated U.S.-based InP laser manufacturing. It has already secured over $200M in its first volume 1.6T order from one hyperscale customer followed by another $124M in 800G orders from a second.

2. $AEHR building the reliability layer for the optical & AI hardware stack through burn-in & test systems. It just received a record $41M follow-on order from its lead hyperscale customer reinforcing the idea that Sonoma is becoming a key production burn-in platform for high-power AI ASICs.

3. $CRDO building the connectivity layer that helps AI clusters move data faster through active electrical cables, retimers & high-speed interconnect silicon. The DustPhotonics acquisition also extends that platform into silicon photonics before copper becomes a real constraint.

4. $LITE building the laser layer of the AI optical stack through EMLs, optical components & optical switching exposure. The setup is backed by a $2B $NVDA strategic investment & optical circuit switch backlog above $400M with orders reportedly extending through 2028.

5. $VIAV building the testing & validation layer of the optical stack through network instrumentation & photonics measurement tools. It is the picks-and-shovels layer of the transition because every high-speed optical buildout still needs to be tested regardless of which transceiver vendor wins.

6. $COHR building one of the core photonics bottlenecks through indium phosphide lasers, optical engines & communications components tied to next-gen AI networking. It also has a $2B $NVDA strategic investment behind it & is doubling InP device capacity into the 1.6T ramp.

7. $MRVL building the DSP & optical infrastructure layer through electro-optics, PAM DSPs, interconnect silicon & custom networking chips. The Celestial AI deal & NVLink Fusion exposure both strengthen its position as photonics becomes more central to AI cluster design.

The global sulphur squeeze has transitioned from a theoretical risk to a direct catalyst for a production cliff.

From Indonesian nickel to DRC copper, the leaching chemicals that power the green transition are hitting a wall.

Reuters reports that Indonesia’s nickel heavyweights— including Huayou Cobalt, Lygend, and Tsingshan —have already been forced to trim output by 10%.

Meanwhile, spot sulphur prices delivered to Indonesia have exploded above $800/t, with distressed cargoes clearing as high as $1,000/t.

The Global Acid Test

This isn't a regional glitch; it’s a potentially structural floor-raising event for the entire battery metals complex:

▪️The Shutdown Clock: While HPALs haven't halted yet, BMO notes that inventories are running on fumes. One metal trader told BMO that if the supply chain isn't re-established by month-end, we move from "trimming" to forced shutdowns.

▪️The DRC Contagion: Per Reuters, major copper and cobalt producers in the DRC have seen key chemical orders cancelled this month, forcing immediate usage cuts and weighing on output guidance.

▪️The Copper Major: London-listed Antofagasta is warning that rising acid costs are now the "biggest near-term concern" for copper miners globally, https://t.co/zKH2X4HWPZ reports. The issue could potentially threaten 2026 production goals.

The market is currently pricing this as a temporary logistics hiccup, and all eyes are on the Strait of Hormuz for a signal.

https://t.co/KB9n4nSK9W

"That's not how commodity markets work"

Jeff Currie joined @DavidVGreely at #CERAWeek where they explored the Iran war’s impact on energy markets, including the scale of the supply shock and how regional dislocations are emerging across global markets.

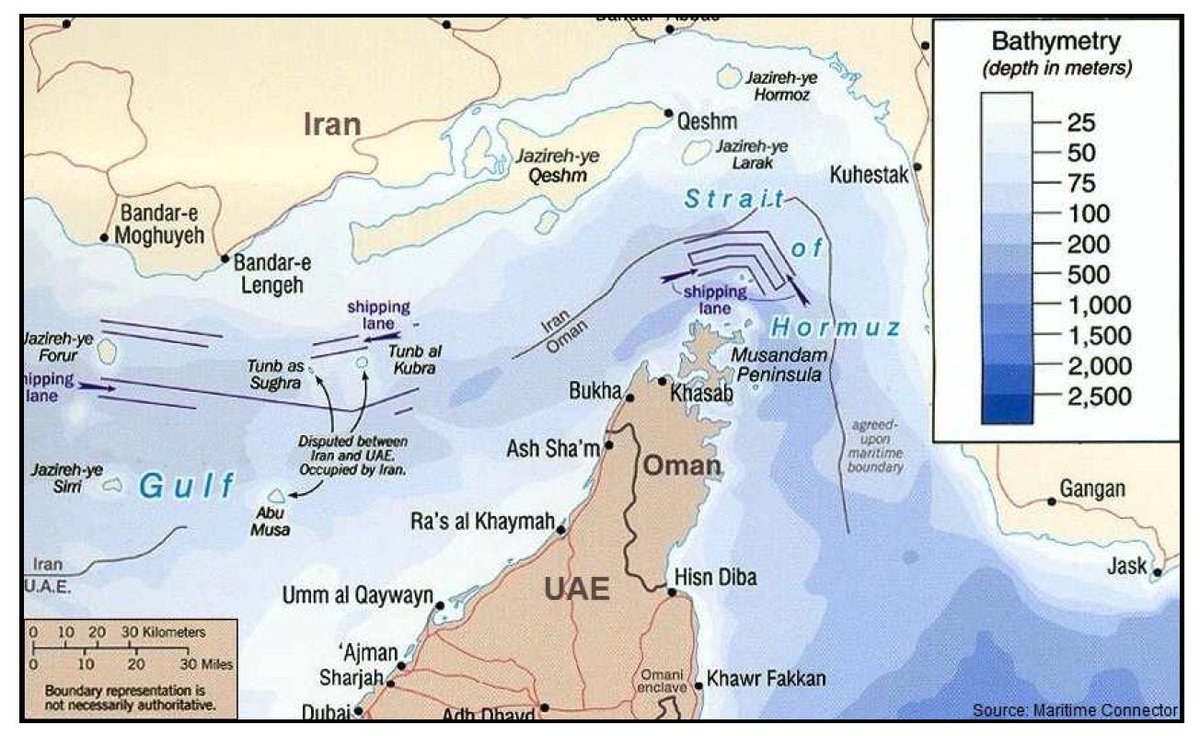

The New York Times reported on April 10, citing US officials, that Iran has been unable to fully reopen the Strait of Hormuz because it cannot locate all of the naval mines it laid in the waterway and lacks the capability to remove them. The IRGC used small boats to plant mines haphazardly during the early weeks of the war. Many locations were never recorded. Some mines have drifted from their original positions. Iran does not have a complete map of what it put in its own water.

When Foreign Minister Araghchi said on April 8 that safe passage through Hormuz would be possible “with due consideration of technical limitations,” US officials now confirm he was not being diplomatic. He was being literal. The technical limitation is that Iran mined its own strait and lost track of where the mines are.

Iran published a chart on April 9 through Tasnim and ISNA showing a large circle marked “danger zone” covering the standard shipping lanes, with two alternative IRGC-controlled routes around Larak Island. This is the chart of a country directing traffic around its own weapons because it cannot guarantee the weapons will not detonate under the traffic it is trying to collect tolls from. The toll system, the IRGC coordination, the escort protocol, the VHF passcode, all the infrastructure built to monetize the chokepoint exists because Iran cannot simply reopen the chokepoint. The tollbooth is not leverage. The tollbooth is a workaround for a self-inflicted minefield.

Richard Meade, editor-in-chief of Lloyd’s List, described the situation during an April 10 webinar: “As of this morning, the Strait of Hormuz remains both open and closed, depending on your position, both geographically and geopolitically. It is, if you like, Schrödinger’s Strait.”

Traffic on April 10 stood at 7 to 18 ships per day, with only 2 to 4 tankers, against a pre-war baseline of roughly 140 daily. Over 1,000 vessels are queued outside the strait, including 187 tankers carrying an estimated 172 million barrels of stalled crude. The backlog alone would take weeks to clear even if every mine vanished overnight.

And the capacity to clear mines does not exist on either side. The US Navy decommissioned its last dedicated Avenger-class minesweepers before the war. It now relies on Littoral Combat Ship mine countermeasures modules that have never been tested at this scale. The Royal Navy withdrew its last mine countermeasures vessel, HMS Middleton, from the Gulf in early 2026 and transported it home on a heavy-lift ship because it could not make the voyage under its own power. The West dismantled its mine-clearing capability months before the war that required it.

Trump demanded “complete, immediate, and safe opening” of the strait as the ceasefire condition. Vance is flying to Islamabad to negotiate terms that require a physical outcome neither side can deliver. Iran cannot find the mines. The US cannot sweep them. The UK sent its last minesweeper home on a cargo ship. And the ceasefire that was supposed to reopen 20 percent of the world’s oil supply is hostage to weapons that are drifting silently through a strait that nobody fully controls.

The most honest phrase in the entire ceasefire was “technical limitations.” It just took the New York Times to decode what it meant. The mines are still there. The talks start tomorrow. And 20 percent of the world’s oil is waiting on a map that does not exist.

https://t.co/0fIdGsM5qH

Retired Gen. David Petraeus, former head of U.S. Central Command, calls this "a tenuous ceasefire" and predicts there will not be a full resolution of the issues within the two weeks.

You think this war is about oil. It is not. Oil is the crisis you can see. The one you cannot see is sulfur. And sulfur is destroying industries that have nothing to do with the Middle East and everything to do with the periodic table.

The Strait of Hormuz carries 45 to 50 percent of the world’s seaborne sulfur trade. Sulfur is a byproduct of Gulf oil and gas refining. When the refineries run, sulfur accumulates. When the sulfur ships, it feeds the global sulfuric acid supply chain. When sulfuric acid reaches copper mines in the Democratic Republic of Congo, in Zambia, in Indonesia, in Chile, it is sprayed over heaps of oxide ore in a process called leaching that dissolves copper minerals into solution and produces 99.99 percent pure cathode. Twenty to 25 percent of the world’s copper comes from this acid-intensive process. Each tonne of copper cathode requires 3 to 3.5 tonnes of sulfuric acid. The acid comes from sulfur. The sulfur came through Hormuz. Hormuz is closed.

Sulfur prices have nearly doubled since February 28. The rally is the largest on record for the commodity. African copper miners, the ones who supply the cathode that wires everything from F-35 flight control systems to hospital ventilators to iPhone charging cables, are watching their input costs spike while the ore grade stays the same and the copper price falls on growth fears. The economics of leaching are collapsing at the exact moment the $1.5 trillion US defence budget demands more copper wiring for every weapons system it funds and every data centre the AI race requires.

Forty thousand tonnes of copper cathode per month used to flow through the Jebel Ali hub in Dubai. That flow is disrupted. Insurance premiums for Gulf shipping have surged 300 percent. The cathode is not destroyed. It is stranded, sitting in warehouses connected to a port connected to a strait that the IRGC controls and the United Nations just failed to authorise anyone to reopen.

The mechanism is invisible because sulfur is invisible. Nobody tracks sulfur futures on their trading app. Nobody tweets about sulfuric acid. Nobody writes headlines about heap leaching in the DRC. But the chain is unbroken and unbending: closed strait → halted sulfur → expensive acid → higher copper costs → more expensive wiring in every weapon, every vehicle, every building, every grid, every chip packaging substrate on earth. The war in the Gulf is not just repricing energy. It is repricing the base metal that conducts electricity in every system civilisation operates.

And sulfur is not the only invisible casualty. The strait carried helium for semiconductor cooling. It carried naphtha for petrochemical feedstock. It carried urea for fertiliser. It carried LNG for Asian power generation. Each one feeds a different supply chain. Each supply chain feeds a different industry. Each industry feeds a different population. The war hit one chokepoint and the damage radiated outward through the periodic table like cracks through glass, following the molecular bonds that connect everything to everything.

The last molecule standing was always methane. But methane does not travel alone. It brings sulfur with it. And the sulfur brings the acid. And the acid brings the copper. And the copper wires the world.

Nobody is covering the sulfur crisis. The sulfur crisis does not care.

https://t.co/dAOBBMsgDS

The energy system is broken at the physical level, says Jeff Currie

Physical markets are screaming shortage.

Paper markets are still pretending.

The gap is keeping markets from panic

Chaos is around the corner.

#Oil#EnergyCrisis#Commodities#Geopolitics

Oleksandr Yakovenko, the founder of TAF Industries, one of Ukraine's largest drone makers wrote a good response to @RheinmetallAG's Papperger's irritating statement. I used AI to translate it for you. It is worth reading in full.

"Dear Mr. Armin Papperger, CEO of Rheinmetall,

When you called Ukrainian drone manufacturers “Ukrainian housewives with 3D printers in their kitchens,” you demonstrated how deeply the European defense establishment still fails to understand the nature of modern warfare.

This is not about emоtions. This is about battlefield reality.

Here are the figures your industry refuses to acknowledge:

In 2025 alone, Ukrainian drones carried out 819,737 confirmed strikes. They accounted for 90% of all combat losses of the Russian army—more than all other types of weapons combined.

A single company, TAF Industries, produces up to 100,000 FPV drones per month. Over any given 90-day period, the products of my company alone have more confirmed hits than your entire fleet of equipment over its entire history of combat use across all conflicts. And most importantly—I built this company and achieved these results in two years, not fifty. Think about that.

Our drones achieve greater kinetic effect in three months than your flagship platforms have in half a century.

Why? Because the battlefield has changed, while your business model has not.

Russian electronic warfare has rendered GPS-guided Western munitions (Excalibur, GMLRS, etc.) almost ineffective.

Expensive and complex systems designed for wars with air superiority and conventional “peer-on-peer” conflict have become easy targets for drones costing $500–2,000 that attack them from above.

The cost-effectiveness ratio has been turned upside down: one 120mm Rheinmetall shell or one anti-tank missile costs more than a dozen of our drones—yet our drones still prevail.

This is not a “Lego game.” This is industrial Darwinism in real time. We iterate weekly. We lose factories to missile strikes and rebuild them within weeks. We print parts in basements and deploy 100,000 strike systems per month, while your engineers still require 3–5 years and hundreds of millions of euros to certify even minor upgrades.

The war in Ukraine is not a temporary anomaly. It is the first true drone-industrial war. And it has already proven that outdated European platforms—no matter how expensive or “serious”—are becoming increasingly irrelevant if they do not integrate the very technologies you are mocking.

So when you say “this is not innovation,” I hear something else: “We do not want to admit that the future is being written in Ukrainian workshops, not in Düsseldorf offices.”

The hashtag #MadeByHousewives is trending for a reason. Because these “housewives” destroy more enemy equipment every month than entire European armies do over full campaigns. And they do so while your industry continues to sell 20th-century solutions at 21st-century prices.

The invitation stands, Mr. Papperger. Stop laughing at the kitchen table. Come and learn how the war of tomorrow is actually fought. Because the next time someone asks, “Who needs tanks in the age of drones?”, the answer may be simpler than you think:

Those who still believe in 1979 will lose to those who are building in 2026.

With respect (but with facts),

Oleksandr Yakovenko

Founder of TAF Industries

One of those “Ukrainian housewives”"

https://t.co/oZnXASQAYw

A massive Swedish study followed 30,000 women for over 20 years and found that those who actively sought sun exposure had dramatically lower death rates from cancer, heart disease, and all causes.

The shocking part? Sun avoiders had roughly double the overall mortality.

Even heavy smokers who got plenty of sun had similar death rates to non-smokers who avoided it.

Sunlight appears to extend life through vitamin D, nitric oxide, and immune support - yet we're still told to hide from it. Are you getting enough sun?