US May PCE Inflation: take a look at the year over year increase of 4.8% in goods,3.3% in durables and 5.6% in non-durables. That is tariffs and AI related pricing pressures.

Second, look at the increase in service sector prices that advanced 3.8% from one year ago in contrast with 3.5% previously.

Falling oil prices will not impact those sticky service costs nor will it provide relief to trade policy induced inflation and the cap-ex supercycle driven by AI.

Finally, there is a large increase in US defense spending on the way to replenish the weapons stock and address the revolution in military affairs around drone and robotic warfare-which will draw on many of the same resources that are in demand from tech companies to support the AI buildout-will put pressure on core and topline inflation going forward.

Gold moves inversely with real US interest rates. Those are rising because markets think the Fed's reaction function is shifting in a hawkish direction under Warsh. That - plus the huge drop in oil prices - is driving up real rates as inflation tumbles...

https://t.co/qc9mdTqN5j

Core PCE

The Fed’s preferred inflation gauge again points to shelter as the primary driver of core PCE, yet policymakers refuse to confront their own role. Aggressive rate hikes have directly impaired housing affordability, raising mortgage costs and constraining supply, which in turn pushes rents higher.

This is not a coincidence; it is policy feedback. Wall Street Keynesians and central bankers alike ignore that restrictive monetary policy, in this context, is not curbing inflation, it is actively sustaining it.

Have a nice day.

The Non-Traversable Bridge Einstein Found Inside Gravity

Einstein’s equations not only describe gravity as a force but as the shape of Spacetime as well.

In 1935, Einstein and Rosen found that the Schwarzschild solution could be written in a way that reveals something astonishing:

Two separate exterior regions of Spacetime joined by a bridge-like throat

Rᵤᵥ = 0

This became known as the Einstein-Rosen Bridge.

It is often called a Wormhole, but the classical Einstein-Rosen bridge is not a science-fiction tunnel. In the standard Schwarzschild geometry, it is non-traversable. The throat does not remain open long enough for ordinary travel from one region to the other.

Its real power is mathematical.

It shows that General Relativity is not merely about objects moving through space. The theory allows Spacetime to have global structure such as different regions, horizons, extensions, and hidden connections that are not visible from one local patch alone.

The Einstein-Rosen bridge is one of the earliest glimpses of that deeper idea.

Gravity is geometry.

And sometimes, geometry has two worlds joined by a throat.

#Astrophysics #GeneralRelativity #Einstein #BlackHole #Spacetime #Cosmology #Gravity #Wormhole #Mathematics #Physics

Rising Dollar Is Deflationary

And you know my saying, "The Dollar Makes The Weather" and it's rate of change determines its severity...

https://t.co/BUIM4BuTVC

FCI Loop.

Inflation up -> Fed hawkish -> rates up -> dollar stronger -> stocks correct. If allowed to play out for 3-6 months, inflation solved.

But, stocks down -> bonds bid -> dollar reverses -> stocks moon -> story continues endlessly.

We are about to repeat this loop.

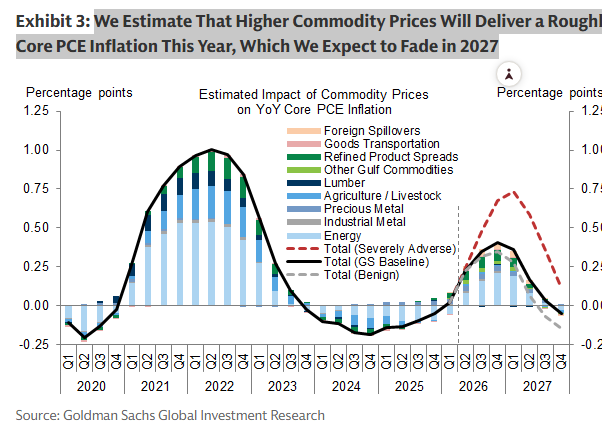

GS: We Estimate That Higher Commodity Prices Will Deliver a Roughly 0.4pp Boost to Year-over-Year Core PCE Inflation This Year, Which We Expect to Fade in 2027

Kind a perfect setup for the new Fed chair... he'll look like a hero

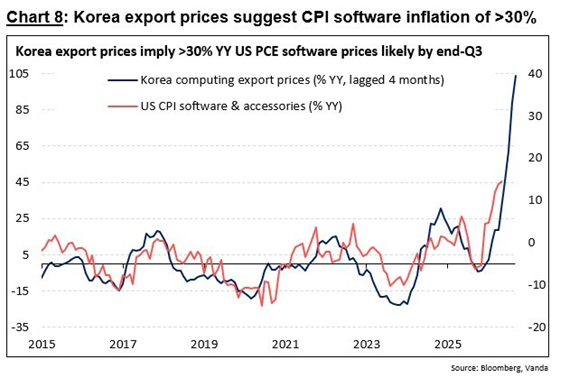

I find it interesting when I hear that AI is deflationary/disinflationary. If you look at something like CPI software, the price level has been in a deflationary trend for decades. Yet over the past 6 months, it has clearly broken out and increased at a 59% annualized pace

Yuval Noah Harari behoort tot de invloedrijkste denkers van deze tijd. Zijn boeken worden gelezen door politici, CEO’s en internationale instellingen. Zijn visie op kunstmatige intelligentie verdient een kritische analyse.

Wat opvalt is dat Harari AI vaak benadert vanuit een diep wantrouwen tegenover de capaciteit van gewone mensen om met nieuwe technologie om te gaan. Volgens hem dreigt AI democratieën te destabiliseren, verkiezingen te manipuleren, banen overbodig te maken en grote delen van de bevolking economisch nutteloos te maken. De impliciete conclusie is telkens dezelfde: de risico’s zijn zo groot dat technologische ontwikkeling niet aan individuen, ondernemers en markten kan worden overgelaten.

Dat is in essentie een moderne vorm van topdown luddïsme.

Niet omdat Harari machines wil verbieden. Dat wil hij niet. Maar omdat hij consequent de nadruk legt op centrale sturing, toezicht, regulering en mondiale coördinatie om de gevolgen van innovatie te beheersen. De onderliggende gedachte is dat een kleine groep experts de risico’s beter begrijpt dan miljarden individuen die dagelijks beslissingen nemen.

De geschiedenis wijst juist in de tegenovergestelde richting.

Bij de drukpers waarschuwden elites voor chaos en desinformatie. Bij de stoommachine voor massawerkloosheid. Bij elektriciteit voor maatschappelijke ontwrichting. Bij de computer voor het verdwijnen van miljoenen banen. Iedere technologische revolutie vernietigde bestaande functies, maar creëerde tegelijkertijd nieuwe beroepen, nieuwe markten en een hogere levensstandaard.

Wat Harari systematisch onderschat, is het vermogen van vrije mensen om zich aan te passen.

Niemand voorspelde de beroepen die ontstonden door internet. Niemand voorspelde miljoenen app-ontwikkelaars, social media managers, cloud engineers, YouTubers of digitale marketeers. De markt ontdekte die mogelijkheden spontaan. Niet omdat een ministerie een vijfjarenplan schreef, maar omdat ondernemers experimenteerden.

Vanuit mijn libertair perspectief is AI geen bedreiging voor de mensheid. Het grootste gevaar is dat overheden en internationale bureaucratieën AI gebruiken als excuus voor meer controle. Digitale identificatie, censuur van informatie, toezicht op communicatie en centrale regulering van kennisproductie vormen een veel concreter risico dan de technologie zelf.

AI is uiteindelijk slechts een instrument.

De vraag is niet of machines slimmer worden. De vraag is wie de macht krijgt over die machines. Een wereld waarin miljarden mensen vrij kunnen experimenteren met AI biedt ongekende kansen voor welvaart, innovatie en menselijke creativiteit.

Een wereld waarin een kleine technocratische elite bepaalt welke algoritmen zijn toegestaan, welke informatie mag circuleren en welke innovaties maatschappelijk verantwoord zijn, is veel gevaarlijker.

De geschiedenis leert dat vrijheid innovatie voortbrengt. Harari lijkt vooral bang voor wat vrije mensen met AI zouden kunnen doen.

Ik ben veel banger voor wat regeringen ermee zouden kunnen doen.

A man's ability to throw projectiles overhead leaves telltale traces on his face.

Humans have a remarkable and unique capacity to throw projectile weapons. The ability to throw overhand with power and accuracy, to wound and kill from afar, is a derived adaptation within the genus Homo that undoubtedly had a profound effect on the success of our ancestor, by offering advantages in fighting and hunting. As a result, the capacity to quickly infer this trait in others could have also been adaptive for the purposes of assessing coalitional partners, rivals and potential mates.

The current research investigates whether people can accurately infer the overhand throwing ability of others based on facial appearance.

We demonstrated that face-based inferences of overhand throwing ability are accurate, predicting an analogue of ancestral projectile weaponry, the javelin, among male track and field athletes. Moreover, we found that javelin throwers have distinctive facial shapes, which may be driving these perceptions. Facial morphometric analyses showed that javelin throwers could be distinguished from the other track and field athletes by more prominent brows, a narrower interorbital distance, a broader mid-face and a more elongated chin.

Finally, we replicate these effects and demonstrate that face-based inferences of overhand throwing ability can be decoupled from perceptions of physical strength and formidability. Overall, the ratings from male and female participants were highly similar across all three studies, which is consistent with the view that face-based inferences of overhand throwing could have been adaptive both in terms of assessing potential rivals and coalitional partners (male–male competition) as well as identifying mating partners that can provide, protect and provision (female choice).

Scientists have detected a steady seismic pulse every 26 seconds, first noticed in the 1960s. This “heartbeat” of the planet originates near the Gulf of Guinea off West Africa. Most evidence suggests it comes from ocean waves striking the continental shelf, though some researchers believe volcanic or hydrothermal activity may also play a role. Remarkably, this rhythm has persisted for decades, quietly resonating across the globe.

“Every living being is an engine geared to the wheelwork of the universe. Though seemingly affected only by its immediate surrounding, the sphere of external influence extends to infinite distance.”

— Nikola Tesla

Warsh fans will claim he declared a *NEW data-dependent regime change coming to the Fed.

Warsh critics will note he bashed the Fed particpants, process, data, track record & (most importatnly) its independence.

KEY: The end of forward guidance sets up an environment for opaqueness, based on data that is 'based' at best, corrupt at worst.

And given the changes to rules that determine CPI, BLS, now FED policy - under Trump - can you blame analysts for mistrusting the 'data' they producw... and Warsh?

So to pull this off - the 'management-by-committee' task-force approach Warsh is implementing with outside political voices helping to frame future Fed policy - Warsh will need to convince bond & equity markets alike he is able to suppress equity & bond volatility while he suppresses his FOMC committee's hawkish tilt.

You have to choose now: old way or new?

The Warsh-Affect is clear: diminish the legacy, obscure & distract. This will be the focus of his tenure. That and getting markets to BELIEVE they are pricing real data 'real-time', not Fed's reaction to the data - that is Warsh War & ultimate goal.

Do you see how insidious this is?

Warsh just made the Fed irrelevant & the market doesn't see it yet.

Good for equity bulls of course (assuming bond vigilantes don't call his bluff). But vigilantes are not well-organized like Trump/Bessent/Warsh. And they are far too patient.

Warsh is Akin to the Boy Who Cried Wolf and the bond market is the wolf.

Too often, the Boy reported a falsehood until no one believed him anymore.

Then the wolf was unimpeded in his feast of boy and flock alike.

We will revisit this story at a future point in time.

Good night.

For years now, the actual rate change announced at every FOMC meeting did not matter. By the time the meeting occurred, the move was priced into the SOFR curve weeks in advance. The only exception to this was in September 2024 when Powell surprised the rates market and cut 50bps. This was one of the only times where we went into a meeting with 50/50 odds priced into the market (either 25bps or 50bps). This meant that the market reaction was largely driven by the change in pricing once it was announced, not the future reaction function.

Before the ZIRP era, this was the common way to do things. However, under Yellen and Powell, and pioneered by Bernanke, the Fed mandate was to never surprise the rates market and ensure their move gets priced into markets well-ahead of time.

This is why for so many years casual Fed observers would be confused on days when for example we would cut rates and markets would sell off, or we held rates steady and rallied. The market reaction function was entirely dependent on forward guidance and forward expectations, not the announced change that day.

We are now going to enter a regime where what the Fed actually decides to do each meeting will be the marginal market driver again and that is by design.

In practice, I expect the next few meetings to be priced at 50/50 odds moving forward and that's by design. It is now up to rates speculators to analyze the economic data and come to their own analysis on where rates should be, the Fed will not be spelling it out for us any longer.

Overall, I think this is a good thing. Forward guidance was a tool from the ZIRP era pioneered by Bernanke as a way to ease monetary policy without going into negative rates. We are no longer in a ZIRP world and it was time to change this.

On net, expect higher rate volatility, more sensitivity to changes in SOFR in the economy, less smoothening of business cycles, and a return to a more pure Taylor rule-like reaction function.

This is a big shift and in my opinion a welcome one, despite my podcast being named Forward Guidance!

The SOFR long opportunity is imminent.

Leveraged fund shorts in SOFR futures just hit a record as the market's rate hike expectations have repriced dramatically in recent months.

The Warsh (and Bessent) Fed is stressing the large difference in headline and core inflation, which raises the bar for hikes.