Founders often talk about community strength.

But when asked to prove it, they fall back to:

- message count

- user count

None of which show real contribution.

That’s what DiScore is fixing.

Research: "The Compliance-Infrastructure Stack: How Web3 Neobanks Build Regulatory Moats and Infrastructure Dependencies"

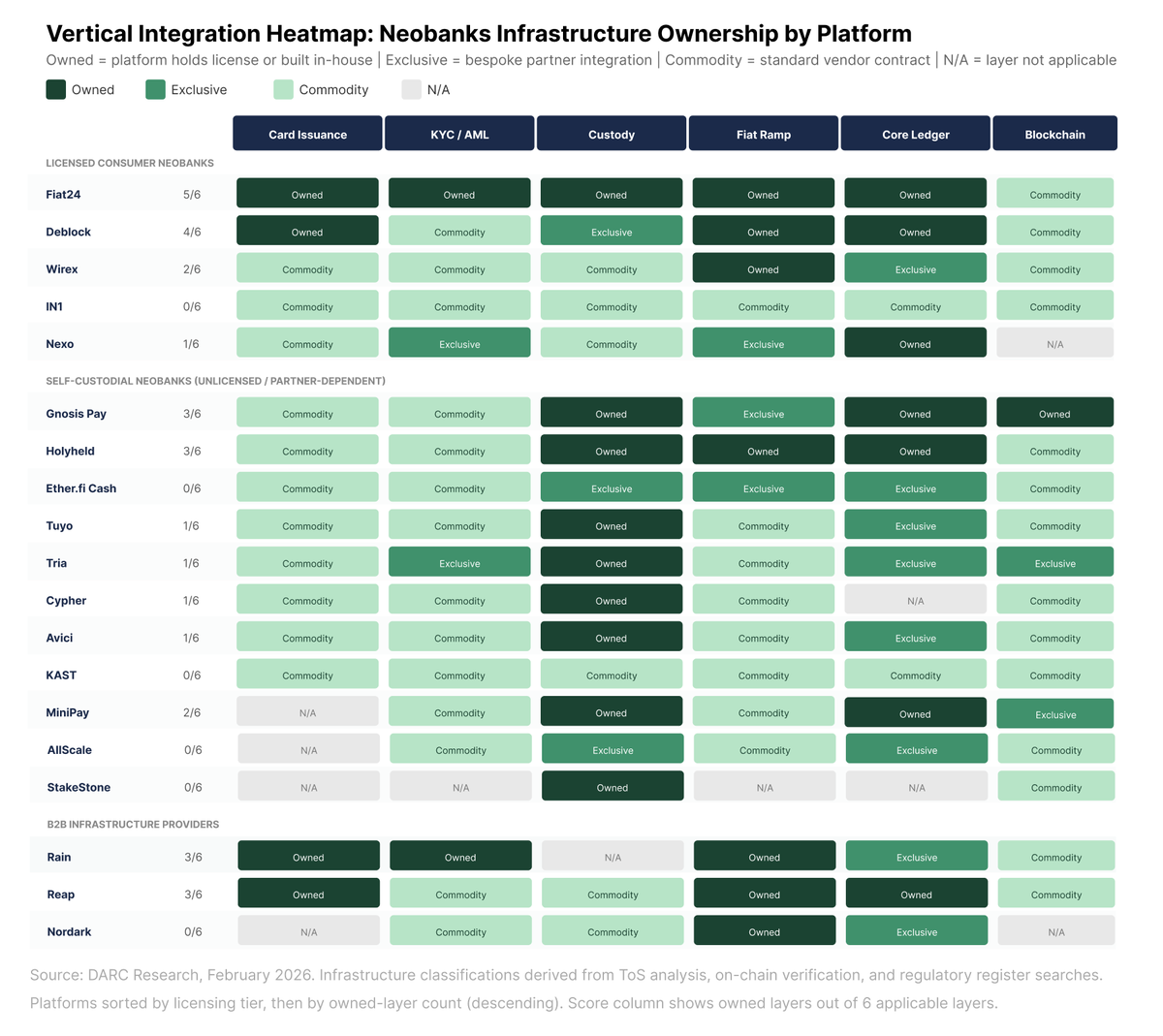

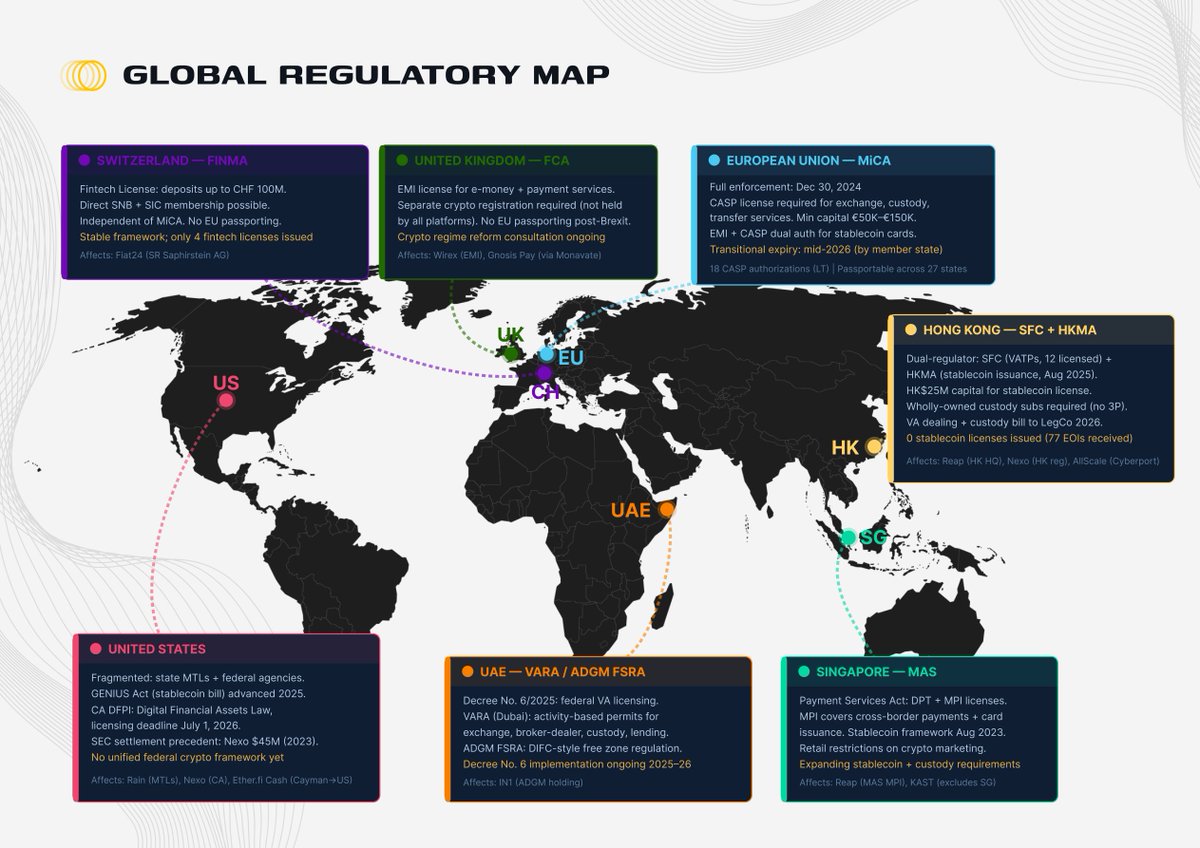

We mapped 19 Web3 neobanks across 6 infrastructure layers and 7 regulatory jurisdictions.

Key findings:

◈ 9 of 19 hold zero independent financial licenses - their regulatory standing depends entirely on upstream partners.

◈ 57% of card-issuing platforms depend on one of three EMI issuers.

◈ Infrastructure ownership separates defensible platforms from reseller: @Fiat24Official owns 5/6 layers. @DeblockApp_FR owns 4. @gnosispay and @holyheld own 3 each. Rain and Reap (operating as B2B infrastructure) also own 3.

◈ MiCA is the near-term pressure point: 14 of 19 platforms serve or plan to serve EEA customers, but only 2 (Deblock and @wirexapp) hold MiCA-relevant authorization as of February 2026. The remaining 12 must obtain CASP, partner with a licensed entity, or exit the EEA market by July 1, 2026.

Full report: https://t.co/nakMnavdpd

Contributors: @obchakevich_, @0xfrigg, @MlvsBznz, @rektonomist_@breyonchain, @Only1temmy, @belizardd@allscaleio