eating glass and staring into the abyss with @mikebelshe and the entire @bitgo team and our incredible investors. it has been an honor.

now the real work begins.

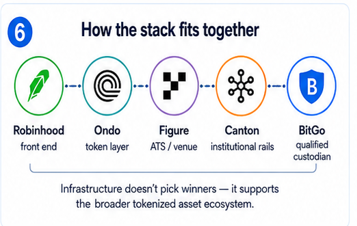

we. are. infrastructure.

Great thread by BitGo's Belshe, literally threads BitGo's role in Tokenized Asset Infrastructure

I already reshared it but this time made it into an infographic, check it out !

The future of finance is here & $BTGO is the Backbone

🧵

It's wild that we let customers experience FSD coast-to-coast themselves.

No professional production, just a normal drive.

Yet to me, this is a bigger step change than AlphaGo or GPT, as there's no special machine behind it—it's something you can buy today.

On the remarkable return on capital potential for Starlink on Starship.

Including customer acquisition cost, ground station capex, and an expendable top stage, we think SpaceX should be able to launch its 10th commercial starship rocket for ~$500m.

The bandwidth it launches could yield $1.2 billion in revenue annually for as long as the satellites are in orbit. 13x cash on cash return.

For a time (100 launches or so) cash requirements per kg (and per tbps) of launch should roughly keep pace with the revenue decay in monetizing incremental orbital comms throughput. Basically, their per launch cost decline, driven by rocket upsizing, satellite manufacturing efficiency and full re-useability, should out-compete declining ARPU (or at least keep pace).

Net, very crudely, it works to the company being able to deploy $50b in capital building satellites, launching rockets and acquiring customers at a ~13x cash on cash return over a few years.

This is a business without precedent.

Composer 2.5 being Pareto dominant in coding per CursorBench is important.

This is after only a few weeks of supplemental training and/or RL in the Colossus 2 cluster.

The 1.5 trillion parameter version of Grok will likely be a much better base model than Kimi. We shall see.

.@ashleevance says @elonmusk "has no time zone."

"We were at Neuralink filming something for a movie I'm making and were there until 1AM. Then he went straight from there back to xAI."

"Then I had a friend who met with him at 4AM."

"He lives life constantly like that."

🚨 MICHAEL BURRY JUST WARNED THE ENTIRE AI BOOM MAY BE BUILT ON TEMPORARY DEMAND.

He published a post today calling Nvidia "the North Star, Orion, the whole Milky Way" and explaining why that makes it the most dangerous stock in the market right now.

His core argument is:

Nvidia is selling into a concentrated group of buyers Microsoft, Google, Amazon, Meta who are all racing to buy chips not because they need them for real revenue generating products right now, but because they are in a training and benchmarking phase that will not last forever.

Hyperscalers currently account for approximately 50% of all Nvidia data center revenue.

When the training phase ends and these companies shift from building AI to deploying it, the demand profile changes completely.

Burry calls this the "bullwhip effect." When the buyers at the end of a supply chain over order because they are afraid of missing out, the distortion amplifies all the way back through the chain.

Nvidia sees record demand.

Nvidia locks in massive custom supply commitments. Data center financing expands to accommodate the buildout. Everyone bets the demand is permanent.

Nvidia just reported $81.6 billion in quarterly revenue, up 85% year over year. Data center revenue alone was $75.2 billion, up 92%. The numbers are real but the question Burry is asking is whether the demand behind those numbers is structural or temporary.

He calls it the "bezzle." A term coined by economist John Kenneth Galbraith to describe the gap between what people think they own and what actually exists.

In a bezzle, the money feels real, the assets feel real, and everything looks fine until the moment it does not.

Historically the semiconductor industry is highly cyclical.

The persistent fear among analysts is that the current build out phase of AI will eventually lead to oversupply of computing power and when that happens the whiplash into Nvidia's revenue could be severe.

Burry has been wrong on timing before. He called the market a sell in 2023 and it went up 131% since then.

But the 2008 mortgage crisis he predicted also looked like a timing mistake for two years before it was not.

The difference this time is that he is not just making a macro call. He is pointing to a specific mechanism, concentrated buyers, a temporary demand phase, and custom supply commitments that create obligations on both sides and saying the math only works until the training phase ends.

Nvidia trades at 33 times forward earnings on $81 billion in quarterly revenue.

If hyperscaler capex slows even 20%, that math changes very fast.