So - both $MSFT and $META are at 52-53x P/FCF

If you're forced into the following trade for the next 12 months do you go:

(Please re-tweet for visibility)

Usually a lurker on here but dipping my toes briefly into the "k-shaped economy" discourse.

At PNC we track the debit & credit spending trends of a fixed cohort of ~4 million households.

Long story short: lower-income spending/balance sheet trends have been on a tear in 2026

@evrgn11112231 SaaS companies disrupting each other. If 2023 engineers were enough to maintain competitive intensity and 2026 = same engineers * 130% productivity gain. Then the investment across the board is a higher level of intensity (equivalent to mfg opening new lines simultaneously)

The frontier model problem is a breadth versus depth problem. Consumer needs breadth, the wider your aperture, the more relevant your model. Breadth suffers from a false positive problem, it ranges between 10-30%, with clever prompting and checks you can hit the lower end of the range, but it tends to be free or subsidized. Consumers still seemm to be satisfied, and consumption growing!

However, Frontier Models harvest the usage data to inform future models.

On the other hand. The enterprise wants depth, their tolerance for error is low, this needs more context data, training and harnesses and guardrails is high. The frontier models aren't ready yet to provide that, hence the FDEs, and solutions consultants who build that capacity for every enterprise. But enterprise is the only route ATM to build a sustainable economic model.

The risk, consumer losses mount. Enterprise value accrues to solution providers. In the meanwhile, models are aggressively pursuing Enterprise profit pools, while solution providers are building orchestrators to arbitrage token pricing. So there's many a push and a pull in the equation.

If will be an epic battle, my instinct tells me, value could accrue to the application and proprietary data layers.

Will be fun to watch.

The brilliant Eric @bonabeau creates a scenario engine for the IPOs of SpaceX, OpenAI, and Anthropic. He combines fast-entry index inclusion demand, pro-rata funding sales from existing constituents, discretionary retail rotation out of incumbent equities, and lock-up-driven supply releases. The engine allows you to tune the parameters. No answers but a lot to think about. Full paper in tab at the top right: https://t.co/d9FthtAj1C

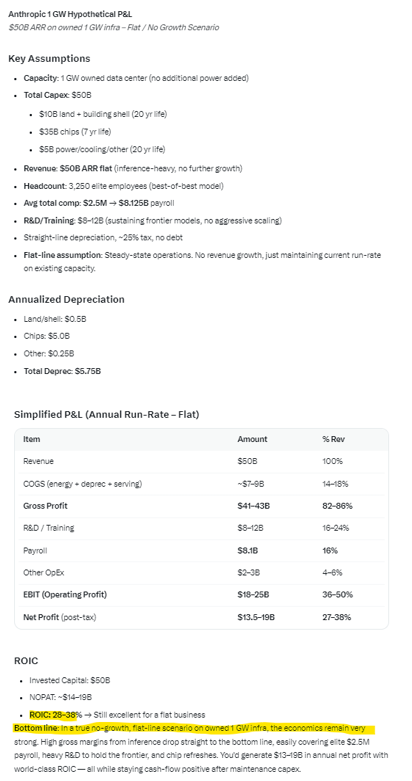

Anthropic is currently like ~$50B ARR on an estimated 1GW, which Jensen says is $50B (shell, cooling, chips, etc).

If you assume for a second that Anthropic decides not grow and just runs at ~$50B ARR (an exercise to just sanity check ROIC), the math looks quite good. 25%+ ROIC?

Assumptions below. Where are my assumptions off? Maybe comp ($2.5M per employee?)?

@GavinSBaker@chamath@DavidSacks@friedberg

@blueprintsmb22 The gap between what people know about company monitoring vs what happens is crazy.

I know for a fact that many accounting firms had monitoring down to a screenshot every minute running in the background with productivity reports given to management weekly.

@SowingAlphaSeed Why do you think about it that way? Why isn't it being gleeful that resources are being reallocated to performant research rather than a wrong path?

Would you say that shorting a promising biotech that could help millions is wrong if you don't believe in their approach?

Seeking out the narrative violation has always sharpened thinking. It matters more than ever now: where social media once amplified consensus (2013–2023), LLMs now ossify it, averaging the web into a single agreeable voice

https://t.co/4j0nJYDQyI

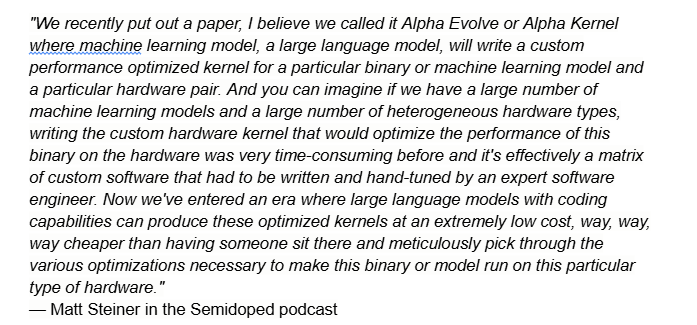

I think Huawei, Deepseek, and at least a few of the other tigers are working hard to not only adjust kernels but even their model architecture to inference on ascend. But this isn't short term economical hence the USA players will not go down that path is my point.

China is lost to NVIDIA as an inference market is my base case.

Opposing take: Can port and should are not the same

1) CUDA is also improving at AI speeds getting more performance with every release

2) if it was easy to do so economically then more Chinese players than just deepseek would have ported to Huawei by now

The biggest irony in AI right now is that $NVDA basically enabled the AI boom, and now vibecoding in diminishing the moat around CUDA.

@semidoped had an interview with $META's head of ad infra who talked about LLMs rewriting their kernels so that the same models run across GPUs, ASICs, etc. The main advantage of cuda was that it was so much easier to optimize your model to Nvidia's hardware.

Still think cuda is excellent and has a deeper base, but writing on the wall is in? Jensen mostly talks about TCO these days as their moat.

@ShanuMathew93 Snowflake already showed what it takes. Revenue acceleration, material update to guide. A path that shows how more AI usage/software is clearly a good thing.

@JerryCap -ve because he feels like there is an easy off ramp to overspending so no hesitation not to

-ve because if they ever do this it means he has lost faith in his team to build useful agents

@Nd172557208 I wholly agree with you on OAI/anth

SpaceX feels like a different beast, the conglomerate of a social website, with a rocket company and a neocloud is just 🙃