water scarcity problem is getting solved before even it started..

CHINA JUST UNVEILS SOLAR DESALINATION BREAKTHROUGH

- They developed a 3D photothermal material that converts seawater into freshwater using only solar energy, with no external electricity.

- This material absorbs 90.2% of sunlight, cuts evaporation energy nearly by 50% and achieves an 8.5× higher evaporation rate than previous designs.

- A 0.75 m² outdoor prototype produced over 20 liters of safe drinking water per day, enough for about 10 people, while meeting WHO water standards.

- New system also irrigated a 5 m² test farm growing spinach, corn, and Chinese cabbage, demonstrating potential for both drinking water and agriculture.

- Researchers estimate that after about 2 years of operation, the production cost of freshwater could become lower than commercial bottled water.

Stanford has just leaked this free class that explains how claude and chatgpt work from the inside

The majority wastes 90% of its potential

Stanford teaches it to you in 1h50 minutes

Save this to favorites so you don’t lose it.

No sé si la mayoría entiende lo que está empezando.

Pero podría haber comenzado el mayor superciclo de materias primas de nuestra generación.

Y estos movimientos no aparecen todos los años.

Aparecen una vez cada varias décadas.

Pasó durante la revolución industrial.

Pasó después de la Segunda Guerra Mundial.

Pasó con la urbanización de China a fines de los 90.

Y ahora, la inteligencia artificial podría estar detonando el próximo.

Mientras la mayoría sigue mirando acciones tecnológicas después de subas enormes en los últimos años…

El capital grande ya empezó a rotar hacia otro lado.

Minería.

Energía.

Agricultura.

Materias primas.

Porque el problema ya no es la demanda.

El problema es que no hay oferta suficiente.

Los centros de datos que planean construir las grandes corporaciones necesitan cantidades gigantescas de cobre, uranio, energía y recursos básicos.

Y el mercado no está preparado para eso.

Durante más de 15 años casi no hubo inversión en minas, refinerías ni infraestructura energética por regulaciones, costos y falta de incentivos.

Y en commodities, cuando la oferta no alcanza…

Los precios no suben de forma lineal.

Explotan.

Una mina de cobre puede tardar más de 10 años en entrar en producción.

Ese desbalance no se corrige rápido.

Por eso muchos creen que estamos entrando en una etapa similar a otros grandes ciclos históricos donde las materias primas terminaron superando ampliamente a la bolsa durante años.

Y ni siquiera estamos hablando todavía del sector alimenticio.

Los fertilizantes ya comenzaron a dispararse.

La presión sobre alimentos sigue creciendo.

Y varios organismos internacionales ya advierten posibles tensiones fuertes para esta década.

La pregunta es:

¿Seguimos persiguiendo acciones después de años de suba o empezamos a mirar commodities antes que el resto?

Circle 🤝 Standard Chartered

@StanChart has launched institutional USDC minting and redemption through DIFC, becoming the first G-SIB to offer institutional access to USDC through a regulated banking channel.

A major milestone for institutional stablecoin adoption.

https://t.co/U18owEHWrm

The Internet's Settlement Layer Doesn't Get Disrupted by a Press Release.

@jerallaire laid it out with precision - and I want to add the builder's perspective from inside the @Arc ecosystem.

Everyone's talking about Open Standard and 140+ companies backing OUSD. Let me tell you what the data actually says, because stock tickers and Twitter hype are two very different things from onchain reality.

THE NUMBERS THAT MATTER

• @USDC processed $30 TRILLION in onchain transactions in Q1 2026 alone

• That's 80% of ALL dollar stablecoin volume. Not 30%. Not 50%. Eighty percent.

• 263% year-over-year growth in USDC transaction volume

• $77 billion in circulation with 28% YoY growth

• Top 3 most liquid digital asset globally - after BTC and USDT

These aren't projections. These are settled transactions. Real money moving through real infrastructure that took years to build.

STOCK PRICE ≠ NETWORK STRENGTH

Circle stock dropped ~70% from its June peak. Markets priced in fear of a consortium that hasn't shipped a single transaction yet.

But here's what markets missed:

• USDC's network effects compound with every new integration

• Thousands of applications already built on USDC rails

• Liquidity dispersed across dozens of platforms - not concentrated, not fragile

• The only large global stablecoin available in ALL of Europe AND Japan simultaneously

Stock markets price emotions. Networks measure fundamentals. USDC's fundamentals didn't flinch.

THE CONSORTIUM PROBLEM

140+ companies joining @openstandard is impressive optically. But Jeremy raised a point that deserves attention:

Consortiums have a historically dismal track record in shipping product.

• Revenue sharing sounds attractive until you realize it starves infrastructure investment

• "Everyone governs" often means nobody decides

• Circle tried consortium governance in USDC's early days - it created "endless challenges and complexity"

• Open USD hasn't launched yet. No chain announced. No regulatory clarity. No transaction processed.

Meanwhile USDC has been battle-tested through multiple market cycles, regulatory regimes, and technical stress events since 2018.

ARC L1: THE VERTICAL INTEGRATION PLAY

This is what most people are sleeping on.

@Circle isn't just issuing a stablecoin - they're building the entire settlement stack:

• Arc Network: Purpose-built L1 for stablecoin finance

• 244+ million testnet transactions processed

• $222 million raised in Q1 2026 presale at $3B valuation

• Backed by a16z, BlackRock, Goldman Sachs, Visa, ARK Invest, ICE

• Mainnet beta launching THIS summer

USDC on Arc isn't wrapped. It's not bridged. It's native. Zero friction settlement at the protocol level.

Open Standard is assembling a committee. Circle is shipping a chain.

THE REGULATORY MOAT

Today July 1, 2026 - is the MiCA full compliance deadline in Europe. Every stablecoin issuer must have full regulatory approval or face delisting.

USDC already has it. Globally licensed. EU-compliant. Japan-approved. GENIUS Act-ready.

OUSD? It doesn't exist yet. No regulatory pathway established. No compliance track record.

In institutional finance, compliance isn't a feature - it's table stakes. And USDC has been clearing that bar for years.

FROM THE ARC INDIA PERSPECTIVE

I am local leader- Arc House India Chapter - 1,250+ builders, operating in a market that processes 17 billion UPI transactions monthly with 800,000+ onchain developers.

What Indian builders need isn't another governance token or revenue-sharing pitch. They need:

• Battle-tested infrastructure that won't break under load

• Regulatory clarity that lets them ship product without legal ambiguity

• Native USDC settlement that works at India-scale throughput

• A chain purpose-built for payments, not retrofitted for them

Arc delivers this. USDC powers it. That's not speculation - that's architecture.

THE BIGGER PICTURE

Competition validates the thesis. 140+ companies didn't join Open Standard because stablecoins are failing - they joined because USDC proved the model works at $30 trillion quarterly volume.

This isn't USDC vs OUSD. This is the entire world waking up to what Circle has been building for 8 years.

The pie is expanding. And the builder with the deepest infrastructure, strongest network effects, tightest regulatory compliance, and a purpose-built L1 - isn't the one who should be worried.

They're the one everyone else is trying to catch.

Jensen Huang, CEO de $NVDA, esta llamando a que compremos acciones de energía, y es una señal que muy pocos están leyendo bien.

El verdadero cuello de botella en la explosión de data centers no es el hardware.

Es la energía. Te dejo 10 acciones que podrían multiplicar x10 por eso 🧵

The market is finally realizing Physical Ai is the next bottleneck , stocks to buy :

$OUST — Lidar sensors for robots and autonomous vehicles to perceive their environment.

$AMBA — AI vision chips for cameras, drones, and edge robotics.

$MP — Mines rare earth materials used in robot motors and actuators.

$SYM — Autonomous warehouse robots for picking and fulfillment.

$QCOM — AI processors and wireless chips for edge robots and autonomous devices.

$AMD — GPUs and CPUs powering the data centers that train physical AI.

$TER — Tests the semiconductors inside every robot and autonomous system.

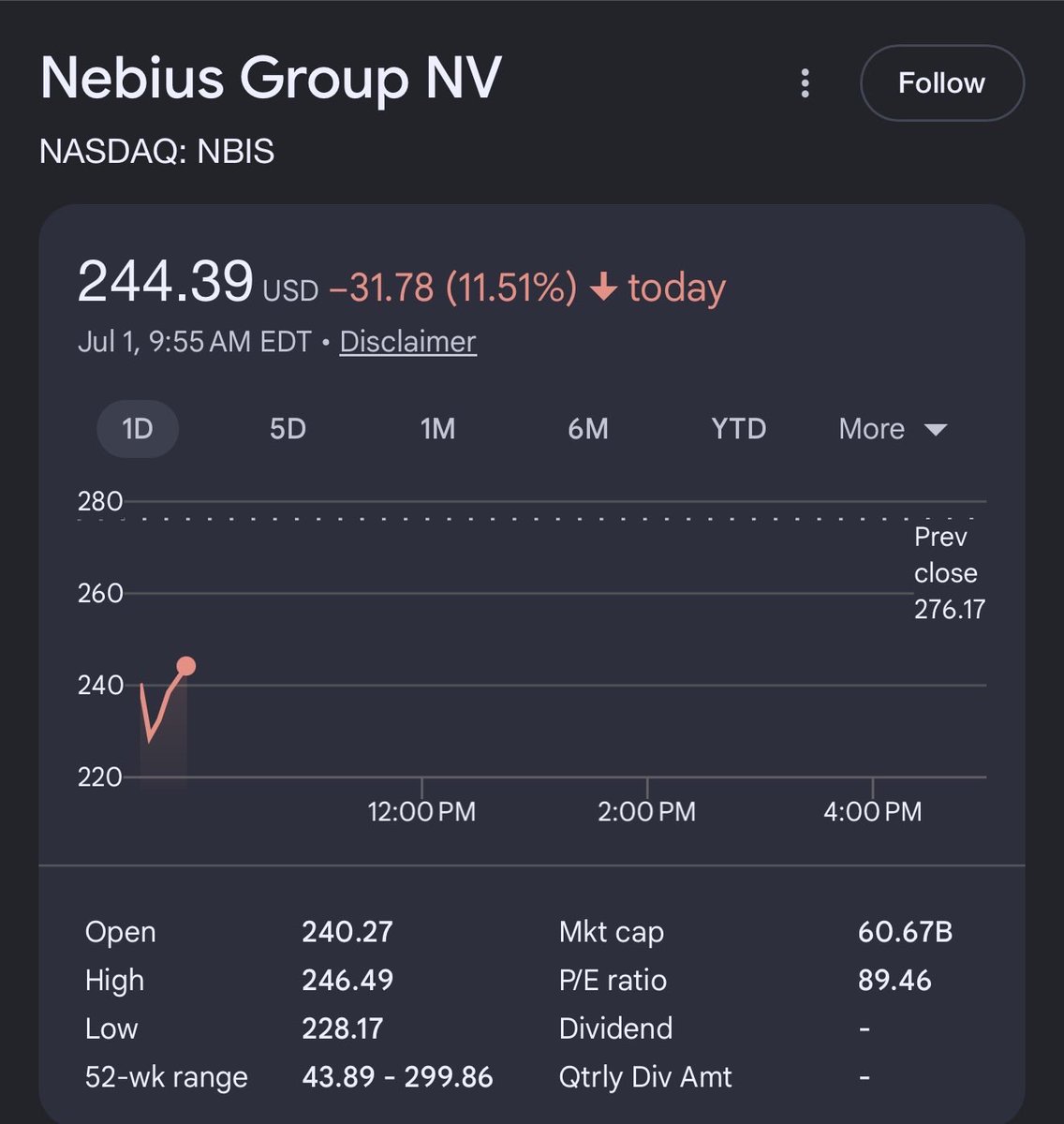

The market is overreacting to the Meta cloud news, and the irony makes it obvious.

Bloomberg reported $META might sell its excess AI compute, putting it in the same lane as neocloud names, and $NBIS dropped as much as 18% on the fear of a new competitor.

$META is already a $NBIS customer, with a capacity deal worth up to $27 billion. Meta is paying Nebius billions precisely because it cannot build compute fast enough on its own.

If Meta had endless spare capacity to sell, it would not be handing Nebius $27 billion to build more. The selloff is punishing Nebius over competition from the same company funding it.

This sector exists because demand for AI compute massively outstrips supply. Nebius grew revenue 684% last quarter and keeps selling capacity before it is even built.

They cannot build fast enough to meet the demand already signed, let alone worry about a competitor that has not launched anything.

This is a report of plans, not a product. Meta reselling leftover compute someday does not change the fact that the market is starved for compute right now.

Couple observations on Trump’s Stock portfolio 🇺🇸

- He’s not in any nuclear names that stand to benefit from the Trump admins nuclear efforts

- he’s not in any of the garbage stocks that his sons have pumped and dumped on everyone

- he’s not in any of the rare earth stocks that stand to benefit from the Trump admins rare earth efforts

- portfolio still mainly focused on American excellence

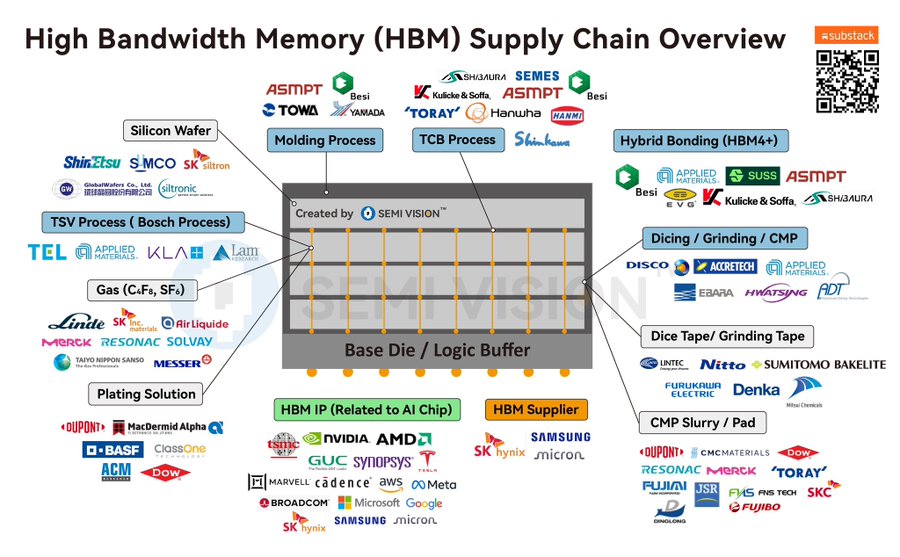

Total wafer fab equipment spending is projected to reach $145 billion in 2026, $200 billion in 2027 and $250 billion in 2028, a near doubling in three years driven almost entirely by HBM and advanced logic demand (Save this).

And this image above shows exactly who collects a toll on every single chip that gets built.

Before any HBM chip can exist, you need an ultra pure silicon wafer to build it on.

Shin-Etsu Chemical and Siltronic are the dominant global silicon wafer suppliers, with Shin-Etsu controlling roughly 30% of global supply, one of the quietest monopolies in all of semiconductors.

The most technically complex step is the TSV process drilling microscopic vertical holes through each silicon die so electrical signals can travel between stacked layers.

Tokyo Electron (TEL), Applied Materials (AMAT), KLA Corporation (KLAC), and Lam Research (LRCX) dominate this step,and all four beat earnings, raised guidance, and reported sold out capacity simultaneously in the most recent cycle, an extraordinarily rare alignment that signals just how tight the HBM supply chain truly is.

Applied Materials leads in deposition tools, Lam Research controls roughly 50% of the global etch market, and KLA holds a near monopoly at 55% share in process control and inspection, every wafer must pass through KLA's equipment to confirm chip integrity before moving forward.

The TSV etching process also requires specialized industrial gases, C4F8 and SF6 that create the precise chemical reactions needed to carve through silicon without damaging surrounding material.

Linde, Air Liquide, SK Materials, and Merck supply these gases and none of them are substitutable within current production timelines making them some of the most overlooked AI infrastructure plays in the market.

Once the dies are prepared, they need to be stacked and bonded together, currently via Thermal Compression Bonding, but the industry is shifting toward Hybrid Bonding for HBM4 and beyond.

Besi, ASMPT, Hanmi Semiconductor, and Kulicke & Soffa dominate the bonding equipment market, and the hybrid bonder market alone is projected to reach nearly $2 billion by 2028 as every memory maker upgrades to the next-generation process.

After stacking, chips need to be thinned, cut and polished through grinding, dicing, and CMP processes where DISCO Corporation holds near-monopoly control in precision dicing equipment, with DuPont, Dow, CMC Materials, and Resonac supplying the CMP slurry chemicals needed to polish chips to atomic smoothness.

All of this feeds into just three companies that actually build and sell HBM, SK Hynix with over 50% global market share, Micron ramping HBM4 for Nvidia's Rubin platform and Samsung fighting to regain ground after falling behind on qualification timelines.

And at the very bottom of the supply chain sits the demand engine, every hyperscaler and chip designer whose AI accelerators require HBM to function, Nvidia, AMD, Broadcom, Google, Microsoft, Meta, AWS, Marvell, and Tesla.

Every company in this supply chain is a toll booth and the traffic is only getting heavier.

Make sure to follow me @MelvinInvests for more semiconductor opportunities.

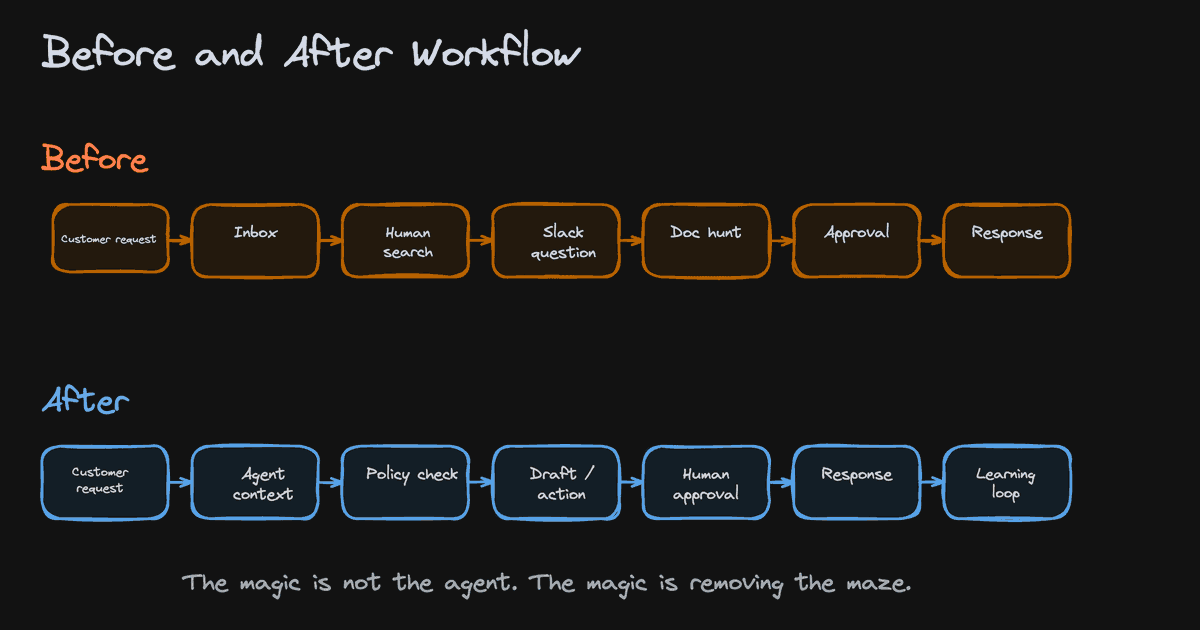

A friend asked me how to actually build a company that runs on AI agents.

I drew him 4 simple diagrams and this is what I told him:

For this to work, a few things have to be true.

- The humans move up to strategy, taste, and judgment while agents handle the execution.

- The whole business becomes readable to agents. Your data, SOPs, pricing, permissions, and decisions all live in one shared context layer.

- And you point it at the right work. Repetitive enough for an agent, complex enough that the incumbents never bothered. That's the goldmine.

In the old world, the company was the people. They held the knowledge, made the calls, did the work.

In this new world, the people become the creatives, the agents become the labor, and the company itself becomes the context layer.

That shared brain is the actual company now. The humans and the agents are just plugging into it.

Which means the most valuable thing you can build in 2026 is a business so well-documented that an agent can run it.

I see it everyday with @MeetLCA. I don't talk about it much publicly, but we've built a SWAT team for building AI-native orgs and AI-native products.

The moat is how legible your company is.

I drew it all out below.

GOLD TELEGRAPH CONVERSATION 16:

FRANK GIUSTRA

"This is not a normal bull market. We are going through a structural change in the global monetary system."

In this discussion, Frank breaks down why he believes we are witnessing the biggest structural shift in the global monetary system in generations, why central banks continue accumulating gold, how de-dollarization is reshaping global finance, and why he believes the coming decade will belong to hard assets.

Frank Giustra is the Founder and Chairman of Fiore Group and one of the mining industry's most successful entrepreneurs and investors.

Thank you for joining me, Frank. @Frank_Giustra

TIMESTAMPS:

(00:00) – On Argentina, Hyperinflation & Lessons That Changed His Life

(08:24) – Why 1971 Changed the World Forever

(15:21) – The Biggest Consequences of Leaving the Gold Standard

(22:02) – Are Central Banks Solving Problems or Just Delaying the Inevitable?

(25:47) – Why Central Banks Are Buying Gold at Record Levels

(29:02) – Does China Secretly Own More Gold Than the United States?

(29:47) – Will We Ever See a Fort Knox Audit?

(33:35) – China, De-Dollarization & The New Global Order

(37:16) – The Petrodollar System Explained

(41:28) – BRICS, Gold & The Future of Global Trade

(46:32) – Why Gold Still Matters More Than Ever

(49:49) – The Rise of Hard Assets

(53:31) – Why This Commodity Cycle Is Different

(55:14) – Bullish Copper Thesis

(01:00:54) – Are We Entering a Copper Supercycle?

(01:01:42) – Greatest Achievement

(01:04:52) – What Most Investors Still Don't Understand

Why is @jvisserlabs not long hyperscalers right now, even though he is bullish on AI?

Because the next 3-6 months in semiconductor infrastructure look like "equal news of disappointment with equal news of surprises." The market has priced in the largest earnings growth in its history.

His actual portfolio positions: long silver (expects 10x), long copper, long energy. Short narrative, long physical inputs.

The thesis: whoever wins the AI model war still needs silver, copper, and power to run. Own the inputs, not the output.

The AI mid-cycle slowdown argument and where Visser is actually positioned: https://t.co/sC4T7uAKCw

Source: The Pomp Podcast - https://t.co/ehw2PIa3sa

Japanese actor Hiroyuki Sanada spoke about the contradictions of human nature:

“Some people dream of having a swimming pool at home, while those who have one hardly ever use it. Those who have lost a loved one feel a profound sense of loss, while others often complain about their living relatives. Those without a partner long for one, while those who have one often don't appreciate it. The hungry would give anything for a meal, while the satiated complain about the taste of their food. Those without a car dream of owning one, while those who have a car are always looking for a better one.”

The key to happiness is gratitude: truly seeing and appreciating what we already have, and understanding that somewhere, someone would give anything for what we take for granted.

David Sacks just delivered an economics masterclass on Elon becoming the world’s first trillionaire.

@davidsacks: “People see the headline and imagine Elon suddenly has a trillion dollars in the bank. That’s not how it works. His balance sheet didn’t change overnight.”

Why?

The real point is deeper. Wealth isn’t in the “stuff” we consume. Food, shelter, clothes. Things that depreciate and disappear. It’s in the machines that create stuff for decades: tools, workflows, and corporations.

These are the true engines of human progress.

“If you create a machine that makes more stuff, then there’s a discounted present value for all the stuff in the future that machine might create. That’s where the wealth comes from.”

Elon started with nothing. An immigrant who slept on the floor building Zip2. He created these machines from vision and relentless effort. Thousands joined him, including a SpaceX welder who turned his labor into a million dollars in stock.

That’s the magic of tech and free markets: labor can become capital. It’s fluid.

The outrage misses this entirely. The people building machines that deliver medicines, energy, and abundance are creating lasting prosperity for everyone.

What do you think? Does viewing wealth as future productivity change how you see stories like this?