TODAY is the day. The DOJ must charge Fauci for lying under oath or lose the chance forever. This man oversaw gain-of-function research at the Wuhan lab, lied to Congress about it repeatedly, and watched as you were called crazy for asking questions. The statute of limitations expires tomorrow. The American people have waited long enough for accountability.

anyone else felt like @coffeebreak_YT is a plug and purposely got rinsed in that debate w/ @PunterJeff ? my guess is he is a massive $ASST & $MSTR shareholder.

Sat down with @coffeebreak_YT today on Bitcoin and Digital Credit.

His edit will drop soon. Posting the full raw hour for anyone who wants the unfiltered version.

Enjoy

Largest number ever quantum-factored: 21. Hardware gap to break ECC: 120x. Your Q-Day estimate shared by ~15% of experts. Adam Back says 20-40yr. Gidney (Google) says 10% by 2030. Every vendor roadmap revised backward. The '9 min' attack needs 500K qubits. Best today: 4,158. Debunked here https://t.co/R0uY9hOs9w

If Coinbase had never gone down the altcoin/gambling path I never would have started @River.

I can promise you this: we will never push gambling products on you or the people you care about. We're bringing Bitcoin Banking to your pocket, while Coinbase is bringing a casino.

COINBASE UPDATE- 18 OF MY CLOSE FAMILY AND FRIENDS HAVE TAKEN EVERYTHING OFF COINBASE AND WILL NEVER USE THIS COMPANY AGAIN!

ITS A START BUT IF EVERYONE DOES THE SAME WE MAY HURT THEM

RISE UP AND DO YOUR BEST TO SUPPORT YOUR SURVIVAL

Folks, we told you this was coming, and today the mask is fully off.

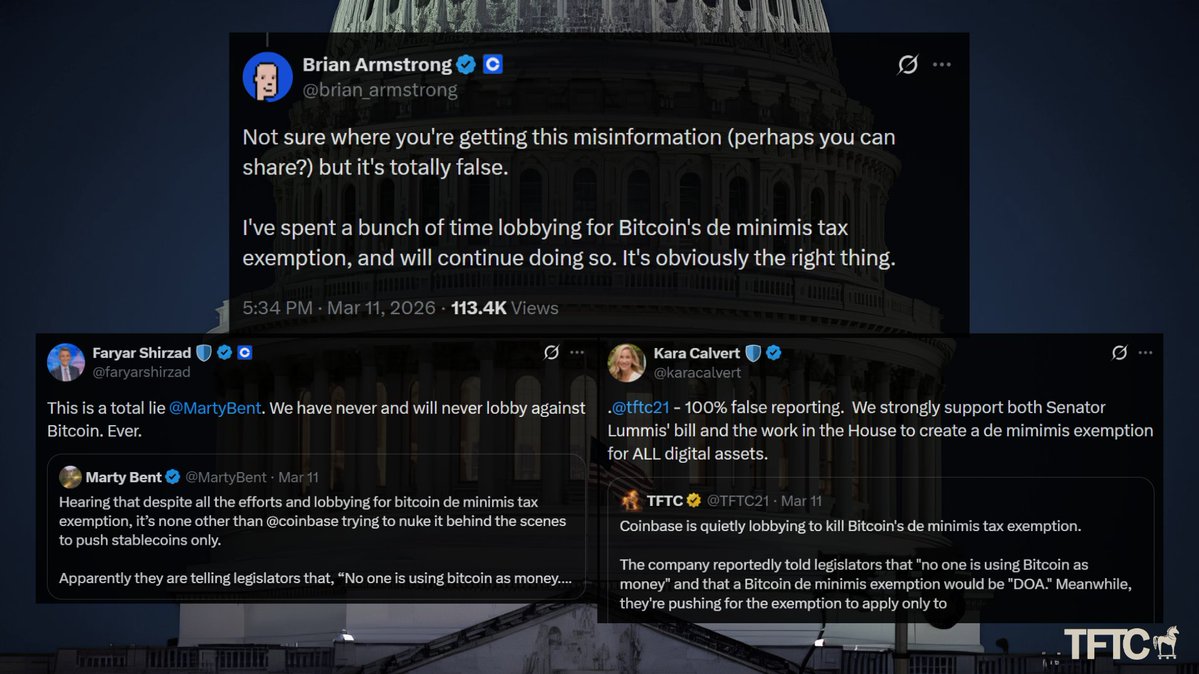

A couple weeks back we reported, based on solid sources, that Coinbase was quietly lobbying to kill a real de minimis tax exemption for Bitcoin while pushing one that applied only to stablecoins like USDC. We laid out the clear incentives in our deep dive. Coinbase made 1.35 billion dollars in stablecoin revenue last year, up 48 percent year over year, almost entirely from yield on the Treasuries backing USDC.

A proper Bitcoin de minimis would let people spend sats on everyday purchases without triggering taxable events on every transaction. That directly competes with their centralized yield machine. We called it what it was. Policy that protects Coinbase’s float rather than advancing neutral Bitcoin adoption.

Brian Armstrong pushed back hard. He called our reporting totally false and misinformation while insisting he was personally lobbying for Bitcoin de minimis. Some accused us of lying or spreading rumors. We stood firm. We offered to have Brian on the TFTC podcast to clear the air. We waited.

Now the latest draft from Reps. Horsford and Max Miller on the updated PARITY Act framework has dropped. It confirms exactly what we warned about. It gives a de minimis exemption to stablecoins but leaves Bitcoin out entirely. It keeps the punishing double taxation on Bitcoin mining fully intact while carving out relief for passive validation, basically staking. This is not an oversight or sloppy drafting. It abandons any pretense of technology neutrality and deliberately picks winners. Dollar-pegged stables and staking get the breaks, while actual Bitcoin usage as money and Proof-of-Work mining get kneecapped.

Without de minimis for Bitcoin, every small Lightning payment or sat transaction still forces cost-basis tracking and IRS headaches. Paying your plumber in sats or grabbing lunch with Bitcoin remains a taxable event. Stablecoins, being pegged and low-volatility, get an exemption they barely need. The real beneficiary is protecting that massive USDC reserve float and the yield it generates.

Meanwhile, American Bitcoin miners, already operating in one of the toughest, most capital- and energy-intensive industries, face continued double taxation while staking gets a pass. That is not neutral policy. It is industrial policy against domestic Bitcoin mining at a time when we should be leaning into energy abundance and securing the hardest monetary network.

The Bitcoin Policy Institute is releasing a full statement soon, and we fully back the call for strong community pushback. Every Bitcoiner needs to contact their reps and make it politically radioactive to sideline Bitcoin while handing carve-outs to stables and staking. This language slows real adoption, entrenches custodians, and weakens American Bitcoin infrastructure.

We weren’t lying. Our sources weren’t lying. The draft proves the reporting was on target. Those who rushed to call it misinformation owe the community some honest reflection.

Brian, if you’re still open to that conversation, the invitation stands. Come on the podcast. No spin, just walk us through how this draft lines up with your stated support for Bitcoin de minimis. The mic is warm.

This fight isn’t over. Bitcoin doesn’t need permission, but bad policy can delay sovereign adoption and punish the miners securing the network. We’re here to protect the protocol and the right of individuals to use sound money without turning every transaction into a compliance nightmare.

Stay sovereign. Stack sats. Use Bitcoin as money anyway. Call your reps today.

Breaking down our latest raise. Our single KPI is Bitcoin per share. Every capital decision we make gets measured against that. After our last institutional offering, we heard from shareholders that they wanted us to think differently about how we raise capital. The demand was still clear: more Bitcoin. So here's what we did.

Japanese PIPEs typically price at a ~10% discount to market. We sold shares at a 2% premium to market and packaged our equity vol into fixed-strike warrants at a 10% premium. The company gets immediate capital to grow the Bitcoin balance sheet. If the stock goes higher and warrants are exercised, we receive additional capital at a price above today's market. The investors get to express a view on volatility. This isn't zero-sum. Both sides can win.

This is the same playbook MSTR pioneered with convertible bonds. A 0% coupon convert was a bond and an embedded call option packaged into one security. The coupon was zero because the embedded option on a levered BTC vehicle was so valuable it replaced the coupon entirely. The bondholder wasn't lending for free. They were paying for vol. Saylor understood this before anyone else in BTC and it unlocked a new paradigm for Bitcoin treasury capital formation.

Same principle, different wrapper. We used stock plus warrants instead of converts, so there's no debt, no maturity risk, no overhang, no ongoing dividend or interest payments. The capital structure stays clean with no debt sitting above equity holders, and that's by design. When we issue preferred shares, the balance sheet underneath needs to be pristine. Every Bitcoin we add strengthens that foundation. The bigger the base, the more credible the credit. We are intentionally building this to become the dominant issuer of Bitcoin backed fixed income instruments in Japan.

And finally, we run one of the most active BTC derivatives books in the world. Every scenario here has been stress tested and is being managed, including the tail risk on future warrant exercise. We built this company around Bitcoin volatility and BTC Yield. This is what we do.

This is permanent capital with no ongoing cost. The proceeds go to Bitcoin. ~$255M now. Up to ~$531M on exercise. March toward 210,000 BTC continues.

Coinbase is quietly lobbying to kill Bitcoin's de minimis tax exemption.

The company reportedly told legislators that "no one is using Bitcoin as money" and that a Bitcoin de minimis exemption would be "DOA." Meanwhile, they're pushing for the exemption to apply only to stablecoins, specifically regulated, dollar-pegged stablecoins like USDC.

Coinbase made $1.35 billion in stablecoin revenue in 2025, up 48% year over year, almost entirely from interest earned on U.S. Treasuries held in USDC reserves. Bloomberg estimates that number could surge 7x under the GENIUS Act. Every person who uses USDC for payments instead of Bitcoin is a person whose dollars are sitting in Coinbase's reserve pool generating risk-free yield for Coinbase.

A de minimis exemption for Bitcoin would let people spend it freely for everyday purchases without triggering a taxable event. That makes Bitcoin a direct competitor to USDC as a payment method. Coinbase doesn't want that competition. They want you locked into their centralized stablecoin ecosystem where they clip yield on every dollar you park there.

The irony is that a de minimis exemption doesn't even make sense for stablecoins. They're pegged to the dollar. They don't fluctuate in value. There's no capital gain to exempt. The exemption matters for Bitcoin precisely because it does fluctuate, and without it, every coffee purchase becomes a taxable event.

Senator Lummis proposed a $300 de minimis exemption that would cover Bitcoin. The House framework only covers stablecoins under $200. The Bitcoin Policy Institute has already warned that Bitcoin is being deliberately excluded from these talks.

A de minimis exemption that covers stablecoins but not Bitcoin isn't a tax framework. It's a subsidy for Coinbase's treasury management business disguised as consumer protection.