Chinese robotics didn't enter mainstream America through a Pentagon demo. It entered through a talent show.

A 26 year old Chinese engineer just walked in with 8 Unitree humanoids and got a standing ovation.

Finnish scientists trucked in real forest dirt and grass and laid it over the gravel at four daycare yards. They let the kids dig around in it for a month. The blood tests came back with changes the researchers hadn’t expected to see so fast or so clear.

The study ran at ten daycares in two Finnish cities with 75 kids aged three to five. Four of the yards got the forest treatment: about a tennis court worth of soil and grass laid over the gravel, plus planters and peat blocks the kids could dig and climb on. Three others stuck with their normal gravel yards. The last three were daycares where the kids were already visiting real forests every day.

After one month, the variety of bacteria living on the kids’ skin shot up, and the kind that helps train the skin’s immune defenses jumped the most. Their gut bacteria started to look like the gut bacteria of the forest-visiting kids. Their blood showed more of the immune cells whose job is to keep the body from freaking out at harmless stuff like pollen and peanuts, and overall inflammation dropped. The kids on the plain gravel yards showed none of this.

Childhood asthma in the US doubled between 1980 and 1995. Food allergies in kids jumped 50 percent between 1997 and 2011, then jumped another 50 percent between 2007 and 2021. And peanut allergies in one-year-olds tripled between 2001 and 2017.

The Finnish researchers think one of the reasons is simple: kids today don’t get dirty enough. 37 percent of American preschoolers now spend an hour or less outside on a normal weekday. Their immune systems are getting trained in environments stripped of the bacteria humans have always lived around.

Aki Sinkkonen, who led the study, put it in plain words: “It would be best if children could play in puddles and everyone could dig organic soil.” The Finnish government is now helping pay for daycares across the country to make the same changes.

NVIDIA QUIETLY DROPPED A $249 BOX THAT REPLACES YOUR $200/MONTH OPENAI SUBSCRIPTION WITH $2 IN ELECTRICITY

it's called the jetson orin nano super. smaller than a wallet, runs at 25 watts, does 70 trillion ai operations per second. runs llama 3, mistral, gemma and deepseek locally with no api fees and no data leaving your house

a developer running automations and coding assistants pays $200 a month to openai. the same workload on this box costs $2 a month in electricity and breaks even in 10 weeks

install ollama with one command. change one line in your code. point it at localhost instead of openai. everything else works identically

7 billion parameter models handle 80% of what people use chatgpt for. summarization, drafting, coding, document q&a, automation pipelines. total monthly cost drops from $200 to $22

cloud subscriptions keep getting more expensive and rate limits keep getting tighter. the people who set this up in 2025 are going to look very smart in 2027

bookmark this and read the article below

Elon Musk avait dit un truc qui m'avait marqué sur l'allocation de ressources. En substance : passé un certain niveau de richesse, l'argent n'est plus de la consommation, c'est de l'allocation de capital.

Cette phrase change tout.

L'économie, dans le fond, c'est juste un problème d'allocation. Tu as des ressources finies et des usages infinis. Qui décide où va quoi ?

Imagine une cour de récré. 100 enfants, des paquets de cartes Pokémon distribués au hasard. Tu laisses faire. Très vite, un ordre émerge. Les bons joueurs accumulent les cartes rares, les collectionneurs trient, les négociateurs trouvent des deals. Personne n'a planifié. Et pourtant chaque carte finit dans les mains de celui qui en tire le plus de valeur. Le système maximise le bonheur total de la cour. C'est ça, la main invisible.

Maintenant fais entrer la maîtresse. Elle trouve ça injuste. Léo a 50 cartes, Tom en a 3. Elle confisque, redistribue, impose l'égalité. Trois effets immédiats. Les bons joueurs arrêtent de jouer, à quoi bon. Les mauvais n'ont plus de raison de progresser, ils auront leur part. Les échanges s'effondrent. La cour est égale, et morte. Elle a maximisé l'égalité, elle a détruit le bonheur.

Le problème de la maîtresse, c'est qu'elle ne peut pas avoir l'information que la cour avait collectivement. C'est le problème du calcul économique de Mises, formulé en 1920. L'URSS a essayé de le résoudre pendant 70 ans avec le Gosplan. Résultat : pénuries, queues, effondrement. Pas parce que les Soviétiques étaient bêtes, parce que le problème est mathématiquement insoluble en mode centralisé.

Quand Musk a 200 milliards, il ne les consomme pas, il les alloue. SpaceX, Starlink, Neuralink, xAI. Chaque dollar est un pari sur le futur. Et lui a un track record. PayPal, Tesla, SpaceX. Il a démontré qu'il sait identifier des problèmes immenses et y allouer des ressources avec un rendement spectaculaire.

L'État aussi a un track record. Hôpitaux qui s'effondrent, éducation qui décline, dette qui explose, services publics qui se dégradent malgré des budgets en hausse constante. Le marché identifie les bons allocateurs, la politique identifie les bons communicants.

Le profit n'est pas une finalité, c'est un signal. Il dit : tu as alloué des ressources rares vers un usage que les gens valorisent suffisamment pour payer. Plus le profit est gros, plus la création de valeur est grande. Quand Starlink est rentable, ça veut dire que des millions de gens dans des zones rurales ont enfin internet. Quand un ministère est en déficit, ça veut dire qu'il consomme plus qu'il ne produit. L'un crée, l'autre détruit, et on appelle ça redistribution.

Dans nos sociétés il y a deux catégories d'acteurs. Les entrepreneurs et les bureaucrates. L'entrepreneur prend un risque personnel pour identifier un problème, mobiliser des ressources, créer une solution. S'il se trompe il perd. S'il a raison, ses clients gagnent, ses employés gagnent, ses fournisseurs gagnent, l'État collecte des impôts. Il est la cellule de base du progrès humain.

Le bureaucrate ne prend aucun risque personnel. Son salaire est garanti. Au mieux il maintient une rente existante. Au pire il la détruit par excès de réglementation, mauvaise allocation forcée, incitations perverses qui découragent ceux qui produisent. Mais dans aucun cas il ne crée.

Regarde les 50 dernières années. iPhone, internet civil, SpaceX, Tesla, Google, Amazon, Stripe, mRNA, ChatGPT. Toutes des inventions privées, portées par des entrepreneurs, financées par du capital risque. Pas un seul ministère n'a inventé quoi que ce soit qui ait changé ta vie au quotidien.

La France est devenue le laboratoire mondial de la dérive bureaucratique. 57% du PIB en dépenses publiques, record absolu. Une administration tentaculaire, une fiscalité qui pénalise la création de richesse. Résultat : décrochage face aux États-Unis, à l'Allemagne, à la Suisse. Fuite des cerveaux. Désindustrialisation. Dette qui explose.

Et le pire c'est que la mauvaise allocation s'auto-renforce. Plus l'État prélève, moins les entrepreneurs créent. Moins ils créent, moins il y a de base fiscale. Plus l'État s'endette et taxe. Boucle de rétroaction négative parfaite. La maîtresse pense qu'elle aide, et chaque année la cour produit moins.

Dans nos sociétés, ce sont les entrepreneurs, toujours, qui font avancer la civilisation. Les bureaucrates au mieux maintiennent une rente, au pire la détruisent. Aucune société n'a jamais progressé en taxant ses créateurs pour subventionner ses gestionnaires.

La question n'est jamais qui a combien. C'est qui alloue le mieux la prochaine unité de ressource pour maximiser le futur de l'humanité. La réponse depuis 200 ans n'a jamais changé. Ce ne sont pas les fonctionnaires.

@mwebster1971 Charles Harris, "non hedge fund managers," anyone with insight on how large funds manage positions. (Yes, you've done a couple of those already.)

“People always forget that 50% of a stock’s move is the overall market, 30% is the industry group, and then maybe 20% is the extra alpha from stock picking. And stock picking is full of macro bets. When an equity guy is playing airlines, he’s making an embedded macro call on oil.���

— Stanley Druckenmiller

2028: The Year the Lights Go Out for AI Clusters?

The AI industry has officially shifted from a "Compute Crunch" to a "Photonics Panic."

$LITE CEO Michael Hurlston just delivered a seismic warning: if current order rates for US hyperscalers persist for just two more quarters, their production capacity will be completely sold out through the end of 2028.

This isn't just a corporate milestone; it’s a structural ceiling for AI growth.

When the market leader closes its books for the next three years, the "Optical Nervous System" of AI becomes the most valuable commodity on Earth.

1⃣The Direct Capacity Alternatives (Primary Laser & Module Sources)

As hyperscalers scramble for slots that Lumentum can no longer provide, they are diverting billions to the only other firms with high-volume production lines:

➡️Applied Optoelectronics $AAOI:

The primary beneficiary of the spillover. Their strategic partnership with Microsoft and massive Texas-based manufacturing capacity makes them the immediate "Plan B" for 800G and 1.6T modules.

➡️Coherent $COHR:

Lumentum’s most formidable rival. They hold a massive share in EML (Electro-absorption Modulated Laser) technology.

With LITE full, Coherent becomes the default gatekeeper for high-end optical capacity.

2⃣The Foundry & OSAT Layer (Manufacturing & Advanced Packaging)

These firms provide the physical fabrication and specialized assembly services for the industry's biggest players:

➡️Tower Semiconductor $TSEM:

A crucial "Foundry" player. They specialize in Silicon Photonics (SiPh) fabrication, acting as the factory floor for fabless designers who need to integrate light onto silicon at scale.

➡️Fabrinet $FN:

The "Gold Standard" of optical contract manufacturing.

They physically assemble the complex modules for Nvidia, Cisco, and Lumentum.

A sold-out industry means Fabrinet’s high-precision lines are the most contested real estate in tech.

3⃣The "Intelligence" Layer (DSP & Architecture Control)

Hardware is useless without the silicon that manages the signals.

This layer dictates the efficiency of every photon:

➡️Marvell $MRVL & Broadcom $AVGO:

The duopoly in DSP (Digital Signal Processors). Every laser module requires their silicon to "talk" to the GPU.

Marvell’s TERA platform is the mandatory brain behind the 1.6T era.

➡️MACOM Technology $MTSI:

The pioneer of LPO (Linear Pluggable Optics). By removing the power-hungry DSP in specific short-reach links, MACOM offers a "power-saving" escape hatch for data centers hitting their electricity grid limits.

4⃣The Innovation Accelerators (Bridging the Supply Gap)

With traditional capacity blocked, these innovators are accelerating "Next-Gen" architectures to bypass the bottleneck:

➡️Sivers Semiconductors $SIVE:

A leader in external light sources (CW-WDM) for CPO (Co-Packaged Optics).

Sivers is essential for moving the laser from the pluggable module directly into the processor package - the holy grail of efficiency.

➡️Alumea $ALMU:

A specialist in high-efficiency silicon photonics engines, streamlining the transition to 1.6T and 3.2T speeds where traditional optics fail.

➡️POET Technologies $POET:

Their "Optical Interposer" is a motherboard for light, allowing for radical miniaturization and lower-cost assembly compared to traditional "active" optical alignment.

➡️Lightwave Logic $LWLG:

Developing proprietary electro-optic polymers. These materials modulate light at speeds (200G+ per lane) that standard inorganic crystals struggle to achieve.

5⃣The Transport Giants (DCI & Global Infrastructure)

Data must move between clusters and across continents. These firms control the "Inter-City" light:

➡️Ciena $CIEN: Their WaveLogic coherent optics are the global standard for long-haul Data Center Interconnect (DCI).

➡️Nokia $NOK - Optical Networks (NOC):

They provide the high-capacity optical transport and carrier-grade routing that form the literal backbone of the global AI internet.

6⃣The Quality Gatekeepers (Testing & Validation)

In a world of scarcity, a single "dud" laser can take down a $10B cluster.

Yield is everything:

➡️Aehr Test Systems $AEHR:

The kings of wafer-level "burn-in."

Their FOX-XP systems test thousands of lasers simultaneously under extreme stress to ensure they don’t fail after installation.

➡️FormFactor $FORM:

They provide the ultra-precise "probes" and test systems that validate optical performance on the wafer before it is even cut into chips.

7⃣The Atomic Foundation (Raw Materials & Substrates)

The "Bottleneck of Bottlenecks."

No substrate = no laser.

Period.

➡️AXT Inc $AXTI:

A critical supplier of Indium Phosphide (InP) wafers—the physical medium required for the high-performance lasers that drive AI.

➡️IQE PLC $IQE:

The masters of Epitaxy. They "grow" the complex semiconductor layers on wafers atom-by-atom. IQE is the first point of failure in the global supply chain.

➡️Soitec $SOI.PA:

The dominant provider of SOI (Silicon-on-Insulator) wafers, the essential building block for the entire Silicon Photonics movement.

⬇️Executive Summary: The Photonics Supercycle

A situation where a market leader (Lumentum) sells out production nearly 3 years in advance happens once a decade. This means the speculative phase of AI has ended, and the phase of brutal infrastructural execution has begun.

Key Investor Takeaways:

▶️Seek "Available Capacity": If LITE is full, capital and orders will immediately flow to AAOI and COHR.

▶️Watch the Foundations: Without wafers from AXTI and processes from IQE, not a single additional laser can be built. These are the true "Gatekeepers."

▶️Bet on Quality: With such massive production scales, errors are inevitable. Testing companies like AEHR and FORM will benefit from every photon produced.

▶️Innovation is Mandatory: New architectures like LPO (MACOM) or CPO (Sivers/POET) are no longer just curiosities, they are the only way to prevent AI from "suffocating" due to energy and bandwidth limits.

⬇️Question to the Community:

Analyzing the current supply chain and the fact that optical infrastructure is becoming the new "AI bottleneck", which of these companies would you invest in today at their current market valuation?

Which one has the highest potential for a "re-rating" in the coming quarters?

Let us know in the comments by dropping the Ticker! 👇

🚨 In 1992, a MIT lecture quietly revealed more about product and sales than most 2-year MBAs ever will.

Most people have never seen it.

It came from Steve Jobs and instead of teaching theory, he broke down how great products actually win.

Watching it today feels unreal.

He explained that people don’t buy products they buy meaning. The best products aren’t just functional, they connect with how people see themselves. That’s why some ideas spread effortlessly while others die, even if they’re technically better.

He also made it clear that marketing isn’t about features. It’s about clarity. If you can’t explain why your product matters in simple terms, it won’t matter at all. Complexity doesn’t impress it confuses.

And his biggest edge? Obsession with experience. Not just what the product does, but how it feels. The small details, the simplicity, the story that’s what separates good from unforgettable.

That’s why this MIT lecture still hits hard.

Because while most people are building products…

Very few understand why people actually buy them.

$OPTX $AAOI ... #1 TELECOM FIBER OPTICS

The telecom fiber optics industry group is the best performing group in 2026. This group has advanced 84% year to date. Syntec Optics (OPTX) is the top performing stock in this industry group, and has advanced 200% in 2026. Applied Optoelectronics (AAOI) has advanced 198% in 2026.

$AEHR ... Aehr Test Systems (AEHR) announced it has received an initial order from a major new customer that is a global leader in networking products and solutions and a major supplier to the data center optical transceiver market. The customer is developing advanced silicon photonics-based transceivers for data center networking and optical I/O applications to address the rapidly accelerating demand for high-speed fiber optic communication links in hyperscale AI and cloud data centers.

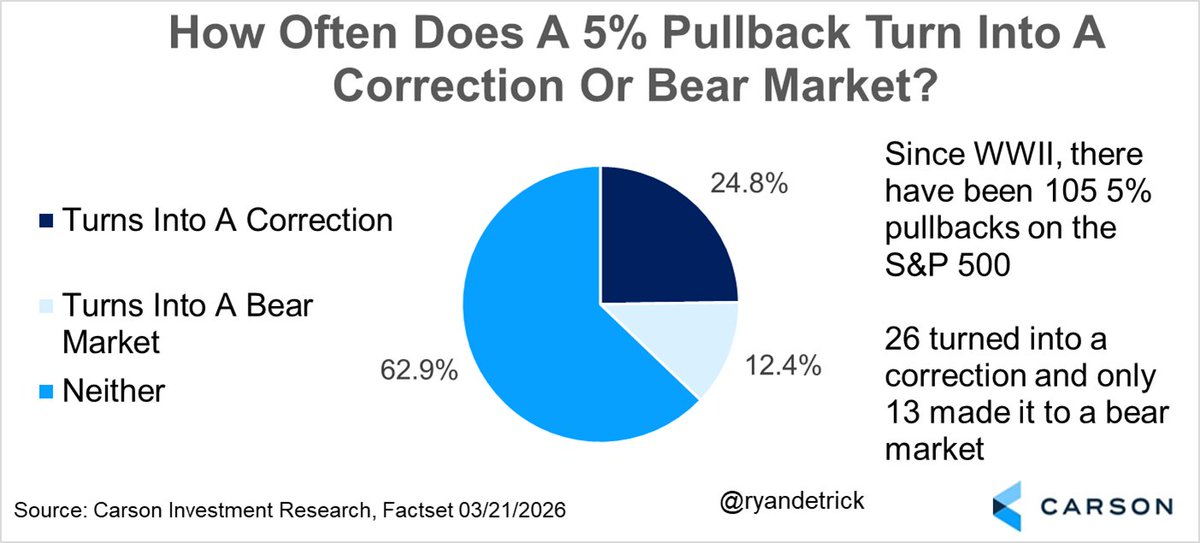

Since WWII, there have been 105 5% pullbacks (not including the current one).

About 25% of those turned into a correction and only 12.4% turned into a bear market.