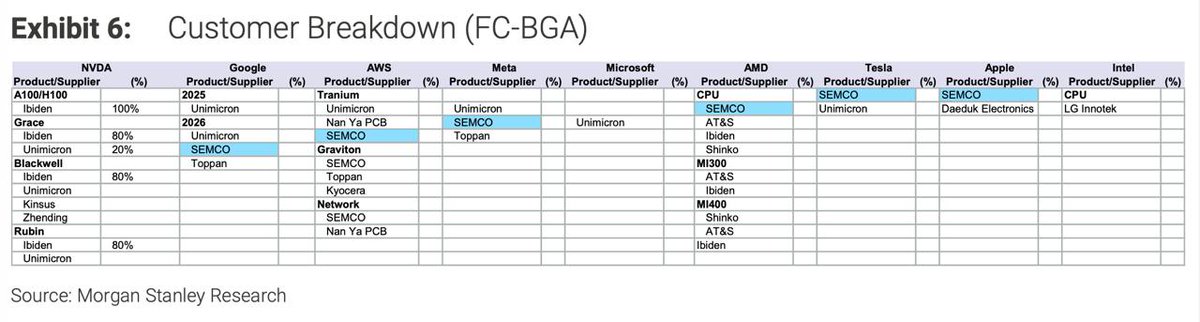

I think Samsung Electro-Mechanics is still undervalued.

A lot of people still see it as “just an MLCC company,” but in reality it supplies FC-BGA substrates to most ASIC players outside of NVIDIA.

I believe Samsung Electro-Mechanics will deliver explosive growth next year.

I think Samsung Electro-Mechanics is still undervalued.

A lot of people still see it as “just an MLCC company,” but in reality it supplies FC-BGA substrates to most ASIC players outside of NVIDIA.

I believe Samsung Electro-Mechanics will deliver explosive growth next year.

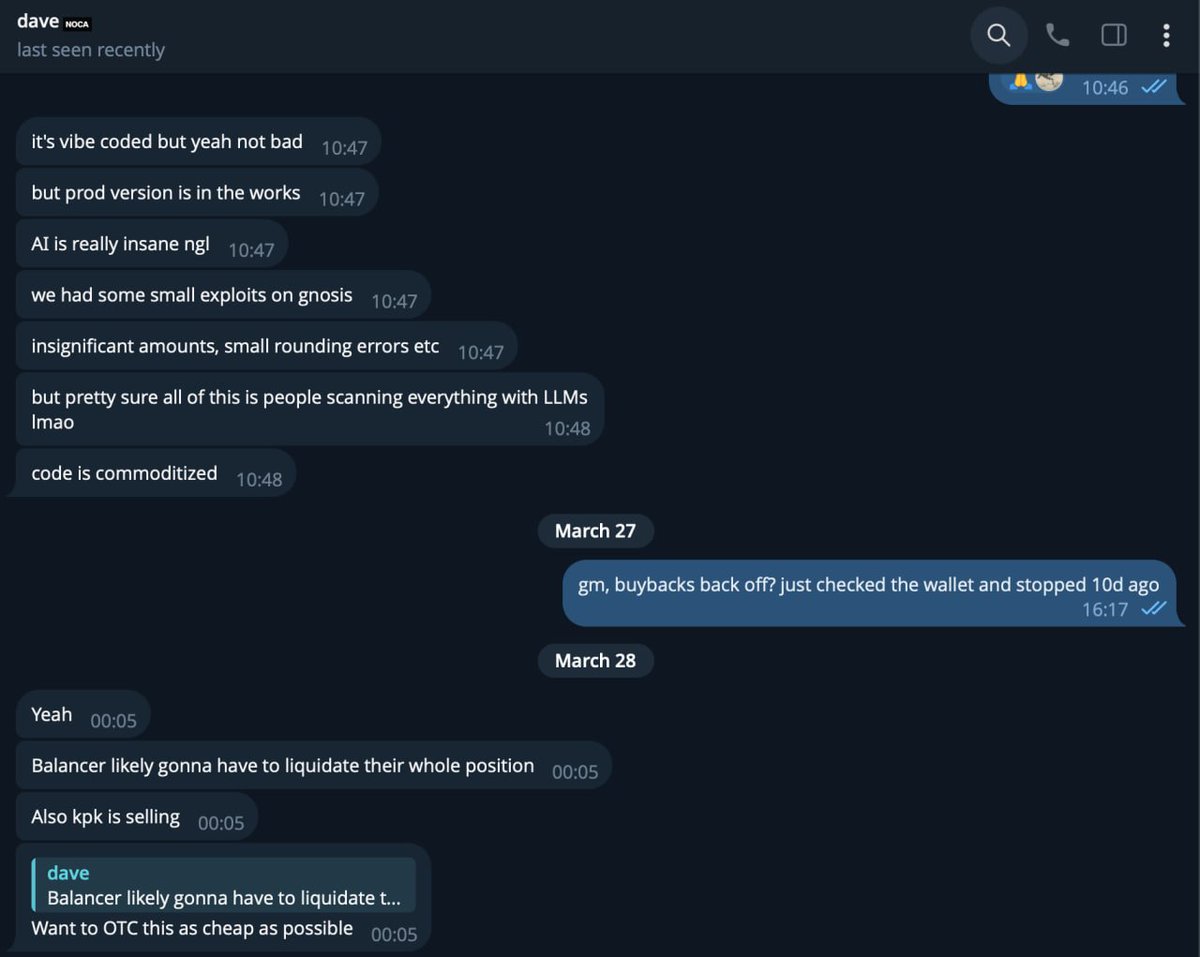

Re: airdrop farming

Back when Ansem had motion and wasn’t a useless “which coins bro” KOL, tailed him out of my predominantly ETH bag into SOL around $20-30 and actually was able to get decent size on WIF for 1000x. Should have sold when GCR bought the WIF nft but it is what it is

Given my port was demonized in sol, I basically played with every solana protocol and got mid 5/low 6 figure bags from each (Kamino, tensor, sanctum, etc). This was while doing nothing I wouldn’t already be doing (ie borrowing against my sol and using usdc to farm other protocols/earn yield, or leverage looping sol). Holding wif/popcat, I was getting airdropped 4/5 figures every other month for no reason whatsoever lol (twocat, maneko, etc)

I agree with the takes that airdrop farming as we’ve known it is largely dead. HyperEVM protocols are about as extractive as it gets in terms of their points programs. For @HypurrFi, @hyperbeat, and @pvp_dot_trade badge holders, it’s on sight if I see you mfers. I was hoping to run the same playbook back with just holding high % of my port in hype LSTS and reaping “free” airdrops (in the sense, I would borrow against/loop if no airdrops). But farming HyperEVM has been the most -EV thing if purely doing it to farm the protocol airdrops.

I do still think that @chameleon_jeff and co will do something to supercharge the evm at some point and that the evm tokens ($KNTQ, $HPL, $FELIX) will reprice massively at some point as well. Also excited to see what @izebel_eth and @papertrade_xyz bring to the evm. But airdrop farming is largely changed and the best way to play it is to simply use the protocols that you would use already and expect no rewards AND always trying out new things is always ++EV. I did this when I got my first big airdrop in 2023 with $ARB when I was max long eth into the merge in 2022 (triple halvening thesis LOL) by trading on GMX

Morpho is coming to @arc

Today: $2,500,000,000+ in USDC already earning yield on Morpho.

Soon: the open credit network will power the Economic OS built for the internet-native economy.

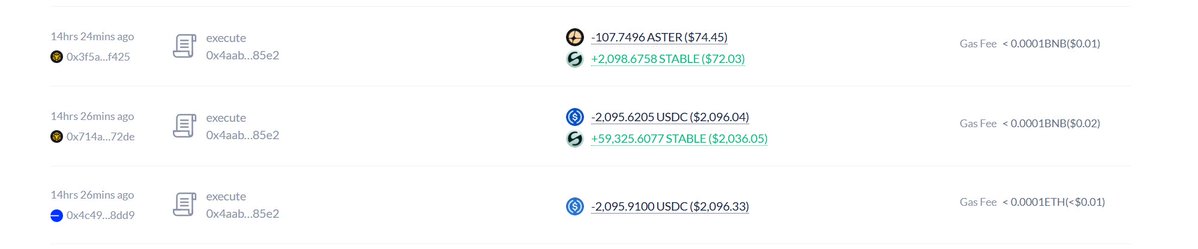

This wallet also bought stable on BNB Chain 14 hours ago, and coincidentally, if you look at the second screenshot,

upbit has been testing USDT, the gas token for the Stable chain, continuously since a month ago, and even tested it 19 hrs ago.

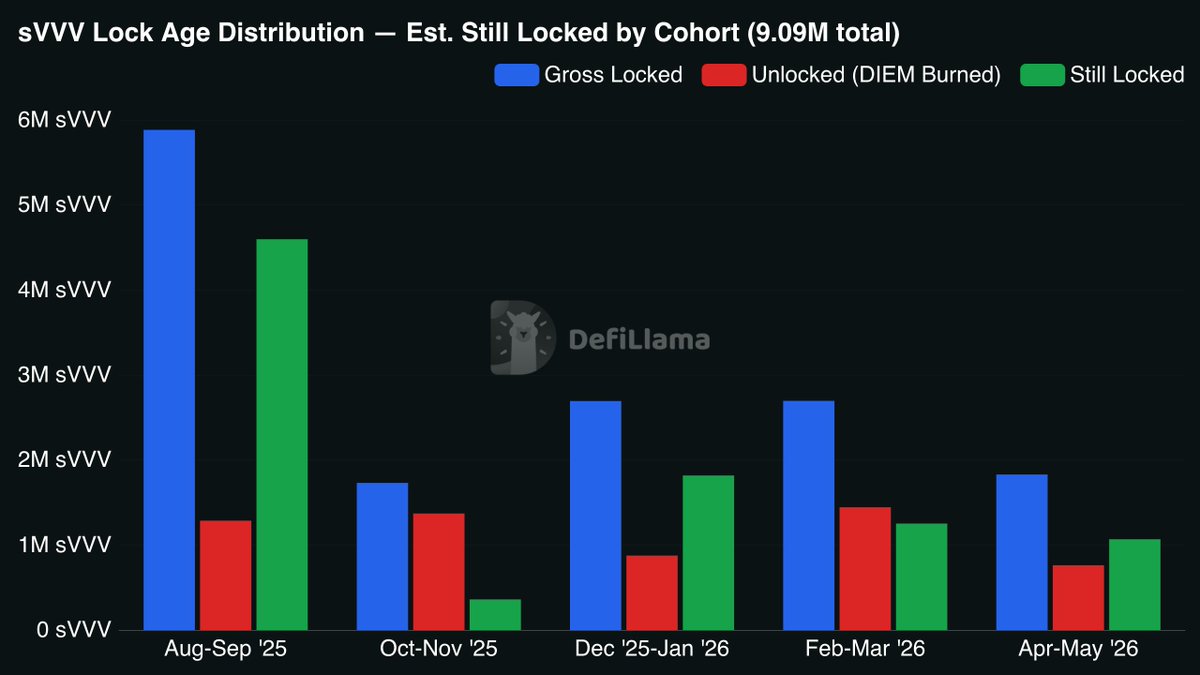

since $VVV is popping off, some helpful links:

- https://t.co/kTOctxeIeB (unstaking/staking analysis)

- https://t.co/yjt1kzI9MG very robust dashboard

- https://t.co/no9Rv9a6cF another dashboard

- https://t.co/pvj0wRlb0V some more $VVV / $DIEM stats

if you just bookmark and not like this post you dont deserve this pump ;)

and huge thanks to @0xMaki who shilled vvv/diem to me super early on :) luv you and much appreciated

must read paper on arbitrage between dex and cex!!!

so proud of @stabble_loewe for publishing in journal of banking and finance and so happy being a part of it from day 0

https://t.co/eQp6wzXCIz

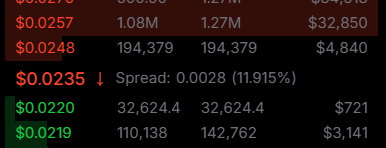

Hilarious:

Gnosis Ltd (the entity that took $30m/yr of DAO money and produced $400k of revenue for it) claims that there's some activist investors vying for a 'buyout at a premium', and how unfair this is to remaining GNO holders.

Let's fact check that a little...

We approached Gnosis Ltd saying that trading below NAV wasn't acceptable, need to close the discount. They agreed, and said they agreed with the NAV posted on their dashboard. Great.

Then they randomly changed the dashboard and added 250k GNO from nowhere, 20% of circulating supply, ($30m/yr funding proposal was made on the premise that equity like claims would be extinguished => Ltd held GNO isn't circulating for NAV)

Then they offered to OTC us out with a 7d TWAP. I know that they've been turning off buybacks unilaterally every time they agree one of these, so declined, and said that OTC at NAV was where we were at. (@Balancer@karpatkey did you know you both got rinsed on this btw?)

Then they come out talking about how we are greedy and want an OTC at a premium (nice framing, ignoring that you trade at a negative operational valuation and we just wanted NAV - i.e. $0 value for the ops), without the actual greedy reintroduction of 20% of supply for no reason.

Now, they are cutting their enormous 150 head count to a still ridiculous 110, for an entity making $400k/yr of ops revenue. They're planning to focus on 3 nepotism-driven products (Circles is the pet project of two of the three co-founders and is the absolute lowest PMF of any Gnosis product, for example). They are inviting a governance proposal to buy back to NAV (One already exists to pro-rata redeem any GNO that wants to exit at NAV), but also say that people pushing for GNO to trade at NAV are greedy (not the ppl extracting tens of millions for no return though!).

We aren't going to let these guys continue to drain GNO holders' cash. GNO will trade above NAV for the first time in years and Gnosis Ltd, who are unlikely to be a service provider of the DAO in 3 months, can go and look for a new gravy train. The current proposal, and any successive ones, must not be buybacks at the whim of people who have been shown to lie, pilfer, and dilute people on the other side of their incentives.

Our path forward sounds much fairer for GNO holders to finally trade >NAV than the status quo of having $30m taken every year for no return, and random introduction of supply to dilute the already dwindling NAV some more.

Lots of people are dunking on the Circle proposal to shift Aave rates, and I have, inevitably, been asked my opinion. I’ll share it here publicly.

Gordon’s proposal is not incorrect directionally. He correctly diagnoses that the market is not clearing, and provides a pretty standard solution that would fit into half the textbooks on my bookshelf.

Where I disagree with him are on his rate (in)sensitivity assumptions. Going straight to 40% seems destined to force liquidations. In the current market, contagion risk is already high, so cascades would need to be mitigated.

I don’t know if Aave can throttle the liquidation throughput like the old Maker vaults could, but that would be a way to do that. It’s an open question whether this would be a good idea. I’m open to considering it, but am not convinced at this time.

Gordon doesn’t say that the goal is repayment or liquidation, though. He believes this is a way to finance attracting supply, which I agree WOULD be the best way to unstick the market for the moment.

However, the rate can’t just be the usual mechanics. For starters, anyone who has been in DeFi knows that juicy rates get diluted quickly in a floating rate lending protocol. Given the high probability of at least some loss, why would a lender put their stables to work even for a temporary (maybe a week?) 40% rate?

Imagine you had $100m, and you saw this 40% deposit rate on Aave. Knowing there is more than $1b of impaired collateral in the system, are you going to risk your clients’ money for $109k/day? You’d need a week and a half just to break even on a 1% loss to your deposited funds.

Except this is a floating rate. Once danger has passed, the rates drop down. And if they stay elevated it’s likely because the situation hasn’t gotten better. The calculus COULD be different if it was 40% for 6 months or a year. But you’re really just getting outsized rates for a few days in the best case scenario, and it is rising or realized risk that would let you keep earning that rate.

This is at its heart a risk that is unmeasured, and so you can’t know what is the correct rate to price it at. You can’t tell if this is picking up nickels in front of a steam roller or the trade of the century.

So I think depositors are the most rate insensitive group at the moment, and due to a very wide range of possible outcomes at the intersection of distressed collateral assets, ultimate recovery rates on those assets, timeline to realize that recovery, secondary damage that has created bad debt, and governance risk around things like implementation of Umbrella or the funds seized by Arbitrum.

Basically everyone is standing around keeping rsETH marked to some imaginary number because we don’t have enough guidance from Kelp (and possibly L0 and now Arbitrum) for Aave to know how to begin liquidations and realize losses without accidentally taking on someone else’s loss because they were too pessimistic in valuing the impaired collateral.

I do think at this point, Aave would be better off making an “ok” plan and acting today than waiting for a “good” plan that requires information from Kelp/L0/Arbitrum/law enforcement that may not be available for some time.