@bundesbank | views are my own | private | monetary policy, financial markets, finance, economics | retweets, likes and following do not imply endorsement

A new working paper of mine, forthcoming in JPE: Macroeconomics, makes a simple point with data. The point is old and well understood, but easy to forget.

When output is supply-constrained, or close to it, with a steep aggregate supply curve, a central bank can engineer rapid disinflation at little cost to output. Raising rates aggressively does nothing more than withdraw the excess aggregate demand.

Many missed this during COVID and the recent energy shocks. A central bank that accommodates when output is supply-constrained is pushing on a string.

The same withdrawal of excess demand can come through fiscal policy, and in some circumstances, that is the better tool. This was Keynes’ central insight in his 1940 essay, “How to Pay for the War.”

My read is that many central banks drew the wrong lesson from the late 2000s and early 2010s. Expansionary monetary and fiscal policy did not raise inflation then, but only because output was demand-constrained. Accommodation buys output cheaply when demand is the constraint. It buys inflation when supply is.

There is an equivalent reading through the FTPL. For space, we set it aside in the paper, but we are really making a statement about the real value of government debt. When output is supply-constrained, an excess of nominal claims chasing a fixed bundle of goods shows up as inflation: the price level rises until the real value of outstanding nominal liabilities equals the present value of the primary surpluses that back them. Disinflation then requires raising that present value, either through higher future surpluses or by retiring claims today, which is exactly what an absorption of excess demand does. Keynes’ compulsory saving scheme and the central bank’s rate hike become two routes to the same revaluation.

An ungated copied can be found here:

https://t.co/wy4J6g4sLV

Second, technological rents are driven by local knowledge spillovers. So if we manage to create a Silicon Valley in one EU member country, how are we going to ensure that the technological rents will be spread within the EU? Some fiscal redistribution will be probably needed.

@LucaFornaro3 I think this is a really important constraint. We won't be able to commit to a single European innovation hub, so our model *must* be different from the American one & we should think about how to get the knowledge spillovers of physical proximity in multi-innovation-hub Europe.

I put together a short practical guide for economists who want to use Claude Code, but who haven't gotten around to trying yet.

The goal is to reduce the start-up costs by using Claude Code within VS Code.

10-Punkte-Agenda für Deutschland mit einen lagerübergreifenden Kompass "Die Resilienz".

Heute im Handelsblatt:

Überblick und 30-seitige Dokument finden Sie hier: https://t.co/ig0a7B4uMK

Super interesting food for thought!

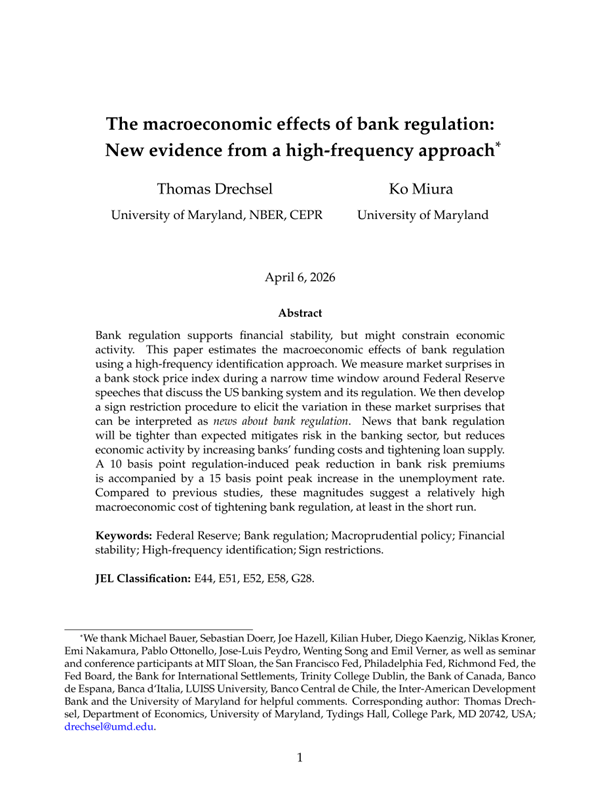

"The macroeconomic effects of bank regulation: New evidence from a high-frequency approach" by Thomas Drechsel and Ko Miura.

"Bank regulation supports financial stability, but might constrain economic activity. This paper estimates the macroeconomic effects of bank regulation using a high-frequency identification approach. We measure market surprises in a bank stock price index during a narrow time window around Federal Reserve speeches that discuss the US banking system and its regulation. We then develop a sign restriction procedure to elicit the variation in these market surprises that can be interpreted as news about bank regulation. News that bank regulation will be tighter than expected mitigates risk in the banking sector, but reduces economic activity by increasing banks’ funding costs and tightening loan supply. A 10 basis point regulation-induced peak reduction in bank risk premiums is accompanied by a 15 basis point peak increase in the unemployment rate. Compared to previous studies, these magnitudes suggest a relatively high macroeconomic cost of tightening bank regulation, at least in the short run."

https://t.co/FyzLgs1MDK

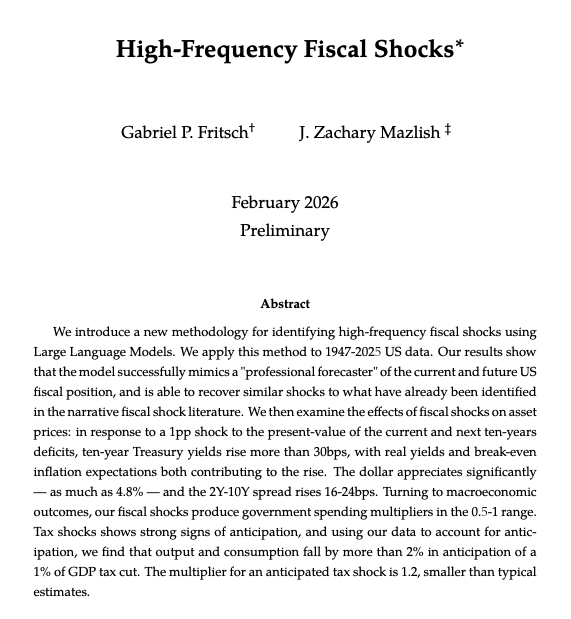

New paper out w/ my excellent co-author (and friend) @gabrielpfritsch : “High-frequency fiscal shocks”.

We use LLM’s to construct a daily time-series of expectations about US fiscal deficits (1947-2025) and thereby identify “fiscal shocks” in the historical record.

Thread:

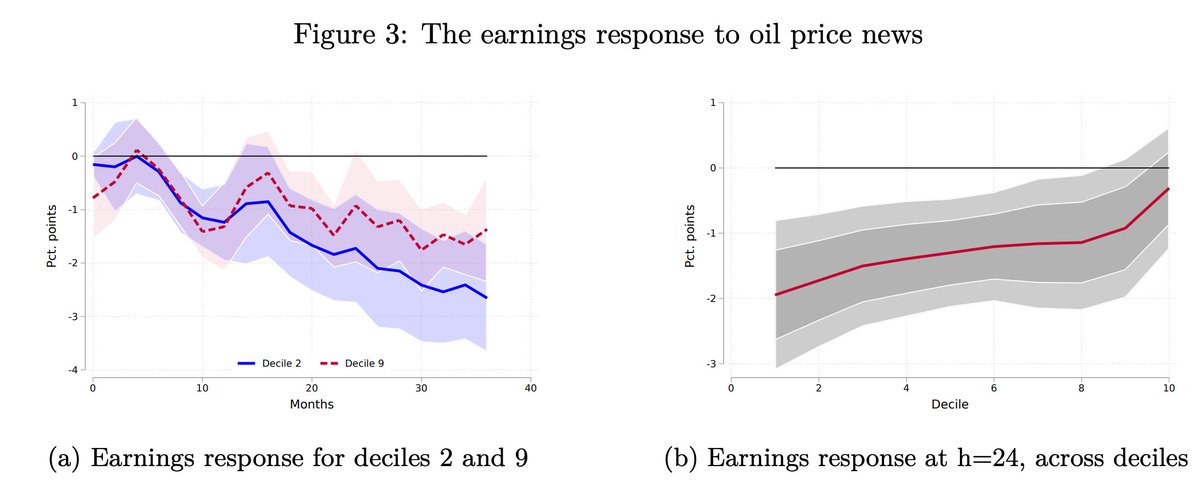

Oil prices just surged 8% in light of recent events. In our recent paper in @IMFEconReview, we study exactly this kind of shock: what happens to workers across the income distribution when oil supply contracts? 🧵

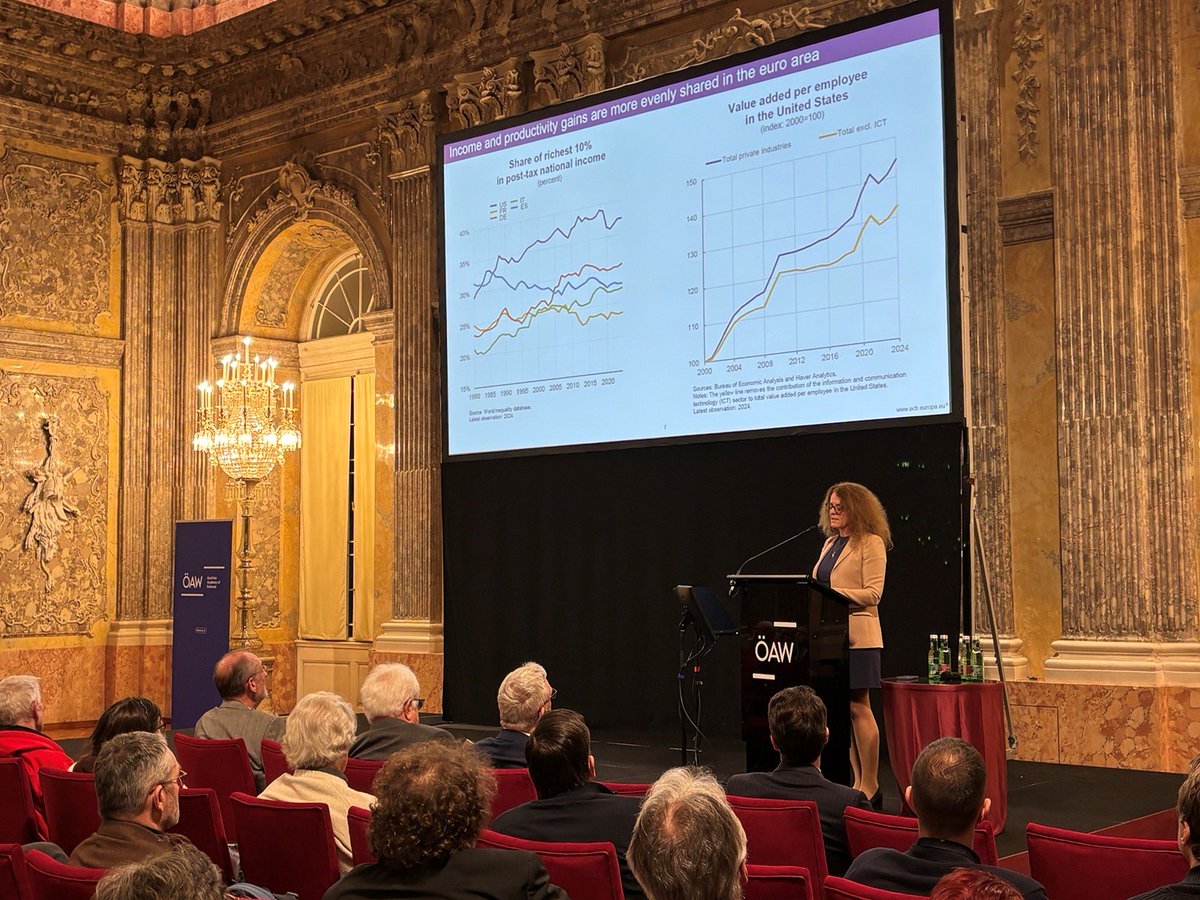

Last week, I had the honour to hold the #EugenBöhmVonBawerkLecture of the Austrian Academy of Sciences. I argued that the narrative that Europe is in decline is misleading and that Europe should unlock the full potential of the Single Market by introducing a #28thRegime. 1/20

This is a deep misunderstanding of how economics works.

Economists don’t start with unrealistic assumptions to reach irrelevant conclusions. Theorists spell out the assumptions under which an idealized, stylized result can be proven—and very often that result is an irrelevance result. In finance, for instance: Modigliani–Miller (capital structure doesn’t matter), no-trade theorems (nobody trades), etc.

The point isn’t the conclusion. We all know firms do optimize their capital structure (we teach how) and people trade trillions of dollars of securities every day.

The “result” is really the assumptions: they tell you what has to be true for a phenomenon not to matter or not to exist—and therefore what frictions make a field interesting or a phenomenon exists. A huge share of economic research is about relaxing those assumptions and studying what changes.

So when we say markets work “perfectly” under perfect competition, perfect substitutes, complete markets, and fully rational agents, we’re not claiming those conditions hold. We’re saying the literature should be built around the violation of these assumptions.

@stevehou The report by former central banker Noyer and Finance Minister Kukies spells out key factors in this regard - not only for Germany but for Europe with its fragmented capital markets /2

@stevehou „Europe’s scaleup gap stems from a lack of deep capital pools,

due in particular to Europe’s pension architecture, institutional

investors’ risk aversion, regulatory constraints and internal

market fragmentation“ according to a recent report. https://t.co/VOxRdYEVPT /1

Here's a possible explanation. Higher exports from China crowd out production of high-tech goods and innovation in the rest of the world. Over the medium term, GDP in the rest of the world drops because of lower productivity growth.

Tariff shocks work through weaker aggregate demand (adverse uncertainty and wealth effects). This effect might even be stronger than the direct cost-push effects with inflation falling.👇

SF Fed study examines 150 years of U.S. tariffs and find that they lead to lower inflation and weaker aggregate demand (which raises unemployment) https://t.co/d7d9WmIHHJ