Do not read Jensen Huang’s visit to Korea as just another news event.

Inside this visit are important investment insights into how NVIDIA is advancing robotics, factories, and the AI feedback loop in Korea.

Read @PhotonCap's insightful article right now.

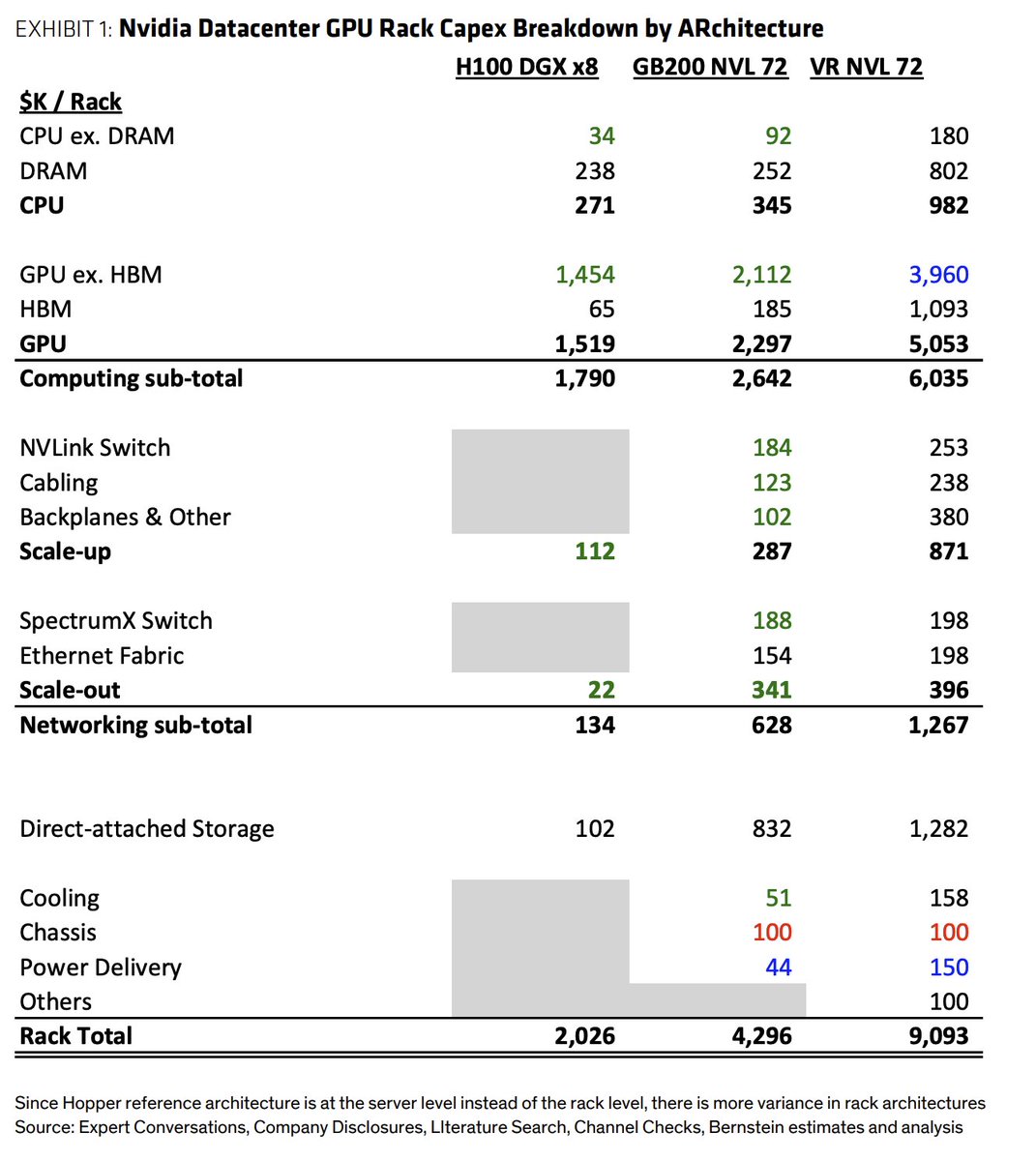

Bernstein: "We estimate that a typical VR / NVL72 rack costs ~$9.1M per rack. This estimate is notably higher than the ~$8M figure reported in the media, which appears to be based on stale memory prices."

"We estimate all-in AI data center capex of ~$47B per GW" $NVDA

NVIDIA CEO Jensen Huang:

"Every company in the world today needs to have an agentic system strategy. This is the new computer."

In 2 hours he breaks down the architecture under every working AI agent and the difference between chatbots that talk and agents that actually do the work.

Watch the full talk, then grab the exact setup below👇

SOFTWARE IS DEAD: "The software companies frankly got fat & happy. I think what will happen over time is ChatGPT & Claude will end up sitting on top of basically the entire enterprise software stack & almost everything else will end up being a dumb data pipe into those two."

Fascinating conversation this week with Dominic Rizzo, who manages the $8.7bn Global Technology Fund at @TRowePrice, which has returned 44% PER YEAR since he took over Dec 2022. He has been super bullish AI & has the performance to match, & explains why he is confident the AI capex cycle continues, not least following $GOOG capital raise last week.

BULLISH: "Electricity added roughly 1% to global GDP growth every year for 32 years. I think AI is already smashing that. And the question people always ask me, have we overspent yet? I don't think we've overspent yet."

COMPUTE WINS: "We've learned time & time again - compute equals revenue. I'm going to say it again it's so important. Compute equals revenue. Compute equals revenue."

NVIDIA KING: "So is $NVDA still the king? Yes, is the answer pretty unequivocally. Jensen's really brilliant and he knows how to bring the symphony together of all the different pieces." Also very bullish on $AMD & $INTC. Memory NOT commoditised $MU #Samsung #SKHynix

Timestamps:

0:00 Intro

3:00 Great performance & good timing

6:29 AI - we haven’t overspent yet

09:28 Impact of agentic computing

11:47 Four part framework for picking stocks

14:34 Software companies got fat & happy

17:01 Can $MSFT $CRM adapt? No.

22:05 Why $NVDA is still the King. $AMD $INTC too.

27:59 $ARM figured out low power CPU processing

30:56 Memory is the hardest “commodity” in world to make

35:00 Technical market factors – ETFs & IPOs

36:30 $GOOGL capital raise signals capex boom continues

38:40 Compute equals revenue

41:43 Why leading intelligence beats cheap

45:13 Is $AAPL vulnerable?

47:22 Upcoming mega IPOs

52:11 Pressure on broader mkts from insanely large IPOs

54:12 Valuations overall

56:00 Concluding investment advice

Goldman may have just made one of the more important "second-order AI" calls I've seen recently.

It´s not about GPU or CPU ... It's about wafers - specifically, 300mm wafers.

Goldman believes 300mm wafers have entered a multi-year growth cycle driven by AI. AI servers already account for more than 20% of wafer demand, while GPU/ASIC deployments, HBM scaling, CoWoS, silicon photonics, and the rise of agentic AI are increasing semiconductor content across entire systems - not just accelerators. At the same time, next-generation memory architectures such as CBA NAND, 400+ layer NAND, and eventually 3D DRAM could further increase wafer consumption per bit shipped. With supply growth slowing while demand continues to broaden, Goldman sees the setup becoming increasingly supportive for wafer pricing and profitability.

Goldman thinks the industry is moving away from the traditional "shrink more, use fewer wafers" model.

Instead, advanced packaging, stacking, bonding and AI system complexity are causing wafer consumption per unit to rise.

That's a subtle but potentially huge shift.

Potential beneficiaries:

(++) SUMCO (https://t.co/oAG6VEG9h8) – largest estimate increase in the report

(++) Shin-Etsu (https://t.co/l2RQM6lVdz) – stronger 300mm wafer pricing assumptions

(++) Resonac (https://t.co/vZ7iWq6ifB) – AI packaging materials outperforming expectations

(+) Mitsubishi Gas Chemical (https://t.co/0fCEqM6q0k) – BT substrates and AI server materials

(+) Mitsui Kinzoku (https://t.co/OT8gj11OYW) – copper foil increasingly tied to package substrates

10 stocks I will be watching going into the SpaceX IPO next week:

1. $STM - STMicroelectronics

The most direct SpaceX supply chain play you can buy. STM's BiCMOS chips power every Starlink phased-array antenna across 10,000+ satellites and millions of user terminals. Decade-long partnership. Close to 90% market share in LEO satellite semiconductors. Space revenue targeting $1B in 2026, with $3B+ cumulative from 2026 through 2028. Revenue up 23% YoY.

Semiconductor Laser Annealing Gains Broader Adoption… Push Underway for SiC and 400 Layer NAND

Demand for annealing, one of the heat treatment steps in semiconductor manufacturing, is expanding. The process, traditionally used mainly on silicon (Si) wafers, is spreading to silicon carbide (SiC), regarded as a next generation power semiconductor material. Annealing is also expected to see wider use in next generation memory such as NAND with 400 or more layers, as well as in advanced system semiconductors.

According to industry sources on the 3rd, Wolfspeed, the top player in the SiC wafer market, has recently been moving to adopt laser annealing equipment. It is understood to be negotiating a purchase order (PO) with a domestic laser annealing equipment partner. The expectation is that it will start with a small initial volume and then increase the applied quantity.

An industry official said, “Full scale introduction and adoption have now begun in the SiC wafer process, where annealing had seen little use until now,” adding that “the transition of SiC wafer sizes to 8 inches and above is also a positive for the use of annealing equipment.”

Semiconductor annealing is used to apply a set temperature to a wafer in order to repair lattice damage and to activate implanted dopants, thereby enabling the desired electrical characteristics. It is generally classified as a step that follows ion implantation.

While annealing has been widely adopted for silicon, the mainstream wafer material, its use in SiC has been limited. This is because SiC requires higher temperatures (above 1,600 degrees) compared with roughly 1,000 degrees for Si. Interfacial damage at the wafer surface and defect formation were also reasons that made annealing difficult to apply.

More recently, the ability to perform annealing on very narrow, specific regions or within extremely short timeframes using lasers has reduced the thermal burden, raising the feasibility of SiC application. Beyond Wolfspeed, Samsung Electronics, which is preparing a SiC contract manufacturing (foundry) business targeting mass production in 2028, is also known to be reviewing the adoption of laser annealing.

As SiC draws attention amid expanding demand for power semiconductors, the annealing process is expected to spread alongside it. SiC is a compound semiconductor material with superior heat and durability characteristics relative to silicon, and is in the spotlight as a next generation power semiconductor.

Annealing is also expected to expand in next generation memory and advanced system semiconductors. NAND flash with 400 or more layers is a leading example. Raising NAND performance and capacity requires increasing the layer count. Manufacturers then etch the “channel hole,” the signal path between vertically stacked memory cells, and the higher the layer count, the deeper the channel hole becomes, making it harder to secure electrical characteristics and structural stability.

Annealing is drawing attention as a methodology to solve these problems by crystallizing the channel hole region. Some NAND makers are in fact said to be pursuing annealing for the localized crystallization needed to realize NAND with 400 or more layers.

Another industry official said, “There are continuing attempts across the industry to apply localized annealing to advanced system semiconductor manufacturing processes at 2 nanometers (㎚) and below,” adding that “the spread of the annealing process will contribute to growth in the laser solutions market.”

A strong example of innovation emerging from the ASML ecosystem in the Netherlands.

Invisix, the deep-tech spinout advancing semiconductor metrology, has just raised an oversubscribed €20 million seed round. The funding comes from Hitachi Ventures, Transition Ventures, imec.xpand, Doosan Investment Co., and a tier-1 semiconductor manufacturer.

Invisix’s systems push metrology into the soft X-ray regime, using wavelengths matched to nanoscale features in advanced devices such as Gate-All-Around transistors and Complementary Field-Effect Transistors. While visible light metrology struggles with buried structures in complex 3D-stacked chips—often requiring slower or destructive methods—Invisix offers non-destructive, high-throughput solutions well suited for high-volume manufacturing.

You've been watching football wrong your entire life.

This 40-minute Databricks talk on how LaLiga uses data is the proof.

The goals and assists you obsess over are the least interesting numbers on the pitch.

By fusing tracking data (every player's position, many times a second) with eventing data (every action on the ball), LaLiga measures the invisible game space created, defensive lines pulled apart, the value of a run nobody passed to.

The best player in a match is often the one who never touched the scoresheet.

Pair it with article by Roan and you are good.

Once you see the game as data, you can't unsee it.

🚨 BREAKING: Google Gemini can now analyze any stock like a Wall Street analyst (for free).

Here are 14 insane Gemini prompts that replace $4,000/month Bloomberg terminals:

(Save this 🔖 you’ll need it later)

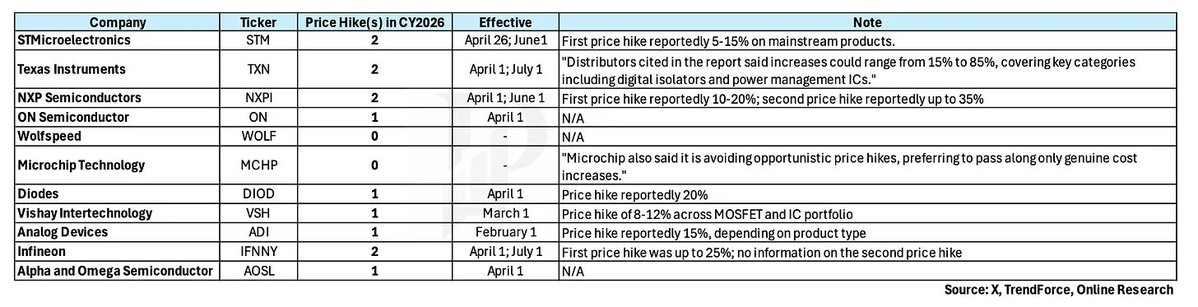

Summary of power semiconductor price hikes in CY26:

STMicroelectronics $STM - April 26; June1

Texas Instruments $TXN - April 1; July 1

NXP Semiconductors $NXPI - April 1; June 1

ON Semiconductor $ON - April 1

Wolfspeed $WOLF

Microchip Technology $MCHP

Diodes $DIOD - April 1

Vishay Intertechnology $VSH - March 1

Analog Devices $ADI - February 1

Infineon $IFNNY - April 1; July 1

Alpha and Omega Semiconductor $AOSL - April 1

4 price hikes on the way in June and July.

Mitchell Green is the co-founder and managing partner of Lead Edge Capital, a $9B growth equity firm he founded in 2011.

For 15 years, he and his partners have built one of the most disciplined investment machines in the business, designed to deliver consistent returns by hitting doubles and triples rather than chasing power law outcomes. He obsesses over avoiding zeros and is constantly underwriting investments to know exactly when to sell.

He has built a unique culture at Lead Edge, sending handwritten thank you notes to nearly everyone he meets and sitting down one on one with every person at the firm once a year.

He is, by his own admission, one of the most persistent and competitive people you will meet. After the episode, he told me he believes the most important thing in life is to be memorable. You will find, listening to this conversation, that he very much is.

We discuss:

- Why it’s the best time to buy public software companies

- Lessons from 10,000 cold calls

- His unique LP base

- Why consistency of returns matters more than home runs

- The art of knowing when to sell

- How culture is built from the top + the importance of follow-through

- What skiing taught him about risk and competition

Enjoy!

Timestamps:

0:00 Intro

1:00 The Hierarchy of BS

2:20 Lessons From 10,000 Cold Calls

9:05 Base Hits vs. Grand Slams

15:24 The 8 Buying Criteria

17:24 Pricing and the AI Exit Multiple Trap

19:24 Software as a Game of Distribution

23:20 Creative Deal Structuring

26:27 The Framework for Focus

29:01 The Art of the Investigative Cold Call

34:24 Culture of Hustle

35:34 The Annual One-on-One Process

37:59 Playing to Strengths

39:43 The Mount Rushmore of Investment Machines

42:05 Fears and Excitement Around AI

48:54 Ski Racing

52:29 Advice for Starting a Firm

54:35 The Kindest Thing

⚡ Skills mean nothing if you do them in slow motion.

As Lee says in the clip, use the move, then explode. Sell the feint, react, and burst into space.

Train it here ➡️ https://t.co/WkUfNlQW9U

Some crude AI TAM analysis:

- It was recently reported that $CRM is on track to spend ~$300M on Anthropic this year. That works out to ~$300/mo per employee

- A GitHub copilot customer I spoke to was quoted a 10x price increase in June ($300/mo)

- I myself happen to spend ~$300/mo in AI subscriptions

- Let’s use $300/mo as a proxy for decent penetration of AI into a knowledge workforce.

$MSFT 365 has ~450M users, $GOOG Workspace has a similar number (est., not disclosed). That’s a decent proxy for global knowledge workers ex-China at ~900M.

If every knowledge worker consumed $300/mo of tokens, that’s a $270B monthly or $3.24T annually. Would equate to ~5-6% of global white collar labor spend ($50T).

On consumer side: if every GOOG/META DAU consumed ~$20/mo of tokens, it would be ~3B * $20/mo * 12 = ~$720B. GOOG/META could basically fully subsidize this with their existing business models within a few years. Let’s assume $20/mo of tokens is covered some mix of ads, subscriptions, commerce share, and subsidization.

Combining the TAMs we get to ~$4T of token spend. Keeping to simple numbers, at ~50% gross margins, it would sustainably require ~$2T of infrastructure spend to support these tokens. That would be ~2x the 2026 rate of ~$1T of AI infra spend ex-China.

So from there:

- Is enterprise token spend too high or too low? Could argue token consumption will only grow for CRM, but also that cost per token will fall, and the avg company won’t consume that much.

- Is consumer token consumption too high or too low? Maybe consumers will be more willing to spend on subscriptions for this than in past consumer tech cycles. Maybe it’s too high if ai models don’t monetize.

But at least $300/mo per user for enterprise and $20/mo for consumer are tangible numbers I can get my head around. That feels like the bogey for infra cycle to have another double from here and not be a huge bubble, and probably need another double at least for the stocks to work.

Very crude round numbers throughout here. Appreciate thoughts and pushback.

Cloudflare CEO Prince on how AI changes who gets laid off first:

Two weeks ago I laid off more than 20% of my workforce. I didn’t do it because Cloudflare is struggling. We posted record revenue growth, have strong free cash flow and are adding an unprecedented number of customers around the world. I did it because business is changing, and to win the future, Cloudflare needs to change with it.

We haven’t found another example in U.S. business history of a public company growing at more than 30% that laid off more than 20% of its workforce. Yet what we did is likely going to become the norm over the next year. This is a story about artificial intelligence, but executives and commentators are misunderstanding how it will disrupt business and who will be affected.

AI isn’t coming for builders or sellers, but it is coming for measurers. Tireless, independent, efficient and available, AI systems can now measure an organization with a level of objective detail and precision that was previously impossible even for the best employees.

For Cloudflare, internal audit previously picked a handful of business risk areas to scrutinize each quarter. Now we’re moving to a system in which every business risk is audited continuously. We’re closing our books faster. We’re making fewer mistakes and catching the ones we do more reliably. And, as CEO, I’ve never had better tools to measure exactly how the business is performing, including identifying our rising stars.

The vast majority of those we laid off last week were measurers. We cut middle managers across the organization because AI allows us to have more direct reports per manager while still measuring and mentoring our teams effectively.

We consolidated our operations functions into a single group that can support teams across the business, using AI to gain specific expertise when needed. We significantly reduced our marketing team, which, like in most companies, was teeming with measurers. Across our finance team, we found opportunities to consolidate and automate.

We received almost a million applicants for 1,111 paid internships this summer. The interns we hired are extremely qualified and AI-native. They’re all builders or sellers, and we expect that the majority will get full-time offers.

Electrical infrastructure to power a data center costs $1.5 – 3M per MW today.

Here's where it goes:

⚡ MV transformer — $70K

🔌 LV switchgear — $300K

🔋 UPS system — $1M

📦 PDU + remote power panels — $250K+

🏗️ Gray space shell + wiring — $120K

👷 Labor — $730K

Total: ~$1.77M/MW

An SST that collapses this chain to one conversion stage eliminates every line above except cables.

New total: $420K/MW.

At 1 GW, that's $1.35 billion savings.

N.b. this is significant but much smaller than the value of turning the DC into a first-class grid asset.

In addition to the post below UBS with a kinda reframing of the server CPU market through the lens of Agentic AI

AI workloads are about to massively expand the server CPU TAM - not just accelerators.

UBS now sees the server CPU market reaching ~$170B by 2030 - close to our beloved 2031 again ;-)

$ARM share projected to jump from 16% to 42%

$AMD also gaining share, while $INTC could fall from 60% to 29%

Agentic AI workloads expected to require far more orchestration, planning, retrieval, and CPU-side processing

But a possible big read-through for the broader AI stack:

more CPUs leads to more leading-edge wafers leads to more packaging leads to more memory leads to more networking.

UBS thinks $TSM becomes one of the biggest beneficiaries of this entire trend as ARM/AMD server demand scales aggressively through the decade.

Evercore introduced their token consumption model and implications for data center demand/capex today:

“Base Case: In our base case, we see total annual token demand growing from ~100 quadrillion in 2026 to ~4 quintillion in 2030, representing a ~150% 4-year CAGR. Key assumptions here include ~1.5B AI consumer users growing to ~3.7B by 2030 and ~50M AI agents growing to ~800M by 2030.

2) Upside Case: Total annual token demand grows from ~156 quadrillion in 2026 to ~8.3 quintillion in 2030, representing ~170% 4-year CAGR. Key assumptions here include ~1.8B consumer AI users growing to ~4.4B by 2030 and ~100M AI agents growing to ~1B by 2030.

3) Downside Case: Total annual token demand grows from ~71 quadrillion in 2026 to ~2 quintillion in 2030, representing a ~131% 4-year CAGR. Key assumptions here include ~1.3B consumer AI users growing to ~1.9B by 2030 and ~40M AI agents growing to ~640M by 2030. The logical question is what future token usage will represent for data center demand – this will vary depending on average install base throughput (Tokens per watt per MW or TPS/MW which also depends on Interactivity or TPS/user) but assuming ~4.0 quintillion annual token consumption in 2030 and a blended install base throughput of ~500,000 TPS/MW, we see demand for data center capacity reaching ~250 GW by 2030, which should provide tailwinds for our IT Hardware/Networking & Data Centers coverage. Net/net: We see growth in AI token consumption driving durable multi-year demand tailwinds for suppliers of DC/AI infra within our coverage.”