Monthly VC/LP debrief.

What I actually saw in May 2026:

1/ SF is in full gold rush mode again, but history says the current winners won't stay on top forever. Every dominant technology eventually gets surpassed – newspapers, telecom, cable, Google in ads, IBM in computers. In AI the same pattern is already playing out: compute will hit walls, chips get dramatically more efficient, new energy sources emerge, and entirely new model architectures appear. The people feeling left behind today may just be early in a much longer cycle. (h/t @TurnerNovak)

2/ The largest $10B+ funds went from 140–150 collective early-stage deals per year in the SaaS era to 370–400 in the AI era. But the concentration is at the top of the market – top-decile rounds, known founders, proven operators. @kevinhartz calls it "option value": a small check today for the right to lead Series A tomorrow. The average seed round remains territory for EMs.

3/ We might be entering a Zombie VC era. ~85% of 2017–2018 vintage funds still haven't returned 1x DPI after 7–8 years. Median DPI sits at $0.34 on the dollar, while median IRR for the same cohort looks respectable at 11.6%. Paper returns hide the reality. The liquidity window opening over the next two years will be the moment of truth for most of these funds.

4/ @SpaceX IPO might be the single largest DPI event in VC history dropping into the lowest-distribution moment in venture capital history. @foundersfund alone, with an early $20M check in 2008, could return $60B+ (~3000x). When that capital hits LP accounts, it needs to be redeployed and that will circulate a new wave of fundraising for the same funds and fresh allocations from LPs who finally have liquidity to work with.

5/ The @cerebras IPO was the first real data point on crossover returns after two years of everyone writing off the model – both early-stage VCs and late-stage crossover funds made money on the same company, and LP conversations shifted from "do we have any exposure to the winners" to "how do we get into the next one." The same strategy that was declared dead in 2022-2023 got fully rehabilitated by a single exit. (h/t @MeghanKReynolds)

6/ Monte Carlo across 1,391 VC funds: concentrated portfolios (15 companies) and diversified ones (100 companies) produce the same average fund return – 2.44x. But compounded across multiple vintages, diversified wins: 2.25x vs. 1.78x. Concentrated funds carry more variance per fund, and variance drag compounds against you over time. The extreme outcomes (15x+) are almost exclusive to concentrated funds but the probability is tiny either way. (h/t Steve Kim)

7/ EM activity is showing the first real pulse in years. @cartainc logged 78 new US venture funds in the $10M–$100M range in Q1 2026 – a 34% jump from Q1 2025. Still well below the 2022 peak of 147, but the post-winter bottom might finally be in. The managers raising right now are doing it without a favorable macro, without easy LP recycling, and into a market where mega-funds are more active at seed than ever. (h/t @PeterJ_Walker)

8/ 76% of all EM-focused FoFs are American. The entire addressable market for a Fund I or Fund II isn't 132 FoFs – it's roughly 33. The other 100 exist, but Classic and Government-Led FoFs structurally can't anchor an early-stage vehicle: the check size doesn't justify the overhead, and a pension board can't be sold on a first-time manager without a track record. Geography and fund type filter out 75% of the market before the first meeting. (via @murphcapital)

9/ The 10-year fund is structurally mismatched with the assets mega-funds are holding. @SpaceX has been private for 18 years. @stripe for 15. For managers at that scale, @sequoia's move makes sense – open-ended, permanent capital, indefinite horizon. For small funds the logic runs the opposite way: the 10-year horizon enforced as a hard constraint, secondaries at Series C/D as the default exit, actual distributions on schedule. (h/t @credistick)

10/ There are only 3 positions that matter in a startup's cap table story: first investor, most helpful investor, biggest investor. Biggest is reserved for ~10 megafunds. First requires conviction most managers don't have – and LP preferences for concentrated portfolios often push against it structurally. So 90%+ of firms end up competing for "most helpful," which is why every pitch deck has a platform slide and every GP talks about their right to win oversubscribed rounds. (h/t @arian_ghashghai)

Every month I track new fund launches, LP events, market reports, and what's actually moving in VC/LP.

All of it in the @murphcapital newsletter: https://t.co/Wi8pAGQHLB

A lot of the best GPs I’ve backed gave me a strong gut feeling in the very first meeting.

Most of the work afterward was really about pressure testing that initial reaction. Of course there were times when the deeper work led me to pass, but I think people underestimate how often conviction forms early.

Benchmark's track record is their brand - twice producing the top-returning fund of its era with 156 characters on their website and zero LinkedIn presence.

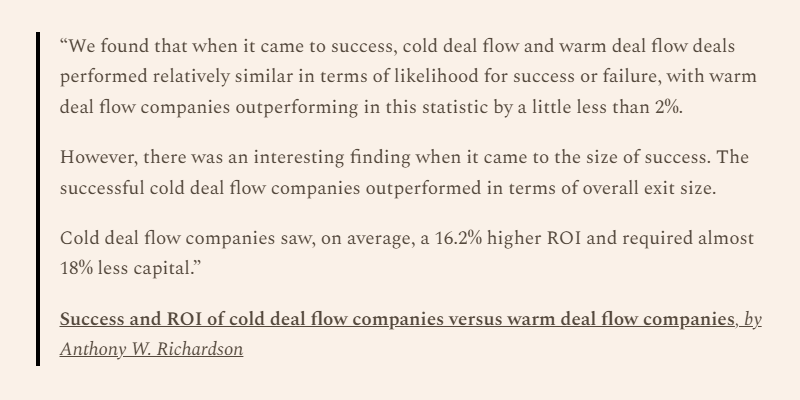

12 companies raised >$3B private, went public, and only one is beating the S&P - aggregate return of -117% is a rough number for anyone still defending the private premium.

There are 12 venture-backed companies that raised >$3B in private markets and then listed in the US.

Only one that has a positive return today, relative to the S&P 500's performance over the same period.

Most are deeply negative (aggregate -117%).

Only two that were positive at lockup expiry, neither stayed that way.

The high cost of private capital means the companies that raise the most, and stay private longer, are almost inevitably overvalued as insiders raise the price of funding events aggressively to stay NPV positive.

tangentially, imo the reason a lot of VCs like to talk about "the right to win" an allocation in a hot deal (and things of the like) is rooted in the following:

there are basically only 3 buckets of superlatives for VCs in the lifecycle of a startup that matter (and VCs try to sell themselves to LPs and founders as firmly being in 1 of these 3 buckets, as the rest is truly commoditized capital):

1) the first investor

2) the most helpful investor

3) the biggest investor

in practice, being someone's biggest investor is reserved for about 10 firms (i.e. megafunds), and most investors lack the conviction to be someone's first investor (imo there are also LP dynamics, e.g., preferring concentrated portfolios, that might push managers off this strategy).

so this leaves >90% of firms competing to be someone's "most helpful investor", which articulates some tangible right to win in oversubscribed rounds. this is not the only way to win in venture, however, the game most play

ICYMI: A comprehensive market map of 130+ FOFs from @pavelprata at @murphcapital that unpacks their DNA, mandates and LP networks - all bucketed into 4 distinct archetypes 👇

Keep an eye out for V2 with more fund investors coming soon.

Murph has an anchor partner. Welcoming @legiondotcc 🤝

Legion is building modern infrastructure for private markets – specifically for emerging fund managers and LPs.

Deal formation, fund admin, banking, liquidity – all on one platform. $300M+ in investor capital flows already on the platform. Backed by @vaneck_us and @BHDigitalAssets.

Legion is invite-only right now. They hand-pick a small founding cohort and build the platform shoulder-to-shoulder with the managers using it. Once the stack is proven, they open it wider.

We signed with them because they're serving the same people we write for. Expect proprietary data, benchmarks, and resources built specifically for emerging managers and LPs – coming through the Murph x Legion partnership. And of course… capital for emerging GPs!

Learn more: https://t.co/b8dDEOsBqz

If you're currently raising and want an intro, drop a comment below.

1/

After founding a gaming company and spending more than a decade in venture, one thing has become very clear to me:

I love early-stage investing.

Today, I’m excited to share that I’ve started @entropyVC.

Important context for anyone backing or building an emerging seed fund.

Mega-funds have structurally increased their early-stage volume, so “edge” needs to be much more specific than geography or stage.

Are mega-funds really taking over seed?

I decided to look at the behavior of the world's largest VC funds ($10B+ AUM) at early stages and answer a simple question: should EMs worry about their structural edge?

So I used @harmonic_ai and looked at all pre-seed, seed, and seed extension rounds across 3 eras:

- SaaS Era (2015–2019): 5 years of a normal market. Cloud, SaaS, fintech were the dominant theses.

- ZIRP Era (2020–2022): 3 years of zero interest rates and free capital.

- AI Era (2023–2026): from ChatGPT to the present day.

We focused on one core metric: average number of early-stage deals per year for each fund in each era.

Here are a few insights we found interesting:

1/ In the SaaS era, a typical mega-fund made 10–20 early-stage deals per year. This was moderate, targeted seed activity – a complement to the core Series A/B and later strategy.

2/ In the ZIRP era, everyone scaled up. Each of the 10 funds increased their early-stage deals/year (some by 2–3x), because capital was free, competition at later stages was fierce, and seed felt like a cheap entry point.

3/ Then came the AI era and it became clear this was no temporary effect. Even as rates rose and capital became more expensive with the end of ZIRP, @a16z and @generalcatalyst posted peak early-stage activity.

> @a16z: 16.6 → 48.7 → 75.3 deals/year. A 4x increase from the SaaS era.

> @generalcatalyst: 15.2 → 31.7 → 61.5 deals/year. Also 4x.

The most interesting finding, though, is 3 distinct behavioral models:

1/ "Accelerators" - deals/year in the AI era exceed ZIRP levels: @a16z (75.3/yr), @generalcatalyst (61.5/yr), @khoslaventures (31.5/yr). These funds didn't just stay active in seed after free money ended – they doubled down.

2/ "Stabilizers" – deals/year in the AI era are slightly below ZIRP peak, but well above SaaS-era levels: @sequoia (19.6 → 49.3 → 50.6), @Accel (15.2 → 43.3 → 34.7), @lightspeedvp (11.6 → 41.7 → 32.1). The ZIRP spike moderated, but activity levels remain sustainably 2–3x above the SaaS era. There's no return to the old normal.

3/ "Disciplined" – steady, gradual growth across all eras: @BessemerVP (9.4 → 23.0 → 20.9), @Lux_Capital (7.2 → 14.3 → 14.7), @IndexVentures (10.0 → 23.3 → 17.6). No ZIRP spikes, no AI explosions – but the baseline has durably shifted upward.

So in the SaaS era, these 10 funds collectively made roughly 140–150 early-stage deals per year. In the AI era – around 370–400. And I think they just set up a new, sustained baseline, not just doubled after a ZIRP-peak era.

For an LP evaluating an emerging seed manager, this is the most important context.

The early-stage market your GP is investing in is one where 10 funds with $10B+ in AUM are doing dozens deals a year.

An emerging manager needs to be able to articulate exactly where, in that market, they have the right to win.

Do you want to read a 30-page synthesis of research on why some companies use venture capital, and others are used by venture capital?

Also...

- Why capital efficiency is, for capital-intensive businesses, a more reliable predictor of long-run public-market performance than capital availability.

- Why hot-markets naturally focus on making companies absorb a maximum amount of capital, rather than creating the maximum value.

- Why Tesla and Rivian had such dramatically different IPO outcomes, and how that might reflect on upcoming listings for SpaceX and OpenAI.

Of course you do.

Robotics founders increasingly looking for a path to software-first margins - makes sense as a goal, but the defensibility usually lives in the hardware layer.

robotics is inherently about hardware, however I'm meeting more and more founders who want to find a software (or just non-hardware) business to build for robotics. thoughts:

> software is behind hardware (so this realization is correct, but not unique), and "robot brain" is indeed a hard problem to solve (further out than most think). that being said, I don't think solving robot intelligence as a company that is neither 1) collecting data (either by robot deployment, or other means) nor 2) a true research company like PI makes a lot of sense

> Selling dev tools to robotics companies is a horrible business idea right now (sounds smart, but not enough robot deployments + nowhere near the #1 pain point)

> the most obvious non-hardware opportunity is in the deployment gap. specifically, imo the demand for businesses in manual labor that want to try robotic solutions *today* I believe is much greater than most people realize, however no robot (humanoid to service bot) is ready to work out of the box (i.e. someone needs to come set them up, teleop, maintain etc). if I were thinking about a business, I would think about doing something that helps old-school, regular-ass businesses put robots into their space

tl;dr build stuff that actively puts more robots into the world

@PalmerLuckey on warm intros: the asymmetry between VC networks and founder access is one of those structural features of the market that's easy to criticize and hard to replace.

On one side, you have the VC, with a network.

On the other, the founder, without.

Just to get the attention of the VC, the founder must navigate a network of strangers to find someone who believes in their idea enough to agree to pass it on.

And then they hope the VC, hearing this idea from a second-hand source, also sees the potential.

Who does this nonsense work well for?

It works reasonably well for founders with "obvious" ideas that have some recognisable "pedigree", who are perhaps gifted with charisma.

However, none of these attributes are positively correlated with returns.

They are positively correlated with generating faster markups, so it also works well as a filter for the scaled venture platforms who sell allocation to LPs.

But, for most founders, it's a massive waste of time and a painful distraction to be forced to play this ridiculous ego-driven relationship game.

The first thing any new VC should pledge is to not waste founders' time, because it is infinitely more precious than any VC's time.

The arrogance of making founders jump through hoops for a chance at raising money is insane. Unless you believe your customers are LPs, rather than founders.

LP alignment shaping GP behavior more than strategy or thesis keeps coming up across conversations in the ecosystem and still doesn't get enough direct attention.

Talk with a lot of venture GPs and one thing is clear: LP alignment is shaping venture behavior more than people admit. More VCs would swing harder if their LPs were less risk averse. This game was never meant to be about consensus or career-risk minimization. Venture at its core is conviction, asymmetric bets, and disproportionate outcomes. LPs who back the bold get the bag.

The fund size question is genuinely hard to answer mid-raise - round sizes have moved, ownership math has changed, and the right answer depends on what you're actually trying to build.

Big question going around emerging managers these days - does my fund size still make sense?

Rounds got bigger. Which means leading = more $. And if leading entails follow-ons, that's another big slug of $.

Or you give on leading / ownership. But does that work in your model?

Scott Kupor's framing on sins of omission vs commission is one of the cleaner articulations of how VC decision-making should work in theory.

Whether it matches how decisions actually get made is a different conversation - @credistick and @arian_ghashghai get into it on Going Solo.

To quote @skupor: “Sins of omission are worse than sins of commission. It’s okay for a VC to invest in a company that ultimately fails, that’s par for the course in this business. What’s not okay is to fail to invest in a company that becomes the next Facebook.”

This becomes a real problem for small and emerging managers if their proposition to LPs is access to consensus-type opportunities.

They end up with a dilemma; to face scrutiny for overpaying, or even greater scrutiny for missing out on seemingly obvious winners. There's also real systematic risk in tying a fund to a particular category where the window of opportunity may close at any moment.

Deal-by-deal SPVs are one answer, but that approach amplifies venture capital's principal-agent conflicts as GPs pass most of the risk to their LPs.

In truth, it's probably just not a strategy that small and emerging managers should pursue. The scaled venture platforms, on the other hand, are relatively price-insensitive, and can pay up when required.

Enjoyed chatting to @arian_ghashghai of @EarthlingVC about this, and many other topics, in the recent episode of Going Solo. Links below.

A 2009 Palantir investor reflecting on 16 years of watching a company grow from obscurity into a defense tech standard-bearer before the category existed and before anyone called it conviction.

I invested in Palantir in 2009 and have watched them grow from a startup nobody had heard of into a company worth over $320b. Copying their playbook is probably the least Palantir thing you can do.

What Palantir did was craft a strategy around building and distributing their product that was very much a de novo, wholly original output of their unique first principles approach. If you're trying to build a truly revolutionary product, how you build it and how you distribute it is going to be something you have to discover. If you want to do something that's as great and disruptive as Palantir, the need to find your own methods is axiomatic.

Now, if you're coming at it from first principles, you might arrive at something that looks a lot like Palantir's model. And that's fine. Just because Palantir hired engineers doesn't mean you should not hire engineers. But don't do it just because Palantir did it, either.

The meta point here is that there's an important difference between local and global maxima. If you just want to raise money, you can parrot some playbook nonsense and get there a little faster than doing it the hard way. But if you want to build a generational company, get rid of the playbooks and follow first principles.

That said, there's plenty worth internalizing from Palantir, beginning with their inputs rather than their model. Extreme ambition is the starting point. From there, unconventional thinking, a very high bar on talent, a genuine willingness to tackle hard problems, and an important mission worth embracing are all high on the list. And missionary zeal and work ethic matter just as much. You can be ambitious and lazy at the same time, so you've got to have the work ethic to back it up.

When you do those things, you end up with novel outputs. That's exactly what Palantir did. And it’s the only thing worth copying from them.

The hierarchy of metrics a GP leads with is usually a good proxy for where they actually stand on DPI.

@johnfelix123 on Lead Edge's framing - worth the read.

When fund managers have good realized performance, they show net DPI.

If they don’t have good net DPI, they show net TVPI.

If they don’t have good net TVPI, they show gross MOIC.

If they don’t have good gross MOIC, they show SAFE-adjusted MOIC.

If they don’t have good SAFE-adjusted MOIC, they show net IRR.

If they don’t have good net IRR, they show gross IRR.

If they don’t have good gross IRR, they show a logo slide.

If they don't have a good logo slide, they show brand-name co-investors.

If they don’t have good co-investors, they show founder references.

If they don’t have good founder references, they show a venture partners slide.

If they don’t have a good venture partners, they show Twitter followers.

VC Fund of Funds: The Market

At @murphcapital we manually mapped 132 active Funds of Funds backing global VC managers to unpack how their mandates and LP networks really work.

Key takeaways from Part 1 of our research:

1/ The market is smaller than it looks. There are 132 active FoFs, but for a real emerging manager, the addressable market is roughly 33 funds – just 25% of the total.

2/ 76% of all EM-focused FoFs are American. Furthermore, 58% of the entire 132 FoF pool is based in the US. For a non-US manager, this is the first and most brutal hurdle, even if a fund’s mandate formally covers other markets on paper.

3/ China ranks second by FoF count, but it is an unaddressable market for Western GPs. Out of 22 funds, 12 are government-led and only 2 are EM-focused. Political mandates and strict geographic boundaries make this ecosystem closed by definition.

4/ European breakouts will trigger the flywheel. @ElevenLabs birthed @baobab_ventures. @CredoVentures closed an €86M fund on the back of that exit. This is precisely how the European market will evolve.

5/ AI is a structural catalyst. AI captured 88.8% of all VC deal value in Q1 2026. If this technology cycle spans 20 to 30 years, the market is only beginning to fragment – and this is where EM-focused FoFs hold a structural advantage.

Read the full deep dive on our Substack for more insights: https://t.co/oEUMAryai8

@PeterL4e returning full-time to a16z on infrastructure, at exactly the moment when the infra investment cycle is running as hard as it has in a decade.

I am thrilled to announce my return to a16z as a full-time General Partner. Having made a full recovery from cancer and navigated some of life’s most taxing personal hurdles, I am returning with a sharpened sense of purpose and a deep optimism for the future, both personally and professionally.

My time away reinforced that living to one's fullest capacity requires doing what you love with the people you trust. While I’ve continued to support my boards and founders, I’ve realized my greatest impact happens when I am 'all in.' I believe he current pace of innovation in infrastructure is unmatched, and I couldn't be happier to be back in the trenches with my colleagues and close friends on the a16z Infra team.