A few months before he died I had dinner with Charlie Munger.

I spent over 3 hours with him.

I got to see his library.

I could ask him any question I wanted.

At 99 he was still *ferociously* intelligent.

The most important lesson I learned from him that night was: Go for great.

In typical Charlie fashion it’s a combination of 4 simple ideas:

1. Charlie looks at everything through the lens of history. Human nature does not change. The same behaviors repeat forever.

2. Charlie has a complete indifference to problems. Troubles from time to time should be expected. This is an inescapable part of life.

3. Wise people do not whine about problems. They prevent them:

"Wisdom is prevention." —Charlie Munger

4. Great businesses are rare. Great people are rare too.

Great people *and* great businesses produce fewer problems.

Your mission in life is to get into a great business (and stay there!)

and build relationships with great people.

Doing so will prevent the majority of problems that are under your control.

All of this can be remembered in the simple maxim: Go for great.

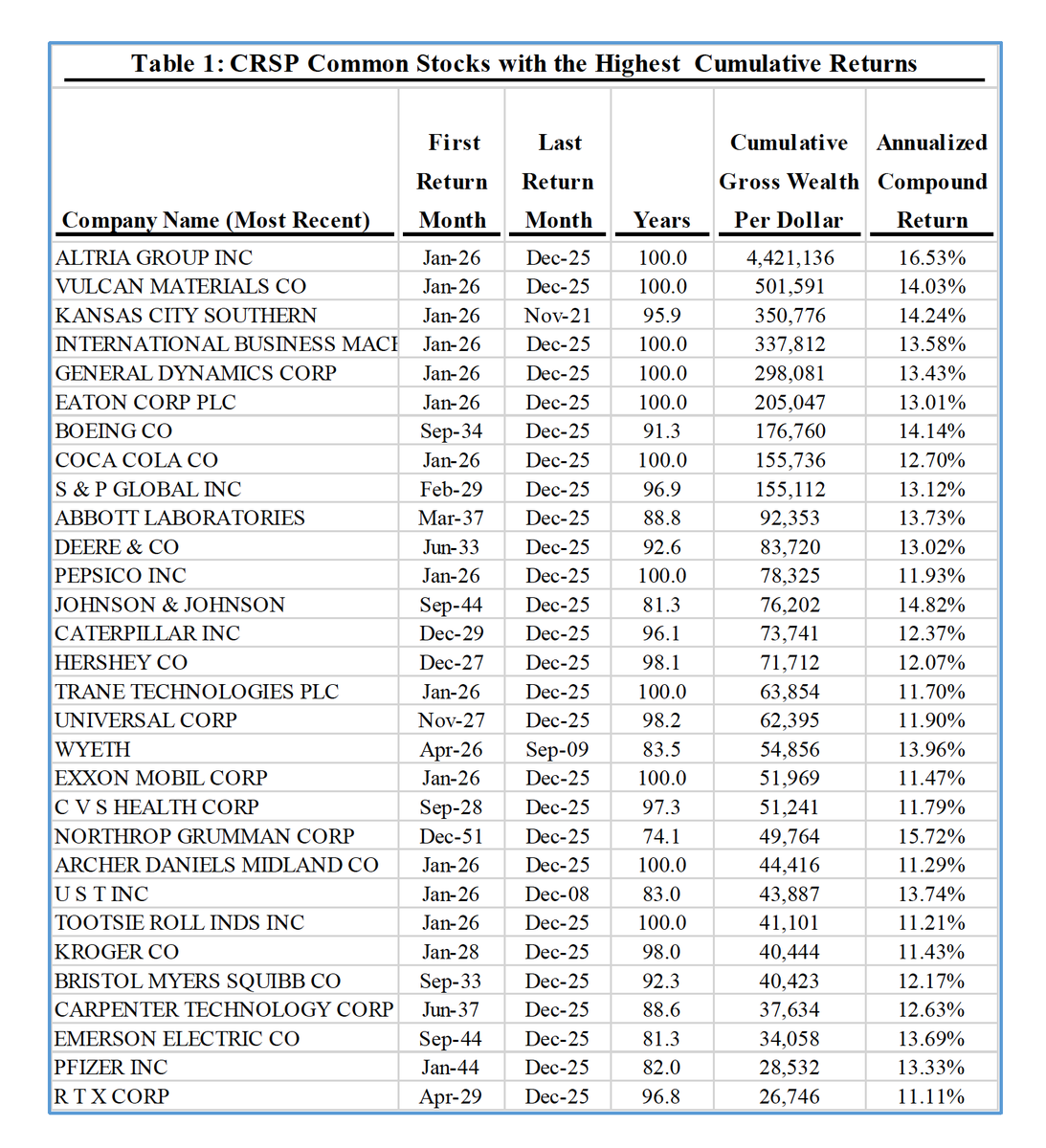

If grandpappy bought $1 worth of Altria stock 100 years ago and reinvested the dividends, it would be worth $4,421,136 today.

(ignoring Uncle Sam's cut)

https://t.co/xAeDUtYZMt

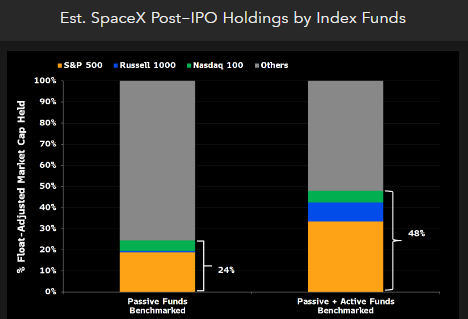

This is just the tip of the iceberg, but the majority of the supply will come when the lockups expire. This week only 5% of Spacex came. The other 95% is yet to come. The next big event will Anthropic/OpenAI in the fall

One of the highest levels of investing is recognizing what mainstream media sees as a red flag is often a green light.

The Business Week article was a hit piece. An astute investor would see through it and appreciate Singleton’s genius.

Passive S&P 500 funds could have to buy roughly 19% of public SpaceX shares within 6mo under fast-tracking framework (it would enter the index at the est 6th spot), Russell 1000 and Nasdaq 100 may buy another 5.5% within weeks of the IPO. Thrown in active MFs benchmarked to those indices and you get to HALF of SpaceX shares. Nice study from my colleague @rduboff

Most investors understand the bond yield curve.

Almost no one thinks about the equity yield curve!

The further out your time horizon, the fewer people you compete with, the bigger your edge, and possibly the higher returns, because, as I just said, fewer investors are willing to give an investment thesis this much time to unfold.

I don't think individuals can change much about themselves, including this.

This is how people can stay wrong on covid lockdowns, Ukraine war outcomes, AI economics even in the face of new evidence that comes out against their original thesis.

It seems very hard to beat the market if someone is prone to this, and most (90%?) people are. If someone is getting into investing, they should make an honest assessment if they do this. If so, they should just give up early.

🇩🇪 stocks = What is growth ?

🇬🇷 stocks = Let’s drop a 300 page report but won’t answer your emails

🇨🇦 stocks = We had a great quarters let’s dilute you to death

🇸🇪 stocks = Our regulators can’t still sniff out a scam

🇵🇱 stocks = We only answer if you are polish

🇯🇵 stocks = We have $5 billion in cash, our market cap is $2 billion, and we absolutely refuse to do a buyback, please have a bag of rice.

Was catching up with a friend from my days in public equities and was reminded of how investors will always *dramatically* overestimate how much any company actually knows about their own business

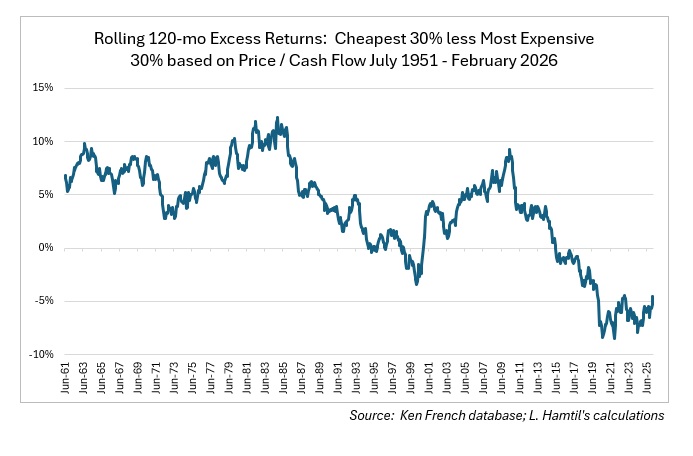

For most of modern history, a cheat code was to own the cheapest 30% of the market based on P/CF; you would have outperformed the most expensive 30% by ~3.6% per year. That has broken down since the GFC, & I haven't seen a satisfactory explanation.

Jensen falling for the trope:

"AI will commoditize a lot of things. Your things. My thing is extremely hard and it's out of reach for AI."

Great thing all the labs have ASICs projects, so we'll discover who's right.

Charlie Munger on how to succeed:

“It’s so simple: you spend less than you earn. Invest shrewdly. Avoid toxic people and toxic activities. Try to keep learning all your life. And do a lot of deferred gratification. If you do all those things, you are almost certain to succeed. And if you don’t, you’ll need a lot of luck. And you don’t want to need a lot of luck. You want to go into a game where you’re very likely to win without having any unusual luck.”

I might even spend more time thinking about these tail positions than the bigger ones.

There are a few buckets of small positions in my mind (ignoring things that can't be sized big due to liquidity):

1. Call-option type investments (such as levered equities) that have tail risk.

2. Things that are cheap but not cheap enough.

3. Positions that are cheap but have some issue where you can't size them big, like corporate governance / capital allocation.

4. Things you don't know that well, but own a toehold position .

For #1, I'd argue you probably minimize time spent once invested. Set it and forget it. Or maybe don't do them at all. #2 and #4 are probably worth spending time on, especially when news hit and the stock tanks and you can decide to make a core position. #3, I think these are a waste. Causes too much anxiety and you will never size them up. I also find these never do well!

The older I get, the more I'm convinced that enjoyment is one of the most underrated skills. If it costs a gallon of energy to move a mile, it doesn't matter how fast you go. You're not efficient. The person who finishes the day energized will always outpace the one finishing depleted.