Li Lu has three pieces of advice for value investors.

Imagine you inherited 100% of a business. You would want to learn everything about it, everything, all the ins and outs, better than the management running it. This is an Owner Mentality.

You want complete intellectual honesty. Don't lie to yourself about what you really know. Earn your opinion through hard work. Steelman the opposing arguments.

Study the history of great businesses and the people who built them. Expand your circle of competence. Look for patterns and lessons.

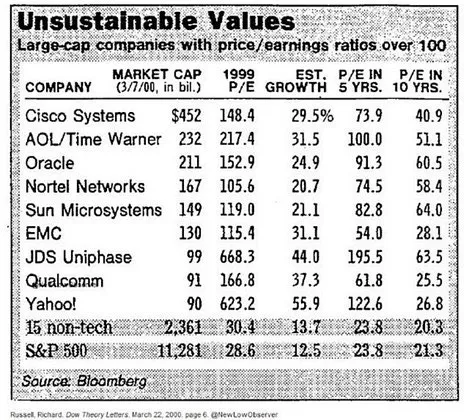

In 2009, Nick Sleep wrote a passage about Walmart that should permanently influence how you think about valuation.

He showed that an investor in 1972 could have paid over 150x the prevailing share price — a P/E above 1,500 — and still earned a 10% annual return through to the time he wrote the letter. Even buying ten years later at over 200x earnings would have delivered the same result.

𝐒𝐥𝐞𝐞𝐩 𝐭𝐡𝐞𝐧 𝐚𝐬𝐤𝐞𝐝 𝐭𝐡𝐞 𝐪𝐮𝐞𝐬𝐭𝐢𝐨𝐧 𝐭𝐡𝐚𝐭 𝐦𝐚𝐭𝐭𝐞𝐫𝐬 𝐦𝐨𝐬𝐭:

“𝐓𝐡𝐞 𝐦𝐚𝐫𝐤𝐞𝐭 𝐬𝐭𝐫𝐮𝐠𝐠𝐥𝐞𝐝 𝐭𝐨 𝐚𝐩𝐩𝐫𝐞𝐜𝐢𝐚𝐭𝐞 𝐭𝐡𝐞 𝐦𝐚𝐠𝐧𝐢𝐭𝐮𝐝𝐞 𝐚𝐧𝐝 𝐥𝐨𝐧𝐠𝐞𝐯𝐢𝐭𝐲 𝐨𝐟 𝐭𝐡𝐞 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬’ 𝐬𝐮𝐜𝐜𝐞𝐬𝐬. 𝐁𝐮𝐭 𝐰𝐡𝐲?”

___

𝐋𝐞𝐬𝐬𝐨𝐧 𝐎𝐧𝐞: 𝐈𝐭 𝐢𝐬 𝐛𝐞𝐭𝐭𝐞𝐫 𝐭𝐨 𝐛𝐞 𝐚𝐩𝐩𝐫𝐨𝐱𝐢𝐦𝐚𝐭𝐞𝐥𝐲 𝐫𝐢𝐠𝐡𝐭 𝐭𝐡𝐚𝐧 𝐩𝐫𝐞𝐜𝐢𝐬𝐞𝐥𝐲 𝐰𝐫𝐨𝐧𝐠 (John Maynard Keynes).

The investors who passed on Walmart because it looked “too expensive” were precisely wrong. The ones who paid up — even substantially — and focused on the 𝘲𝘶𝘢𝘭𝘪𝘵𝘺 𝘢𝘯𝘥 𝘭𝘰𝘯𝘨𝘦𝘷𝘪𝘵𝘺 of the business were approximately right.

When you own a truly exceptional business with decades of runway, whether you overpaid by 5% or 10% barely registers over a 10- or 20-year holding period.

The catastrophic mistake is not slightly overpaying for greatness. It is refusing greatness because the price wasn’t perfect — and deploying that capital into something mediocre instead.

𝐋𝐞𝐬𝐬𝐨𝐧 𝐓𝐰𝐨: 𝐅𝐨𝐜𝐮𝐬 𝐨𝐧 𝐭𝐡𝐞 𝐦𝐨𝐬𝐭 𝐢𝐦𝐩𝐚𝐜𝐭𝐟𝐮𝐥 𝐝𝐫𝐢𝐯𝐞𝐫𝐬, 𝐧𝐨𝐭 𝐣𝐮𝐬𝐭 𝐭𝐡𝐞 𝐬𝐮𝐫𝐟𝐚𝐜𝐞-𝐥𝐞𝐯𝐞𝐥 𝐝𝐚𝐭𝐚.

Sleep’s answer was clear. 𝘛𝘩𝘦 𝘤𝘦𝘯𝘵𝘳𝘢𝘭 𝘦𝘯𝘨𝘪𝘯𝘦 𝘰𝘧 𝘞𝘢𝘭𝘮𝘢𝘳𝘵’𝘴 𝘴𝘶𝘤𝘤𝘦𝘴𝘴 was a thrift orientation that fueled growth by consistently sharing savings with customers. The culture reinforced this behavior, creating a self-reinforcing loop. This was the deep, permanent reality of the business.

𝘠𝘦𝘵 𝘪𝘯𝘷𝘦𝘴𝘵𝘰𝘳𝘴 𝘱𝘭𝘢𝘤𝘦𝘥 𝘵𝘰𝘰 𝘮𝘶𝘤𝘩 𝘦𝘮𝘱𝘩𝘢𝘴𝘪𝘴 𝘰𝘯 𝘵𝘳𝘢𝘯𝘴𝘪𝘵𝘰𝘳𝘺 𝘧𝘢𝘤𝘵𝘰𝘳𝘴 — valuation heuristics, margin trends, and incremental growth rates — while underweighting the engine that actually mattered. These surface-level metrics are anecdotal and short-lived.

The deep reality of how a business truly compounds is what deserves the greatest weight in the minds of long-term investors.

𝐋𝐞𝐬𝐬𝐨𝐧 𝐓𝐡𝐫𝐞𝐞: 𝐓𝐡𝐞𝐬𝐞 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐦𝐨𝐝𝐞𝐥𝐬 𝐚𝐫𝐞 𝐞𝐱𝐭𝐫𝐞𝐦𝐞𝐥𝐲 𝐫𝐚𝐫𝐞 — 𝐚𝐧𝐝 𝐬𝐡𝐨𝐮𝐥𝐝 𝐧𝐨𝐭 𝐛𝐞 𝐭𝐚𝐤𝐞𝐧 𝐟𝐨𝐫 𝐠𝐫𝐚𝐧𝐭𝐞𝐝.

There are very few business models where growth begets growth in the way Walmart (or Amazon / Costco) has grown. In many companies, size eventually becomes a burden.

𝘉𝘶𝘵 𝘪𝘯 𝘴𝘰𝘮𝘦 𝘤𝘢𝘴𝘦𝘴, 𝘴𝘤𝘢𝘭𝘦 𝘵𝘶𝘳𝘯𝘴 𝘪𝘯𝘵𝘰 𝘢𝘯 𝘢𝘴𝘴𝘦𝘵. 𝘌𝘷𝘦𝘳𝘺 𝘪𝘯𝘤𝘳𝘦𝘮𝘦𝘯𝘵 𝘰𝘧 𝘨𝘳𝘰𝘸𝘵𝘩 𝘴𝘵𝘳𝘦𝘯𝘨𝘵𝘩𝘦𝘯𝘴 𝘵𝘩𝘦 𝘤𝘶𝘴𝘵𝘰𝘮𝘦𝘳 𝘱𝘳𝘰𝘱𝘰𝘴𝘪𝘵𝘪𝘰𝘯, 𝘸𝘩𝘪𝘤𝘩 𝘥𝘳𝘪𝘷𝘦𝘴 𝘮𝘰𝘳𝘦 𝘴𝘤𝘢𝘭𝘦, 𝘸𝘩𝘪𝘤𝘩 𝘴𝘵𝘳𝘦𝘯𝘨𝘵𝘩𝘦𝘯𝘴 𝘪𝘵 𝘧𝘶𝘳𝘵𝘩𝘦𝘳.

MercadoLibre is one of the clearest modern examples. Its five-pillar flywheel — marketplace, advertising, payments, logistics, and credit — reinforces itself daily. More buyers attract more sellers. More transactions generate better data. Better data improves credit decisions. Superior logistics deepens loyalty. A larger audience and decades of rich data makes advertising more valuable. This is scale economies shared in action with magnitude and longevity.

That engine is why MercadoLibre has grown revenue more than 30% year-over-year for 29 consecutive quarters. A business model where growth begets growth — a rate and valuable structure in investing.

___

$MELI $AMZN $WMT

*This post is not to say that valuation doesn’t matter at all. Severely overpaying can undo years of strong business performance. However, the greater mistake is placing 𝘵𝘰𝘰 𝘮𝘶𝘤𝘩 weight on near-term metrics and entry price while underweighting the quality and durability of the business itself. It’s important to see the forest, not just the trees.

Warren Buffett: "Edgar Lawrence Smith changed the world with ['Common Stocks As Long-Term Investments'] — and people have forgotten all about it now."

"Darwin said if you found evidence that was contrary to what you already believed, write it down in thirty minutes or your mind will just block it out. People have a great resistance to new evidence."

"We don't get rich on our dividends that we receive — although we are happy to receive them. We get rich [based] on the fact that the retained earnings are used to build new earning power [and] repurchase shares which increases your ownership in the company."

(CNBC || 2020)

ON THE ANTHROPIC - ALIBABA DISTILLATION QUESTION

Here's the latest, summarized from sources such as the BBC, the Straits Times, and the Library of Congress:

1. @DarioAmodei sent formal complaints to Tim Scott and Elizabeth Warren about the alleged distillation attacks. These two sit on the Senate Banking Committee, a committee that oversees sactions and export controls. Amodei's choice of recipients indicates he is looking to get Alibaba sanctioned or blocked from trading with the U.S. in some way.

2. Other U.S. Senators, Bill Hagerty and Andy Kim, are working on a bill to increase penalties on foreign firms found infringing U.S. intellectual property. Whatever you think of "distillation" (it is an industry standard practice within the U.S. and without), it will likely be classed as intellectual property theft under the new laws.

3. This situation is a risky one for Amodei himself. He has been repeatedly accused of giving foreign companies too much access to Anthropic's models, and has protested the accusations. Recently, he was flatly ordered to ban foreign nationals from using certain Anthropic models. Now he is complaining to the government about something that allegedly occurred because of his company's policies. Prior to all of this, Anthropic was put on a Pentagon blacklist because of safety guardrails built into Claude.

4. If Alibaba were sanctioned by the U.S. government, the severity of the situation would depend on the nature of the specific sanctions. Denials of access to U.S. infrastructure and freezing of assets in the U.S. wouldn't impact it much, as Alibaba does not have much of a physical presence in the United States. The "big gun" sanctions wise would be denying Alibaba the right to transact in U.S. dollars altogether. This would be serious if enacted--it would impact its relationships in Europe, Latin America and Southeast Asia--but this is the most extreme sanction the U.S. typically uses, last used when Russia invaded Ukraine. The odds of things going this far are relatively low.

5. Alibaba was recently classed a Chinese military company by the pentagon. The consequences of this in itself are minimal to companies that don't supply military hardware--Tencent got hit with this one years ago and its business wasn't affected. Alibaba is currently suing the Department of Defense over the "military company" designation.

@MohnishPabrai explains why he sold out of $MU (& SK Hynix).

Once Samsung tried to take more market share, it was no longer a rational oligopoly. Add to that the uncertainty of the China trade war banning Micron products at the time.

Buffett said Coke and Pepsi was a rational duopoly and both made money. But not in geographies where one tried to take more market share share by slashing prices.

https://t.co/yKkVOJKzVN

Alibaba is the world's largest global retail market by GMV.

It has 1.1 billion users.

Its AI business is rapidly spreading across Asia, Europe, Brazil, Mexico and Dubai.

It's working that AI into its core commerce offerings, giving it advantages its e-commerce competitors can't match.

Finally, were its AI business to cease growing, or lose to competitors, $BABA could pull the plug on the segment, leaving it with tens of billions of dollars in annual FCF to spend on buybacks at a depressed valuation.

Ignore the market noise, this is one of the strongest companies in the world.

Alibaba finally restarted buybacks.

On June 22, $BABA / $9988 repurchased 952,488 ordinary shares on the NYSE for ~$12.5M, at ~$105 per ADS equivalent.

George R.R. Martin tracked 8 viewpoint characters in the first book. By the fifth he was tracking 31. The reason book six never ships is hiding in that jump.

Every POV is a piece of state that has to stay consistent: where the character is, what they know, what day it is, who they've crossed paths with. 8 characters give you 28 possible pairings to keep straight. 31 give you 465. The bookkeeping doesn't grow in a line. It grows with the square of the cast.

He hit the wall in 2005. What became A Feast for Crows and A Dance with Dragons was one novel he had to split by geography, Westeros in one volume and Essos in the other, because he could no longer interleave the timelines into a single thread. That's sharding a story because the monolith stopped compiling.

Martin named the worst piece himself: the Meereenese knot. Several characters converging on one city, each arriving at a different time, each chapter depending on the order of the others. He worried at it for six years and finally cut it by adding a new viewpoint to cover the gaps. Untangling it only widened the surface he then had to resolve in the next book.

Now run the other side of the ledger. The show aired its ending in 2019, to a fan revolt. His net worth sits near $120M, with royalties and HBO money landing every year whether or not the book exists. Two spinoffs are filming right now and want his hours. Finishing carries one near-certain outcome: getting measured against a finale fans despised, on plot threads he's publicly said he can't untie. The wait since 2011 has already passed the 15 years it took to write the first five.

The sprawl of viewpoints is what made Westeros feel like a real place with no center. It's also the thing he now has to resolve by hand, at 77, for almost no money he doesn't already have. He calls the book the curse of his life. The curse was the architecture.

New Mauboussin paper.

It splits every stock price into the business you own today and the growth you're paying for, then asks how much of the price is just expectations.

Case studies: Nvidia, Microsoft, Amazon, JPMorgan Chase.

https://t.co/qHwe2WGqDs

Costco is one of the only companies in the world that will lower prices on an item if inflation goes down on that item.

The vast majority of companies will just keep prices the same and pocket the savings.