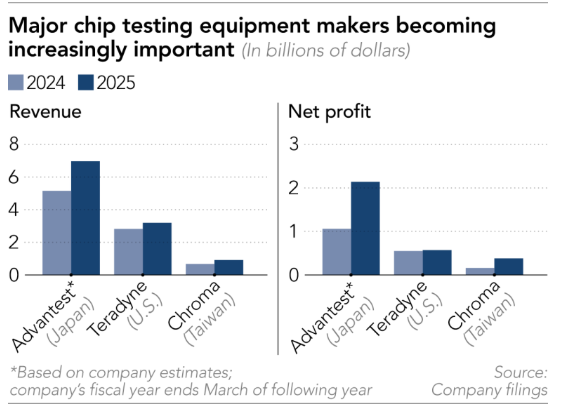

AI chip testing is shaping up as the next bottleneck in the supply chain.

Nikkei reports an AI chip can take more than 10 minutes to test, versus under a minute for a phone processor, and many now require 100% testing across multiple stages.

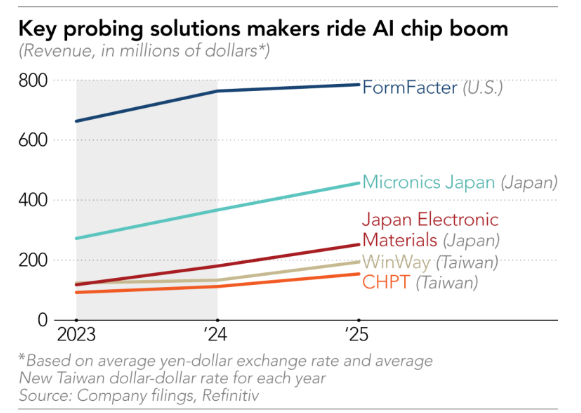

That is driving a sharp revenue ramp for probing and test names like FormFactor, Micronics Japan, JEM, WinWay, and CHPT.

Trade idea that I published to my shower thoughts channel:

Korean Index volatility arbitrage and taking advantage of Black-Scholes models.

$EWY long options seem mispriced.

This is Blackrock's Korea Index, which is majority memory (Samsung Electronics, Sk Hynix).

The stock swings 2-5+% a day, and is up 136.25% 1Y, despite priced like a normal index IV.

Samsung is volatile. SK Hynix is volatile (eg. 65% - 80% est).

But the combination of the two through the index is priced way less than both low beta $GOOGL (37.33%) and $AMZN (39.12%) at ~32% IV.

I've been watching $EWY for a bit and it does look volatile.

As for pricing my guess is MMs priced in IV based on historical averages (5-10 years), where the Korean index was completely flat. And were expecting calls 2 years out to revert to the mean.

But this volatility should be the new norm as markets price in the new memory supercycle (eg. $TSM went from 30% IV to 46.2% IV).

Long calls should benefit from both Samsung + Sk Hynix carrying the index.

And the main benefit is vega expansion that you won't get from $KORU.

You also can't get this option MM pinning like individual US stocks since this is Korea's national index and long term.

TLDR: Individual components SK Hynix + Samsung are highly volatile.

They're basically half of the index, but options in index are priced with low volatility, perhaps due to historical 5-10 year data.

Long calls benefit from vega expansion that weren't priced in correctly as MM forward vol estimates are anchored too heavily on historical realized vol, which was low for $EWY over the past 5-10 years