📣Sharing an update: OpenLP is moving to LGT Capital Partners!

OpenLP founders @Beezer232, @LauraLPThompson & @natewcl, along with other @SapphirePrtnrs fund investing team members Dan Clayton, Vittorio Reynoso-Avila & Anna Jacoby, will be joining LGT on April 15!

OpenLP will continue under LGT, and you will still receive the OpenLP newsletter, as well as new episodes of the Origins Pod alongside co-host @nchirls.

Stay tuned for more updates from LGT and OpenLP coming soon!

Read more about the news here: https://t.co/bM3QIe74kj

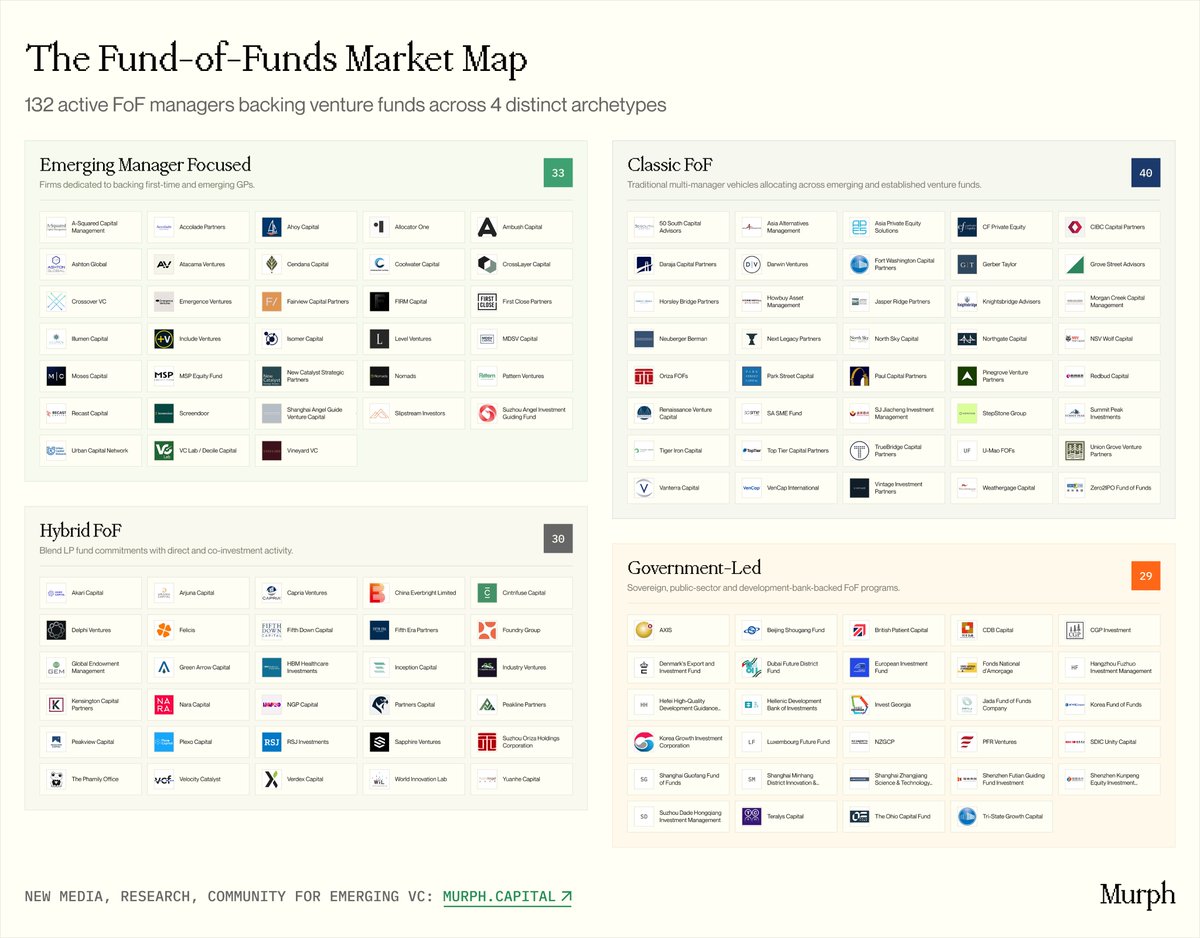

ICYMI: A comprehensive market map of 130+ FOFs from @pavelprata at @murphcapital that unpacks their DNA, mandates and LP networks - all bucketed into 4 distinct archetypes 👇

Keep an eye out for V2 with more fund investors coming soon.

What actually triggers a first close for an emerging VC manager? Spoiler: A strong Fund of Funds (FoF) anchor.

Me and @sharanjhangiani spent weeks analyzing 130+ Fund of Funds backing VC managers globally.

We mapped their geo concentration, how they evolved, and who the LPs behind them actually are.

Part 1 is out. Link in comments.

🚨 Just 3 IPOs could determine the future of VC.

According to @PitchBook, North American VC AUM could reach $2T by 2030. A key variable: anticipated IPOs from @SpaceX, @OpenAI & @AnthropicAI.

3 companies that could raise as much as all US VC-backed IPOs over the past decade combined. A liquidity event this massive could restore LP confidence and restart the flow of capital back into venture.

📊 Read the report:

https://t.co/49d8ptf0Nx

1/ Venture investing is often framed as a strategy game, but it’s just as much an exercise in emotional calibration. And who you have behind you matters.

@nchirls & I unpack a new framing “cynical optimism” in the new Origins minisode.

My🔑Takeaway 👇

https://t.co/LYvn0XMlUp

🧵Is “cynical optimism” replacing Silicon Valley’s long-celebrated culture of unbridled optimism in venture? And if so... what happens to pragmatism?

@Nchirls & @beezer232 unpack a new concept from their convo w Nicholas Csicsko (LP, Trinity Church)👇

https://t.co/TWRv9whDKl

3/

📌 How the old SaaS playbook (1M → 4M → 10M ARR) may no longer be venture-fundable

📌 What it means when companies can reportedly add ~$100M ARR in a month

📌 Why some companies risk becoming obsolete before they ever reach liquidity

📌 Exit windows, secondaries, and the uncomfortable reality that “companies are bought, not sold”

Big question going around emerging managers these days - does my fund size still make sense?

Rounds got bigger. Which means leading = more $. And if leading entails follow-ons, that's another big slug of $.

Or you give on leading / ownership. But does that work in your model?

“Outlier returns come from outlier people.” The best EMs often don’t look obvious on paper - exactly why many LPs miss them.

For LPs investing in EMs, there is no shortcut to success & much greater expected volatility. As with VC, those that embrace risk often reap the greatest reward.

Great piece by @credistick on harnessing conviction in both EMs and early-stage venture. 👇

Consensus is comfortable, but comfort rarely generates alpha.

The most common bias amongst LPs is to believe that former founders have a particular edge, having experienced entrepreneurship first-hand.

This is what could be called the “player-coach fallacy”, where it is assumed that the best coaches would be former professional players. It turns out they are quite different skill-sets.

There’s a specific study on how this relates to venture capital, based on analysis of 13,000 firms. Overall, former founders produced a lower rate of success than professional investors.

While successful founders outperformed, it’s worth recognising that that group is likely to outperform at most activities they attempt.

🧵What happens when one of 🇺🇸's oldest institutions starts asking whether VC has too much money?

On the latest Origins, Nicholas Csicsko (MD of Investments,Trinity Church Wall Street), joined @beezer232 & @Nchirls to talk liquidity & the disconnect btwn public & private mkts👇

4/ A few of key takeaways:

🔹Excess capital may be eroding venture’s illiquidity premium

🔹“Everyone wants DPI” = nobody trusts the marks

🔹More partners + more AUM isn’t always a better VC model

🔹Venture could actually get very attractive again soon... what will it take?

2/ In this minisode, Beezer & Nick break down David’s data confirming VC consolidation, debate what comes next & dive into Beezer’s latest piece: “I See Dead VCs.”

00:33 Top Takeaways from David’s episode

02:01 Venture Contraction Data

04:17 Fund Survival Math

05:47 Seed Ecosystem Risk

07:35 What Gets You to Fund II

08:48 Building a Durable Firm

11:13 Traits of Long Run Managers

Listen now & check out her article here:

https://t.co/Ybxd6uMI9E

1/“If all you wanna do all day is spend your time investing… don’t start your own fund.”😮💨

As always, @daveclark85 came to Origins w venture data, fund math & a grounded LP reality check. He left a lot to unpack… so @nchirls & @Beezer232 kept rolling.

https://t.co/w7WRNsaeT3

6/ If you care about how venture returns are actually generated (and distributed), this episode is worth your time.

As always, TY @daveclark85! 👏

https://t.co/0nNoadSLtf

🧵What actually drives venture returns at scale & can it still work today?

@daveclark85, CIO of VenCap, joins Origins w @beezer232 & @nchirls to break down VC performance using decades of LP data + firsthand insight as an LP in franchise firms like @a16z 👇

5/ One big shift: Late-stage private markets have quietly become the public markets for early-stage VCs. More liquidity. More secondaries. New playbook.

On consolidation: Yes — capital is concentrating at the top. But David’s view is that it’s cyclical, not permanent.