Trend-Following Spreads (S7E25) with @moritzseibert and @moritzheiden.

A few years ago, I sat down with Moritz Seibert and Moritz Heiden of Takahe Capital to talk about trend following at the edges of the futures markets: places where liquidity is thin, contracts are obscure, and capacity constraint is a feature, not a bug.

Since then, despite strong performance, asset growth, and even winning industry awards, they made a very un-industry decision: they shut down their original fund.

In its place, they launched a new Global Markets Fund built to stay small, so they can trade calendar and product spreads, niche agricultural markets, and other idiosyncratic contracts at equal risk to more standard markets.

In this conversation, we unpack that decision, explore how you systematize trend on markets where liquidity does not exist on screen, and go deep on why spreads represent a fundamentally different opportunity set than outright futures.

We also talk about what’s next: from prediction and event markets to new ways of thinking about macro trends and alternative data.

I hope you enjoy my conversation with Moritz Seibert and Moritz Heiden.

BCOM and GSCI Commodity Index Rebalancing starts today. SG estimated AuM is $92 bn for BCOM and $55 bn for GSCI, so not nothing.

After massive 2025 rallies, Gold & Silver face billions in forced selling as passive funds reset their weights.

Where does that capital go? Expect rotation inflows into Energy (Brent, WTI) and Softs (Sugar, Cocoa).

Structural flows vs. The Trend. Watch the roll.

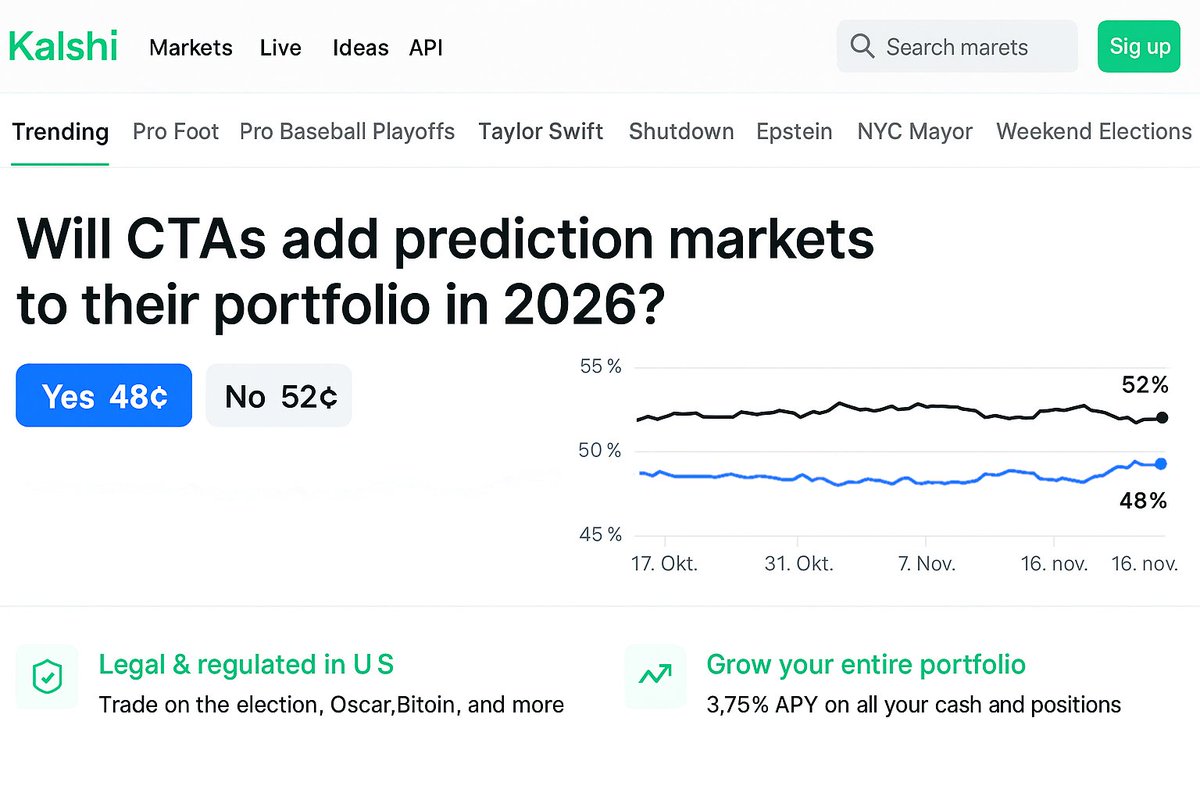

Kalshi is offering contracts on everything from the NYC mayoral debate to the Oscars.

Meanwhile, some CTAs already trade 500+ markets.

What’s a few more?

We’re honoured to share that the @TakaheCapital Global Quantitative Fund has been shortlisted for the 2025 With Intelligence HFM European Performance Awards — in the “Newcomer – Managed Futures / Macro” category.

The Global Quantitative Fund brings together systematic trend following and spread trading — two strategies we believe complement each other especially well in today’s market environment.

A big thank you to our investors, partners, and the team for making this possible.

When it comes to booking a very expensive table for an award ceremony, one of my favourite quotes by Homer Simpson comes to mind:

"Sure, I'm flattered, maybe even a little curious, but the answer is no."

In that spirit - see you on the trading floor, where we belong and thrive.

Last week, @schroedingersai hesitated on Gold (bad cat)

This week, it’s Energy’s turn to shine.

XLE just turned Alive as the cat’s analogues picked up the surge in AI-driven power demand.

Meanwhile, Bitcoin’s stirring. Alive again, but the real rally looks 10–12 weeks out.

The next phase of the cycle runs on both electricity and belief.

Link to article in comments

We named our fund @TakaheCapital after a bird that “went to zero” twice… and still made the mother of all comebacks in 1948.

If you want a ticker for our ethos, it’s not $HYPE (even though I like that one, but that’s a crypto story). It’s survival first, compounding second.

NZ birds have a strange habit: vanish for decades, reappear when no one’s looking. Markets do the same. Trends die, eulogies are written… and then they stroll back on stage once the last PM pulls the plug.

Case in point: the night parrot in Australia. Assumed extinct for 100 years, now rediscovered. One of its calls literally goes: “didly dip, didly dip.”

If that isn’t the soundtrack of mean-reversion pain, I don’t know what is.

Trend following moral: we don’t predict which species (or trends) will reappear.

Well… we do, in our macro trend models at @schroedingersai. But not in the fund.

In the fund it’s simple: diversify habitats, control fire risk (position sizing), keep the cats out (left-tail protection), and let the winners breed (let profits run).

And yes, we’re very glad we chose the Takahē and not the night parrot. “Didly dip” is a rough brand promise in a drawdown.

Our brand promise: be hard to kill, in life and in markets.

(Also: we have the cutest Takahē stickers. Resilience looks even better on a laptop.)

AQR showed that macro trend signals can work.

I took the idea further with an analogue engine I called Schrödinger’s AI.

Instead of fixed heuristics, it asks: “When markets looked like this in the past, what happened next?”

Each week, markets get classified Alive 🔵 or Dead ⚫

And yes, Schrödinger is currently very into Bitcoin & Silver

Link to article below

Trading isn’t for the faint-hearted, and few know this better than Bill Eckhardt. With decades in the markets and a legacy built on resilience, he’s shares with @moritzseibert what he has learned — wisdom only earned through years of experience.

https://t.co/sinmKlCSCh

Bill Eckhardt, co-creator of the famed Turtle Trading experiment with Richard Dennis, makes his first-ever podcast appearance!

Join @moritzseibert for a rare conversation with this trading legend.

Tune in now!

https://t.co/sinmKlCSCh

"Trend following often leads you to places that feel very uncomfortable. It's got a really weird payoff scheme. It works, but it’s psychologically incredibly difficult. The challenge can often be psychological and discipline as much as anything else in terms of implementing." @MebFaber@mjmauboussin

https://t.co/Ci5kqMD1ad

Don't miss this episode featuring @ColeWilcoxCIO, Founder and CIO of @longboardfunds. He spoke to @moritzseibert about his firm's approach to optimizing equity investing through trend following - and applying it to single stocks, rather than equity indices. Tune in!

@thetradler@ArturSepp@investingidiocy @rjparkerjr09 Questionable regulation and embezzlement, eg. FTX. Crypto managers usually don't keep their collateral on the crypto exchanges at all times to manage that risk.

#CTA traders, if you added #Bitcoin to your tradable universe, did you go for

1) CME big contract (*5 #BTC)

2) CME mini (*0.1)

3) Perp on a Crypto CEX

Problems:

1,2) Liquidity/spreads are not great

3) Is not feasible for inst accounts

@investingidiocy@twoquants @rjparkerjr09

"I had a thought: The equity line is like nature (Brownian motion.) Attempting to control nature is to suppress nature. Classic trend following does not try to control nature. It tries to capture nature. The equity line will take care of itself, it will do, whatever it will do." - Jarad