Financing the Global Industrial Renaissance with Apollo CEO Marc Rowan

Marc Rowan is CEO of Apollo Global Management, one of the most important financial institutions and the largest provider of retirement income in the world. In this conversation, he joins a16z's David Haber to discuss the story of Apollo, the state of public and private markets, how the AI revolution will be financed, and more.

00:00 Intro

00:52 Drexel, Milken & the origins of "clean sheet thinking"

04:55 The Apollo origin story: From unemployed to $6 billion

08:46 How Apollo became a trillion-dollar firm

13:00 Permanent capital, origination & why assets are the scarce resource

16:08 Democratizing private markets: Daily pricing & new capital channels

22:04 Where venture meets credit: Financing the industrial renaissance

30:01 AI, enterprise software & which jobs will be replaced or enhanced

38:52 Moral leadership: UPenn, merit & doing right over easy

46:02 Apollo's culture: Playing to win & building to outlast the founder

$583B comp if @elonmusk colonizes Mars.

A $28T TAM. Easter eggs pointing to a Tesla merger.

@AmanVerjee read the 308-page @SpaceX S-1, so you don't have to.

It's a big week. Full breakdown:

[ tech news and vc ]

00:43 - AI holy trinity DGAF ⃤

08:04 - @AnthropicAI profitable, $900B looks cheap 🤯

13:38 - @OpenAI rushes to IPO after courtroom win 🏃♂️➡️

17:53 - @nvidia $82B print $80B buyback 💰🫲

22:20 - @mercury $200M Series D @ $5.2B 🏦

25:35 - US Govt = Quantum VC ⚛️

29:05 - NPM sues Hiive over 2ndry plumbing 🪠

[ val corner: 308 page SpaceX S-1 ]

31:06 - SpaceX S-1 highlights ���🔦

35:56 - $28T TAM includes Martians 🌎🌍🌏🌖✨

37:00 - 3 core biz units: Connectivity, Space, AI 3️⃣

47:05 - SpaceX-@Tesla merger? 🤔

50:10 - board members revealed @IraEhrenpreis @kimbal @AntonioGracias @Gwynne_Shotwell @LukeNosek @rglein @SteveJuvertson0

53:48 - unusual staggered lock-up period 🔐

1:01:00 - @davemcclure sings a whole new Mars to close the show 🎶

Do you dare???

Pitch this "Mean VC" 😈

You'll get rigorous critique that sharpens your strategy, challenges your assumptions, and helps prepare you for IRL investors.

Link: https://t.co/wiT3XFrxnT

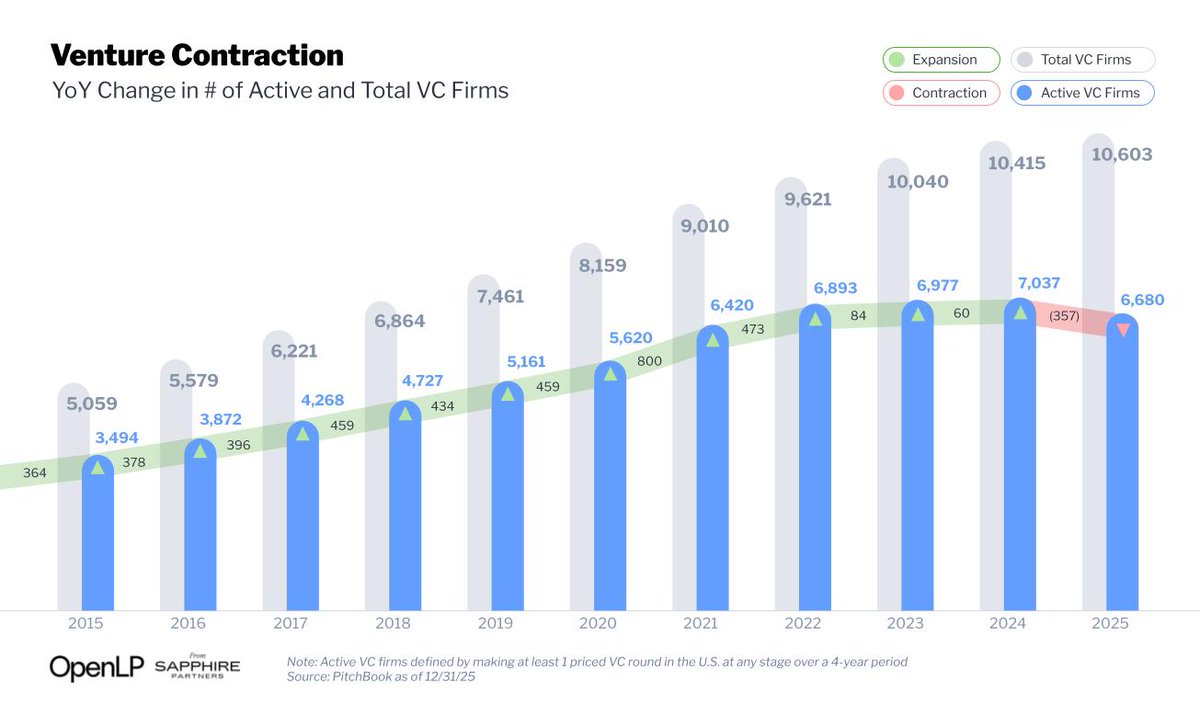

🧵1/ For decades, venture has expanded practically by default: more funds, more managers, more capital.

After 20+ years, we are now facing the first meaningful industry-wide contraction since the dot-com collapse, with the smallest active investor base in more than 25 years.

moolah in the coolah: the science of selling & how to turn tvpi into dpi via secondary sales.

this is just the teaser. full [trading places] ep1 drops tuesday morning.

@davemcclure@AmanVerjee@cupazhou

“winners keep winning. losers keep losing. tweeners keep tweening.”

brutal vc wisdom from @davemcclure on portfolio triage.

be helpful… but be the voice of reality.

full episode soon on [trading places].

the 5 chapters of secondary selling 🧵

never sell

i didn’t sell… and regret it

sell 10–20%

teach your founders

set up your own SPV & sell to yourself

@Jason & @davemcclure break it down on @twistartups

full episode coming soon on [trading places]

“vc marks are bullshit.”

– @davemcclure@Jason says 70% of unicorns aren’t actually unicorns.

@davemcclure says every VC knows

most fund marks are inflated — they just pretend it's only OTHER VC funds which are way off, but THEIRS are "just fine”

[trading places] @twistartups

@Samir_Kaji on what LPs should know about:

- VC is cyclical: consistency beats timing

- Seed funds: sourcing & winning matters more than picking

- New firms created every decade that dominate in the future

- LP diligence requires expertise

Original thread with more insights ⬇️

13 things LPs should know about venture capital.

1/ VC is highly cyclical, alternating between long risk-on periods followed by sudden risk-off periods. Trying to time things is a fools errand, which is why consistency across vintages is required.

2)75-90% of VC funds (depending on the cycle) will underperform top quartile lower middle-market PE funds, especially when accounting for illiquidity/risk.

3)Most LPs would achieve better returns investing in established large/mid-cap tier-1 brands rather than trying to pick individual micro funds. The latter requires expertise and TIME

4) Small seed funds consistently make up the majority of the top 10% and bottom 10% of funds in every vintage year.

5)While DPI (Distributions to Paid-In) ultimately matters most, avoid drawing conclusions from funds <6 years old. Our data shows that some top-performing funds actually took longer to achieve their first meaningful DPI. The Carta and AngelList data is valuable, but being surprised by lack of DPI for 2020+ vintage years shows little understanding of the asset class. Also 2017/2018 DPI is indeed poor, but this reflects the challenging exit markets of 2022-2023. Focus on company quality and wait to judge.

6) Recent posts suggesting that $100M-$500M funds are in "no man's land" are both incorrect and correct at the same time. This applies to firms lacking advantages in brand, domain expertise, or network. There's significant value for founders raising Series A from high-quality mid-cap managers who can provide quality senior partner support.

7) While track records and historical performance provide useful context, in VC, backward-looking analysis almost always leads to suboptimal deployment decisions.

8) A recent LI post citing PitchBook benchmarks claimed 11% of sub-$100M funds achieve 5x returns. This is significantly overstated due to survivorship bias and using small samples as a denominator. The figure is closer to ~1-2%. Funds achieving 5x+ DPI are truly rare.

9) VC faces a significant liquidity challenge and needs to mature in developing better liquidity paths. Extended liquidity timelines are increasingly incompatible with viable risk-returns, especially for those who cannot access top managers.

10) Thea ability gap between top and mediocre/poor VCs is enormous and becomes readily apparent to LPs with sufficient experience. However, since VC often represents only 5-10% of an LP's portfolio, many lack the sample size or network access for proper comparison.

11) Track record assessment requires careful analysis of holding values. Managers' holding valuations can inversely correlate with the firm's fundraising risk. I've seen firms that don't worry much about being able to raise typically maintain more conservative valuation policies. LPs must scrutinize the marks of top portfolio companies driving past unrealized performance.

12) For seed funds having a real edge in sourcing & winning deals can> picking ability. Brand/distribution matter.

13/ Every decade, there is a new guard of firms that come in and become dominant long term forces. 2000's, 2010's saw it, and we are already seeing early signs of breakout new firms in the 2020's.

There are far more things.

13 things LPs should know about venture capital.

1/ VC is highly cyclical, alternating between long risk-on periods followed by sudden risk-off periods. Trying to time things is a fools errand, which is why consistency across vintages is required.

2)75-90% of VC funds (depending on the cycle) will underperform top quartile lower middle-market PE funds, especially when accounting for illiquidity/risk.

3)Most LPs would achieve better returns investing in established large/mid-cap tier-1 brands rather than trying to pick individual micro funds. The latter requires expertise and TIME

4) Small seed funds consistently make up the majority of the top 10% and bottom 10% of funds in every vintage year.

5)While DPI (Distributions to Paid-In) ultimately matters most, avoid drawing conclusions from funds <6 years old. Our data shows that some top-performing funds actually took longer to achieve their first meaningful DPI. The Carta and AngelList data is valuable, but being surprised by lack of DPI for 2020+ vintage years shows little understanding of the asset class. Also 2017/2018 DPI is indeed poor, but this reflects the challenging exit markets of 2022-2023. Focus on company quality and wait to judge.

6) Recent posts suggesting that $100M-$500M funds are in "no man's land" are both incorrect and correct at the same time. This applies to firms lacking advantages in brand, domain expertise, or network. There's significant value for founders raising Series A from high-quality mid-cap managers who can provide quality senior partner support.

7) While track records and historical performance provide useful context, in VC, backward-looking analysis almost always leads to suboptimal deployment decisions.

8) A recent LI post citing PitchBook benchmarks claimed 11% of sub-$100M funds achieve 5x returns. This is significantly overstated due to survivorship bias and using small samples as a denominator. The figure is closer to ~1-2%. Funds achieving 5x+ DPI are truly rare.

9) VC faces a significant liquidity challenge and needs to mature in developing better liquidity paths. Extended liquidity timelines are increasingly incompatible with viable risk-returns, especially for those who cannot access top managers.

10) Thea ability gap between top and mediocre/poor VCs is enormous and becomes readily apparent to LPs with sufficient experience. However, since VC often represents only 5-10% of an LP's portfolio, many lack the sample size or network access for proper comparison.

11) Track record assessment requires careful analysis of holding values. Managers' holding valuations can inversely correlate with the firm's fundraising risk. I've seen firms that don't worry much about being able to raise typically maintain more conservative valuation policies. LPs must scrutinize the marks of top portfolio companies driving past unrealized performance.

12) For seed funds having a real edge in sourcing & winning deals can> picking ability. Brand/distribution matter.

13/ Every decade, there is a new guard of firms that come in and become dominant long term forces. 2000's, 2010's saw it, and we are already seeing early signs of breakout new firms in the 2020's.

There are far more things.

@gokulr@gokulr could this lead to short term thinking? point (c) is probably the most critical factor…a lack of quality tech stocks in India may have led to this inflation in tech valuations… the problem may be in the Indian stock market…

@IbrahimAjami@mikeeisenberg Admiting to mistakes is admirable (and common in SV)… but not sure this absolves anyone…2020 and 2021 vintages were obvious mistakes to most professional VC’s at the time….

Best part of this episode was @DavidSacks maintaining intellectual integrity and highlighting that “woke-ism” and “mob mentality” have existed on both the right and the left of the political spectrum for a long time …

https://t.co/0KlS0ckcpc

VC EMs that are not spin-outs: Family Offices are your most likely investors. Remember these 4 things:

1) For most FO's, VC is a participation sport and often as important as the returns are. The service/experience can be everything. You can differentiate through better reporting, community efforts, transparency, and touch.

2) Get to really know them before you start pitching what you do. Ask questions about their background, and understand what they care about before going into the pitch. Still see too many EMs go right into pitch mode. You can't offer a product unless you know who you are speaking to and what they care about.

3) The strategy is different when speaking to the principal vs. investment team member. For the former, you need to make sure to find common ground, and connect with the heart. For investment folks, you need to make sure you understand their incentives.

4) Don't burn bridges. Sometimes FOs go through changes on the fly. I've seen some GPs get upset when people pass. Don't. Sometimes it's truly a "not now".