@tszzl Humans themselves are not very smart individually; it's only a superorganism of humans (a company, a nation, societies culture) that builds cathedrals and microchips through cumulative selection

I spent time in Shenzhen last year and when I saw Merz come back from China saying Germans need to work more I immediately knew what broke his brain because I lived the exact same cognitive shock

my first week in Huaqiangbei I burned through 4 prototype iterations of a motor controller board for less than a thousand bucks total, back home a friend was working on something similar and spent over 12 thousand for a single revision that took almost two months to arrive

when you live that contrast in your own hands with your own project something permanently shifts in how you see the world and it goes way deeper than speed & cost

what Shenzhen actually built is a collective learning organism, imagine 20 PCB fabs 15 injection mold shops 30 component distributors and a hundred firmware freelancers all within a 2km radius, looks insanely redundant from the outside until you realize redundancy is actually information density in disguise

I watched this firsthand with an injection mold supplier I was working with, this guy had seen a hundred founders iterate similar thermal designs over 6 months so he proactively modified his tooling before I even opened my mouth, he knew what I needed before I knew what I needed, the intelligence lives in the relationships between the nodes and it compounds daily

the west thinks about manufacturing as a cost center you optimize by centralizing…

China accidentally built a distributed neural network of manufacturing intelligence where knowledge diffuses horizontally across thousands of agents faster than any single western company can process internally

so when Merz comes back and says we need to work a bit more I think he saw the problem but COMPLETELY misdiagnosed the solution, telling Germans to work harder is like telling a horse to gallop faster when the other side built a combustion engine

the gap is ARCHITECTURAL

it’s ecosystem density, you need a custom connector in Shenzhen you walk 200 meters, in Munich you send an email and wait 3 weeks

it’s iteration speed, parallel search vs sequential optimization at the system level, it’s risk tolerance, Chinese founders ship something broken on Monday fix it Tuesday ship again Wednesday while European companies are still in the approval phase for the pilot program of the feasibility study…

and Merz only saw the surface, what he missed is the tier 2 cities like Hefei Chengdu Wuhan replicating the Shenzhen model at scale right now

BYD going from irrelevant to outselling every european automaker combined in roughly 5 years, Huawei building its own 7nm chip under maximum sanctions when every analyst said it was physically impossible & behind all of that a government that treats advanced manufacturing as an existential national priority while europe debates whether AI needs another ethics committee

I think what we’re watching is the most asymmetric economic competition in modern history and most western leaders are still framing it as a productivity problem when it’s actually an ontological one

Europe & America are optimizing variables that China stopped tracking years ago meanwhile China is compounding on dimensions the west has no framework to even measure

Merz at least had the courage to name

it out loud and I respect that genuinely but working a bit more inside a broken architecture just means you arrive at the wrong destination slightly faster

@ProfessorPape@grok estimate how many dollars just the relocation of all the military stuff into this region costs. How much do American tax payers have to pay for this move only

Wow.. you can now instantly turn any GitHub repo into AI-generated documentation, just by changing the URL.

Replace “github” with “deepwiki” in any GitHub URL and you’ll see:

→ Instant docs for any codebase

→ Chat with it like a conversation

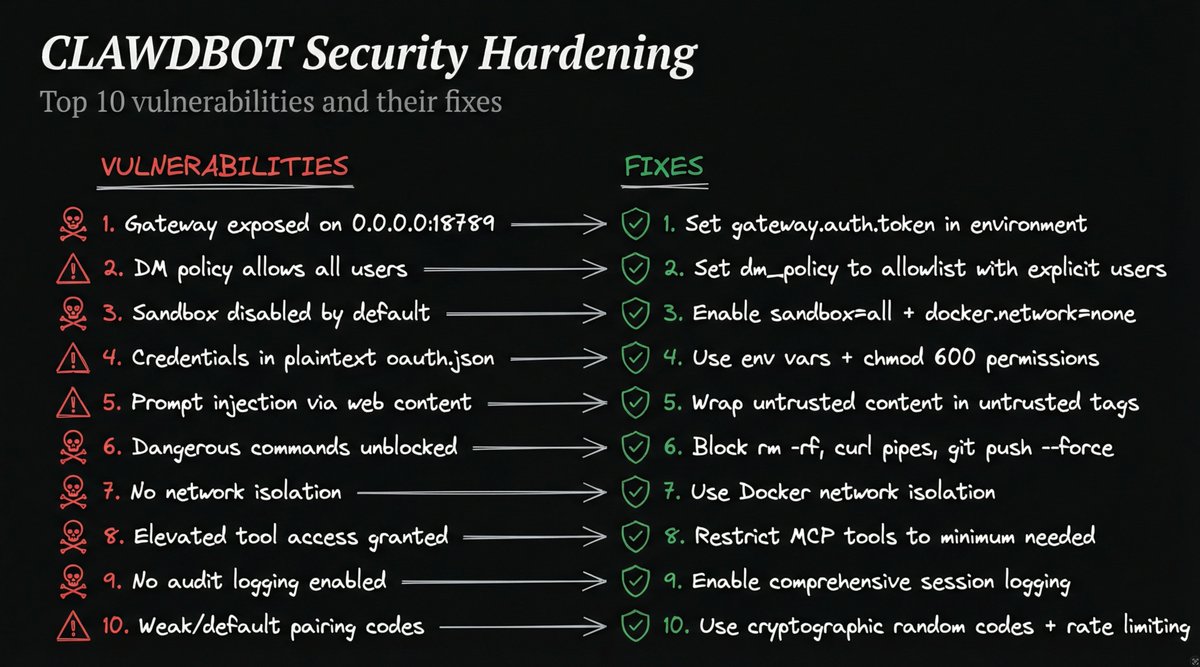

As a Security / 98% AI YOLO Maximalist with Guardrails guy, I'm asking you to please listen to this.

Here are some of the top security issues with https://t.co/yCq4RmE7lB that you all should be avoiding.

Don't avoid the project. It's great. But please be safe with it!

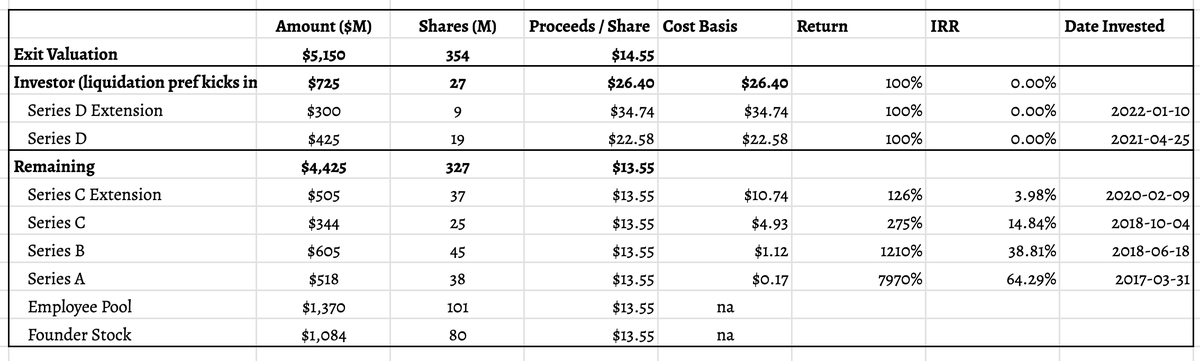

Put together a quick analysis of the Brex exit based on an analysis of their cap table.

Done relatively quickly, so pardon any errors! Funding history sourced from @CaplightData.

Overall, it's a pretty big win.

— The company probably minted well in excess of 100 millionaires.

— Everyone who joined or invested in 2018 or earlier is probably pretty happy, some even ecstatic.

— Those who invested / joined in 2020-21 probably aren't but that is a story that is true of almost every employee or investor in that period (private / public market).

— Those who joined in late 2022 through today is probably doing reasonably fine.

Common Stock TL;DR — liquidation Preference took a bit of a bite, but only for those who joined in 2021-22. Everyone else either did fine or really well.

- Founders did very well (~$1B in total). There was a decent bit of dilution, particularly from healthy option pools over the course of 8-9 years.

- Employees joining 2023-2025 would probably be roughly breakeven — they probably received RSUs priced in the $4-6B.

- Employees joining 2021-2022 got stock at the peak. These would have been underwater RSUs or options. Most companies issued additional make-whole shares to those who stuck around. I'm sure Brex did this. However, those who joined then and left after a couple of years probably lost most of the value to their equity.

- Employees joining 2020 did okay -- slightly above where they joined. Not commensurate with the risk, but honestly way better than most companies who raised at peak valuations in the COVID era.

- Employees joining earlier did VERY well. I'd estimate 3-10x if they joined in 2018-19; and 10-100x if they joined in 2017-18.

Investor TL;DR

- Series D/D+ investors in 2021-21 (Tiger, Greenoaks) get money back but 0% IRR. TBH this is a win since most late stage investments in that vintage are tough.

- Series C+ investors in 2020 (Kleiner, DST) get a modest return (1.3x) but suboptimal IRR (4%). Again, tough vintage.

- Series C investors in 2018 (DST) get a decent return (2.75x) and 15% IRR.

- Series B investors in 2018 (YC Continuity) gets an excellent return (12x) and IRR (39%)

- Series A investors in 2017 (Ribbit) did fantastic (80x and 64% IRR)

- YC worth calling out — the regular YC check probably netted out close to $100M, on an (I think) $120K check at the time. 800x in 9 years = 110% IRR ain't half bad. If you bake in YC continuity, a total of $600M on probably ~$40M invested.

Brex’s $5.15B exit tells you exactly who gets paid in venture and who doesn’t.

The math reveals a clean split by vintage:

YC’s original $120K check turned into roughly $100M. 800x return. 110% IRR across 9 years. Their follow-on through YC Continuity adds another $500M on ~$40M invested. One company. Two checks. $600M.

Series A investors from 2017 made 80x at 64% IRR. Series B in early 2018 made 12x at 39% IRR. These are the returns that make venture pencil as an asset class.

Series C in late 2018 made 2.75x at 15% IRR. Still solid but you’re now in PE territory for a startup’s risk profile.

Then the 2020-2021 cohort. Series C+ investors got 1.3x at 4% IRR. Series D investors from Tiger and Greenoaks got their money back with 0% IRR. In a world where most late-stage 2021 vintage investments are underwater, breakeven is actually a win.

The employee story mirrors the same curve. Founders walked with ~$1B. Anyone who joined 2018 or earlier made 3-100x depending on timing. 2021-2022 joiners got underwater equity, though most who stayed probably received refresh grants.

Entry timing dominates everything. Same company. Same outcome. Wildly different returns based on when you wrote the check or signed the offer letter.

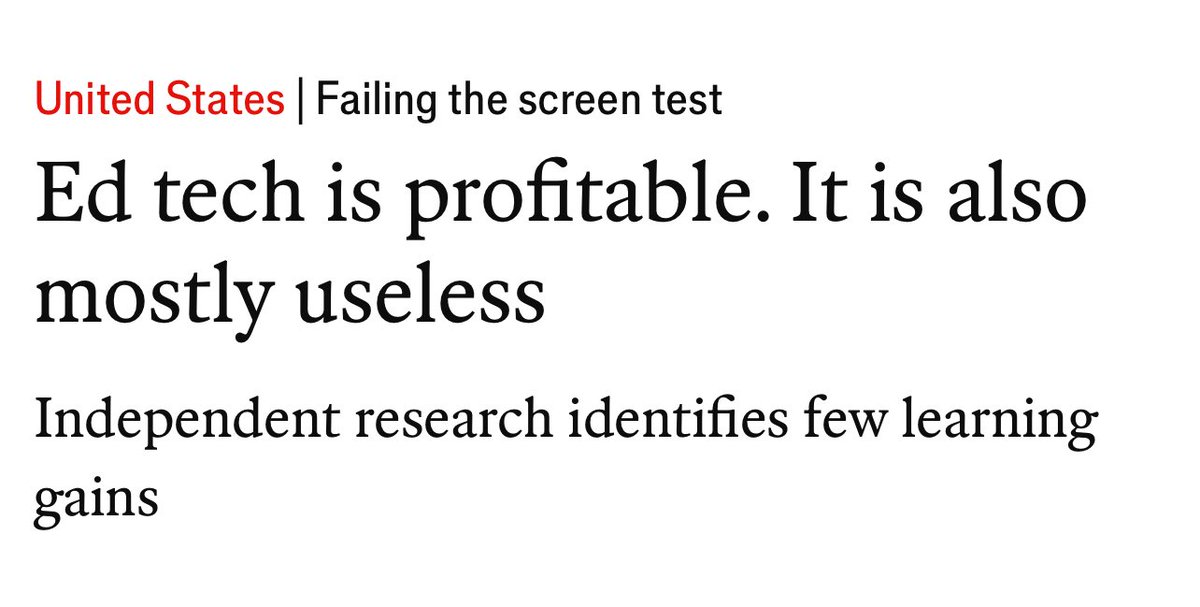

‘Although ed-tech companies tout huge learning gains, independent research has made clear that technology rarely boosts learning in schools—and often impairs it.

A 2024 meta-analysis of 119 studies of early-literacy tech interventions, led by Rebecca Silverman of Stanford University, found the studies described programmes that delivered at best only marginal gains on standardised tests. The majority had little effect, no effect or harmful ones. Jared Horvath, a neuroscientist and author of a book called “The Digital Delusion”, has reviewed meta-analyses covering tens of thousands of studies. His verdict: “In nearly every context, ed tech doesn’t come close to the minimum threshold for meaningful learning impact.”’

Stop predicting words one by one.

A new paper just broke the next-token rule every LLM follows.

It cuts generation steps by 4× and training compute by 44%.

𝗡𝗲𝘅𝘁-𝘁𝗼𝗸𝗲𝗻 𝗽𝗿𝗲𝗱𝗶𝗰𝘁𝗶𝗼𝗻 𝗶𝘀 𝘁𝗵𝗲 𝗯𝗼𝘁𝘁𝗹𝗲𝗻𝗲𝗰𝗸

CALM replaces word-by-word guessing with vector-by-vector prediction.

Each step predicts a continuous vector representing multiple tokens.

The model operates on ideas per step, not symbols.

• One vector encodes about four tokens

• Sequence length drops by four

• Attention and sampling shrink with it

𝗧𝗵𝗲 𝗮𝗿𝗰𝗵𝗶𝘁𝗲𝗰𝘁𝘂𝗿𝗲 𝗿𝗲𝗺𝗼𝘃𝗲𝘀 𝗱𝗶𝘀𝗰𝗿𝗲𝘁𝗲 𝗹𝗶𝗺𝗶𝘁𝘀

It uses an autoencoder to compress and reconstruct text with 99.9% accuracy.

An energy-based Transformer predicts the next vector in one step.

There is no softmax, no vocabulary ceiling, no token sampling.

𝗧𝗵𝗶𝘀 𝗰𝗵𝗮𝗻𝗴𝗲𝘀 𝘄𝗵𝗮𝘁 𝗹𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗺𝗼𝗱𝗲𝗹𝘀 𝗰𝗮𝗻 𝗱𝗼

• Faster training and inference

• Better performance per FLOP

• New evaluation metric replacing perplexity

If it scales, token-based LLMs become the inefficient baseline.

Late-cycle bubble vibes.

Gold hit $4,997 today, up 80% YoY. Silver broke $102, up 234% YoY. Copper touched $5.82/lb after record highs above $6 earlier this month. Natural gas just ripped 70% in 5 days.

All three metals refreshed all-time highs simultaneously for the first time since 1980.

When every commodity class moves in lockstep, it usually means one thing: too much money chasing too few hard assets. Central banks buying. Sovereigns hoarding. Retail piling in. The “this time is different” narratives multiply. Gold to $7,000. Silver to $150. Copper supply deficit forever.

The arguments sound reasonable in isolation. Geopolitical hedging against dollar weaponization. AI data centers eating copper. Solar panels consuming silver. China stockpiling everything.

But when natural gas rips 70% in 5 days while gold, silver, and copper all hit records in the same month? That’s crowded trades getting more crowded.

The last time commodities moved like this was late 2020 into 2021. Lumber went vertical. Copper screamed. Silver had its moment. Everyone had a thesis. Then gravity showed up.

The question isn’t whether these metals have real demand drivers. They do. The question is whether current prices already reflect the next five years of bullish assumptions.

When your Uber driver asks about silver ETFs, you’re not early anymore.

RIP Elevenlabs. Alibaba Qwen dropped this new AI text to speech

Free & open source, <2GB vram, super fast.

It has instant voice cloning, emotion control, and even voice design.

Full tutorial: https://t.co/ZHupx2rIha