I've really been enjoying @DavidBeckworth@Macro_Musings podcast lately (we are in a golden age of econ podcasts!). A recent episode with former CEA chair Tyler Goodspeed takes on a fascinating question: Are recessions driven by random shocks (bad luck) or the product of inherently cyclical boom-bust phenomena? Goodspeed's new book argues it's the former. The episode is good fun and very interesting.

https://t.co/cUN5cHFl4L

Two thoughts I wanted to share in reaction, given that this is a topic close to my heart:

1) Somewhat ironically, even though we call short-run fluctuations business *cycles*, the random shocks view is close to the mainstream approach in academic macro. A long tradition in time series macro going back to Granger's work in the 60s looks at the properties of macroeconomic time series (spectral densities!) and finds that there is not much evidence of stable, regular cycles in macro series. Modern DSGE macro models expansions/recessions as the product of relatively persistent shocks, rather than endogenous cycles. The view that business cycles are the product of endogenous boom-bust dynamics is slightly more on the periphery of macro than people might think!

2) That said, I would push back a bit on the strongest version of the random shocks view. I agree that a lot of variation at business cycle frequencies comes from random shocks. But there is quite a bit of evidence that the endogenous boom-bust story has some truth, at least during specific episodes featuring credit and financial booms preceding financial crisis recession. There is quite a bit of evidence that rapid expansions in credit, especially to certain risky sectors like real estate, coupled with booming prices of real estate and other assets, are a strong predictor of future downturns and financial crises. Financial crises are not unpredictable "bolts from the blue." While the exact timing of a crisis is very hard to predict, there are certain vulnerabilities that make financial crises and deep recessions more likely. These dynamics don't hold mechanically during every business cycle, but they do matter for understanding major downturns involving financial instability.

A few examples off the top of my head include: 2008 in the US, Spain, Ireland, etc; the Japanese financial crisis after the 1980s boom; the crises and deep recessions in the Nordic economies of late 1980s; emerging market crises like Mexico 1994 and Thailand 1997; or historical crises like Australia’s housing boom and bust in the late 1880s, the panic of 1893, and perhaps the US Great Depression.

📢 Macro Theory with Measured Expectations (with Roth, Wiederholt, Wohlfahrt)📢

The Lucas critique says policy evaluations based on historical correlations can fail because policy changes alter expectation formation.

We propose a way to address this: measure expectations under alternative policy scenarios.

Below, I quickly describe 4 key results that emerge from this approach. Details in the paper👇

https://t.co/GpBpyKzTQH

📢 New paper w/ @GregWKaplan 🧵1/10

How small is “small” for local-linear methods to deliver reliable answers in heterogeneous-agent models of fiscal stimulus?

Our answer: very small.

Good education has never been more important than it is now.

With AI, *what* you know matters less. Whether you can figure out and understand new stuff is totally essential.

Degrees like econ that teach you to think analytically about new problems are worth more than ever.

AI will be the end of universities! MOOCs will be the end of universities! YouTube will be the end! Libraries! The printing press!

And each time life continues almost as before. Universities provide peer interaction, evaluation, coordination and commitment. That’s the value.

Excited to FINALLY release toughest+most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

It is an absolute pleasure to release this new work, joint with the great Emmanuel Farhi and Alan Olivi: "Price Theory for Incomplete Markets" (the title is a wink at my alma mater).

At long last, as it has been a very long haul.

https://t.co/YArkolyWYu

A brief thread 1/n

🚨 New Paper and Public Good🚨

"The Global Macro Database: A New International Macroeconomic Dataset", joint with @chenzix, Mohammed Lehbib, and Ziliang Chen.

We built the most comprehensive macro database ever—covering 243 countries from 1086-today, integrating 110 sources. 🧵

▶️ The video of the First Calvo Lecture is now available.

@IvanWerning (MIT), introduced by @SFGaliani, presented:

“On Inflation: A Look From Above, Backwards and Forwards”

Watch the lecture here:

https://t.co/haeSsGxJ3U

Super interesting!

"A Demand Theory of the Price Level" by Marcus Hagedorn (The paper was submitted to the International Economic Review posthumously. Sadly, Marcus Hagedorn passed away too soon.).

"Heterogeneous agent incomplete markets models offer a new perspective on price and inflation determination. In contrast to complete markets, the price level is determined from the asset-market clearing condition. Fiscal and monetary policy then jointly and uniquely determine the finite steady-state price level and the inflation rate, including in a steady state in which the nominal interest rate is constant. Fiscal policy can determine the long-run inflation rate for a fiscal rule which sets the growth rate of nominal government debt, whereas both fiscal and monetary policy determine the long-run inflation rate under different tax rules."

https://t.co/xQyfA1rJEa

Same thing in economics: many of the truly influential papers from the 1930s to the 1950s would probably never get published today because the reaction would immediately be: “Did you run 126 robustness checks?” or “Is the identification strategy airtight?”

Take Keynes’ General Theory. I doubt a major university press would accept it today.

What we often end up with instead are countless papers that are extremely methodologically careful but focused on relatively minor questions.

Of course, there are still genuinely outstanding papers being produced. But probably far fewer than there should be.

An Econ PhD student at the 20th ranked program who is working on stuff they are passionate about will have a better job market than one at MIT who's been doing nothing but phd-app-maxxing since undergrad.

People get confused by this because they don't observe *how* successful people came about their insane knowledge bases. It wasn't by relentlessly grinding away at stuff because they had to.

They look at Scott Kominers and say "if i grind and learn as much math as he did, i will be successful." You can't! *You* can't learn as much math as Kominers because he gets energized by configuration results for type ii lattices. You will burn out if you try to do it this way.

You cannot, through grind alone, learn more about the economics of cities than Glaeser, or about how to maximize a value function than Acemoglu.

Research careers are long. Most people give up and stop working on research (graph is share of elite PhD graduates with at least one publication in year X after graduation).

If you're starting a PhD, you're presumably doing it to have a successful 40-year research career. The number one factor in whether that happens is not which program you get into, it's whether you find a research angle that energizes you enough to push through the endless barriers an academic career throws in your path.

This is why a lot of the received wisdom around PhD applications is wrong. If you're 100% consumed by the predoc rat race already, it's going to be a long, hard road ahead.

Obv you still have to do admissions, you should study a lot for the GRE, sigh it seems like taking real analysis is probably worth it.

But spending time on the things that energize you about economics is a no-brainer, whether it's policy, or blogging, or whatever, you gotta do the things that light your fire and make you want to be on this road.

Thrilled to share a project I've been refining: a complete, open-source repository on "Deep Learning for Solving and Estimating Dynamic Models in Economics and Finance."

I've cleaned up the materials from my PhD classes and summer schools into one coherent resource. 🧵 1/6

🚨 Public Good Alert 🚨

Two years of development. Zero funding. 𝟲,𝟲𝟵𝟯 𝗼𝗳𝗳𝗶𝗰𝗶𝗮𝗹 𝘀𝘁𝗮𝘁𝗲𝗺𝗲𝗻𝘁𝘀 𝗳𝗿𝗼𝗺 𝟱𝟭 𝗰𝗲𝗻𝘁𝗿𝗮𝗹 𝗯𝗮𝗻𝗸𝘀. #TextData

Today, we are opening the doors to it all for free 🚀

Visit our website: https://t.co/ToBke8Dxww

🧵1/12 #NLP

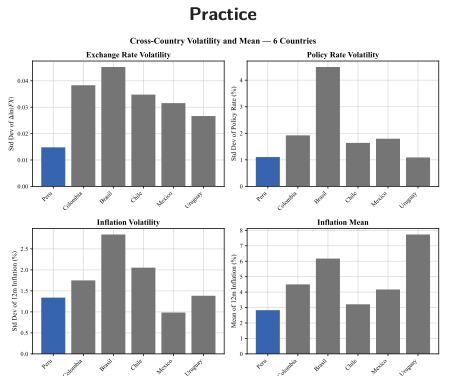

Slides of the presentation where I discuss Peru's successful joint control of inflation and FX via a creative deployment of central bank tools, which defied conventional wisdom.

My slides end with lessons for other small economies:

https://t.co/LvRFIpK6e3

2/10 Mancur Olson argued in "Raise and Decline of nations" that old democracies accumulate distributional coalitions: unions, professions, regional lobbies, public-sector constituencies. As a result, these societies only reform themselves when something forces them.

What is most shocking about all of this is that a very large number of people are exceedingly confident in their understanding of something that they never bothered reading even slightly about.

They did not study the topic, they do not work in the field, they don't even do it as a hobby, but they legitimately believe that they somehow see something that all of us are missing.

Then, if you try to explain to them that they aren't quite applying the ideas they are trying to apply correctly, that there's legitimately something wrong about their views, that's arrogance...

I have seen the comments some people left you today. The level of arrogance is absolutely staggering and impossibly ironic given that they, themselves, call other people arrogant.