$NOW is a once-in-a-lifetime opportunity.

2030 price targets:

• Bear case: $315

• Base case: $407

• Bull case: $523

The bull case implies ~22% 5-year FCF CAGR - and it’s achievable through:

• Consistent beat-and-raises through 2030

• Operating leverage through AI efficiency unlocks and revenue scaling faster than expenses

• NDRR >115% + accelerated token consumption monetization

Other key factors:

• CEO buying shares while calling for a $1T valuation by 2030

• Strong Rule of 40 performance (~60%),

• Multiple “massive” new logo deals going live on the Now platform this quarter

Do you think $NOW reaches $500?

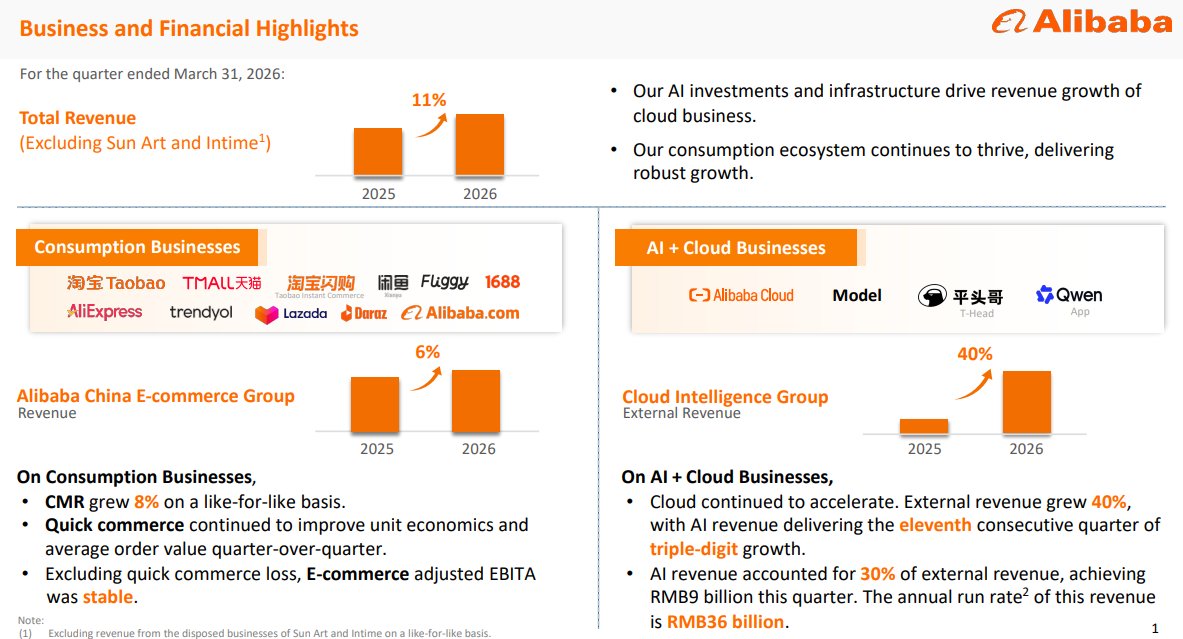

Alibaba’s AI Moment Is Finally Here And The Market Still Doesn’t Fully Get It

I’ve been covering Alibaba $BABA for years, and honestly, for a long time, the story around this company felt stuck in the mud.

Every quarter looked the same.

Investors obsessed over slowing Chinese consumption, regulatory fears, weak sentiment, and whether Alibaba had permanently lost its identity as a growth company.

The market stopped viewing BABA as a technology platform and started valuing it like a mature retailer trapped inside a struggling macro environment.

But after going through Alibaba’s fiscal Q4 2026 results in detail, I think something important just changed.

Not the headline numbers. Those actually looked terrible at first glance.

I’m talking about the underlying narrative.

For the first time in years, Alibaba is showing clear evidence that its AI investments are no longer just experimental projects or flashy demos designed for investor presentations.

The monetization engine is finally starting to appear in a meaningful way.

And once you dig beneath the ugly earnings headlines, you start realizing why the stock reversed from a sharp premarket selloff to finishing the session up more than 8%.

In my opinion, this was one of the most important quarters Alibaba has reported since the regulatory crackdown era began.

The Headline Numbers Looked Ugly

If you only looked at the surface-level metrics, you would think Alibaba had delivered a disaster.

Revenue grew just 3% year-over-year to RMB243.4 billion, while adjusted EBITA collapsed 84% YoY.

Non-GAAP EPS also fell dramatically and free cash flow turned deeply negative as the company accelerated spending across AI infrastructure, cloud expansion, quick commerce, and user acquisition for its Qwen ecosystem.

Initially, algorithms reacted exactly how you would expect.

The stock sold off aggressively in premarket trading because the quarter looked like a classic margin destruction story.

But that interpretation completely missed what was actually happening underneath the hood.

Alibaba is intentionally sacrificing near-term profitability to build what could become China’s dominant AI-cloud ecosystem.

And unlike previous AI narratives that were built mostly around theoretical future potential, this quarter showed actual commercialization momentum.

This Wasn’t A Retail Quarter It Was An AI Quarter

The real story here wasn’t e-commerce.

It was Cloud Intelligence Group.

Cloud revenue surged 38% YoY to RMB41.6 billion, while external customer revenue accelerated to 40% growth.

More importantly, AI-related product revenue continued posting triple-digit growth for the eleventh consecutive quarter.

That matters a lot more than people realize.

For years, the bearish argument around Alibaba’s cloud business was that growth had structurally peaked.

Investors believed Alibaba Cloud had become little more than a slower-growing infrastructure utility tied to China’s weak economy.

This quarter shattered that thesis.

What we’re seeing now is Alibaba evolving beyond traditional cloud infrastructure into something much more valuable.

The company is transitioning from basic IaaS-style compute and storage into full-stack AI monetization.

And that changes the economics entirely.

Management made it very clear during the earnings call that demand is rapidly shifting toward Model-as-a-Service offerings, enterprise AI agents, orchestration software, inference workloads, and production-scale AI deployments.

This is where the real money in AI infrastructure will likely be made over the next decade.

Anybody can rent storage.

Very few companies can provide an integrated ecosystem combining proprietary LLMs, AI chips, cloud infrastructure, orchestration software, enterprise agents, and consumer distribution at scale.

Alibaba is trying to become all of that simultaneously.

Qwen Is Quietly Becoming A Serious Asset

I think the market still underestimates how important Qwen could become.

For a while, Western investors largely ignored Alibaba’s AI models because the assumption was simple: Chinese AI companies would remain permanently behind OpenAI, Anthropic, and Google.

But that narrative has started breaking apart.

Alibaba’s Qwen models are now showing increasingly competitive performance across reasoning, coding, multimodal applications, and enterprise workflows.

The company also launched specialized models focused on video generation and real-time interactive world models.

More importantly, Alibaba is no longer treating Qwen as a standalone chatbot product.

They’re integrating it directly into their commerce ecosystem.

That’s a major strategic advantage.

Taobao and Tmall services are now integrated into the Qwen app itself, while Alibaba also launched AI shopping assistants and enterprise AI agents designed for merchants.

This creates something Western investors may not fully appreciate yet:

Alibaba owns one of the largest real-world commercial datasets in China.

Every search, every transaction, every merchant interaction, every logistics workflow, every product recommendation, and every consumer behavior signal feeds directly into the ecosystem.

That data advantage becomes incredibly powerful in the AI era.

Amazon figured this out years ago.

Alibaba is now pushing aggressively in the same direction.

The Market Is Missing The Bigger Picture

One thing I keep noticing with Alibaba coverage is that investors are still analyzing this business primarily through a retail lens.

But Alibaba is increasingly becoming an AI infrastructure and platform company.

And if that transformation succeeds, the valuation framework changes dramatically.

At roughly 21x forward earnings, Alibaba is no longer dirt cheap like it was during the peak pessimism phase when it traded closer to 10-12x earnings.

But I still think the stock remains materially undervalued relative to what this business could become over the next several years.

Because if Alibaba successfully scales its AI-cloud monetization engine, the market will eventually stop valuing it like a Chinese retailer and start valuing it more like a strategic AI infrastructure provider.

That multiple difference matters enormously.

The market already gives companies like Microsoft $MSFT , Amazon $AMZN, and Nvidia $NVDA premium valuations because investors understand they sit at the center of the AI compute stack.

Alibaba is trying to build the Chinese equivalent of that ecosystem.

And frankly, they may be further along than many people realize.

Their AI Chip Strategy Is Flying Under The Radar

Another thing that caught my attention this quarter was Alibaba’s growing vertical integration strategy.

Most investors know Amazon has been aggressively building its own AI chips through Trainium and Inferentia.

Alibaba is following a similar playbook.

Its proprietary Zhenwu PPUs are already being deployed across Alibaba Cloud infrastructure, and management disclosed that over 100,000 chips have been deployed on its public cloud platform.

This is important for several reasons.

First, China’s access to advanced Western semiconductors remains uncertain due to export restrictions.

Second, proprietary silicon meaningfully improves long-term cloud economics.

Third, owning both the infrastructure layer and the chip layer creates stronger ecosystem lock-in.

And finally, AI demand itself is becoming so large that every hyperscaler increasingly wants control over its own hardware stack.

That’s not unique to Alibaba.

That’s becoming the new industry standard.

The company also announced partnerships tied to intelligent driving and autonomous systems, which shows Alibaba is expanding beyond generic cloud workloads into higher-value AI compute markets.

Again, this is exactly the kind of ecosystem expansion investors reward in U.S. mega-cap AI companies.

The Profitability Collapse Looks Scary But It’s Probably Temporary

Now obviously, there are real risks here.

You can’t ignore an 84% collapse in adjusted EBITA.

Free cash flow also deteriorated sharply because Alibaba is spending aggressively on AI infrastructure, quick commerce subsidies, and ecosystem expansion.

And yes, the quick commerce business is still pressuring margins.

But when I step back and look at this quarter strategically, I don’t see a collapsing business.

I see a company entering investment mode again.

That distinction matters.

There’s a huge difference between margin compression caused by structural weakness versus margin compression caused by deliberate reinvestment into high-growth opportunities.

Amazon went through this exact phase multiple times.

So did Meta.

Wall Street punished both companies during heavy investment cycles before eventually rewarding them once monetization scaled.

Alibaba now appears to be entering a similar transition period.

The Most Important Signal From This Quarter

The biggest takeaway from this quarter wasn’t the revenue growth.

It wasn’t the EPS miss.

It wasn’t even the cloud acceleration itself.

The most important signal was this:

Alibaba finally proved that AI demand is materially driving customer acquisition and external monetization growth.

That’s the inflection point investors were waiting for.

For years, the AI story around Chinese tech felt speculative.

Now we’re seeing actual evidence that enterprise customers are adopting Alibaba’s AI services at scale.

Management even stated that Model Studio customers grew eightfold year-over-year as enterprises accelerated deployment of AI applications and production-scale workloads.

And once commercialization starts showing up consistently, valuation frameworks begin changing fast.

Valuation Still Looks Attractive To Me

Even after the recent rally, I still think Alibaba offers a compelling long-term setup.

Consensus estimates currently project fiscal 2028 EPS around the high single-digit range, and if Alibaba successfully executes on its AI-cloud transition, I think the market could eventually justify a materially higher earnings multiple than where the stock trades today.

Not because Alibaba suddenly becomes a pure AI company overnight.

But because the mix of the business starts improving.

Higher-margin AI services, enterprise software, cloud infrastructure, inference workloads, and AI agents are structurally more valuable than low-margin retail operations.

And once investors believe those segments can drive sustainable growth again, the re-rating potential becomes significant.

I don’t think the market fully appreciates how large China’s enterprise AI opportunity could become over the next decade.

The demand for AI compute, enterprise automation, inference infrastructure, and industry-specific AI deployment is still in the very early innings.

Alibaba is positioning itself right at the center of that trend.

🇨🇳A railway maintenance robot in China.

Detects scratches on rail surfaces down to 0.1mm units while automatically repairing them with a grinding tool at a maximum of 10,000 rotations.

It finds internal defects via ultrasonic flaw detection.

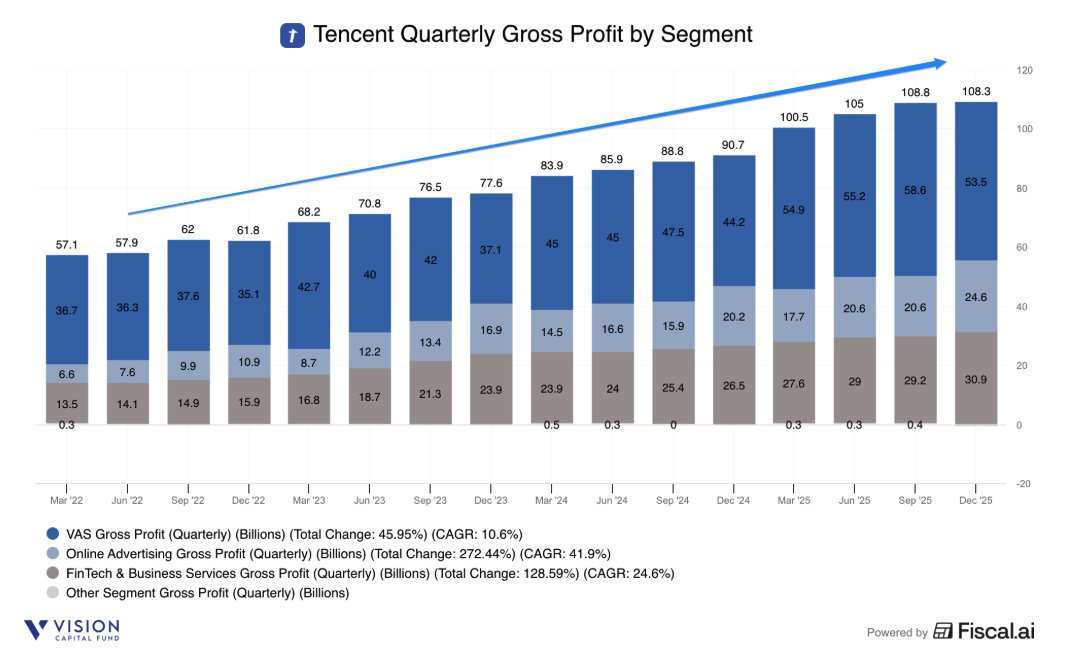

Tencent 4Q25 Earnings

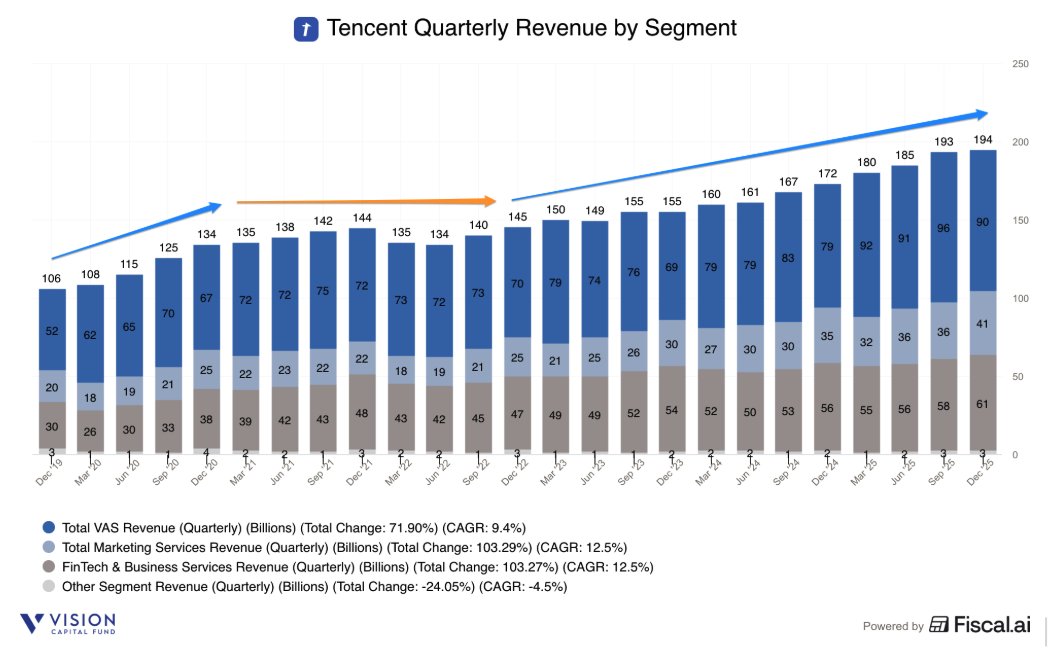

- Rev ¥194.4b +13% ↗️🟡

- GP ¥108.3b +19% ↗️🟢 margin 55.7% +314 bps ✅

- Adj EBITDA ¥83b +19% ↗️🟢 margin 42.7% +238 bps ✅

- NG EBIT ¥69.5b +17% ↗️🟢 margin 35.8% +128 bps ✅

- EBIT ¥60.3b +17% ↗️🟢 margin 31.0% +119 bps ✅

- NG Net Inc ¥64.7b +17% ↗️🟢 margin 33.3% +121 bps ✅

- Net Inc ¥59.1b +15% ↗️🟡 margin 30.4% +55 bps ✅

4Q25 Revenue by Segment

- VAS ¥89.9b +14% ↗️🟡

- VAS (Social Networks) ¥30.6b +3% ➡️🟠

- VAS (Domestic Games) ¥38.2b +15% ↗️🟢

- VAS (International Games) ¥21.1b +32% ↗️🟢

- Marketing Services ¥41.1b +17% ↗️🟢

- FinTech and Business Services ¥60.8b +8% ↗️🟡

- Others ¥2.5b +10% ↗️🟡

- Fair Value (listed investee) ¥672.7b

- Fair Value (unlisted investee) ¥363.1b

Biz Metrics

- MAU (Weixin and Wechat) 1.42b +2% ↗️🟡

- Mobile MAU QQ 508m -3% ↘️🟠

- Fee-based VAS Subscriptions 267m +2% ↗️🟡

- Time Spent (Mini Programs) +20% ↗️🟢

FY25 Earnings

- Rev ¥751.8b +14% ↗️🟡

- GP ¥422.6b +21% ↗️🟢 margin 56.2% +332 bps ✅

- Adj EBITDA ¥336.4b +21% ↗️🟢 margin 44.8% +280 bps ✅

- NG EBIT ¥280.7b +18% ↗️🟢 margin 37.3% +131 bps ✅

- EBIT ¥241.6b +16% ↗️🟢 margin 32.1% +61 bps ✅

- NG Net Inc ¥259.6b +17% ↗️🟢 margin 34.5% +81 bps ✅

- Net Inc ¥229.8b +17% ↗️🟢 margin 30.6% +81 bps ✅

- OCF ¥303.1b +17% ↗️🟢 margin 40.3% +108 bps ✅

- FCF ¥182.6b +16% ↗️🟢 margin 24.3% +45 bps ✅

FY25 Revenue by Segment

- VAS ¥369.3b +16% ↗️🟢

- VAS (Social Networks) ¥127.7b +5% ↗️🟡

- VAS (Domestic Games) ¥164.2b +18% ↗️🟢

- VAS (International Games) ¥77.4b +33% ↗️🟢

- Marketing Services ¥145b +19% ↗️🟢

- FinTech and Business Services ¥229.4b +8% ↗️🟡

- Others ¥8.1b +4% ↗️🟡

1 | VAS grew +14% dragged by slower growth in social network +3%, long-form video +1%, offset by faster growth in Music Subscription +13%, Domestic Games +15% (Delta Force, Valorant, and Wuthering Waves) and even faster growth in International Games +32% (Supercell, PUBG Mobile, and Wuthering Waves).

Value-added service revenue was CNY 90 billion renminbi, up 14% YoY. Our social network revenue grew 3% YoY to CNY 31 billion renminbi, driven by increased revenue from Video Accounts, live streaming, and from music subscriptions. Music subscription revenue increased 13% YoY on ARPU and subscriber growth. Long-form video subscription revenue increased 1% YoY as video subscribers grew slightly year-on-year, benefiting from the drama series Love's Ambition, the variety show Natural High: Season 3, and the animated series Renegade Immortal. Each of these ranked first by video views in their respective genres across all video platforms in China for the quarter. Domestic games revenue grew 15% YoY, primarily driven by Delta Force, the Valorant franchise, and Wuthering Waves. International games revenue increased 32% YoY, primarily driven by Supercell's titles, PUBG Mobile, and Wuthering Waves.

2 | Continue to strengthen Weixin’s commerce with Mini Shops and Mini Programs, saw user time spent grow +20%

Moving to communications and social networks, we strengthened Weixin's commerce experience by upgrading features for users and tools for merchants in the Mini Shops. The upgraded e-commerce gateway page allows users to check their shopping carts, see what friends are recommending, and receive notifications from their favorite shops, and generated substantial GMV during the quarter. Through the new Likes for Discounts feature, users can discover products liked by friends and receive and share discounts via the e-commerce gateway page, chats, and moments.

For Mini Programs, total user time spent increased over 20% year-on-year, driven by workplace productivity tools, mini-games, and novels. We added Tencent CodeBuddy to our developer toolkit, enabling developers to create mini-programs using natural language input, and we provided developers of AI native mini-programs with free compute resources.

3 | Marketing was strong, saw more time spent with Video Accounts, better conversion rates in Mini Shops, and more engagement in Mini Programs.

Entering 2026, we have deepened collaboration with e-commerce platforms, facilitating their merchants advertising within Tencent, and we've increased the inventory for rewarded video ads and Video Accounts, which have contributed to faster year-on-year marketing services revenue growth in the first quarter to date versus in the fourth quarter of last year. At a product level, Video Accounts total time spent increased due to upgrades to the content recommendation algorithm, enabling faster growth in ad impressions while our ad load remained lower than peers. Better conversion rates contributed to more marketing spending for Mini Shops merchants. For Mini Programs, consumers engaging more with mini-games and mini-dramas attracted more marketing spend from the mini-game and mini-drama studios. Weixin Search overall query volume grew at a rapid rate due to AI enhancements to search results, driving growth in commercial query volume, while search pricing also increased.

4 | Fintech remained robust driven by commercial payment and wealth management.

On fintech and business services, segment revenue was CNY 61 billion, up 8%. We grew fintech services revenue by a single-digit percentage year-over-year, and fintech gross profit at a higher rate driven by wealth management and commercial payment services. Commercial payment volume sustained positive year-on-year growth, supported by a higher number of transactions and a narrowed decline in value per transaction. For wealth management, which is the second biggest contributor to fintech revenue, average assets per user and number of users each increased year-on-year.

5 | Saw strong gross profit margin improvement across all business segments.

Overall gross margin was 56%, up 300bps YoY by segment. VAS gross margin was 60%, up 400bps YoY, primarily driven by greater contributions from internally developed high-margin games. Marketing services gross margin was 60%, up 200bps YoY as AI-powered marketing services drove strong growth in high-margin revenue streams, particularly Video Accounts and Weixin Search. Fintech and business services gross margin was 51%, up 400bps YoY,, benefiting from growing scale of cloud services and improved revenue mix in Fintech services alongside enhanced cost efficiency.

6 | Tencent’s franchises are resilient in the age of AI, have network effects, deep supply chain integration, stringent regulatory and licensing requirements, scarce or unique resources, sticky, and private data that is closed and interactive in nature.

First of all, I would like to talk about our key franchises are very resilient in the age of AI. As we know, AI will affect every part of the technology industry, but some products and services are inherently more resilient than others. We believe that some of the characteristics of resilience would include network effects arising from consumer to consumer to content creator, and consumer to business interactions in descending order of strength. That's number one. Number two, deep supply chain integration linking the worlds of bits with the world of atoms. Number three, stringent regulatory and licensing requirements. Number four, scarce or unique resources, including physical and intellectual properties. Number five, tick rates that are low compared to value provided or cost of switching. And number six, private data that is closed and interactive in nature.

7 | Thus see communication services as continuing to remain extremely sticky against non-AI services and resilient against AI-based services.

We believe this need for human interaction, together with the network effects and closed nature of the data arising from these interactions, have resulted in communication services being extremely sticky in the face of competing non-AI services in the past and will continue to be resilient versus AI-based services in the future.

8 | Network effects also apply to their multiplayer games.

Moving on to our games. They are also very resilient as our multiplayer games, especially PVP games, also enjoy network effects. Similar to sports, they are team-based in nature, and players play with and against other players. Just as people prefer to participate themselves or watch the teams they support compete in sports rather than watching AI sports, game players continue to enjoy the interaction with other humans that our games provide. Our games also cultivate strong IPs.

9 | While AI will enable more games to be made faster, the highest quality and the most innovative will be the best, with more time, more games will be played.

While AI will enable more games to be made faster, the game industry is already in a position of excess supply, with 200,000 new games on mobile and 18,000 new games released on Steam every year. The limiting factor is that new games need to be high quality and more innovative than the best existing games, which in turn requires human creativity on top of cutting-edge technology. Game is a natural beneficiary of AI proliferation, also when people have more time at hand.

10 | Fintech services are also resilient to AI as licenses are limited present barriers to entry, and the payment network with partner banks is hard to replicate, and they have the lowest mobile payment take rates in the world.

Our fintech services are also resilient as they depend on difficult to secure and retain licenses which are limited in nature and also set the boundary on how innovations can be introduced in an industry. We have also invested decades building a payment network of difficult to replicate rails into partner banks, merchants, and connecting them with more than 1 billion consumers, which brings its own network effects. Our mobile payment take rates are already among the lowest in the world, which we believe makes competing with us on price highly uneconomical.

11 | Using AI to accelerate in-game content production, and realistic game play, and with better content creation and ad targeting in marketing.

In games, we are deploying generative AI to accelerate in-game content production, enabling us to produce more content within our big games. We're using generative AI to facilitate new user acquisition and existing user retention through measures such as targeted ads and personalized daily highlight reels. We're enriching the core gameplay experience with AI features such as virtual teammates in PVP games and realistic non-player characters in PVE games

12 | Using AI In marketing to serve more relevant and better ads, create more ads to smaller subset of users more efficiently,, allowing marketing revenues to grow at 19% faster than 14% for the industry.

For marketing services, we scaled up our advertising foundation model to provide more relevant ads to more targeted users, boosting ad conversions for advertisers and providing better user experiences at the same time. We provide generative AI-powered ad creative solutions, enabling advertisers to create more ads which are more relevant to smaller set of users and more efficiently. We introduced our automated ad campaign solution, AiM Plus, under which advertisers can automate targeting, bidding, and placement, improving their return on marketing investments and increasing their budget allocation to us. These initiatives contributed substantially to Tencent's marketing services revenue growth of 19% in 2025, outstripping the overall China ad industry growth of 14%.

13 | Video Accounts is now the 2nd largest by DAU in China (after Douyin), and time spent grew by more than 20% in 2025, AI improving content production, distribution, and recommendation.

For Video Accounts, deploying a longer sequence AI model which captures more of a user's signals to enhance content recommendation is boosting user growth, engagement, and content distribution. Total time spent on Video Accounts increased more than 20% in 2025, and Video Accounts is now the second-largest short video service by DAU in China. For digital contents, we utilize AI in content production, improving production workflow efficiency, and providing visually compelling special effects. AI also helps in content distribution through more intelligent content recommendations across music, videos, and literature.

14 | Now using more AI in enterprise software like note-taking, and lightweight AI models to enhance credit-scoring processes and facilitate fraud detection.

We're using AI in enterprise software to provide features such as AI agents that can take notes on and summarize concurrent meetings for users, and AI agents that generate intelligent summaries of customer service history for merchants. Our enterprise software products, WeCom and Tencent Meeting, are leaders in their categories in China in terms of usage and revenue.

For Fintech, we utilize lightweight AI models to enhance credit scoring processes and facilitate fraud detection, contributing to us sustaining better than industry non-performing loan rates. Now that our core businesses are benefiting operationally and financially from integrating AI, we believe we are in a position of strength to add development of new AI products to our priorities.

15 | While Tencent was not a first-mover in LLMs, they are pushing hard with HunYuan 3.0, which is going to significantly better in capabilities and multi-modal.

Although we're not the first mover in large language models, having already revamped our team, improved our data quality, and rebuilt our AI infrastructure for pre-training and reinforcement learning, we're now iterating more intelligent models at a faster pace. HunYuan 3.0 is in internal testing and currently represents a bigger step in capabilities versus HunYuan 2.0 than 2.0 was versus 1.0. For multimodal capabilities, our 3D text-to-image and world models are early category leaders and will increasingly benefit from leveraging our proprietary data and abundant use cases.

16 | Don’t see AI chatbots as the only means to bring AI to users, as it can come through many ways, AI chatbots are largely competing with search rather than every other application, focusing on find PMF and use cases instead.

Some observers in Chinese tech are single-mindedly focused on AI chatbots as the only means for bringing AI to users. We believe this mindset is overly simplistic because AI can help people in a multitude of ways beyond powering an information advice app. We believe that AI chatbot applications are largely competing with search applications rather than with every other application. For Yuanbao, our own AI chatbot app, we're focused on finding product market fit and use cases which belong in chatbot AI app. We're rapidly iterating Yuanbao to enhance its user experience by providing better search integration, improved speech recognition, easier access to multimodal capabilities, and exploration around group chat, which we believe will increase usage and user retention of the app.

17 | OpenClaw allows AI to be decentralized not via a single point, the browser, or the chatbot, but now allows many companies to have their Claws with different models.

I think OpenClaw is actually a very exciting concept, right? You know, it actually sort of presents a decentralized model or a decentralized regime for, you know, how AI works in this world. You know, so there's some parallel to sort of how the internet evolves, right? You know, in the very beginning when internet first appears, right, you know, there seems to be sort of, you know, there is one entry point, which is the browser. You know, there is sort of one distribution point, which is the search engine. Over time, you know, it, you know, there are different services which evolve, right?

The chatbot being sort of, you know, the single entry point. Now with Claw, you can see, you know, it opens up a completely decentralized regime where, you know, many companies can have their own Claw, and the Claw can be using all kinds of different models, right?

18 | Excite with OpenClaw and see opportunities with personal agents, improving HunYuan will allow them to offer new unique agentic capabilities through Weixin and QQ

The excitement around OpenClaw illustrates that people recognize AI can unlock computer use capabilities to improve their daily lives but also illustrate the risks around unleashing unsupervised AI. We want AI agents in Weixin to deliver AI productivity that's beneficial to the general public as well as early adopters, and which will boost ecosystem activity and naturally generate revenue. AI agents are currently powered by a multiplicity of foundation models, and we expect that users at the application level will continue to have access to a range of models. However, improving the performance of HunYuan will enable us to offer new, unique to Weixin agentic capabilities.

Users control this new generation of AI tools through command line interfaces in their existing communication apps, which generally means Weixin and QQ in China, as it's the most efficient for users to interact with digital agents in a place and format where they are already interacting with human contacts. The new AI products that I described above require substantial and increasing investment, which we believe will generate significant return for us over the long run.

19 | Spent CNY 7bn and CNY 18bn on HunYuan and Yuanbao in 4Q25 and FY25, and expect to 2X these investments in 2026, and these exclude external GPUs via Tencent Cloud, and will be funded from earnings.

Our spending on our two biggest new AI products, HunYuan and Yuanbao, was CNY 7 billion in the fourth quarter of 2025 and CNY 18 billion for the full year. These figures are only for HunYuan and Yuanbao and exclude AI initiatives supporting our existing products and services, as well as exclude costs arising from providing GPUs to external customers via Tencent Cloud. We expect to more than double these investments in HunYuan, Yuanbao, and other new AI products in 2026, which we intend to fund from increasing earnings from our core businesses.

20 | Breaking out these investments, as they see them as upfront lumpy rather than ongoing recurring expenses and thus prefer to separate the reporting, confident of monetization of the usage from these new AI products.

In this transformational period, we are breaking out our investment in new AI products because we view these strategic investment conceptually similar to investment in an affiliate or to CapEx. These are upfront investments required to build the necessary foundation to unlock new value as opposed to ongoing operating expenses. As such, we believe the impact of these investments should be viewed separately from the profits generated by our existing businesses. Over time, we're confident that monetization will follow usage for these new AI products.

21 | Expects Tencent Cloud, which is #2 to follow games, payments, and long-form video to be #1, and similarly, its new AI products. Tencent Cloud’s choice to focus on high-quality rather than high-revenue, low-value-add activities has allowed it to achieve EBIT breakeven in 2024 and RMB 5bn EBIT profitable in FY25.

Lastly, I would like to present a case study on Tencent Cloud as the latest example on how we develop our services into market leaders with economic returns over time. That would follow games, payments, and long-form video. We expect it will be the same for our new AI products. Tencent Cloud was a relative late entrant in cloud services. However, we committed to a patient and long-term investment strategy, believing that it had scale from the start due to Tencent itself being the biggest single end user for a range of technology infrastructure in China, and that it could provide differentiated services arising from Tencent's unique insights, ecosystem, and capabilities.

After a period where Tencent Cloud prioritized the revenue growth somewhat misguided by other industry participants, in 2022, we aggressively restructured Tencent Cloud to focus on high-quality services rather than chasing high revenue but low-value-added activities such as reselling and customizing projects. This pivot cost us several quarters of revenue growth, but it enabled Tencent Cloud to achieve operating profit breakeven in 2024, up from significant losses in prior years. During 2025, although Tencent Cloud continued to face revenue headwinds due to limited availability of GPU for external customers as we prioritize our internal needs, it grew revenue and sharply improved earnings, achieving RMB 5 billion adjusted operating profit.

22 | Tencent Cloud is growing faster and higher compute will drive even faster revenue growth, initial losses were incubating the business that will generate strong profitability.

In recent months, we're seeing a better pricing environment, especially for memory and CPU, which, along with robust AI demand and overseas expansion, allowing Tencent Cloud to grow revenue at a faster rate. Moving through the year, we have ordered a substantially higher volume of compute, which should also facilitate revenue growth.

Overall, we think Tencent Cloud is becoming another example of how Tencent competes on our own terms and pace and how our incubation investment cycle works. We view the initial losses in Tencent Cloud as a fixed sum of cash investment necessary to incubate a successful new business, but ultimately generating good economic returns. We view the initial investment in new AI products, code-named MAP, in the same way.

23 | China Cloud Service Providers struggled historically with low margins because they can source directly, but now it is becoming a monopsony, where the suppliers are priortizing the biggest and most regular customers, the hyperscalers, and finally can raise prices and be profitable.

for years the industry has suffered because the cloud services providers in China were operating at very low margins. One of the reasons they operated at very low margins was because, you know, if there was a new entrant or if the customers wanted to source infrastructure directly, they were able to telephone the supplier and, you know, order the infrastructure that they wanted from the supplier of, you know, CPU or GPU or DRAM. You know, that's no longer the case. You know, now, the supply is booked out months, quarters, in some cases, years in advance. You know, the supplier is prioritizing the biggest, most regular customers, which are the hyperscalers such as ourselves.

Therefore, you know, the smaller cloud providers no longer have certainty that they can source supply, and they need to come to the hyperscalers. You know, the hyperscalers have been operating at low margins and so, you know, when the demand picks up, then, you know, we almost sort of as an industry have no choice but to pass through higher prices. You have seen a number of price increases in China cloud in the last 24 hours as a result. In terms of, you know, how we sort of value capture, you know, in this dynamic environment, then, you know, one broad principle is, you know, we seek to deliver, you know, more value through, you know, enrichment.

24 | Tencent chose not to focus on low-value, low-margin bare metal compute but higher-value, higher-margin compute instead.

Enrichment means that, you know, at a minimum, if you have, you know, compute, you can rent it out bare metal and you get a certain low price and low margin. You know, preferably you rent out. You subdivide it and virtualize it into tokens, and then you get a higher price and higher margin per unit of compute. Ideally, you bundle it into a platform as a service or software as a service. Then you can get, you know, the best pricing and the best margins. That's part of the journey that we've been on, and that's part of, you know, how Tencent Cloud has moved from a very substantial losses four years ago to pretty substantial profits last year. We'll continue on that journey of, you know, moving from bare metal to token to platformization and to software.

ROIC is one of the biggest drivers of quality factors.

But yet it is not just high ROIC alone that one should seek, but also if it can keep rising and stay high, and if there are sufficient opportunities to reinvest.

https://t.co/NA90CZ9ZTy

Nice chart shared by @ReneSellmann.

Chinese battery makers had 70% of the global EV battery market in 2025. South Korean battery makers are struggling to remain profitable.

Top 5 battery makers:

1. 🇨🇳 CATL 39.2%

2. 🇨🇳 BYD 16.4%

3. 🇰🇷 LG Energy 9.2%

4. 🇨🇳 CALB 5.3%

5. 🇨🇳 Gotion 4.5%

Chart: https://t.co/L9CeMrWycZ

Just published my latest deep dive:

Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React

Co-written with @the_zack_zhu after months of work. China is the clearest preview of what’s coming to Southeast Asia and understanding that dynamic is crucial.

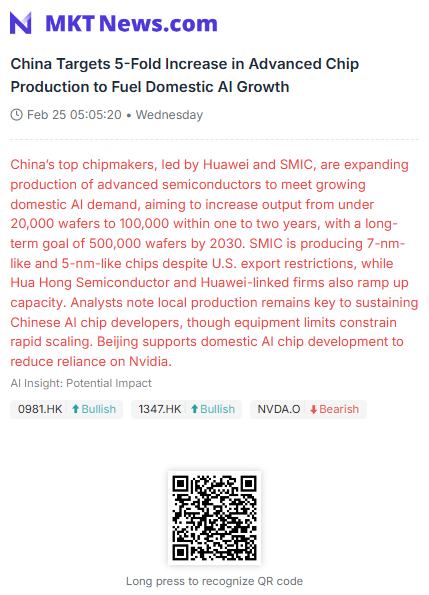

🇨🇳China Targets 5-Fold Increase in Advanced Chip Production to Fuel Domestic AI Growth

China’s top chipmakers, led by Huawei and SMIC, are expanding production of advanced semiconductors to meet growing domestic AI demand, aiming to increase output from under 20,000 wafers to 100,000 within one to two years, with a long-term goal of 500,000 wafers by 2030. SMIC is producing 7-nm-like and 5-nm-like chips despite U.S. export restrictions, while Hua Hong Semiconductor and Huawei-linked firms also ramp up capacity. Analysts note local production remains key to sustaining Chinese AI chip developers, though equipment limits constrain rapid scaling. Beijing supports domestic AI chip development to reduce reliance on Nvidia.

#CHINA #TECH #AI #SMIC #HUAWEI #NVIDIA $NVDA

(https://t.co/ND55ifaOP3)

The real growth for $PATH in the near term isn’t going to come from winning thousands of new clients. They already have 10,680 clients and 65% of the Fortune 500. Currently, NRR is at 108% meaning for every $100 a customer spent last year, they are spending $108 this year.

$PATH is boasting 98% gross retention as nobody is walking away from their core RPA bots. Once a company has PATH automating payroll, or other processes like invoices or claims, they become very sticky infrastructure. The next stage is upselling with Maestro.

Here’s the core thing to understand. Enterprises are now deploying many AI agents at once - think $MSFT CoPilot, Salesforce, $GOOGL Gemini, Open AI, Claude etc etc. This creates very challenging integrations.

There has been two new standards (MCP and A2A) which fix this chaotic integration and $PATH is one of the very few platforms to support both. What does this mean?

It means Maestro turns $PATH into the operating system that lets all of these 3rd party agents integrate with each other and hand off work to each other without endless code.

This means $PATH is not competing against these AI agents. They’re the layer that makes all of them together. It means the more $MSFT Copilot is used, or Gemini, the more $PATH is needed.

Few understand this.

This is the clearest map I've seen of how AI infrastructure constraints move in sequence. Every time one wall falls, another appears. I've watched this pattern since 2020: first it was "can we get enough GPUs," then "can we get HBM attached," now it's "can we plug it all in without melting the grid." By the time the market recognizes a bottleneck, the margin seems to have already moved.

"The future energy system, to my mind, can be defined by three words: distributed, intelligent, circular."

Dr. Robin Zeng spoke at the jointly held World Laureates Summit (WLS) & @WorldGovSummit (WGS), outlining how CATL is actively building the infrastructure to support this vision.

As distributed power systems expand globally, ensuring the stable operation of power systems becomes the new challenge. CATL has addressed this by developing innovative high-voltage grid-forming technology that acts as a stabilizer for zero-carbon energy systems. In China, CATL is applying this technology to build an off-grid industrial park powered entirely by wind, solar, and storage to supply a 40GWh battery plant, showcasing exactly how a net-zero power system operates at scale.

Beyond being distributed, future energy systems will be more intelligent. They will be able to handle vast amounts of data and adjust to fluctuations in renewable power generation and consumption.CATL is currently employing advanced AI-driven scheduling to balance supply and demand for SenseTime's AI Data Center in Shanghai, helping manage the fluctuating energy demand of computing tasks.

Finally, circular economy is crucial for achieving zero-carbon energy. Unlike fossil fuels, materials for zero-carbon systems can be recycled, and CATL is leading this effort with the highest recovery rates in the industry—99.6% for nickel and cobalt, and 96.5% for lithium. This capability is fundamental to securing a stable, sustainable supply of critical raw materials for the future.

#CATL #FutureEnergy #SmartGrid #CircularEconomy

3. $JD - JD,com

Among Chinese companies, JD remains one of the few major stocks that has yet to fully recover, but that may soon change.

JD operates China's largest self-owned logistics network, covering 99% of the population, with 90%+ of urban orders delivered within 24 hours. This unmatched fulfillment moat continues to anchor JD’s dominance in customer experience and reliability.

JD Health is scaling rapidly in telemedicine, AI-powered prescription management, and rare disease support, expanding well beyond traditional e-pharmacy.

JD Logistics global footprint now spans 130+ warehouses in 23 countries, with new hubs in the U.S., UK, France, and Saudi Arabia.

JD plans to onboard 1,000+ international brands into JD Super over the next three years, strengthening its global commerce strategy.

Despite these advancements, JD trades at near all-time-low NTM P/E levels, with a near all-time-high FCF yield, a rare combination signaling deep undervaluation relative to earnings potential.

Snowflake and OpenAI signed a multi-year $200M deal to run OpenAI models inside Snowflake’s data platform.

It lets teams build agents and analytics that stay close to governed enterprise data.

Before this, many enterprise LLM rollouts meant copying data into separate AI stacks, wiring custom retrieval, and then trying to bolt security and auditing back on.

This partnership puts OpenAI as a built-in model option inside Snowflake Cortex AI and Snowflake Intelligence, so model calls happen where the data already lives.

Snowflake says this lands across its 12,600+ customers, with examples like Canva and WHOOP planning to extend internal agents while keeping governance in place.

The next step is deeper workflow support using OpenAI’s Apps SDK, AgentKit, and APIs, plus Snowflake continuing to use ChatGPT Enterprise internally.

This looks most useful for teams that already standardized on Snowflake and want fewer moving parts between data, permissions, and model execution.

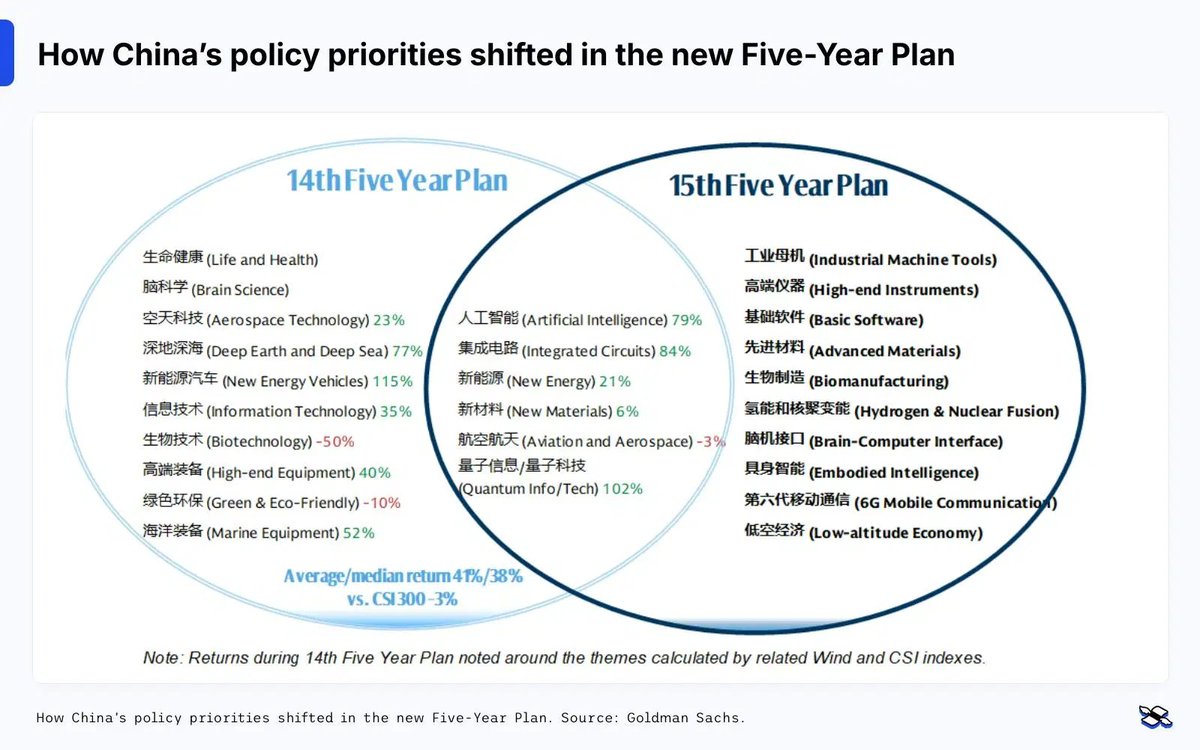

A good reminder of what is in China's 15th 5 Year Plan, which will be finalized in March 2026 (and how it differs from the 14th)

BTW color me very skeptical on low altitude economy but because it's there on the list & many cities want to take a crack at it