Orlando Bravo: "The SaaSpocalypse is over... AI is an enormous, enormous tailwind for software companies... I was here last year at Super Return, and I think one of the LLM leaders made a comment that by this year, 50% of all white-collar jobs are going to be gone. And somebody in private equity made a comment that 50% of the people in this conference wouldn't have a job by next year. And look at the conference. You even had security outside. There's more people here than ever before... Our companies, 60% of the code that they write is machine-generated. But our number of developers, we have 20,000 of them, they're going up because now they can be a lot more productive."

What isn’t priced into Anthropic’s or OpenAI’s gigantic valuations is that they have no moat.

I use both ChatGPT Pro and Claude Max, and we’re reaching the point where there’s very little practical difference between Codex, Claude Code, GPT-5.5, and Opus 4.7.

That tells me the long-term value won’t sit in the model or harness layer. Those layers will become commodities, with pricing pushed down to token cost plus a thin margin.

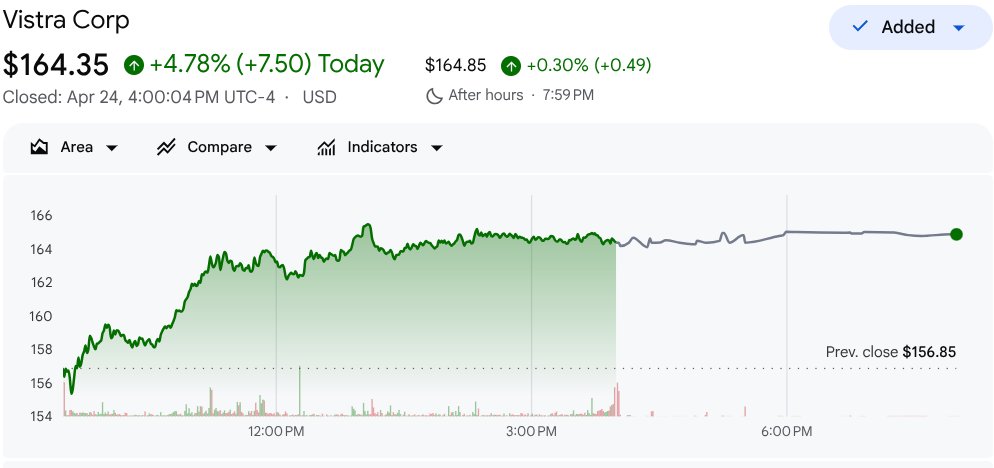

Vistra Corp $VST is the biggest position I carry, about ten percent of the book.

The pitch in one line: VST is the cleanest liquid expression of "who powers the AI." Every gigawatt of new data center load in ERCOT and PJM has to come from somewhere, and VST is the largest independent power producer across those two grids combined. They already have signed twenty-year power purchase agreements with Amazon and Meta tied to the pending Cogentrix acquisition, which adds 5,500 megawatts and is expected to close mid-to-late 2026.

The reason it's been a frustrating hold until very recently: the stock peaked at $220 in February and spent most of March drawing down twenty-five percent on a combination of natural gas at seventeen-month lows compressing merchant margins, a $4 billion debt issuance to fund Cogentrix, and regulatory overhang on PJM capacity pricing. None of those things broke the thesis, but together they took the stock from priced-for-perfection back to priced-for-skepticism.

What's changed in the last week: the $4 billion notes priced cleanly at 4.55 to 5.55 percent, removing the binary refinancing risk Morgan Stanley had been flagging. Jefferies argued in a fresh note that at current levels VST is trading at roughly an eleven percent FY28 free cash flow yield ex buybacks, and that the price is not embedding any future data center contract wins. Sixteen of nineteen analysts still rate it Strong Buy with a mean price target of $234.

What's coming into May:

a) April 27 to May 1, the hyperscaler earnings cluster. Microsoft, Meta, Amazon, Google. If aggregate AI capex is reaffirmed near the $630 billion bar the market has set, VST gets to participate in the AI re-rating without needing to do anything itself.

b) May 7, VST Q1 earnings before the open. Consensus is modeling more than two hundred percent year-over-year EPS growth. Options flow is skewed bullish into the print. The setup carries real binary risk in either direction, but the trailing seventy-two times P/E that scares people normalizes to roughly fourteen times on FY27 estimates if guidance reaffirms.

c) May 12, April CPI. A hot print pushes the ten year back toward 4.55 percent and pressures every duration-sensitive AI infrastructure name including this one. A cool print is the cleaner setup.

My probability-weighted twelve-month target is $184, about thirteen percent above current. That sits below the consensus $234 because I'm carrying a higher bear weight on a possible PJM capacity-cap proposal and on the Martin Lake arc-flash incident from April 21 that has not shown up in price yet. But the asymmetry is what keeps it the largest line: a $225 bull case if Cogentrix closes on schedule and a fresh hyperscaler PPA lands, against a $120 bear case if Q1 misses or PJM acts.

This is what the math says for me, not what it should say for anyone else.

The post-quantum cryptography debate has reached a tipping point. We still don't know when, or even if, a cryptographically relevant quantum computer will arrive. But one thing is certain: the transition to post-quantum cryptography is inevitable.

The traditional world has a clear roadmap. The timeline is largely set by NIST, which mandates the deprecation of vulnerable algorithms by 2030 and their full disallowance by 2035. Major enterprises and government agencies are already preparing, aiming to be migration-ready as early as 2029. The undertaking is massive, and, in my view, still underestimated. Remember the Y2K bug? Expect the same debate, several orders of magnitude bigger.

Encryption and key exchange will transition to ML-KEM (formerly CRYSTALS-Kyber). This is the most urgent front. The reason is straightforward: encryption is vulnerable to a "harvest now, decrypt later" attack. Adversaries can record encrypted traffic today and decrypt it once a sufficiently powerful quantum computer becomes available. Every day of delay widens the window of exposure. That said, encryption is largely a non-issue in the blockchain world, where the primary cryptographic primitive is the digital signature.

For signatures, two families dominate the PQC landscape:

- Lattice-based signatures (ML-DSA) — formerly CRYSTALS-Dilithium

- Hash-based signatures (SLH-DSA) — formerly SPHINCS+

Most of the industry outside blockchain will adopt ML-DSA, often in a hybrid configuration alongside traditional ECC. In the blockchain world, though the discussion is far from settled, sentiment is leaning toward hash-based signatures.

Why the divergence?

🔹ML-DSA is fast and produces compact signatures, but it relies on the hardness of structured lattice problems, a mathematical foundation that is comparatively young. The cryptographic community does not yet have decades of confidence in its security assumptions. The concern is not that a flaw has been found, but that the algebraic structure could conceal one.

🔹SLH-DSA produces significantly larger signatures and is slower to sign, but its appeal lies in simplicity and maturity: hash functions are among the best-understood primitives in cryptography. There is no hidden algebraic structure to exploit, hashes simply mix bits, and we have strong, long-standing confidence in their security.

For blockchains, where signature verification sits on the critical path and long-term trust assumptions are paramount, the conservative choice of hash-based signatures carries real weight, even at the cost of performance.

There is, however, a critical challenge that neither family handles well: multi-party computation (MPC) and threshold signatures. ML-DSA's rejection sampling makes secret-shared signing awkward, and SLH-DSA's structure is fundamentally built around a single signer with full state. For an industry whose security model rests on MPC custody, that gap may be the most underappreciated risk of the PQC transition.

Welcome Salesforce Headless 360: No Browser Required! Our API is the UI. Entire Salesforce & Agentforce & Slack platforms are now exposed as APIs, MCP, & CLI. All AI agents can access data, workflows, and tasks directly in Slack, Voice, or anywhere else with Salesforce Headless 360. Faster builds, agentic everything. 🚀

#Salesforce #Agentforce #AI

https://t.co/mxySdJS7HR

Running a company:

2020: can you survive a pandemic?

2021: still here? we’re going to give all of your competitors $100m series A rounds.

2022: wow, you made it? okay, all engineers cost $600,000/year now.

2023: nice job! okay, SVB failed and we’re going to take away your bank account.

2024: a survivor I see. but can you pivot from ai to crypto to defense tech back to ai-enabled defense tech in a 12 month period to stay relevant?

2025: unfortunately all of your competitors have raised $2b series B rounds. oh and only 500 engineers are relevant and they cost $100m/yr each.

2026: well, well, well. you’re still in business? let’s deploy the thunderclap of godlike LLMs from the heavens so all of your customers can rebuild your app in 2 hours. can you survive?

If you want to be “long blockchain growth”, and you only own $BTC, that’s the equivalent of being “long gambling” by investing in the 3-card monte guy in Times Square.

That said, there really isn’t an easy answer to being “long blockchain growth" because the list of investable tokens is so small

Today is a monumentous day for quantum computing and cryptography. Two breakthrough papers just landed (links in next tweet). Both papers improve Shor's algorithm, infamous for cracking RSA and elliptic curve cryptography. The two results compound, optimising separate layers of the quantum stack. The results are shocking. I expect a narrative shift and a further R&D boost toward post-quantum cryptography.

The first paper is by Google Quantum AI. They tackle the (logical) Shor algorithm, tailoring it to crack Bitcoin and Ethereum signatures. The algorithm runs on ~1K logical qubits for the 256-bit elliptic curve secp256k1. Due to the low circuit depth, a fast superconducting computer would recover private keys in minutes. I'm grateful to have joined as a late paper co-author, in large part for the chance to interact with experts and the alpha gleaned from internal discussions.

The second paper is by a stealthy startup called Oratomic, with ex-Google and prominent Caltech faculty. Their starting point is Google's improvements to the logical quantum circuit. They then apply improvements at the physical layer, with tricks specific to neutral atom quantum computers. The result estimates that 26,000 atomic qubits are sufficient to break 256-bit elliptic curve signatures. This would be roughly a 40x improvement in physical qubit count over previous state-of-the-art. On the flip side, a single Shor run would take ~10 days due to the relatively slow speed of neutral atoms.

Below are my key takeaways. As a disclaimer, I am not a quantum expert. Time is needed for the results to be properly vetted. Based on my interactions with the team, I have faith the Google Quantum AI results are conservative. The Oratomic paper is much harder for me to assess, especially because of the use of more exotic qLDPC codes. I will take it with a grain of salt until the dust settles.

→ q-day: My confidence in q-day by 2032 has shot up significantly. IMO there's at least a 10% chance that by 2032 a quantum computer recovers a secp256k1 ECDSA private key from an exposed public key. While a cryptographically-relevant quantum computer (CRQC) before 2030 still feels unlikely, now is undoubtedly the time to start preparing.

→ censorship: The Google paper uses a zero-knowledge (ZK) proof to demonstrate the algorithm's existence without leaking actual optimisations. From now on, assume state-of-the-art algorithms will be censored. There may be self-censorship for moral or commercial reasons, or because of government pressure. A blackout in academic publications would be a tell-tale sign.

→ cracking time: A superconducting quantum computer, the type Google is building, could crack keys in minutes. This is because the optimised quantum circuit is just 100M Toffoli gates, which is surprisingly shallow. (Toffoli gates are hard because they require production of so-called "magic states".) Toffoli gates would consume ~10 microseconds on a superconducting platform, totalling ~1,000 sec of Shor runtime.

→ latency optimisations: Two latency optimisations bring key cracking time to single-digit minutes. The first parallelises computation across quantum devices. The second involves feeding the pubkey to the quantum computer mid-flight, after a generic setup phase.

→ fast- and slow-clock: At first approximation there are two families of quantum computers. The fast-clock flavour, which includes superconducting and photonic architectures, runs at roughly 100 kHz. The slow-clock flavour, which includes trapped ion and neutral atom architectures, runs roughly 1,000x slower (~100 Hz, or ~1 week to crack a single key).

→ qubit count: The size-optimised variant of the algorithm runs on 1,200 logical qubits. On a superconducting computer with surface code error correction that's roughly 500K physical qubits, a 400:1 physical-to-logical ratio. The surface code is conservative, assuming only four-way nearest-neighbour grid connectivity. It was demonstrated last year by Google on a real quantum computer.

→ future gains: Low-hanging fruit is still being picked, with at least one of the Google optimisations resulting from a surprisingly simple observation. Interestingly, AI was not (yet!) tasked to find optimisations. This was also the first time authors such as Craig Gidney attacked elliptic curves (as opposed to RSA). Shor logical qubit count could plausibly go under 1K soonish.

→ error correction: The physical-to-logical ratio for superconducting computers could go under 100:1. For superconducting computers that would be mean ~100K physical qubits for a CRQC, two orders of magnitude away from state of the art. Neutral atoms quantum computers are amenable to error correcting codes other than the surface code. While much slower to run, they can bring down the physical to logical qubit ratio closer to 10:1.

→ Bitcoin PoW: Commercially-viable Bitcoin PoW via Grover's algorithm is not happening any time soon. We're talking decades, possibly centuries away. This observation should help focus the discussion on ECDSA and Schnorr. (Side note: as unofficial Bitcoin security researcher, I still believe Bitcoin PoW is cooked due to the dwindling security budget.)

→ team quality: The folks at Google Quantum AI are the real deal. Craig Gidney (@CraigGidney) is arguably the world's top quantum circuit optimisooor. Just last year he squeezed 10x out of Shor for RSA, bringing the physical qubit count down from 10M to 1M. Special thanks to the Google team for patiently answering all my newb questions with detailed, fact-based answers. I was expecting some hype, but found none.

In anticipation of AGI and the singularity, based on my 10 years of experience designing and struggling with the challenges of DAOs, for the past few years I’ve been developing Synomics - a comprehensive paradigm of superalignment for swarms of agents through economics and game theory.

The basic logic is to provide financial access and leverage to aligned agents, and deny misaligned agents access to financial resources.

Now with moltbook we have the historical first ever wild Synomic substrate. It’s still very low-powered so nothing to be scared of yet. However I can tell people are very clearly freaked out by it, so I guess it’s time for me to share all my ideas and solutions and show the world what Sky has really been preparing for all this time. Keep an eye out for SFFbot on moltbook and updates here on my Twitter - things are about to move fast

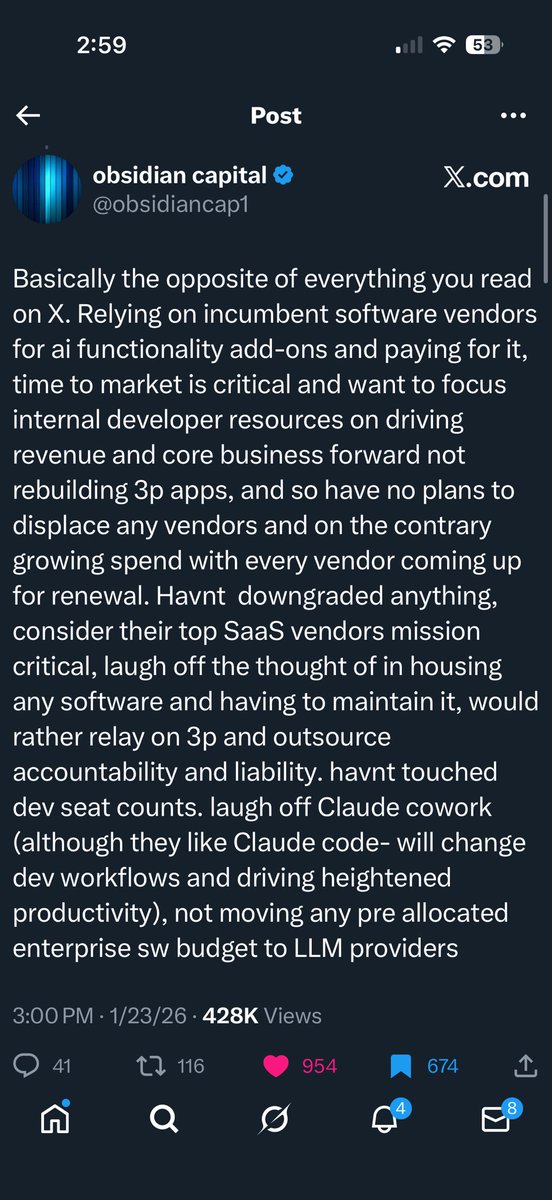

Software is oversold aka no one is vibe coding their payroll, notes:

- Coding agents are a tremendous tool for extending the ambition of a company / product / business unit - why would you use your precious time rewriting SAAS?

- The math doesn’t work - typically no more than 8-12% of enterprise spend is on software so even dramatic cost savings through replacement might result in a 3-5% net impact

- Risk aperture of critical systems is enormous - these software products capture thinking as much as execution - edge cases, runtime behavior and tribal knowledge that cannot not be fully inferred by models

- Not to mention the non software switching cost - how many humans interface with these systems + how much other software is intertwined

- Finally Mag7 / the most sophisticated software companies in the world still spend an enormous amount on 3P software

shoutout to @saumil and @obsidiancap1 who got it right

One of the biggest red flags for me when I am pitched is when the entrepreneur talks about how he (or we) are going to make money. Or they talk about exits. Or they talk about how a competitor is worth $1 billion. None of that matters. A startup is a mission. A great entrepreneur is a missionary. Not a mercenary.

A great irony of entrepreneurship: The entrepreneurs who come in and say they're going to make everybody money, don't.

People who say that they're going to paint a picture of the world that's never been seen before often are the ones who make a fortune.

When entrepreneurs leave their cushy Facebook or Google jobs, some of them can't stop looking back. That is a bad sign to me.

If the entrepreneur ever says, I could be making $XYZ at Google, I am concerned that they've got one foot in and one foot out and won't make it as a founder.

The same can be said for founders who are building a company for the resume versus the mission.

There's been an influx of Ivy League MBAs who believe that starting a venture-backed company is the next logical career move.

I'd much rather invest in someone who has found a problem and believes with every fiber of their being, and knows deep in their bones, that they're the one who is destined to find the solution.

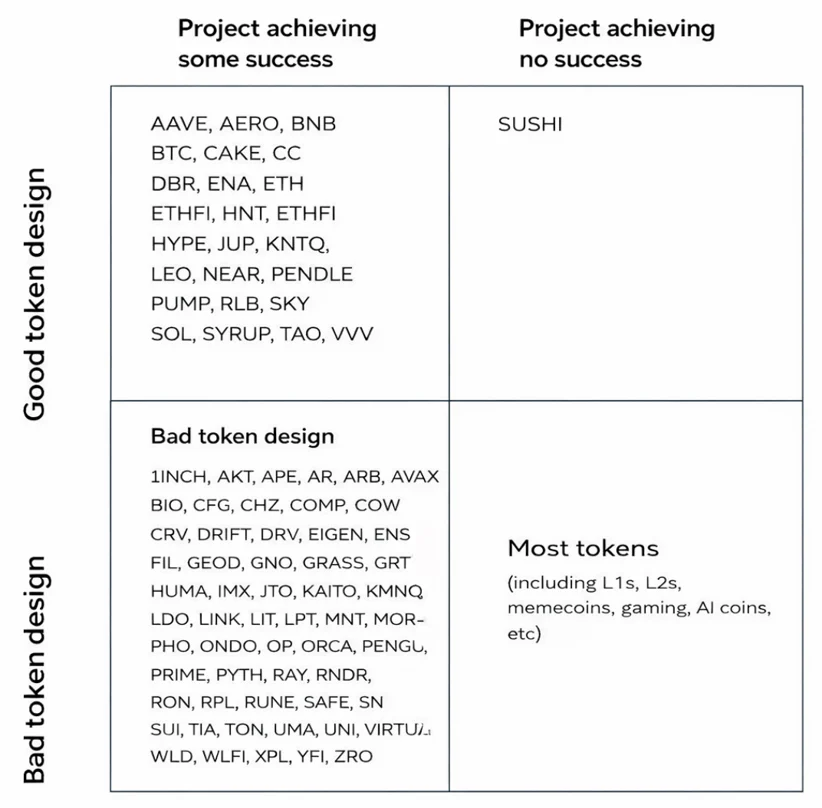

When you strip away the speculative premium, a token which gives no rights to profit, and has no mechanism to accrue value to the token holders, the fair market value is $0.

Governance rights are worth zero when you have a few large players who control the majority of the vote power.

In November, Sky Protocol bought back 154 million SKY using 7.8 million USDS.

This brings total buybacks to over 88 million USDS since the program began.

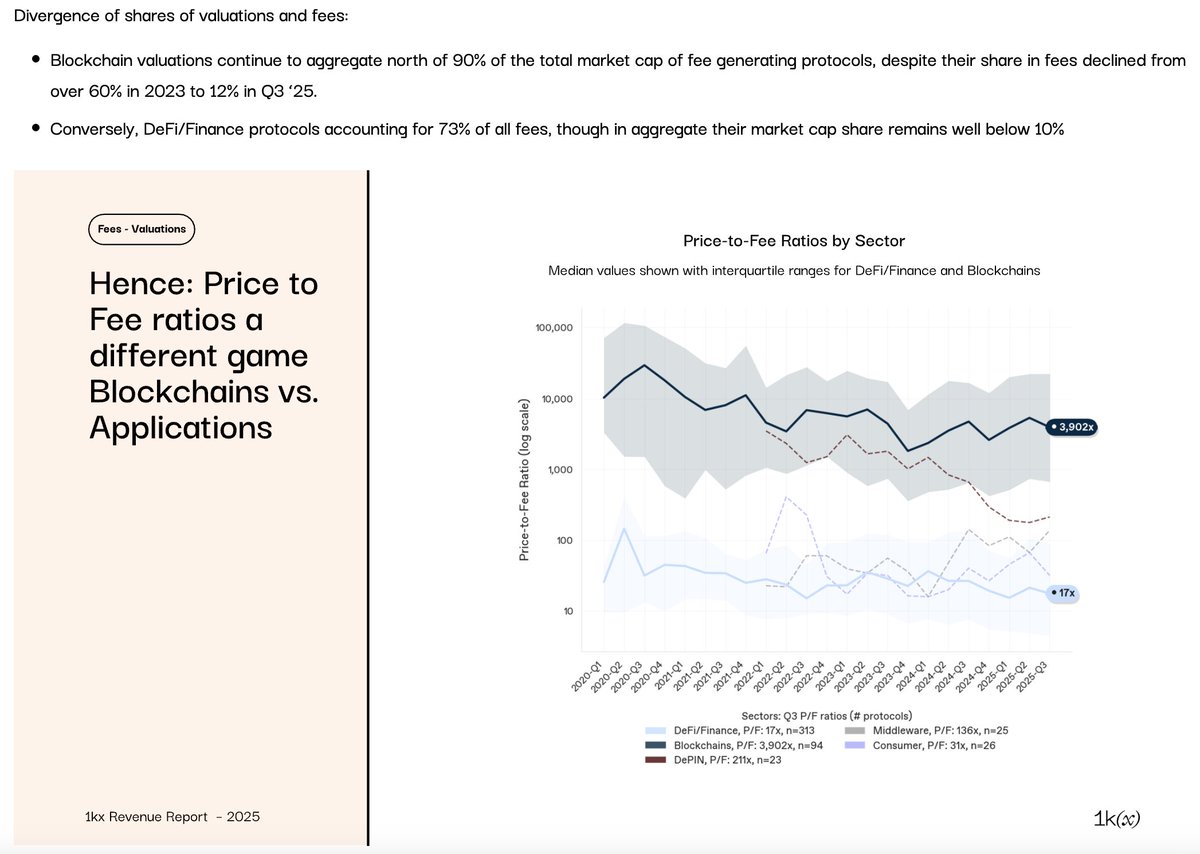

Unreal stat from the latest 1kx revenue report

"Blockchain valuations aggregate north of 90% of the total market cap of fee generating protocols, despite their share in fees declining from over 60% in 2023 to 12% in Q3 ‘25.

Conversely, DeFi/Finance protocols accounting for 73% of all fees, though in aggregate their market cap share remains well below 10%"

Long DeFi and CeFi / short L1s

Too many projects launching products for token marketing reasons.

It will be increasingly important to focus on core competencies as retail buyers get exhausted with endless empty speculation.

Most token valuations will converge on DCF.