Startup discovery platform @harmonic_ai rebuilt Scout, their AI platform using Deep Agents and LangSmith.

Deep Agents: One frontier model + two tool sets (global company data and firm-specific context). Long-horizon execution and context window management handled out of the box.

LangSmith: Deployment and scaling, full conversation traces for debugging, and Engine to automatically surface failure patterns + suggest fixes.

Are mega-funds really taking over seed?

I decided to look at the behavior of the world's largest VC funds ($10B+ AUM) at early stages and answer a simple question: should EMs worry about their structural edge?

So I used @harmonic_ai and looked at all pre-seed, seed, and seed extension rounds across 3 eras:

- SaaS Era (2015–2019): 5 years of a normal market. Cloud, SaaS, fintech were the dominant theses.

- ZIRP Era (2020–2022): 3 years of zero interest rates and free capital.

- AI Era (2023–2026): from ChatGPT to the present day.

We focused on one core metric: average number of early-stage deals per year for each fund in each era.

Here are a few insights we found interesting:

1/ In the SaaS era, a typical mega-fund made 10–20 early-stage deals per year. This was moderate, targeted seed activity – a complement to the core Series A/B and later strategy.

2/ In the ZIRP era, everyone scaled up. Each of the 10 funds increased their early-stage deals/year (some by 2–3x), because capital was free, competition at later stages was fierce, and seed felt like a cheap entry point.

3/ Then came the AI era and it became clear this was no temporary effect. Even as rates rose and capital became more expensive with the end of ZIRP, @a16z and @generalcatalyst posted peak early-stage activity.

> @a16z: 16.6 → 48.7 → 75.3 deals/year. A 4x increase from the SaaS era.

> @generalcatalyst: 15.2 → 31.7 → 61.5 deals/year. Also 4x.

The most interesting finding, though, is 3 distinct behavioral models:

1/ "Accelerators" - deals/year in the AI era exceed ZIRP levels: @a16z (75.3/yr), @generalcatalyst (61.5/yr), @khoslaventures (31.5/yr). These funds didn't just stay active in seed after free money ended – they doubled down.

2/ "Stabilizers" – deals/year in the AI era are slightly below ZIRP peak, but well above SaaS-era levels: @sequoia (19.6 → 49.3 → 50.6), @Accel (15.2 → 43.3 → 34.7), @lightspeedvp (11.6 → 41.7 → 32.1). The ZIRP spike moderated, but activity levels remain sustainably 2–3x above the SaaS era. There's no return to the old normal.

3/ "Disciplined" – steady, gradual growth across all eras: @BessemerVP (9.4 → 23.0 → 20.9), @Lux_Capital (7.2 → 14.3 → 14.7), @IndexVentures (10.0 → 23.3 → 17.6). No ZIRP spikes, no AI explosions – but the baseline has durably shifted upward.

So in the SaaS era, these 10 funds collectively made roughly 140–150 early-stage deals per year. In the AI era – around 370–400. And I think they just set up a new, sustained baseline, not just doubled after a ZIRP-peak era.

For an LP evaluating an emerging seed manager, this is the most important context.

The early-stage market your GP is investing in is one where 10 funds with $10B+ in AUM are doing dozens deals a year.

An emerging manager needs to be able to articulate exactly where, in that market, they have the right to win.

Which Seed investors had the best April?

I used @harmonic_ai to look at every company in the US and Europe that raised a Series A, B, or C and ask a simple question: who seeded them?

In April 2026, I identified 111 companies across the US and Europe that announced a Series A, B, or C round and had at least one prior seed or pre-seed round on record. Then I traced every institutional investor (VC funds, angel groups, venture studios) that participated in those seed rounds.

Each seed-to-upround conversion is scored using three factors – all derived from the April round itself:

1/ Stage Weight:

- Series C = 3x

- Series B = 2x

- Series A = 1x

Later-stage conversions are harder to reach and signal stronger company trajectories.

2/ Round Size Weight:

Rather than using fixed dollar thresholds, we calibrate against the month’s actual distribution. A $100M Series A is exceptional, a $100M Series C is slightly above average. The scoring reflects that:

- Top 10% for its stage = 3x (A ≥ $60M, B ≥ $110M, C ≥ $193M)

- Top 25% = 2x (A ≥ $30M, B ≥ $65M, C ≥ $106M)

- Above median = 1.5x (A ≥ $17M, B ≥ $45M, C ≥ $80M)

- Below median = 1x

These thresholds recalibrate every month from the actual round data – so the scoring stays relevant as the market shifts.

3/ Lead Bonus:

If the fund led the original seed round, the score gets a 1.5x multiplier. Leading a seed requires pricing discipline and conviction – worth rewarding when that bet pays off.

The composite score is Stage × Size × Lead Bonus, stacked across all hits in the month. Tier-1 mega-platforms (aka money banks) are excluded.

The top 5 funds in April, by conversion score:

- @Liquid2V

- @4biocapital

- @airstreet

- @PointNineCap

- @BoostVC

Again, this is not a fund ranking. I don’t have AUM data for most funds, and I don’t know which fund vehicle made the investment.

What I do have is a monthly conversion signal – a real-time view of which seed investors are seeing their portfolio companies break through to significant later-stage rounds.

Over time, the signal compounds. A fund that appears once could be lucky. A fund that shows up three months in a row with multiple hits is telling you something about the quality of their picking.

And we're going to track this every month at @murphcapital.

Scout 2.0 is live. Most of our users made it their daily driver before we even finished building it.

An analyst that doesn't sleep, knows every startup, every founder, every round, your entire network, and soon everything your firm knows too 👀

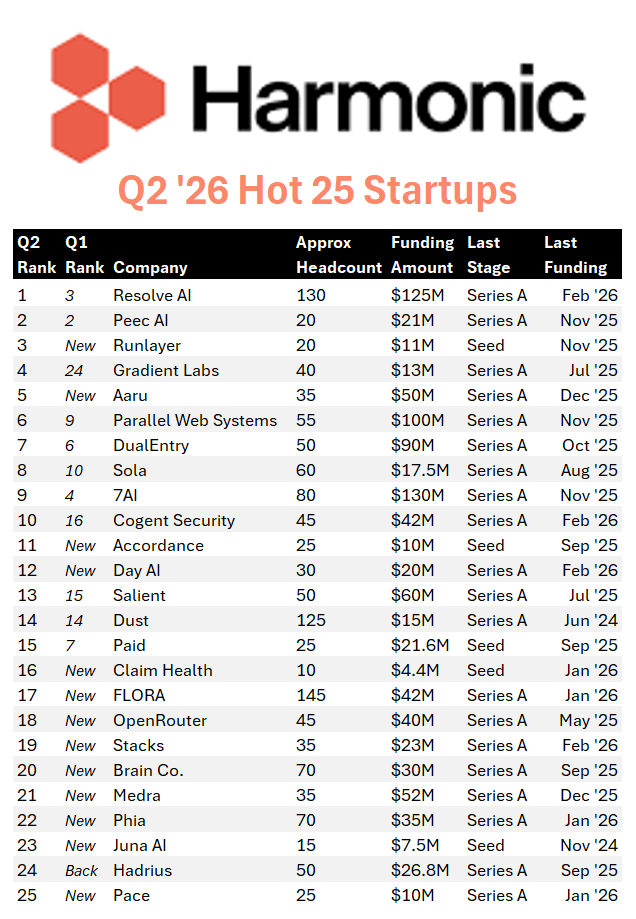

So @harmonic_ai just released their Hot 25 Report on the most in-demand early-stage companies.

The top 3:

🥇Resolve AI moves 2 spots from bronze to gold.

🥈Peec AI holds steady at #2.

🥉Runlayer joins in at #3 as the only new entrant in the top 3.

Biggest riser on the list: Gradient Labs - climbing 20 SPOTS to #4.

Keep an eye out for companies likely to raise soon: Sola at #8, Salient at #13, and Dust at #14.

Find the full report here: https://t.co/lXIWBbV3ug

Harmonic just dropped its Q2 '26 Hot 25 list, featuring the early stage companies seeing the most investor interest on @Harmonic_AI's platform.

My biggest takeaways:

Almost zero competition between these products. Every quarter, this list has multiple clusters of startups all sort of doing the same thing. This quarter you can argue that all of these products operate in completely different spaces / industries / core ICP.

11 of 25 were on Q1's list. This is the highest I've ever seen carry over between quarters.

23 of the top 25 have raised in the past year. On the same thread as above, investors love concentrating into the winners.

Very strong technical teams. If you look at the founders backgrounds (link in next post), there's a strong bias towards very technical founding teams.

Join us and our friends @vercel for a NYC co-working cafe on Feb 4th.

Complimentary Vercel credits, access to the complete startup database and free coffee.

https://t.co/OlvuyRDoMh

We're thrilled to be featured on the @harmonic_ai Hot 25 Startups list for Q1 2026, alongside an exciting class of emerging AI businesses.

https://t.co/0xaioIRm7X

So @harmonic_ai just released their Hot 25 Report on the most in-demand early-stage companies.

Biggest Story… 24 New Entrants compared to 11 last report.

@lovable remains at #1

@peec_ai enters at #3

Payflows in at #5

What do all these 3 have in common…? They’re all 20VC portfolio companies!

@retellai jumps straight to #2 with $10M ARR with just 20 people… NUTS!

@higgsfield_ai, one of the fastest-growing AI video creation companies is in at #14

Keep an eye on Capital OS, Payflows, @credal_ai and @AnteriorAI who haven’t raised in over a year… next rounds on the way?

Companies on previous lists who’ve all gone on raised Series B rounds including @tryprofound, @langchain, @get_tabs, @normativeai & @meetgranola

Find the full report here: https://t.co/p5UcVwR2LW

Harmonic has added 6 new, high-signal stealth launches since August.

Including AIDA, founded by ex-Co-founder/Head of AI at Glean.

Subscribe to these updates for free, no strings attached: https://t.co/XVKLwPK4Ha

The Harmonic Hot 25 Q4 is out!

Check out the 25 early-stage companies receiving the most interest on the platform used by thousands of venture investors every day.

https://t.co/8sAnIrrNP8

Join LangChain CEO Harrison Chase and @harmonic_ai CEO Max Ruderman in NYC as they explore ambient agents and "Above the Line" approaches—moving past manual processes to systems that understand intent and orchestrate intelligent outcomes.

RSVP: https://t.co/LNPTC8S4vo