Long post but the TLDR is choose your reference points carefully.

I grew up comfortable in Kansas with a father who owned a small business pulling $40k a year. I felt rich until I went to Brown. Then I felt like the poor. There were students that had BMWs parked on different parts of campus so they wouldn't have to walk far to get access to a car.

I needed to make money to pay back my parents for college so I went to Wall Street. After Morgan Stanley, I worked for a single manager hedge fund managing $1.5Bn (alot of money back in the day) in SF that had just received an anchor investment from Yale University.

My boss was making more money than ever and was spending it. He would vacation with Lance Armstrong and Cindy Crawford. He became close with Wes Edens at Fortress. We made investments in Fortress portfolio companies. My boss took board seats on some of these investments. My boss spent alot of time frustrated he was not on the same level as Edens.

My boss was also close with Charles Schwab and we also invested in SCHW. Charles would let my boss and the firm stay at Stock Farm in Montana to host events for our LPs and management of some of our portfolio companies. It was the first time I ever flew private. I met Don Valentine of Sequoia who was an LP in our fund. We ran into Huey Lewis in the men's locker room before playing some golf. It was a world I never knew really existed growing up in Kansas.

We were also investors in Herbalife and would complain to the CEO at the time Michael Johnson (ex Disney) that he was massively overpaid and that the compensation structure of the company needed better alignment for shareholders (based on hitting key KPIs, etc). He would say he impressions mattered in his industry and living in LA was expensive.

When 2008-9 happened, our fund got decimated as we basically were a long only. Heavy exposure to Fortress names with massive leverage was no bueno. My boss had board seats which meant we were restricted. Yale pulled their entire investment. While the world was burning down, my boss in his fancy office in the Transamerica building told me that I was lucky "to not have any money to lose" while the world was burning down lol. I get what he was saying now as we saw clients that had amassed generational wealth in tech or owning boring businesses in Louisiana lose half of their net worth in 12 months. People were scared.

I would move back to NYC and end up working for 3 billionaires at different points during my career as a journeyman buysider. I did well enough at points to have direct contact with some of them. I saw the same dynamic - always someone doing better. Always frustrated. Not that happy.

I stayed in this world just trying to stay alive with some good years and years I got paid nothing when performance was poor. I was fine staying on this never ending hamster wheel until 1) I got married 2) we had a daughter 3) my dad's cancer diagnosis got more grim and I did more self reflection on what game of life I was playing.

Ultimately I left to buy a small business which has been hard. I still have friends on the buyside and in tech that struggle with comparison. But the reference points I was around constantly in my W2 are no longer loud. I wake up early and turn on machines. Most of my team members never graduated high school. My customers are mostly salt of the earth sales people working for small distributors sprinkled with some big publicly traded companies. $4 gas is a huge problem to everybody I interact with during my day - my customers complain daily about it in their daily lives. I sometimes lend money to my team members when they need help. I have to fix problems every day as the business isn't big enough to support hiring a general manager right now. But I'm home for dinner every night. This works better for me and my family.

My life is simple now => bring in business to make sure the 10 team members can feed their families. Last year when tariffs and a big customer shutting down hurt business badly for 3 months, my accountant told me to start firing employees as my competitors were either shutting down or firing 25-33% of their entire staffs. Entire shifts were shut down. I fired no one. It didn't feel right. I just stopped paying myself.

This year things have turned around. Team members are making 25-33% more due to overtime. I have more purpose now as my life is simplified as I'm just focused on making sure my team can eat, we make good product for our customers and the business can continue to pay down debt.

This is a hard path. I wouldn't recommend it for many, but it works better for me at this point in my life. My mental health has never been better. My wife reminds me how big of an asshole I used to be in finance as I was always stressed about my exposure / frustrated I wasn't doing better. What changed? My reference points changed. I no longer live in NYC. I live in this myopic world where I spend my weeks talking to team members, customers and vendors. 4am until 4pm is spent living in this world. 4pm-8pm is spent with my family before I go to bed ahead of a 330am wake up.

I have no doubt if I stayed in finance and was living in the Upper West Side in NYC, I'd still be playing my own version of "why aren't I doing better."

It took having a child and thinking more about my Dad's mortality (he passed this October from cancer) to re-evaluate things. I wish I had been brave/smart enough to consider a pivot earlier in life.

https://t.co/kenM7z2Feh

You used to sell stuff on eBay.

Maybe an old camera. Maybe Beanie Babies. Maybe a coat that didn't fit.

You paid a small fee. The buyer got the thing. Everyone went home.

That eBay is gone.

The website looks the same. The logo is the same. The 135 million buyers are still there.

But the company isn't really a marketplace anymore.

It is an advertising business with a marketplace attached for distribution.

Last year, sellers paid eBay $2 billion just to make sure their own listings showed up.

Read that again.

The board calls this growth.

A Canadian who runs a video game store called it something else.

Here is what actually happened.

In 2020 the board hired a new CEO. His name is Jamie Iannone. He arrived with a strategy called focused categories.

In plain English, that means leaning into the stuff people pay extra for. Sneakers. Watches. Trading cards. Auto parts.

The everyday seller, the person with the camera and the coat, was no longer the customer.

The customer was now the seller who would pay to be seen.

In 2025 eBay did $80 billion in transactions. They kept $11 billion of that as revenue. Of that $11 billion, $2 billion came from advertising.

Sellers paid them $2 billion to promote listings on a website those sellers already pay fees to use.

That is the growth story.

In the same year, the number of enthusiast buyers, eBay's own term for their best customers, was 16 million.

It was also 16 million the year before.

And the year before that.

And the year before that.

Four years. Zero growth. They mention this on every earnings call without mentioning it.

So what does a company do when growth stops?

It buys back its own stock.

In 2025, eBay returned over $3 billion to shareholders. Most of that was buybacks. In February the board authorized another $2 billion on top.

Buybacks shrink the share count. Earnings per share goes up even when earnings stay flat. The stock price follows.

The stock was $68 a year ago. It is $108 today.

The company did not improve. The denominator got smaller.

Then a man from Canada noticed.

His name is Ryan Cohen. He runs GameStop. He started his career selling pet food online and sold it to PetSmart for $3.35 billion.

He looked at eBay. 135 million buyers. $80 billion in transactions. Real margins. Real cash flow. A board harvesting the business instead of running it.

He bought 5% of the company through derivatives and stock.

Then on May 4, he offered to buy the rest. $125 per share. $56 billion total.

On May 12, the eBay board rejected the bid. They called it not credible.

The math is credible.

What the board means by not credible is we would have to explain why we sold.

Then Cohen went on Piers Morgan.

He said eBay is run by a bunch of losers with perverse financial incentives.

He pointed out that eBay's CEO has been paid $144 million over six years.

He pointed out that he personally takes no salary and has put $128 million of his own money into the company he runs.

You do not have to like Ryan Cohen to notice he is making a point that is hard to argue with.

eBay used to be a place where regular people sold things to other regular people.

Now it is a $48 billion company whose largest growth driver is charging its own sellers to advertise to a buyer base that stopped growing four years ago, while spending billions a year buying its own stock to make the chart go up.

The board calls this strategy.

A video game CEO from Canada called it what it is.

The market is now waiting to see who else agrees.

Plz fix. Thx.

Sent from my iPhone

Amazon $AMZN CEO Andy Jassy just said today on CNBC

“We believe that AI is the biggest technology transformation in our lifetimes”

“It’s going to reinvent every single customer experience we know and altogether new ones we never imagined”

“After the first three years of this incarnation of AI, our run rate is over $15 billion — 260 times what it was the first three years of AWS”

“When you have shifts that are this momentous … you want to bet big”

Strong Q1. AWS is growing at 28% YoY — our fastest growth in 15 quarters.

What stood out:

Kiro enterprise customer usage up nearly 10x QoQ.

Strands downloaded 25M+ times.

AgentCore can be used to deploy an agent as frequently as every 10 seconds.

Bedrock processed more tokens in Q1 than all prior years combined.

Customers aren’t experimenting with AI anymore. They’re running it — and building agents on @awscloud.

Microsoft sold every spare CPU it had to Anthropic and OpenAI. Amazon tripled its CPU buys year over year and still can't keep up. Two of AWS's biggest customers asked Andy Jassy if they could buy the entire 2026 production run of Graviton chips. He said no.

The ratio inside an AI datacenter used to be 100 megawatts of GPUs to 1 megawatt of CPUs. CPUs handled storage, checkpointing, pre-processing. Light work. GPUs did the actual training and inference.

Then OpenAI shipped o1-preview in September 2024. RL post-training went from "check the model output with a regex" to "run classifiers" to "compile the code and run the unit tests" to "spin up a sandbox, call three databases, run a physics simulation, verify the answer."

Every rollout now needs a CPU-backed environment to verify against.

Codex 5.4 runs agentically for 6-7 hours at a time. Each database call, each cron job, each scraped URL is CPU work. Coding agent revenue went from a couple billion to north of $10B in six months. That compute is sitting on CPUs.

The CPU to GPU ratio is now approaching 1:1. The entire global cloud was built for 1:8.

That's why GitHub has been unstable for weeks. Nvidia and Arm both announced they're entering the server CPU market in March. TSMC will only meet 80% of server CPU wafer demand this year. High-end server CPU prices are already up 50%.

When the GPU king and the IP licensor both pivot to CPUs in the same month, the boring chip isn't boring anymore.

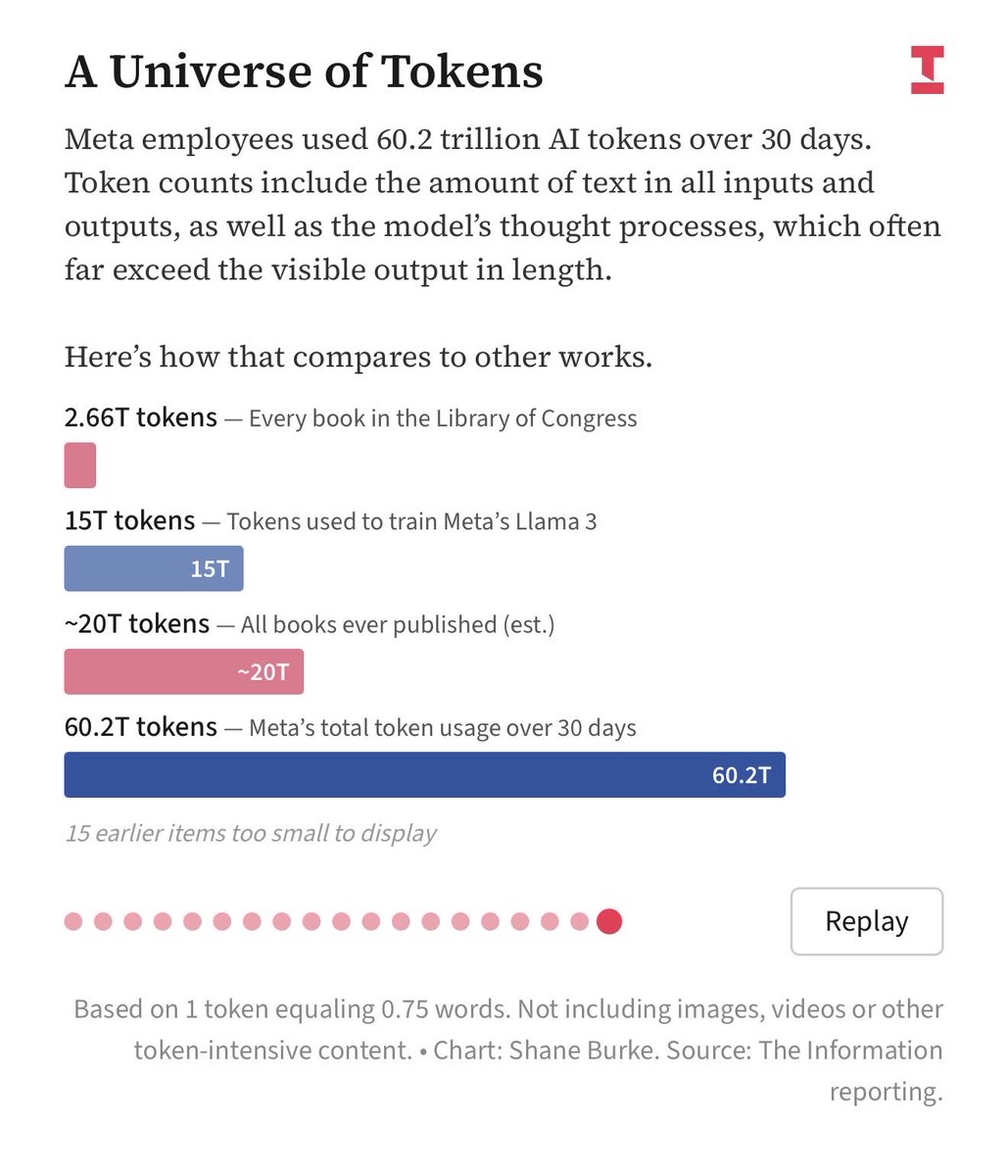

Meta is one third of Anthropic revenue?

60T tokens / mo = $900M / mo = $10B ARR for Anthropic 🤯?

This is also the largest enterprise contract in history.

MS software credit dashboard. All 4 charts telling the same story.

Highest leverage. Lowest interest coverage. Worst vintage concentration. $80B+ entering the refi window by late 2027.

One sector. Every possible red flag. Simultaneously.

NYC gave McKinsey a $4M contract to answer one question

Should trash go in a trash can

They studied it for 20 weeks

Looked at Paris

Looked at Amsterdam

Looked at Barcelona

Produced a 95-slide deck

Titled "The Future of Trash"

$42,000 per slide

The conclusion after 20 weeks and 95 slides

Yes

Trash should go in a bin

Not on the sidewalk

They called it "containerization"

Which is a $4 million word for "trash can"

The mayor then stood at a podium and unveiled a bin

A bin

With wheels

And a lid

Like the one in your garage right now

The one you bought at Home Depot for $50

He presented it like he had discovered gravity

Camera crews were there

Photographers

Press releases

For a bin

I run the finances of an entire company

If I handed my board a 95-slide deck that concluded "put the thing in the container" I would be fired by slide 2

My analyst could have done this in an afternoon

With one slide

That said "yes"

And I would have redlined it for being too long

But this is government

Where common sense costs $4,000,000

And comes with a PowerPoint

Make common sense common again

Plz fix. Thx.

Sent from my iPhone

Cursor internal analysis shows how hard Anthropic is subsidizing Claude Code.

Last year, a $200 monthly subscription could use $2,000 in compute. Now, the same $200 monthly plan can consume $5,000 in compute (2.5x increase).

More color from Well's Rocha re $AMZN

"The stock is getting sold aggressively in the post-mkt -10% as a result of a few key surprises: #1) FY26 Capex of $200B a step-function higher than even the highest whispers of $180B and even post sticker shock of GOOG yesterday, #2) 4Q EBIT light of consensus on an as reported basis ($24.98B vs $25.08B) vs expects for a clean beat, and #3) 1Q EBIT guide at the HE $21.5B as reported shy of the $23B expects and even still shy when adjusted for the $1B of Leo expenses that were called out and not in models into the print.

The unanimous buy side feedback in my convos is that the stock move lower is ridiculous. Buy side EPS seems to be shaking out around $9 / $11 for CY26 / CY27, and so maybe you can argue that they’re a touch lower post-print because of the combination of the surprise between the light EBIT flow-through and now much higher D&A flow-though. My sense is that folks are flat-out frustrated. Qualitative commentary about demand signals for AWS on the actual call hit every nail on the head and the stock did not budge. I could figuratively see people slamming their keyboards in frustration at that. Not even the RPO disclosure of $244B, accelerating growth 16pts from 22% to 38% on a 10pts easier comp, which implies Bookings of $79.5B, accelerating growth 81pts from 9% to 90% on a 56pt easier comp, could do the trick. Not even the fact that AWS Revs printed 24% YoY growth which hit the real buy side bar (not 23%) and matched the same net new dollars added sequentially in terms of incremental revs as what $GOOG reported yesterday which subsequently saw universal rejoicing from the Street.

In fact, I even had to do the debate between the optical 48% YoY GCP print vs 24% YoY AWS print and do the net new math breakdown; but nothing is working tonight. I mean, even NA Retail margins and AWS margins were fine in 4Q, as weakness was in International Retail which no one cares about.

None of that matters... All of this to me suggests that investors aren’t actually looking for revs growth or investment cycles or any of that, and instead are focused squarely on profitability. Again EBIT and EPS had hair. This is of course despite all of us being in the midst of a generational technology transition and AI investment cycle. Go figure. That last point is what doesn’t really make sense to me. And because it doesn’t make sense at all to me, I am not reading the -10% tick as fundamental.

There’s something else going on, perhaps the forced flows kind or something else. Even the regular fundamental read throughs from AWS strength and Capex exploding don’t make sense: $NVDA is down and $DDOG is also down, in particular. I’m all ears for incremental feedback."