The next AI factory may run out of ways to talk to itself before it runs out of GPUs.

This app is full of « photonics this, CPO that, $POET, $SIVE and the gang ».

So I wrote a piece that actually maps why this bottleneck feels different, where it bites first, and how the thesis shifts from chips/HBM/power to the back-end fabric.

You should stop picturing a data center as a room full of chips and start picturing it as a communication system.

Every GPU in a training cluster is constantly asking other GPUs what they know. Gradients, activations, experts, cache state, routing decisions, all of it has to move. At small scale, copper can carry the conversation. At AI factory scale, copper starts becoming a wall.

The signal has to cross board traces, connectors, cables, heat, loss, reflection, crosstalk, and distance. The fix is always more power, more retimers, more cooling, more cable bulk.

At some point the system is spending too much energy keeping electricity alive long enough to become useful.

That is why photonics matters.

Most coverage still frames this as “optics TAM growing.” It misses the supply chain relocation and the new constraints on light sources, integration, and test that actually determine who scales.

The names positioned at the light source + photonic integration layer for next-gen ELS/CPO?

$POET’s Optical Interposer and $SIVE’s high-power DFB laser arrays are right in the critical path, but there are many many others.

AI’s photonics bottleneck: why moving data is now harder than making chips:

https://t.co/OguHp3QzFt

Copper just hit all time highs and almost nobody in your timeline is talking about it because it's not a tech stock with a ticker and a subreddit.

Meanwhile every single AI data center, EV, wind turbine, and power grid upgrade on earth needs more of it than we can currently dig out of the ground.

Don't sleep on it!

This is an excellent interview btw

Nicolai (Norwegian Sovereign Wealth Fund CEO) asks the IBM CEO if AI a bubble

Listen very very carefully to his answer

Are mega-funds really taking over seed?

I decided to look at the behavior of the world's largest VC funds ($10B+ AUM) at early stages and answer a simple question: should EMs worry about their structural edge?

So I used @harmonic_ai and looked at all pre-seed, seed, and seed extension rounds across 3 eras:

- SaaS Era (2015–2019): 5 years of a normal market. Cloud, SaaS, fintech were the dominant theses.

- ZIRP Era (2020–2022): 3 years of zero interest rates and free capital.

- AI Era (2023–2026): from ChatGPT to the present day.

We focused on one core metric: average number of early-stage deals per year for each fund in each era.

Here are a few insights we found interesting:

1/ In the SaaS era, a typical mega-fund made 10–20 early-stage deals per year. This was moderate, targeted seed activity – a complement to the core Series A/B and later strategy.

2/ In the ZIRP era, everyone scaled up. Each of the 10 funds increased their early-stage deals/year (some by 2–3x), because capital was free, competition at later stages was fierce, and seed felt like a cheap entry point.

3/ Then came the AI era and it became clear this was no temporary effect. Even as rates rose and capital became more expensive with the end of ZIRP, @a16z and @generalcatalyst posted peak early-stage activity.

> @a16z: 16.6 → 48.7 → 75.3 deals/year. A 4x increase from the SaaS era.

> @generalcatalyst: 15.2 → 31.7 → 61.5 deals/year. Also 4x.

The most interesting finding, though, is 3 distinct behavioral models:

1/ "Accelerators" - deals/year in the AI era exceed ZIRP levels: @a16z (75.3/yr), @generalcatalyst (61.5/yr), @khoslaventures (31.5/yr). These funds didn't just stay active in seed after free money ended – they doubled down.

2/ "Stabilizers" – deals/year in the AI era are slightly below ZIRP peak, but well above SaaS-era levels: @sequoia (19.6 ��� 49.3 → 50.6), @Accel (15.2 → 43.3 → 34.7), @lightspeedvp (11.6 → 41.7 → 32.1). The ZIRP spike moderated, but activity levels remain sustainably 2–3x above the SaaS era. There's no return to the old normal.

3/ "Disciplined" – steady, gradual growth across all eras: @BessemerVP (9.4 → 23.0 → 20.9), @Lux_Capital (7.2 → 14.3 → 14.7), @IndexVentures (10.0 → 23.3 → 17.6). No ZIRP spikes, no AI explosions – but the baseline has durably shifted upward.

So in the SaaS era, these 10 funds collectively made roughly 140–150 early-stage deals per year. In the AI era – around 370–400. And I think they just set up a new, sustained baseline, not just doubled after a ZIRP-peak era.

For an LP evaluating an emerging seed manager, this is the most important context.

The early-stage market your GP is investing in is one where 10 funds with $10B+ in AUM are doing dozens deals a year.

An emerging manager needs to be able to articulate exactly where, in that market, they have the right to win.

Dan Loeb started Third Point with $3 million. it's now $24 billion.

when asked which books shaped how he invests, he named four, each one representing a different phase of his evolution as an investor:

phase 1. event-driven deep value:

"You Can Be a Stock Market Genius" by Joel Greenblatt. "most of the people i know in that world use that as their framework." spin-offs, privatizations, post-reorganization equities. buying things cheap that nobody else was doing the work on.

....

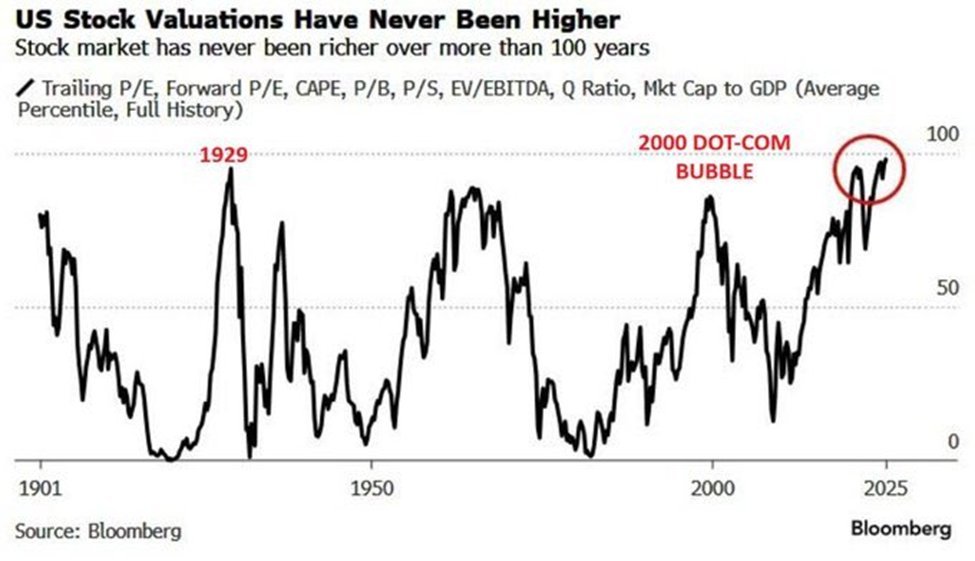

Goldman Sachs: "Token use by AI agents is expected to multiply 24 times by 2030"

AI agents are now creating the first serious cost test for the AI boom. As was reported this week, Uber and Microsoft are already rethinking expensive agent usage.

A chatbot may answer once, but an agent plans, calls tools, checks results, edits mistakes, and repeats the loop.

That loop can make one user request consume 10x, 50x, or even far more tokens than a normal answer.

Goldman’s bullish case is that monthly token use could reach 120 quadrillion by 2030, while inference cost per token keeps falling 60%-70% per year.

The fight is now between agent productivity and token waste.

Earlier this month, Microsoft began revoking developer access to Claude Code, with plans to move them to its in-house Copilot Command Line Interface tool by June 30. The company has framed this as consolidating teams around its own tools, but the timing at the fiscal year’s end hints it may also be about lowering costs.

Cash flow no longer covers the AI capex bill, so hyperscalers are funding it with record debt:

Hyperscaler bond issuance has soared to $150 billion YTD, more than the prior two years combined.

The AI bubble is primarily an earnings bubble rather than a valuation bubble. My report this week discusses the metrics investors should monitor to know when this bubble is about to burst.

Clients can read it here:

https://t.co/nPpZ5E1mas

🔎 Humanoid Robots: A $200B Market by 2035?

The humanoid robotics market is about to enter the exponential phase that AI just went through. According to Barclays Research, the global humanoid market is projected to grow from essentially zero in 2025 to between $28B and $204B by 2035 depending on the scenario. Even the base case at $38B represents a multi decade growth story. But the high case at $204B is what investors should pay attention to, because every transformative technology in history has tracked closer to the bullish projection than the conservative one. Smartphones, EVs, cloud computing, all consistently blew past the "realistic" forecasts.

Key Takeaways

🔸 High case projects 200x+ growth over 10 years. Even the conservative case at $28B is a 100x expansion from today's near zero baseline.

🔸The bull/bear spread (28 vs 204) is massive, showing analysts have no clue how big this gets. That uncertainty is exactly where the biggest asymmetric returns live.

🔸Major catalysts are already in motion: Tesla Optimus, Figure AI, Boston Dynamics, and Chinese manufacturers like Unitree are all entering mass production phases.

🔸The labor market backdrop matters. Aging populations in developed economies + persistent worker shortages = humanoid robots become economic necessity, not luxury.

��� Bottom Line: We're at the inflection point of humanoid robotics. The companies winning this race over the next decade will define the next industrial revolution. Pay attention now while it still looks early.

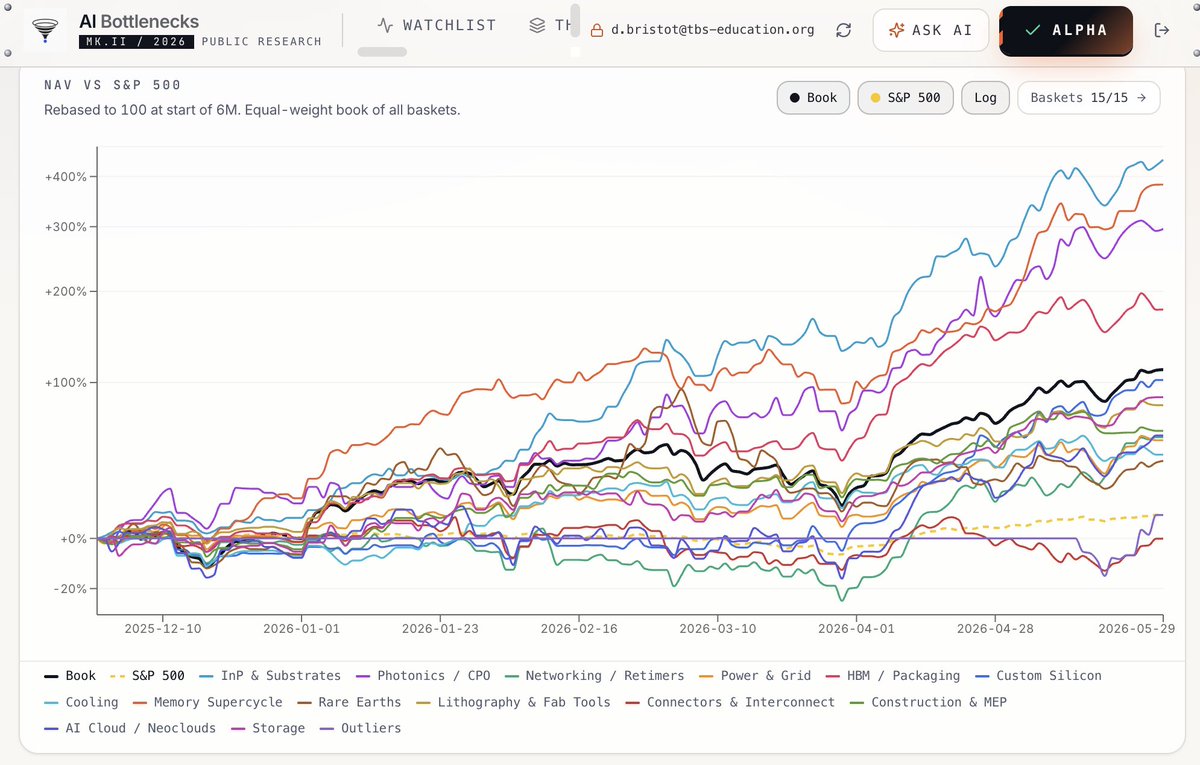

The market is no longer buying AI exposure, it's buying scarcity by layer.

The book I keep is up 111.83% over the last 6 months, while the S&P 500 is up 11.02% over the same window.

That leaves the book with +100.81% alpha (only tracking 112 companies rn)

But the headline return is not really the point, as the more useful signal is what is happening underneath it.

Across the book, 106 of 113 names are up, so this is not a single-stock story or one lucky basket carrying the whole thing. At the same time, the dispersion between baskets is extreme: InP & Substrates is up 438.79%, while Connectors & Interconnect is down 0.14%. That is a huge spread inside the same AI infrastructure trade.

That is what I wanted the dashboard to show.

AI Bottlenecks is not meant to be a stock list. It is a way to rank the physical layers of the AI buildout: substrates, photonics, memory, packaging, power, cooling, networking, cloud, storage, construction, and the rest of the supply chain that sits underneath the model headlines.

Each basket is equal-weighted, and each basket gets one vote in the book. The point is not just to ask whether AI infrastructure is working as a theme. The point is to ask which layer the market is re-rating first, which layer is lagging, and where the constraint may be moving next.

The 6-month leaderboard now looks like this:

InP & Substrates: +438.79%

Memory Supercycle: +382.30%

Photonics / CPO: +295.90%

HBM / Packaging: +176.79%

Custom Silicon: +102.31%

Storage: +87.36%

Lithography & Fab Tools: +80.86%

Construction & MEP: +61.35%

AI Cloud / Neoclouds: +58.07%

Networking / Retimers: +56.89%

Power & Grid: +54.71%

Cooling: +45.11%

Rare Earths: +41.18%

Outliers: +10.96%

Connectors & Interconnect: -0.14%

The top of the table is telling a pretty clear story: the strongest layers are the ones tied to substrates, memory, photonics, advanced packaging, and custom silicon, the things that physically gate the next step of the AI buildout.

These are the pieces that matter when you start asking what has to be true for Rubin Ultra, HBM4E, higher-density clusters, and the next round of inference capacity to actually ship.

The bottom of the table is just as important. A weak basket does not necessarily mean the layer is irrelevant. It may mean the market already paid for the story, the chokepoint did not bind this quarter, or the catalyst was more geopolitical than operational. That is why the rank order matters more than the headline return.

A refinery report gives a useful analogy. A barrel of crude is a barrel of crude, but the yield by cut, gasoline, diesel, kerosene, asphalt, residue, tells you where the constraint was in that quarter.

The commodity is the same. The bottleneck moves. The report ranks the pressure points. That's what this book is trying to do for AI infrastructure.

The visible AI trade is usually shown as one line. This is the same trade broken into 15 physical lines, each one tied to a different part of the route card.

The book is up because most layers are up. It is interesting because the ordering of those layers tells you what the market thinks is scarce.

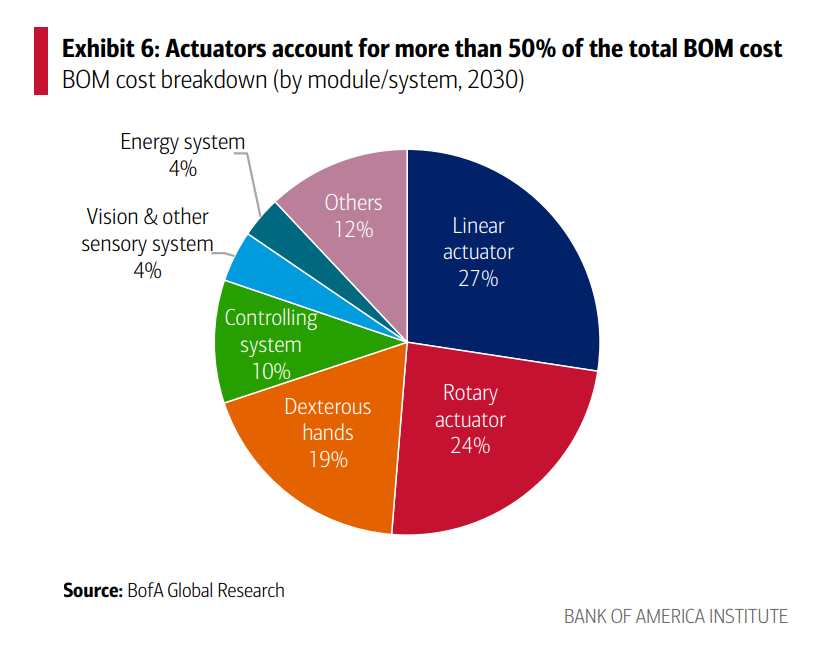

McKinsey humanoid supply chain mapping:

Confirms that Actuators are set to be the key battleground for mass production.

Coupled with BofA analysis where Actuators = 51% total BOM.

A few companies have overlap in different Actuator parts like:

-> Harmonic Drive Systems (6324)

-> Nabtesco Corp (6268)

-> THK (6481)

-> Schaeffler

I'm close to picking 1-2 names for exposure.

HDS are the glaringly obvious pick though, purely from a supply chain overlap POV.

did some digging so you don't have to, and how crazy is this?

One little AI accelerator touches dozens of hyper-specialized companies across three continents, and we’re talking thousands of engineers, chemists, and machinists who’ve never met each other but have to hit their exact tolerances or the whole thing doesn’t work.

If you map every layer of an AI accelerator package and name the under-followed supplier at each layer, the map looks like this:

The fiberglass that goes inside ABF substrates: Nittobo Industries (Japan, private), Asahi Kasei (3407.T), Owens Corning (OC) on the lower-end grades. Unimicron just warned that low-CTE supply is the next constraint.

The ABF film itself: Ajinomoto (2802.T) holds 98% of the IP and licenses it to five substrate makers.

The substrate fabricators: Ibiden (4062.T), Unimicron (https://t.co/ysHqK2LKVS), Nan Ya PCB (https://t.co/CZuj06w7zb), Shinko (7820.T), Kinsus (https://t.co/a1oVl1GoyF). Ibiden's share is 85% to 55% over three years.

The interposer and CoWoS process: TSMC (TSM), with outsourced spillover to ASE / SPIL (https://t.co/wC05wori4M), Amkor (AMKR), Powertech (https://t.co/dGu3NZXbUO).

The hybrid bonding step: BESI (BESIY / https://t.co/P7EXczR8Nt), with KLIC (Kulicke and Soffa) as the secondary equipment vendor.

The 3D metrology for HBM stacking: Onto Innovation (ONTO), Camtek (CAMT), Nova (NVMI).

The encapsulation chemistry that prevents the package from melting: Sumitomo Bakelite (4203.T), Shin-Etsu (4063.T), Nitto Denko (6988.T).

The PCB the package sits on: TTM Technologies (TTMI), Unimicron (cross-listing), Ibiden (cross-listing).

The 800G/1.6T optical chipsets: MACOM (MTSI), AAOI, Marvell (MRVL), Credo (CRDO).

The lasers feeding optical engines: Lumentum (LITE), Coherent (COHR), Sivers (https://t.co/Y78wp2HOGU), IPG Photonics (IPGP), nLight (LASR).

The InP substrate underneath the lasers: AXT (AXTI), Sumitomo Electric (5802.T / SMTOY), IQE plc (IQE.L), Freiberger (private).

The wafer-level burn-in tooling: Aehr Test Systems (AEHR).

The retimers that keep the signal alive: Astera Labs (ALAB), Credo (CRDO).

The CXL controllers for system-level memory: Astera Labs (ALAB again), Marvell (MRVL again), Samsung Electro-Mechanics (009150.KS), SK Hynix (000660.KS).

The HBM itself: SK Hynix (000660.KS, 62% share), Micron (MU), Samsung (005930.KS).

The cooling at rack scale: Vertiv (VRT), Modine Manufacturing (MOD), LiquidStack via Trane Technologies (TT), CoolIT now inside Ecolab (ECL), Boyd (private).

The power semis converting 800V to 1V on the GPU rack: Power Integrations (POWI), Innoscience (https://t.co/yaXvTyRSv9), Navitas (NVTS).

The high-voltage transformers feeding the substation: Siemens Energy (https://t.co/vB88aXEM2D), GE Vernova (GEV), Hitachi (6501.T), Eaton (ETN), Virginia Transformer (private).

That is the supply chain

The names most generalists could pronounce are the GPU vendor and three or four ETF-level large caps. The actual binding constraints sit in the smaller names two and three layers below.

This is the time of year when a lot of investment firms welcome interns. While our work is geared toward institutional investors, a lot of it can be useful for learning about markets and the investment process. Here are a handful of reports and how they can guide interns:

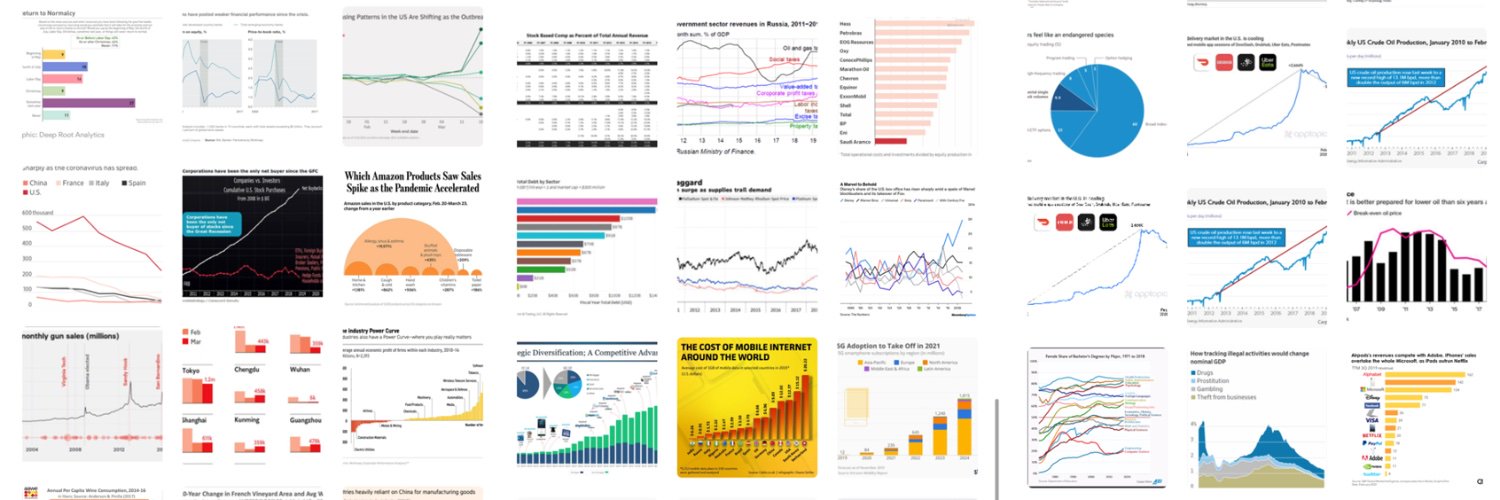

Thoughts from Michael Hartnett, BofA | This Is The Biggest Bubble Since The Railroads

The current AI-driven market rally resembles one of the biggest speculative bubbles in history, comparable to the Nifty Fifty or dot-com era, but investors are unlikely to aggressively sell before two catalysts occur: a major OpenAI/SpaceX-style IPO cycle and a clear Fed policy tightening shock tied to rising CPI from tariffs and inflation.

•AI mega-caps now dominate market concentration, with the “AI bubble” larger than past railroad, Japan, and dot-com bubbles by some metrics.

•Bond yields are the main warning signal: the rise in long-term yields and global cost of capital seen as dangerous for risk assets, especially leveraged consumers, private equity, housing, and emerging markets.

•Several macro stress signals are flashing: weak Asian currencies (KRW, JPY, INR, IDR), widening high-yield spreads, EM outflows, and BofA’s Bull & Bear Indicator hitting a contrarian “sell” level.

•Historically, speculative IPO waves (Alibaba, NTT, Visa, etc.) often marked medium-term market tops rather than immediate crashes.

•Current gains are very narrow (“wealth effect, not wage effect”), while equal-weight consumer stocks remain weak versus the S&P 500.

•Despite near-term bubble concerns, structurally bullish on emerging markets and commodities.

•Preferred post-bubble opportunities would be consumer stocks and smaller AI adopters/disruptors rather than dominant mega-cap AI platforms.

•Geopolitics, energy, AI competition with China, and inflation are increasingly interconnected themes shaping markets.

Zeitgeist quote: “Everyone is now convinced that equities are the best inflation hedge.”

Feedback from recent London trip, main soundbites:

•“we’re long and paranoid,”

•“wants/needs to de-escalate Iran, and stocks pop, yields drop on deal,”

•“if UK gilts find love, everything finds love,”

•“European electorate shifting decisively right, Farage in UK, Le Pen in France, and you watch the AfD in Germany will win Saxony-Anhalt in September, their first state election,”

•“the fear in bonds is nowhere near as strong as greed in equities,”

•“Warsh will be rhetorically hawkish but practically dovish over the summer,”

•“US actions in Venezuela, Ukraine, Iran, Greenland, Cuba should be viewed through single strategic lens competition with China in AI, which can only be won by securing access to critical resources.”