UK Royal Navy is pivoting hard to drone warfare scaling back traditional frigates and allocating £1B+ for hybrid combat vessels optimized for drone deployment.

The global shift to unmanned/autonomous systems is accelerating fast.

$ONDS (via Sentrycs, Iron Drone Raider, etc.) is building exactly the counter-drone and multi-domain solutions governments now need.

Strong macro tailwind. 🚀

https://t.co/hO4M1cvwPh

WHICH QUANTUM COMPANY IS THE MOST EFFICIENT?

We put together a graph @AsymmetricBets_ measuring revenue as a percentage of operating loss for FY2025. This is capital efficiency, how much revenue each company generates for every dollar it loses.

1.) $INFQ leads at 92 cents of revenue per dollar burned. The reason is the sensing business. They already sell quantum clocks, RF systems, and timing products into NASA, the DoD, and the UK government, and that segment is around 75% of revenue. Real hardware shipping today against a small $35M operating loss is what pushes the ratio this high, and much can be used to fund their push at computing.

2.) $IONQ comes in at 70 cents per dollar burned. They are the revenue king of the space at $130M in 2025, up 202% year over year, but they also spend aggressively, so the burn is far larger. Massive top line, heavier spend.

3.) $QBTS sits at 19.5 cents per dollar burned. Annealing is a narrower architecture than gate based quantum, but D-Wave has actual production deployments solving optimization problems right now.

And then $XNDU at 6.6 cents per dollar burned, the least efficient on the board. Photonic quantum is a real long term architecture, but Xanadu only went public in March and its revenue base is tiny against a heavy loss, so this number reflects how early they are rather than a broken business, though they have a massive potential.

$INFQ $XNDU $IONQ

PREDICTION: $INFQ will become the $PLTR of the quantum names as they’ll be the closest company with the US government.

We’ve already been seeing hints of this with Kinsella at the White House, $100 million dollar investment from the government, and their continuous partnerships and contracts received by the government.

But now this:

Their relationship just keeps on getting deeper and I expect big things coming for them. Think about the access they’re getting themselves and access is everything right now.

Will check back in on this prediction in the coming years $INFQ

Credit @MyQuant_um for the image

The comparison between $INFQ and $PLTR is highly accurate, as @infleqtion is perfectly mirroring @PalantirTech early playbook of deep government integration to build an unassailable moat.

Beyond the company's strong @WhiteHouse presence and massive government funding, three strategic pillars position $INFQ to become the $PLTR of the Quantum Era.

First, much like $PLTR early focus on immediately deployable software, $INFQ is prioritizing "Dual-Use" software and quantum sensing over distant hardware promises.

Platforms like Superstaq and QuIRC generate revenue today by solving critical military bottlenecks, such as GPS-independent navigation and advanced radio-frequency processing for the @USNavy. Second, $INFQ is establishing a sovereign monopoly in orbital infrastructure through its "Quantum Space Initiative."

By supplying the foundational quantum hardware for @NASA and next-generation defense satellites, they are making themselves structurally indispensable to national security.

Finally, their deep alliance with @nvidia has unlocked a massive commercial catalyst, allowing them to demonstrate the world’s first real-world material science applications using error-corrected, logical qubits.

By commercializing actionable software, monopolizing space defense infrastructure, and cementing a critical alliance with $NVDA, $INFQ is scaling exactly like early-stage $PLTR.

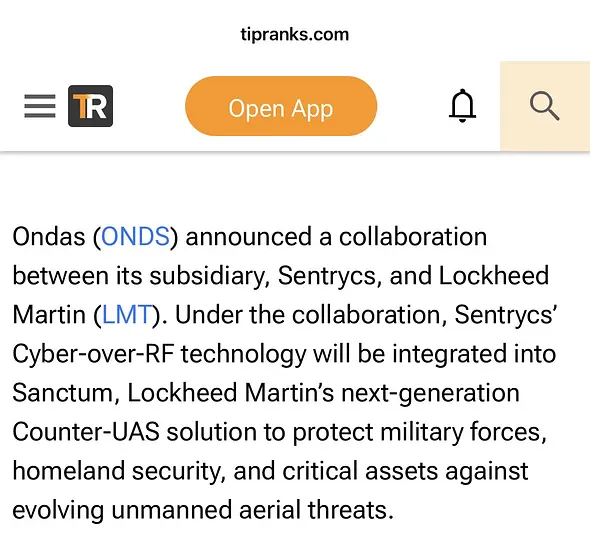

🚨 $ONDS LANDS LOCKHEED MARTIN C-UAS INTEGRATION DEAL

Ondas Holdings ($ONDS) announced that its Sentrycs subsidiary will integrate its Cyber-over-RF technology into Lockheed Martin's Sanctum™ Counter-UAS platform.

━━━━━━━━━━━━━━━━━━

🤝 Strategic Partnership

🛡️ Partner:

Lockheed Martin

🎯 Platform:

Sanctum™ Counter-UAS (C-UAS)

📡 Technology:

Sentrycs Cyber-over-RF

The collaboration adds an advanced cyber layer to detect and defeat hostile drones.

━━━━━━━━━━━━━━━━━━

🚁 What Makes It Different?

Unlike traditional C-UAS systems that rely on:

📶 Jamming

🎭 Spoofing

💥 Kinetic interception

Sentrycs operates directly at the drone communication protocol level.

Capabilities include:

✅ Detection

✅ Identification

✅ Tracking

✅ Taking control of unauthorized drones

✅ Safe landing of hostile drones

━━━━━━━━━━━━━━━━━━

⚡ Key Advantage

The system can neutralize drone threats without:

🚫 RF interference

🚫 Collateral communication disruption

🚫 Physical destruction

This is especially important around:

🏙️ Cities

🏟️ Stadiums

🏭 Critical infrastructure

✈️ Airports

🏛️ Government facilities

━━━━━━━━━━━━━━━━━━

🌍 Why It Matters

Drone threats are becoming a major national security issue.

Demand is growing rapidly across:

🪖 Military

🏛️ Homeland Security

🚔 Law Enforcement

⚡ Critical Infrastructure Protection

━━━━━━━━━━━━━━━━━━

📈 Why This Is Important For $ONDS

🏆 Validation from one of the world's largest defense contractors

🤝 Potential access to Lockheed Martin's customer network

🌎 Greater visibility in the rapidly growing C-UAS market

🚀 Expands Sentrycs' position in next-generation drone defense

━━━━━━━━━━━━━━━━━━

🎯 Bottom Line

This is a meaningful strategic win for $ONDS.

While financial terms were not disclosed, integration into a Lockheed Martin platform significantly enhances the credibility and potential adoption of Sentrycs' technology across military and homeland security markets.

$ONDS $LMT #Drones #Defense #CounterUAS #MilitaryTech #Security

Wedbush just initiated coverage on $INFQ with an Outperform rating and a $20 price target.

The interesting part isn’t the price target.

It’s why they believe Infleqtion is undervalued.

⸻

Most investors still think of Infleqtion as a quantum sensing company.

Wedbush argues that’s outdated.

The company is actually building three businesses on one neutral-atom platform:

• Quantum computing

• Quantum sensing

• Quantum software

That creates multiple ways to monetize the same core technology.

⸻

🧊 Why neutral atoms matter

The quantum race isn’t just about superconducting qubits anymore.

Neutral-atom technology is emerging as one of the most promising architectures because it offers:

• High qubit scalability

• Long coherence times

• Lower error potential

• Flexibility for both computing and sensing

INFQ is currently the only publicly traded pure-play neutral-atom company, giving investors unique exposure to this segment.

⸻

🤝 Validation is already happening.

Infleqtion isn’t developing in isolation.

Its ecosystem includes collaborations with:

• NVIDIA

• NASA

• DARPA

• Safran

• Voyager Technologies

These relationships don’t guarantee commercial success, but they do validate that major government and industry players see value in the technology.

⸻

🇺🇸 Government demand could become a major catalyst.

Quantum sensing is increasingly viewed as a national security capability.

As U.S. defense spending expands into quantum navigation, precision timing, and next-generation sensing, companies with proven platforms may benefit.

⸻

The investment case is becoming broader.

Investors aren’t just betting on a future quantum computer anymore.

They’re gaining exposure to computing, sensing, software, and defense applications—all built from the same underlying technology.

If the market begins valuing INFQ as a diversified quantum platform rather than a niche sensing company, today’s valuation gap could narrow significantly.

Sometimes the biggest catalyst isn’t new technology.

It’s the market finally understanding what a company already is.

I’ve brought my $ONDS share count up to 118k shares.

I consider $ONDS under $8 a gift from the heavens and will continue to add while this opportunity remains available.

To whoever is responsible for this price, thank you from the bottom of my heart.

$ONDS before more acquisitions ONDS should blow away the 2027 rev estimate of $692 mm

Here’s bottoms up guesstimates

Sentrycs $120 mm

Work view $100 mm

Rotron $100 mm

Omnisys. $70 mm

Mistral $200 mm

Indo earth. $75 mm

4M defense. $50 mm

Roboteam. $50 mm

Bird. $60 mm

Iron drone. $75 mm

Optimus. $40 mm

Cyberhawk. $70 mm

Omberg. $75 mm

Apeiro. $18 mm

That totals $1,103 mm

This is before more massively accretive M+A

Let’s grow it organically at 40%

2028 $1544

2029 $2,162

2030 $3,026

2030 stated (and obviously dated) goal is 2030 revs $1.5 B and 30% ebitda

Should roughly double the 2030 rev goal. And if 30% ebitda we are talking $908 mm

So assuming no more acquisitions ONDS trades at 1.5x 2030 revs. And 5x 2030

ebitda

Easily deserves 30x plus ebitda w that kinda growth. In which case it’s a 6 bagger from here and a roughly $50 stock

Of course these numbers will be materially higher. As doesn’t include more massively accretive m+a.

Plus worldview revenue potential is beyond silly. If you have in 4-5 years 1000 balloons a year, each flying 90 days and generating $30k per day revenues the WV revenues world be $2.7 B. It’s just math, people. Whereas if we grow the above WV 2027 estimate of $100 mm at 40% we get $275 mm. That’s an extra $2 B in 2030 revs. Too much? Fine. Call it an extra $1.0 B and we’re talking $4.0 B in 2030 revs and $1.2 B in ebitda

However you look at it ONDS is a screaming buy.

And the acquisition strategy has been brilliant. Those who whine incessantly about dilution ain’t gotta a clue. World view for example is likely worth $5-10 B to ONDS. And they paid $150 mm. At the midpoint ($7.5 B) that a 50x return. Tell me again about dilution…,

A very strong bull case scenario for $ONDS laid out below.

While it may sound overly optimistic, Peter is someone who’s been invested in this company for a while now and knows what he’s talking about.

Worth seeing what perfect execution might look like.

Not financial advice.

$ONDS x @GenevaInvestor

“America may have lost its technological military supremacy in the Iran war, due to the asymmetry brought by low-cost drones. This situation is far from over in my view, and America needs to rearm.

I think Ondas is positioned as the best consolidator in the drone warfare sector. In such a fast-paced, nascent environment, M&A is the company's strategic moat, not a weakness.

I view ONDS's layered, modular anti-drone technology stack and flexible deployment model as superior to single-solution competitors in addressing emerging defense needs.

The $982M IDIQ contract with the US Army validates ONDS’s relevance in the US military’s long-term drone procurement strategy.

With shares below $10, I rate ONDS a BUY and set a $30 price target, while closely monitoring dilution and competitive risks.”

$INFQ is, for me, the next stock that will skyrocket. I called it early with $SIVE, $LWLG and $ALMU.

First of all, the market cap is far too small for the massive potential of this quantum stock.

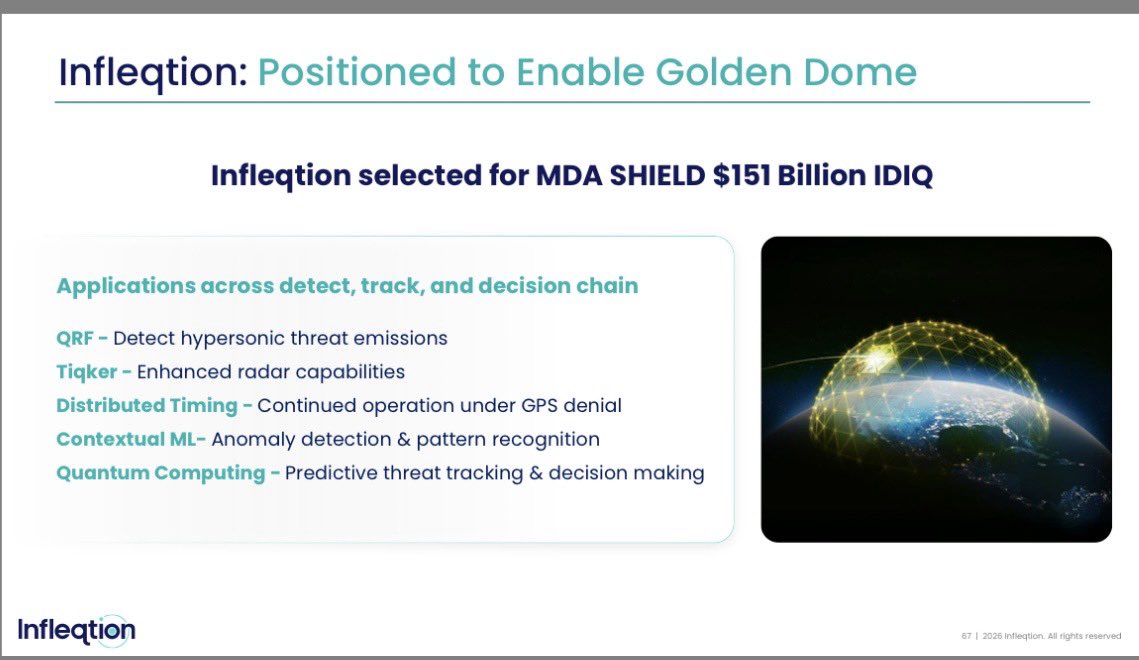

Let’s look at the strong partnerships, the incredibly experienced management, and the Golden Dome connection.

How can anyone still have doubts about this stock in the long term?

My 10x stock idea from GTC isn't photonics?!

But it does involve lasers.

Say hello to $INFQ.

It's a newly IPO'd quantum stock generating tens of millions in revenue in space + defense applications with very unique technology.

@infleqtion went public last month but it's trading 40% below its IPO price with a sub $2B market cap.

$INFQ trades at roughly 70x trailing sales on $29M in revenue. Compare that to $RGTI at $6B market cap on just $7M in revenue, that's 860x sales.

I chatted with $INFQ's Chief Administrative Officer, Julie McGee, to dig in further but here's the TLDR.

Most quantum companies need to cool their chips to near absolute zero temps just to operate.

Infleqtion uses "neutral atom" technology that traps individual atoms inside a glass cell using lasers and runs them at room temperature. It takes the power of a few hairdryers. No giant refrigerators. Way cheaper and way easier to scale.

And unlike most quantum names they're actually shipping products NOW. Quantum clocks for GPS-denied navigation, RF sensors, inertial navigation systems.

Selling to NASA, the DoD, and the UK government. Their quantum clock is being qualified by SpaceX for satellite systems.

Quantum brings a whole new level of precision that works on the ground, in the sky, and underwater. Their technology can enable submarines to navigate without ever linking up to a satellite.

GPS jamming is also becoming a huge problem on the battlefield, showing up in Ukraine and Iran. Quantum timing is inherently unjammable and unspoofable.

They also had a dedicated spot inside the Nvidia booth at GTC. $INFQ partnered with Nvidia to demo the first commercial materials science application running on logical qubits and are working with Nvidia's NVQLink to scale quantum-classical hybrid computing.

What's next: 30 logical qubits targeted this year, one of the most important milestones in the race to fault tolerant quantum computing by 2028. Plus a new NASA contract to measure Earth's gravity from space.

Infleqtion combines an attractive valuation with extremely unique technology (they're the only neutral atom quantum company publicly listed).

Could easily see this re-rating fast, I just think the IPO timing was poor with Iran.

Could be adding this as a lottery ticket to my Asymmetrical Bets portfolio soon...

This post was not sponsored or influenced in any way by $INFQ. All thoughts are my own, NFA / DYOR.

NASA's upgraded Cold Atom Lab is back in operation aboard the International Space Station, and Infleqtion hardware is helping it run.

By cooling atoms to temperatures just above absolute zero, the facility enables a state of matter that behaves according to the rules of quantum mechanics at a scale researchers can actually study. Microgravity makes those experiments possible in ways no ground-based lab can replicate.

Read ScienceDaily's breakdown on how the latest upgrade expands the facility's capabilities and what it means for the future of space-based quantum technology: https://t.co/zzgHewf3lS

📸: NASA JPL-Caltech

$ONDS 1. Lockheed Martin validation is huge. Sentrycs is being integrated into Lockheed’s Sanctum C-UAS platform — that puts ONDS technology inside a major defense-prime ecosystem.

2. This is not regular drone hype. Sentrycs is counter-drone infrastructure: detect, identify, track, and mitigate hostile drones without relying on messy jamming or kinetic takedowns.

3. The timing is perfect. ONDS already has Russell reconstitution, STOXX theme-index additions, heavy short interest, and fresh defense-order momentum stacked into the same window.

4. This strengthens the “platform” thesis. ONDS is not just selling hardware — it is building a defense/autonomy/software stack with Mistral, Sentrycs, Cyberhawk, and Optimus.

At the end you can follow me,I'll be updating you with the latest info on ONDS and more related content.

$INFQ Lot of presumptions flying around after the EO signing. People are already out here calling quantum winners. 🤣

Enough imagination.

Here are the facts:

The White House signed two quantum executive orders.

Google was in the room.

IBM was in the room.

Infleqtion was in the room.

The administration set a 2028 target for deploying a quantum computer capable of scientific research.

Agencies were directed to accelerate quantum sensing, networking, timing, navigation, and post quantum security technologies.

Reuters and Barron’s specifically identified Infleqtion as a beneficiary of the quantum sensing provisions.

Infleqtion CEO Matt Kinsella was present at the Oval Office signing and President Trump publicly acknowledged him during the event.

Everything else is speculation.

The facts are interesting enough on their own.

Ondas’s @Sentrycs is collaborating with @LockheedMartin to bring Cyber-over-RF counter-drone technology into the Sanctum C-UAS platform, supporting layered defense against evolving aerial threats. Its protocol-level approach lets operators detect, track, and safely control unauthorized drones without jamming, helping limit disruption to surrounding communications and infrastructure. $ONDS

https://t.co/LsPwPr75YG