@yq_acc The single biggest problem with crypto:

Devs got used to easy funding & aren't competitive with web2 startups

For yrs crypto gave no need to deliver

- useful products

- sustainable revenue

..& yet multi Billion valuations

Reality has arrived:

create real value or leave

Stock Ratings [June 7th]:

On current AI sector crash. Explanations below.

Strong Buy:

$GOOGL

$MU

$SNDK

SK Hynix

Buy:

$AMZN

$AEHR

$AAOI

$CIEN

$COHR

$CRDO

$DELL

$FN

$FORM

$GLW

$JBL

$LITE

$MDB

$MRVL

$MSFT

$NBIS

$NOW

$NVDA

$RDDT

$RKLB

$SIVE

Hold:

$ARM

$ASML

$AVGO

$AXTI

$BE

$META

$MTSI

$PLTR

$SOFI

Avoid:

$CBRS

$CRWV

$ETH

$HIMS

$IBIT / $BTC

$IREN

$MELI

$SNAP

$TSLA

$SPCX (SpaceX) IPO

---

Thoughts:

Strong Buy:

GOOGL - $85B raise is dilutive but they actually have ROI on their capex. Tbh, they'll probably always be a Strong Buy for me. Just the cleanest AI ROI among all the megacaps.

MU / SNDK / SK Hynix - If you're not bullish on memory, then idk for you.

Buy:

AMZN - Mainly for AWS reacceleration + Trainium. But some tension comparing AWS growth (+17%) vs Azure (+31%). Feel like custom silicon + distribution combo is durable even if growth rate lags a bit.

AEHR - H2 ramp in WLBI/PLBI systems coming, anchored by "significant" follow-on Sonoma order from lead hyperscale customer. Just need to wait a bit esp. for rev to inflect. But AI ASIC burb in is mandatory as device power goes up.

AAOI - Q3 capacity ramp (via facility expansion in Texas) toward 650k+ 800G/1.6T units/mth. Capacity coming online is the catalyst imo along w/ already known laser bottleneck + Made in US premiums.

CIEN - Just a high quality biz that got pounded last week (-22%). Beat + raise earnings, but stock dropping this much is an overreaction. CEO even said demand is "structural, multi year and AI-driven" shown by AI-driven DCI being their fastest growing part of the order book as new long-haul routes get built for latency and bandwidth.

COHR - upcoming CPO ramp (Nvidia spectrum-x) will speed things up, these prices will look cheap when we look back imo.

CRDO - Personally bought a ton last week post-earnings drop. Like Ciena, v. high quality compounding hold through the whole AI supercycle. Crazy high margins. Obviously compete w/ Marvell/Broadcom on SerDes, but also need to factor in the 1.6T switch replacement cycle into late 2026.

DELL - Trump effect. I've learnt my lesson and will listen to him next time.

FN - v. low drama way to ride transceiver demand + iPronics sipho line for cpo. New datacom wins also extending into next FY, although some Nvidia conc. risks. Put them in Buy just to be generous as was unsure tbh.

FORM - Important for HBM, adv packaging and CPO for higher yields. Foundry test intensity only set to increase w/ production.

GLW - Lead glass core substrates which are an advanced packaging bottleneck. LTP w/ Nvidia to expand US optical manufacturing for AI infra too.

JBL - Stock has done nothing for a month, but earnings coming up could be a nice catalyst for a push higher from their DC infra segment growing + outpacing drag from legacy mobility/ev exposure / margin mix.

LITE - CPO ramp + Nvidia qualification like Coherent.

MDB - AI is not replacing them. Imo they win vs. bolt on vector stores since their architecture is so simple.

MRVL - going to $1T according to Jensen. Underlying business is solid though esp. w/ Celestial acquisition for photonics. SPY inclusion last week too is a big positive.

MSFT - Current valuations are a joke tbh, markets probs punishing some margin compression. Rev +18%, Azure +40%, AI run rate +123%. So, v. clear enterprise monetisation path. Will be buying next week in retirement account.

NBIS - Best neocloud by far. They're a $100B biz vs. ~$57B currently. Jensen: "Nebius will take care of you."

NOW - AI is not replacing them. No enterprise CEO/CTO is dumb enough to offboard them at this point.

NVDA - Same as Microsoft. Been buying this whole time, but am now even more confused at current cheap valuations.

RDDT - AI is not replacing them. Cash printer. ARPUs improving also in legacy segments like international.

RKLB - #2 in commercial launch after SpaceX + their IPO should re-rate the entire space comp set where RKLB is the main liquid proxy. Unbelievable earnings also, just executing so well rn.

SIVE - everyone on X knows at this point?

Hold:

ARM - current valuation prices in flawless execution imo. But their IP is growing in DC CPUs e.g. Nvidia grace, AWS Graviton etc.

ASML - Elon said yesterday: "ASML should be treasured and supported. It is arguably the greatest company in Europe." - I agree. Also Terafab fireside chat next week High-NA EUV is the next leg, locking in the roadmap through the decade. Could also be a "Buy" for more risk averse people.

AVGO - CEO didn't raise >$100B FY27 target + flagged that Google will multi-source. Current AI mix is also diluting margins slightly. Just needed a pullback before the thesis starts working again.

AXTI - InP substrate bottleneck, crucial for AI buildout rn. Could also buy rn, just a slow dca since they've run up a ton already + raise completed ($632M) to 2x InP capacity.

BE - SOFC winner imo (Ceres 2nd). Don't think it's a buy just yet due to some valuation vs. profitability gaps.

META - hold based on capital allocation mainly. Market seems wary of the ROI on their AI capex hence the continuous dips. Also potential raise to fund capex like Google too - once that digests, I'll personally look to buy.

MTSI - Big fan of their investment into $IQE since it de-risks operations a lot, but just think COHR/LITE are better options for 800G/1.6T transition.

PLTR - Relatively poor Risk:Reward at current multiples.

SOFI - rate sensitivity. Loan book + credit performance carry macro risk which caps conviction rn. Some positives though w/ young + growing member base. Would need to look at credit trends + Fed path in June FOMC to re-assess.

Avoid:

CBRS - avoid at current prices. Would want it to come down closer to ~$40B mc before I look to dca. Would love to hold since they own genuinely unique tech.

CRWV / IREN - Financing for both is a mess...debt/dilution. Nebius are just a better multi yr neocloud.

HIMS - Forced out of higher margin GLP1s into lower margin braded GLPs from Novo/Lilly. Feel like their moat was to do w/ regulatory arbitrage on compounding. With that gone, it's a customer acquisition + churn biz buying branded drugs at lower margin.

IBIT / BTC - Macro setup is hostile. Higher rates for longer (10Y ~4.54%, 30Y >5%) raise opportunity cost. Pure liquidity/risk appetite instrument + both are tight rn.

ETH - same as bitcoin.

MELI - personally a little confused - either a hold/avoid. Seeing some margin compression via their credit book growing faster than revenues. Talks of margin recovery next year, at which point the stock could re-rate.

SNAP - Absolute worst social media app + CEO is a weirdo. Platform keeps losing share to Meta/Tiktok.

TSLA - Huge competition from other EV makers shown by production > deliveries volumes. Humanoids will be their next key growth driver, just a little while away.

SPCX (SpaceX) IPO: I never personally participate in IPOs + SpaceX specifically is way too overvalued for me. Will be going long eventually though. Rough ballpark would be ~$1.5T if it gets there post IPO.

---

Just for very high level notes at current stock prices (NFA).

I'm personally staying long despite the current macro backdrop, mainly in AI supercycle names e.g. memory, semis etc.

But then you also have great companies at depressed prices, mainly in SaaS which I'm DCA'ing currently.

I don't hold positions in all of these names. This is just a subset that overlaps my "Close Tracking" list + X's favourite names.

This hand-drawn chart is over 90 years old.

Jesse Livermore sketched it in the 1930s to show his students how every speculative stock moves through the same numbered phases:

– Points 1–4: Accumulation cylinder, smart money quietly buying

– Points 5–7: The all-important action, breakout, volume, the rally begins

– Points 8–13: The test before selling short, final euphoric peak, lower high

– After 13: Distribution and collapse

Look at where we are right now.

Micron, SanDisk, the DRAM ETF, Oracle, SMCI, AppLovin, Nvidia – all sitting somewhere between points 8 and 10. Vertical moves. Record volumes. Headlines turning euphoric.

Palantir is further along. Maybe 12 or 13. The phase Livermore literally circled and labeled "test before selling short."

This is where the most money is made in the shortest time in any market cycle. Bull markets are won in this zone. Life-changing returns are compounded here.

But it is also exactly the phase where Livermore lost three fortunes.

Because the same energy that drives a stock from point 8 to point 13 quietly pushes it past 13.

The setups today are real. The opportunities are real. The money being made is real.

The sell rules still apply.

– Trim into strength, not weakness

– Take partial profits at the 20–25% mark

– Cut losses at 7–8%, no exceptions

– Watch for the climax run signature

Make money on the way up.

Just don't give it all back on the way down.

Livermore wrote the rulebook on this. He still ended up broke.

The chart never changes. Because the chart isn't drawing the stock. It's drawing the people who own it.

President Trump is undefeated in the stock market.

On May 8th, President Trump told everyone to "go out and buy a Dell."

19 days later, on May 27th, Dell was awarded a $9.7B contract with the US Pentagon.

Today, Dell, $DELL, reported stronger than expected earnings and the stock surged +30%.

Dell's stock is now up +80% since May 8th, adding +$120 BILLION in market cap.

Truly unprecedented.

@zeroxkyle IRL + Physical world hv moats

AI training data is 100x > Robotics training data

(Robotics will take decades longer to replace physical world)

@adamscochran There's only one way out for Trump;

He's already made a soft deal with Iran and he's just saber rattling to save face

Then comes out with "they listened to my threats and they backed down"

..without that, Trump & markets are screwed

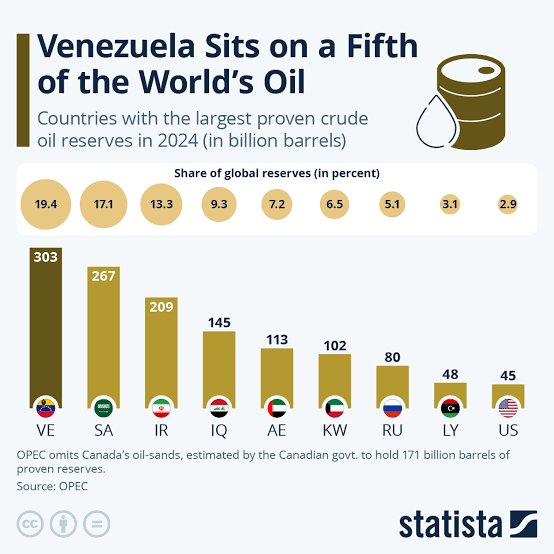

@ericnuttall Devil's advocate:

1. US now hv Venezuelan latest global supply (will take time, but its coming)

2. Oil intensity keeps declining (and will continue with solar + nuclear)

https://t.co/b0EwYHT9IR

@0xNairolf we need better ratings (surely with AI its easier, the same way auditing smart contracts is easier)

some interesting starts but not good enough (yet):

https://t.co/b1wlNfEtP3

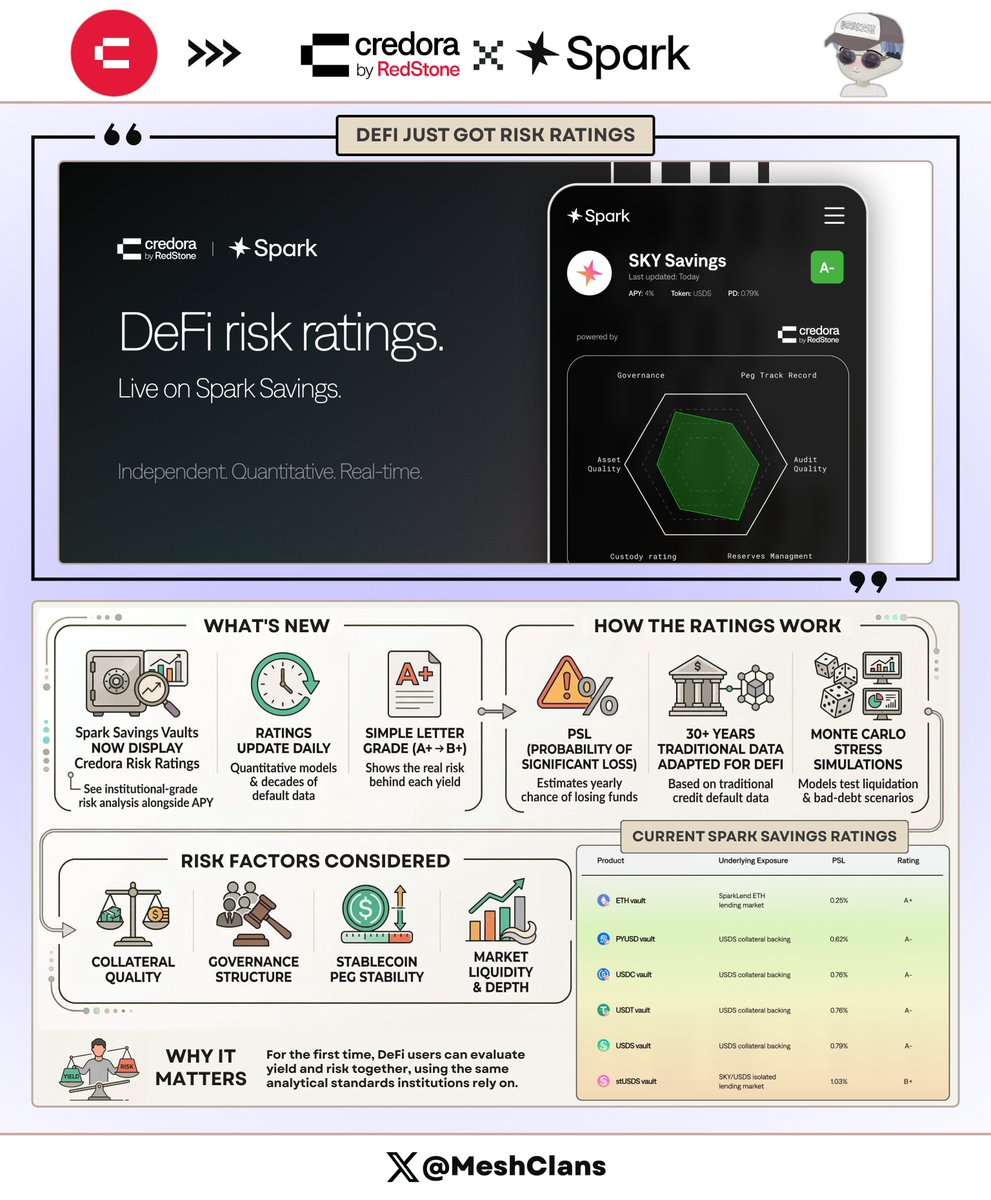

DeFi just got something it's never had before: actual risk ratings

Independent, daily-updated risk grades went live on @sparkdotfi a few days ago, and every Spark Savings vault now shows a Credora rating based on quantitative models and decades of historical default data.

For the first time, you can see institutional-grade risk assessment right next to your APY.

Six Spark Savings products, each with its own Credora rating. A+, A, A-, B+ (one letter that tells you what you're actually risking to earn that yield, updated daily as market conditions shift).

Here's what the ratings show (per the current official report; check live in Spark Savings for any intraday shifts):

> Savings ETH → SparkLend ETH lending market → 0.25% PSL → A

> Savings PYUSD → USDS collateral backing → 0.58% PSL → A-

> Savings USDC → USDS collateral backing → 0.61% PSL → A-

> Savings USDT → USDS collateral backing → 0.60% PSL → A-

> Savings USDS → USDS collateral backing → 0.63% PSL → A-

> Staked USDS → SKY/USDS Aave lending market → 1.03% PSL → B+

This is risk-aware DeFi.

Every rating answers three questions: How safe is the collateral? What happens if prices move? Who's protecting your deposit?

The PSL (Probability of Significant Loss) gives you an annual percentage chance that you actually lose money, not just paper volatility. It's calibrated against 30+ years of credit default data from traditional markets, then adapted for DeFi's unique risk profile.

Behind each letter grade sits serious quantitative work. Monte Carlo simulations stress-test liquidation scenarios and bad debt risk under extreme price moves.

Risk modifiers adjust for collateral quality, governance structures, peg stability, and market depth.

The difference from traditional ratings:

> TradFi measures credit risk on issuers, Credora measures it on protocols and vaults

> TradFi updates ratings quarterly through committees, DeFi gets live updates pushed onchain

> TradFi relies on prospectuses and disclosures, DeFi reads onchain parameters directly

Savings ETH gets an A because of its conservative setup, deep liquidity, and battle-tested liquidator ecosystem. Staked USDS gets a B+ because there's high concentration in certain LTV bands, with $78M in positions against roughly $600K of liquidity at 2% depth. Higher yield, tighter liquidity cushions.

The rating just reflects that trade-off.

When risk is transparent, people trust it. When people trust it, capital flows.

IMO, this is how DeFi crosses the chasm.

Institutions don't deploy capital based on vibes and APY screenshots. They need quantified downside, stress-tested scenarios, and a risk framework that maps to existing mandates.

@CredoraNetwork built exactly that, and Spark is the first major protocol to surface it directly in the user experience.

As @hexonaut, co-founder of Spark, put it: "Until now, DeFi participants have had to piece together risk information from multiple sources, or worse, make decisions based on APY alone. Credora is the missing link!"

You can check it out yourself right now.

Head to spark(dot)fi/savings, open any vault, hit the Risk Assessment tab, and you'll see every rating, every underlying market, every modifier in real time.

Want the full picture? There's a 20-page institutional report with detailed breakdowns, collateral analysis, simulations, and complete methodology at reports(dot)credora(dot)io/spark/latest.pdf

The bigger picture here is Credora already rated 100+ vaults on Morpho, and early data shows rated vaults seeing faster TVL growth and stickier deposits. Sky/USDS integration is coming next, then wallets, fintech apps, maybe even AI agents routing based on risk-adjusted returns.

This isn't just Spark getting a feature upgrade. It's the infrastructure that lets DeFi absorb institutional capital at scale.

Note: Ratings update daily based on market conditions. Always check current ratings before deploying capital.

Quick disclaimer: ratings and data are informational only, not investment advice. Do your own research.

Know your risk.

flatbed rejections are a good indicator for small/mid-cap industrials

AIRR ETF (small cap industrials) is up 24% YTD and 221% over 5yrs

Less so for S&P which is 70%+ tech/services.

Also worth noting the dataset is thin (<5% of SONAR tenders) and the last spike to 41% was mostly tariff front-loading.

Real confirmation is ISM PMI just hitting 52.6 - first expansion in a year.

Flatbed x PMI x homebuilders is a good proxy for economy growing again