This is WILD!

Goldman Sachs says Wall Street consensus 2027 hyperscaler Capex estimates are too conservative (Save this).

The consensus lands at $920 billion but Goldman thinks it could reach $1.4 trillion.

Here is how they get there.

Hyperscaler capex, the combined AI infrastructure spending of Amazon, Google, Meta, Microsoft, and Oracle went from $261 billion in 2024 to an estimated $805 billion in 2026, a 3x increase in two years.

The consensus for 2027 assumes growth decelerates sharply to just 22%, which is where Goldman pushes back.

Goldman economists compared that assumption against every major infrastructure buildout in history, railroads, highways, electrification, the internet and found they consistently consumed 2 to 3% of GDP at their peak.

At 2% of US GDP, hyperscaler capex reaches $950 billion in 2027 and at 3%, it reaches $1.25 trillion.

In the most aggressive scenario where hyperscalers deploy every dollar of operating cash flow plus the full capacity of the investment grade credit market, the number reaches $1.43 trillion.

The fourth chart is what makes the Goldman case feel earned rather than aggressive.

Hyperscalers are expected to reinvest 98% of operating cash flows directly back into capex in 2026, a ratio only ever matched during the telecom bubble of 2001.

The critical difference is that these companies are actually generating the cash flows that are being reinvested, Amazon, Google, Meta, and Microsoft combined are printing hundreds of billions in operating cash every year and putting nearly all of it back into infrastructure.

A buildout this large creates supply chain pressure and earnings volatility in the names most exposed, and Goldman is not dismissing that risk but the direction of spending is not in question, the only debate is whether 2027 comes in at $920 billion or $1.4 trillion.

The companies sitting directly in the path of that spending are the ones worth owning.

Nvidia captures the largest share of every hyperscaler capex dollar, owning 80%+ of AI training compute, and Morgan Stanley raised its 2026 capex estimate specifically because of continued Nvidia demand.

Oracle is the fastest growing capex spender among the five hyperscalers on a percentage basis up 116% from 2024 to 2027 with the smallest absolute base, giving it the most runway remaining.

CoreWeave and Nebius sit between the hyperscalers and frontier AI companies, renting GPU capacity to anyone who cannot get on the hyperscaler queue fast enough and as that capex number grows, so does their total addressable market.

Milk Road subscribers already up massively on these names, come join Milk Road Pro for our full breakdown and what other names we are watching for just a dollar.

Link below!

Capital markets are funding the AI buildout at historic scale: ~$400B over 6 months. Bitcoin ETFs have seen ~$4B of outflows since May 14, pressuring $BTC. This is a capital rotation, not a Bitcoin impairment. Volatility creates opportunity.

Goldman Sachs on memory:

- DRAM to remain in undersupply until atleast 2028 (undersupply of 5.0%, 5.9% and 3.9% in the years 2026, 2027 and 2028 respectively).

- DRAM global demand revised upwards, now expected to grow by 28%, 20% and 19% y/y in 2026, 2027 and 2028 respectively.

- NAND to also remain in undersupply until atleast 2028 (undersupply of 4.4%, 4.6% and 3.0% in 2026, 2027 and 2028 respectively).

- NAND global demand revised upwards, now expected to grow by 20%, 23% and 19% y/y in 2026, 2027 and 2028 respectively.

- HBM to remain in undersupply until atleast 2028 (undersupply of 5.4%, 6.0% and 4.3% in 2026, 2027 and 2028 respectively).

- HBM TAM expected to be $56 billion, $116 billion and $168 billion in 2026, 2027 and 2028 respectively.

Slowly, the overall consensus is shifting towards memory remaining in shortage until atleast 2028, while it was 2027 previously.

$MU $SNDK $DRAM $EWY

Google just opened up the floodgates for the Mag 7 to begin doing ATM offerings.

The Mag 7 used to buy back stock. Now they are dumping shares in the open market.

Why? AI infrastructure.

As long as the capex delivers an ROI, the market may reward it, but it looks like Google feels they have tapped the debt markets enough and now need to visit the equity markets.

They also got Berkshire to buy $10B at $350, showing that Berkshire is supporting the move.

This is incredible to witness...but my question is...will this give the other Mag 7 companies the freedom to do ATM offerings if the market is willing to let them?

This incredible to witness.

$GOOGL $META $AMZN $MSFT

🚨BREAKING: NVIDIA WILL NOW PAY YOU OVER $22,000 A YEAR TO HOST A MINI AI DATA CENTER IN YOUR HOME.

Here's how it works:

A startup called Span (with NVIDIA GPUs + homebuilder Pulte) just launched a program that installs a "node" outside your house, the size of an AC unit.

What's inside one box:

→ 16x NVIDIA RTX PRO 6000 Blackwell GPUs

→ 4x AMD EPYC server CPUs

→ 3TB of memory

→ a 15kWh whole-home backup battery

That's $200k+ of hardware sitting next to your air conditioner. You own none of it.

The deal for homeowners:

→ Free install (new builds first)

→ Span pays your electricity AND internet bills

→ You pay them one flat fee (~$150/mo)

→ Net savings can hit thousands a year

It runs on the "stranded power" your home never uses. The average 200-amp house wastes ~40% of its capacity. They're turning that into compute.

The vision is wild: Span says 8,000 of these nodes = a 100MW data center, but 5x cheaper and 6x faster to deploy. No new power plants. No 4-7 year grid delays.

AI demand is breaking the grid. Their fix? Skip the mega data center. Build it across thousands of suburban garages instead.

100-home pilot drops Fall 2026. Full rollout 2027.

The AI buildout just moved into your backyard.

SpaceX is about to be the largest IPO in human history.

But here’s the catch…

It’s also going to be the trade most retail investors REGRET for the next 5 years.

Here’s why, and the 4 space stocks I’m actually paying attention to instead:

On June 12, SpaceX will list on Nasdaq under the ticker SPCX.

The expected valuation is around $1.75 trillion.

That’s more than twice the previous record IPO, and more than the GDP of all but a handful of countries on earth.

But even if SpaceX doubles from there, your return is 100%.

In the same window, a small cap space stock with the right setup can do 5x or 10x.

The math simply does not work for retail investors hoping for asymmetric returns from a trillion dollar IPO.

You are buying a fully priced, fully discovered, fully institutional name on day one.

The real money in space is not SpaceX.

It’s in the smaller, less-followed public names that will get revalued the moment SpaceX trades.

Here are the 4 I am watching:

VELO Velo3D

3D prints metal parts inside SpaceX's Raptor engines. SpaceX backed them early and was their first customer. The cleanest direct supplier name on the public market.

RDW Redwire Space

The picks and shovels of space infrastructure. Solar arrays, deployable structures, microgravity manufacturing. The stuff every satellite and spacecraft needs.

BKSY BlackSky

Real-time earth observation satellites with major defense and intelligence customer base. Sub-billion-dollar market cap with a Pentagon backlog.

GHM Graham Corporation

Rocket turbopumps through its Barber-Nichols subsidiary. Already supplies multiple US launch players. Nobody is pricing the space exposure inside this name.

Most of these sit between $1 billion and $4 billion market cap.

Meaning even if they 5x to 10x from here, they would still be relatively small businesses.

That’s the power of an asymmetric bet. Either it goes to zero, or it does 5x to 10x over the next few years.

At The Assembly, we are a team of 8 with one goal: help you find the right stocks early.

Turn notifications on so you don’t miss our alerts. This is EXTREMELY important.

If you are not following us yet, you will understand later why that was a mistake.

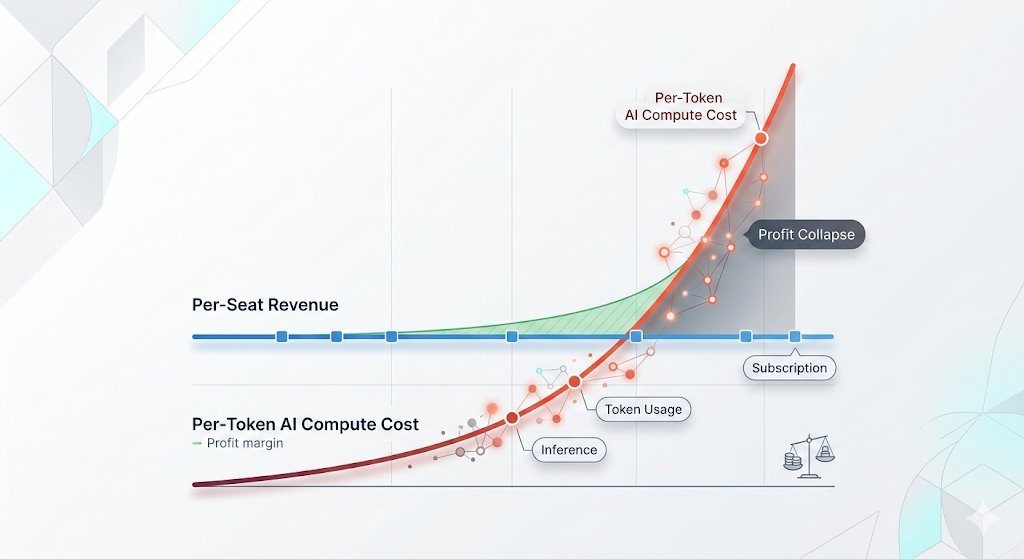

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

🇹🇭 Top foreign companies investing in Thailand in 2025

1. 🇸🇬 TikTok Digital Infrastructure Location: Thailand (Bangkok) $3.76 B

2. 🇨🇳 Beijing Haoyang Hyperscale Data Center Location: Rayong $2.24 B

3. 🇨🇳 Sunwoda Electronic EV Battery Cells Location: Chonburi $1.54 B

4. 🇨🇳 ZDATA Technologies Cloud Infrastructure Location: Rayong & Chonburi $1.22 B

5. 🇦🇪 DAMAC Digital Hyperscale Data Center Location: Pathum Thani $820 M

6. 🇭🇰 Digital Edge Data Center Location: Chonburi $750 M

7. 🇸🇬 Galaxy Data Center Data Center Location: Rayong $690 M

8. 🇯🇵 KDDI Interconnection Location: Bangkok $230 M

9. 🇯🇵 Mazda Motor Electrified Compact SUV Manufacturing Location: Rayong $150 M

In 2025, Thailand recorded approximately $18.8 billion in realized foreign direct investment (FDI) inflows, according to Bank of Thailand data.

🖇️ Source: ASEAN Skyline Rising

Koreans are surrendering life insurance policies to buy SK hynix, Insurance surrenders at the top 3 life insurers jumped 16% last quarter.

Savings bank deposits fell below 100 trillion won for the first time in 4 years. Commercial bank time deposits dropped 12 trillion won since February.

The entire financial system is being rerouted into 2 semiconductor stocks. When new money into a rally comes not from income but from liquidating safety nets, that is how the end of every cycle looks man, this is crazy .....

Investors over 50 now hold 62% of margin loans at Korea top 10 brokerages. Among those in their 60s, margin debt doubled from 3.9 to 8 trillion won in one year.

These are people who spent decades in fixed deposits and real estate, now entering a semiconductor rally on borrowed money at record highs.

When the KOSPI dropped 19% in March, leveraged investors in their 60s lost 20% on average. The rally recovered.

same thing in smaller model happening in India - MTF, i feel this so stupid

🚨 LEOPOLD ASCHENBRENNER IS OFFICIALLY BETTING BILLIONS THAT THE AI HARDWARE BOOM HAS PEAKED.

The exOpenAI researcher who was fired for warning that China could steal their AI models then turned $225 million into $5.5 billion in 12 months just filed his Q1 2026 13F with the SEC.

One quarter ago he had $5.5 billion in disclosed equity exposure. As of March 31, 2026 that number is $13.67 billion. The portfolio nearly tripled in a single quarter across 42 positions.

He initiated $7.46 billion in put options against every major semiconductor company between January 1 and March 31, 2026.

None of these positions existed in his Q4 2025 filing.

- SMH VanEck Semiconductor ETF PUT: $2.04 billion

- Nvidia PUT: $1.57 billion

- Oracle PUT: $1.07 billion

- Broadcom PUT: $1.01 billion

- AMD PUT: $969 million

- Micron PUT: $583 million

- Taiwan Semiconductor PUT: $535 million

- ASML PUT: $494 million

- Intel PUT: $159 million

For the past 18 months Aschenbrenner was betting only on electricity, memory, compute, and physical data center infrastructure. That made him one of the best performing fund managers in the world. And his long stock book still reflects that exact same thesis.

- Bloom Energy: $878 million

- SanDisk: $724 million

- CoreWeave: $556 million

- IREN: $401 million

- Core Scientific: $389 million

- Applied Digital: $320 million

- Riot Platforms: $142 million

- CleanSpark: $104 million

- Solaris Energy: $62 million

- T1 Energy: $43 million

- Bitfarms: $38 million

- Bitdeer: $29 million

- Power Solutions: $26 million

- WhiteFiber: $20 million

- Babcock and Wilcox: $19 million

- SharonAI: $18 million

- ProPetro: $13 million

- Hive Digital: $6 million

He is also running call options on specific names at the same time as his puts, which means he is not simply betting against semiconductors everywhere.

- Micron CALL: $422 million

- SanDisk CALL: $388 million

- Taiwan Semiconductor CALL: $354 million

- CoreWeave CALL: $140 million

- Bloom Energy CALL: $55 million

This means he believes the companies supplying power, storage, and compute to the AI industry still have years of growth ahead of them.

But the chip companies that Wall Street has been buying for the past two years at record valuations have already priced in everything good that is going to happen to them.

The man who has been right about every major AI trade for the past 18 months is now betting that the biggest names in semiconductors are about to fall.

If his track record means anything, the chip stocks Wall Street has been buying for the past two years may be in serious trouble.

$SE a few thoughts on the VIP program

In the past few quarters, while Shopee has been relentlessly investing in logistics and VIP, profits have actually remained pretty stable.

Adj. EBITDA / % of GMV:

Q2 2025: $228M / 0.77%

Q3 2025: $186M / 0.60%

Q4 2025: $202M / 0.55%

Q1 2026: $223M / 0.60%

In that time, VIP members have gone from 0 to 10M, generating over $20M per month (assuming $2 per month pricing on average) in recurring revenue. Annualised, that is $240M, which is the same level of profitability the business earns per quarter today.

They’ve been extremely generous with benefits (ranges country to country).

Let’s see with an anecdotal example. In Singapore, they charge $3.99 SGD for the monthly sub. In return, benefits are:

- Extra 3% cashback on all purchases

- Monthly 400 Shopee Coins (worth $4)

- 99x free doorstep delivery

- ChatGPT Go (3 months free)

- Super Duolingo (1 month free)

- Various other vouchers (Shell, https://t.co/RaCcnmQTFY, Pizza Hut, Surrey Hills, https://t.co/qQyDUaxb3J, Monee Insurance)

On an aggregate basis, this is probably worth upwards of $15 for the average user. The more interesting question will be with regard to cost. There is obviously no clear way to determine it, but from the cadence of profitability within the business despite aggressive expansion, it appears the VIP program is structurally more profitable than it first looks.

A few reasons why:

- Many benefits likely have very low marginal cost to Shopee

- Partner perks are probably subsidised/co-marketed

- Free shipping improves order density and logistics efficiency

- Cashback largely recirculates within the ecosystem

- VIP users have significantly lower churn (80% retention rate)

- Higher frequency drives ad monetisation (not to forget FinTech)

I think this is a real needle mover, especially as Shopee scales member counts to 20, 30, 40M. Today, the average VIP member spends 9.75x more than the average non-VIP member. Over time, this will come down as each incremental sign up is less likely to be a power user.

Still, I expect that Shopee can scale VIP members from the current 2.5% penetration to 15% minimum. If they were to spend 5x the amount of the average non-VIP member, that would generate over 75% of GMV. (Pareto Principle in action)

This doesn’t include Brazil, which I expect will do very well and has started rolling out in April (not included in Q1 numbers) @the_zack_zhu is forecasting ~40-50% QoQ growth for VIP members by end-2026 which I largely agree with.

This is the last step towards Shopee building out their moat, with the key purpose (imo) of extending their moat vs TikTok Shop. So far, GMV metrics have proven that this strategy works.

What impresses me most as I mentioned above, is just how profitable the VIP program likely is, not just because of the subscription revenue, but the incremental GMV spend and low cost structure of perks.

BILL ACKMAN JUST UPDATED HIS PORTFOLIO

This is everything he owned as of the end of Q1

Brookfield $BN - $2.73B

Amazon $AMZN - $3.01B

Uber $UBER - $2.25B

Microsoft $MSFT - $2.37B

Restaurant Brands International $QSR - $1.72B

Meta $META - $1.63B

Howard Hughes Holdings $HHH - $1.20B

Seaport Entertainment $SEG - $114.3M

Google $GOOG - $122.4M

Hertz Global Holdings $HTZ - $84.3M

Google $GOOGL - $12.8M

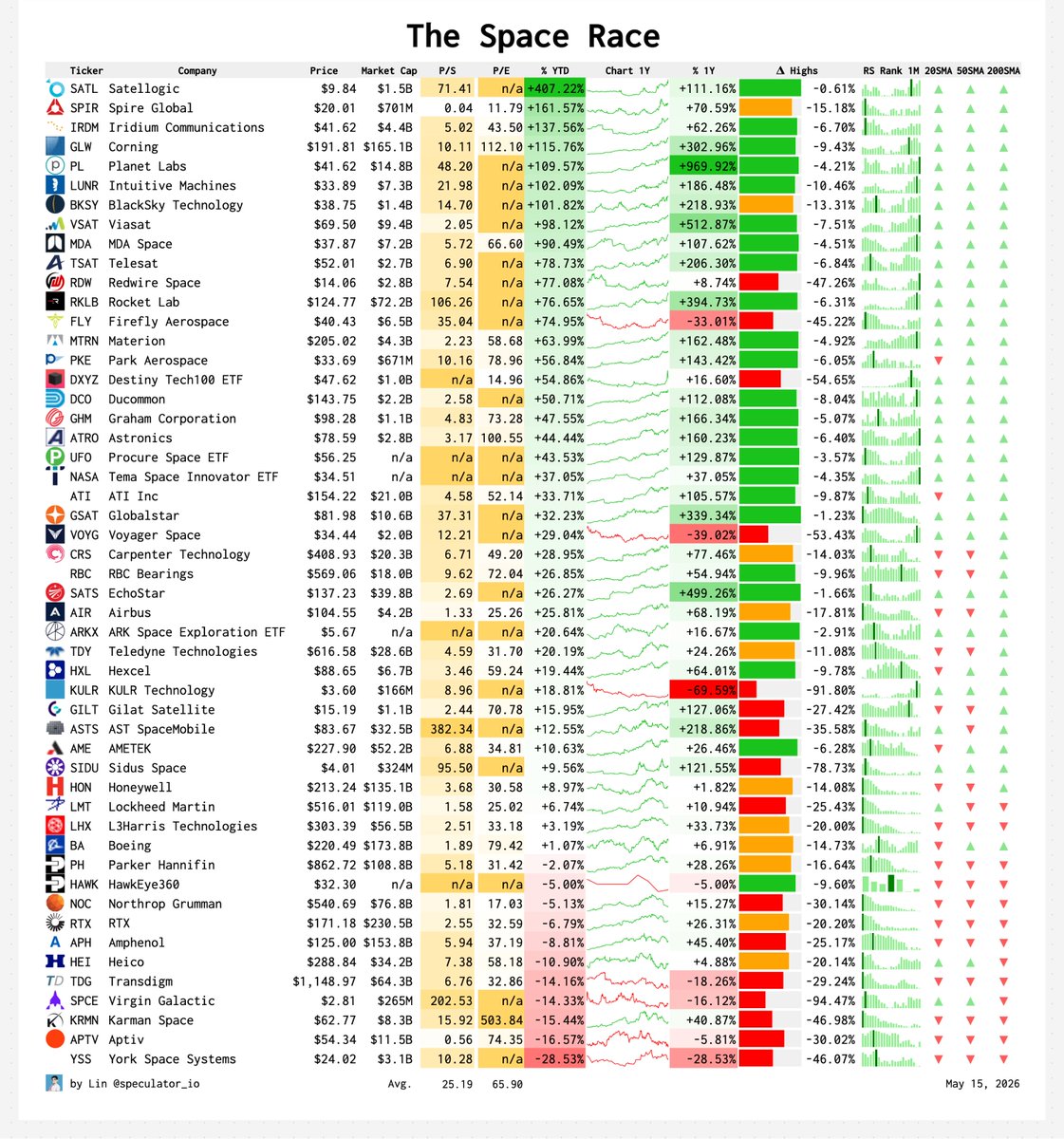

SpaceX $SPCX is planning to go public on June 12.

It's the biggest IPO in history and will instantly reprice the entire space sector.

These are the key space sectors to watch:

Launch Service Providers

$RKLB Rocket Lab

$FLY Firefly Aerospace

Space Imaging

$PL Planet Labs

$SATL Satellogic

$GSAT Globalstar

$BKSY BlackSky Technology

$SPIR Spire Global

$HAWK HawkEye 360

Satellite Communications

$ASTS AST SpaceMobile

$GSAT Globalstar

$SIDU Sidus Space

$SATS EchoStar

$IRDM Iridium Communications

$ETL Eutelsat

$TSAT Telesat

$GILT Gilat Satellite Networks

$VSAT Viasat

Space Infrastructure

$RDW Redwire Space

$LUNR Intuitive Machines

$MDA MDA Space

$VOYG Voyager Space

$YSS York Space Systems

Speciality Materials

$CRS Carpenter Technology

$MTRN Materion

$HXL Hexcel

$ATI ATI

$GLW Corning

$PKE Park Aerospace

Aerospace & Defense

$RTX RTX Corporation

$LMT Lockheed Martin

$KTOS Kratos Defense & Security

$VOYG Voyager Space

$LHX L3Harris Technologies

$NOC Northrop Grumman

$BA Boeing

$AIR Airbus

$HO Thales

Space Components

$TDY Teledyne Technologies

$APH Amphenol

$KRMN Karman Space

$RBC RBC Bearings

$PH Parker Hannifin

$AME AMETEK

$VELO Velo3D

$GHM Graham

$HEI Heico

$DCO Ducommun

$ATRO Astronics

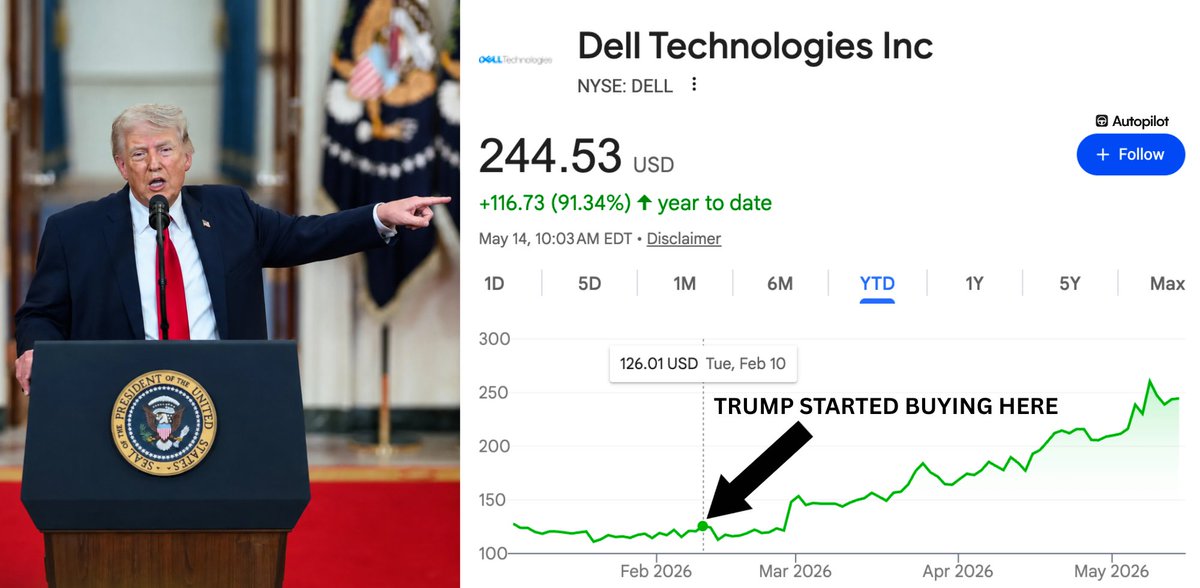

Donald Trump’s latest 278-T disclosure quietly revealed something crazy.

He owns more than $5 million worth of Dell stock.

He purchased multiple times starting on February 10, 2026.

On May 8, while speaking publicly, he told the country: “Go out and buy a Dell.”

At that exact moment, he was already one of the largest individual Dell shareholders in the disclosure.

He did not mention he owned the stock.

For context, Dell is one of the biggest beneficiaries of the AI server buildout, supplying complete rack systems for Nvidia GPU deployments. It is also reportedly part of the recent wave of major federal contracts.

A sitting president telling Americans to buy a stock he personally owns millions of dollars in is the kind of thing that would end the career of any corporate executive in the country.

For a president, it gets disclosed quietly on a government form 30 days later.

The system is not broken.

It’s doing exactly what it was built to do.

New insider trades will be revealed on @InTheAssembly tomorrow.

If you don’t follow them right now, you will regret it later.

Breaking: Trump owned DELL the entire time

On May 8th, Trump said "Go out and buy a Dell, they're great"

$DELL jumped 12% that day

What he didn't mention:

• He had already bought up to $5,000,000 in $DELL on February 10th

• Then bought more on March 2nd

• Then again on March 11th

• Then once more on March 23rd

The disclosure became public 4 days after the endorsement