"There's 20 other search engines: Yahoo big winner, Altavista, Excite, Lycos, etc. We don't understand why the world needs another one. We don't get what you guys're doing: a blank page, a colourful logo, a bar and two buttons...No sports scores...no horoscope?!"

—VCs circa 1999

It’s wild that the most profitable webpage on the internet is made of a textbox, one useful button, and another useless joke button. And it hasn’t changed in 20 years.

This is so true. I lived this.

Functionally, my career as a "hedge fund guy" was over at 32. I built my ego around being a rising star, working at blue chip hedge funds, big bonuses, living the hedge fund lifestyle (fancy dinners, Hamptons share, brokers rolling out the red carpet).

A bad career decision, a few bad trades, and not only did my self identity shift from "rising star" to "damaged goods", but my nervous system was so shot that I couldn't even muster the energy for a comeback attempt.

I pulled the plug and moved my family from NYC to Arizona. I thought the change of scenery & lifestyle would be an immediate balm to the the angst I felt inside. Instead, things got dark, and really for the first time in my life, I struggled with depression.

My advice to anyone who peaks early is the criticality of a new dimension of purpose. For me, three young sons (at that point, 6, 4 & 6 months) and a loving & supportive wife were the critical elements that kept me on track, and got me back on track. And, in retrospect, the pain was the biggest gift I've ever received, as it drove a deep exploration of spirituality & the true architecture of the universe. I had time and space to explore questions I never had time to explore before, like "Who am I and why am I here?".

A UNIVERSITY HOMEWORK ASSIGNMENT IN TURIN BECAME ONE OF THE BIGGEST NETWORK TOOLS ON GITHUB.

His name is Giuliano Bellini. Computer engineering student at Polytechnic University of Turin. Course: System and Device Programming.

The assignment: write a small program that logs network traffic to a file. Command line only. Submit it. Get a grade. Move on.

Most students did that. Giuliano didn't.

After he turned the project in, he kept working on it. Added a GUI. Added geo-location. Added a real-time chart. Added protocol detection. Added 24 language translations. Added webhook notifications. Added PCAP import that runs 2X faster than Wireshark.

Three years later, GitHub picked it for their Accelerator Program and he started working on it full-time.

He called it Sniffnet. Sniffer + network.

Today:

→ 33K GitHub stars

→ 1.2K forks

→ 2,771 commits

→ 64 contributors

→ 24 supported languages

→ 16 official releases

→ Sponsored by NLnet, ADS Fund, and IPinfo

→ Featured by Windows Central as a free GlassWire and Wireshark alternative

His bio still says "pasta addicted, can't resist a good plate of spaghetti." His README still calls it "comfortably monitor your Internet traffic."

The whole thing is written in Rust. 98.8% of the codebase. MIT and Apache-2.0 dual licensed.

He refuses to add ads. He refuses to add telemetry. He refuses to lock anything behind a paid tier.

A homework assignment from Italy is now used by network engineers in every country with internet.

This is what coursework was supposed to lead to.

Repo in the first comment.

NOW FREE - My highest conviction idea 🇯🇵

Tobila Systems $4441.T $4441.JP

Smoak Capital (@dsmoak98) just published an excellent summary (link below).

Daniel at Smoak Capital has an exceptional 37.4% CAGR since 2018!

Smoak Capital owns 7.3% of Tobila.

Disclaimer: Personal opinions only, not investment advice.

Links to Smoak Capital Letter and my own writeup below:

Been reviewing Japanese longs all morning.

Look at this example Tanabe Engineering $1828. It now trades for 7x earnings with 16% return on capital. It has a 4.5% dividend yield. They tripled operating income in a decade.

There are so many companies like this, from unrelated industries, that peaked exactly at the end of February.

This type of small cap Japanese value / GARP stock is in a bear market. This one had a 25% drawdown.

Worst VC behaviour I’ve seen in a portfolio company:

A euro VC limited founder salaries to a very low level (<$100k).

Founders then received a 9 figure acquisition offer.

VC tried to block the deal as was only a 4-5x for them.

I and other angels told them in no uncertain terms that we would go scorched earth on their reputation if they blocked the deal.

The worst part: they failed to connect the fact that their miserly salary cap was likely the cause of the founders wanting to accept the offer.

One of the founders was still renting a 1 bed apartment at this time and had a bunch of credit card debt.

You should want your founders to be financially comfortable post series A so they can really swing for the fences…

Wait. Google is paying SpaceX $920 million per month for GPUs?

Google. The company that builds its own TPUs. That runs one of the largest cloud infrastructures on earth. Is renting 110,000 Nvidia GPUs from a rocket company.

I'm honestly not sure what to make of this. Either Google's AI compute needs have gotten so massive that even they can't build fast enough. Or SpaceX has built something in AI infrastructure that nobody was paying attention to. Or both.

$920M a month. $30B over the contract.

Whatever is happening behind the scenes at these companies is moving way faster than what we see publicly.

$6135.T In a March interview, Makino's sales executive said: “We’ve heard about Starlink-related components, so that might be a positive development for our company as well.” I checked, and he is right - SpaceX likely uses Makino's machines to make Starlink satellites.

SpaceX manufactures Starlink satellites at the dedicated facility in Redmond, Washington. GPT 5.5 helped me unearth local county permit records, which show new foundations for relocated machinery and related fire-alarm alterations in early 2025 under the project name "SPACEX SE03 - MAKINO EXPANSION AND HITL".

In addition, SpaceX is looking for experienced machinists for the Redmond facility to operate multi-axis CNC machines, including 5-axis mills and 6-axis lathes.

This convinced me that Elon is also a fan of Makino's gigantic "mother machines".

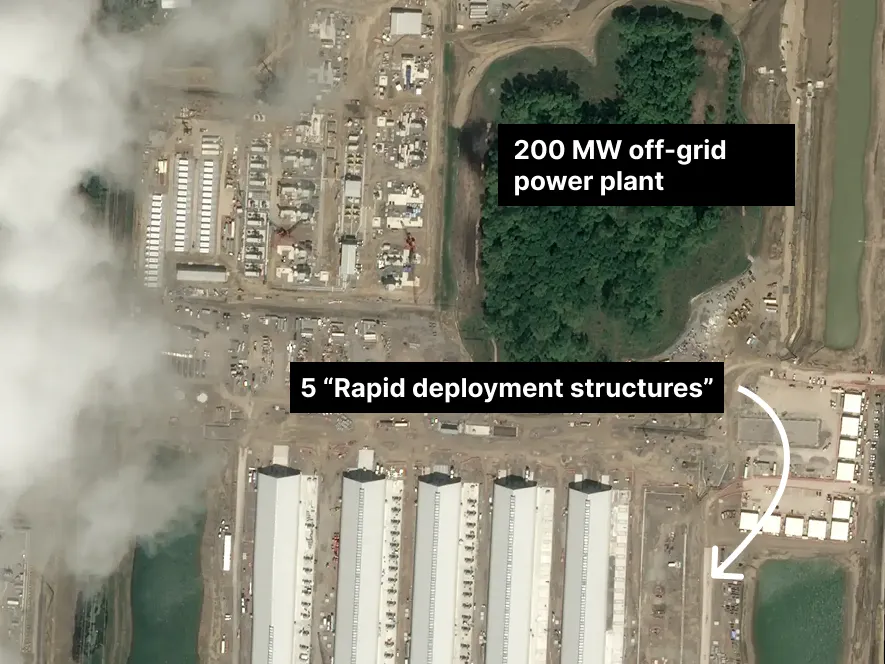

Meta is building dozens of massive tents at campuses across the US, sticking billions of dollars of chips inside, and powering them with off-grid turbines.

The AI race has officially entered its Mad Max phase.

Over the last month, I reviewed hundreds of documents and satellite images for Cleanview's latest report on behind-the-meter data centers. Meta's data center strategy, which is very visible from space, was one of the weirder approaches I came across.

Mark Zuckerberg recently ditched the data center designs that Meta had perfected over the last decade and told his team to stick tens of thousands of chips in tents outside their data center in New Albany, Ohio. Each of these chips costs about $60,000. Zuckerberg plans to stick billions of dollars worth of them in the tents.

The strategy has helped cut the time to build compute in half. The first five buildings at Meta’s New Albany, Ohio data center took between two and three years to build. Meta started building five ~125,000 square foot tents between April and June of 2026, according to city permits. Satellite images show the structures have all been built.

To power those "rapid deployment structures", as they are officially named, Meta signed a 10-year deal with Williams to build a pair of 200 MW off-grid power plants. Those power plants began construction about a year ago and are nearly complete.

Meta is using the same strategy to build a data center in Tennessee, bringing the total count of tent data centers to three.

Strategies like this are part of the reason behind-the-meter data center capacity is growing so quickly.

In Cleanview's report, I found that there's currently about 2 GW of BTM capacity online today. By the end of the year, it will likely be 3 GW—equivalent to three nuclear power plants. By the end of 2027, it could be as high as 13 GW—more than the power demand of NYC.

I've been talking to a lot of reporters about this research. When I told one reporter about these tents and other companies powering their data centers with jet engines, he said, "It's like a scene out of the movie Mad Max."

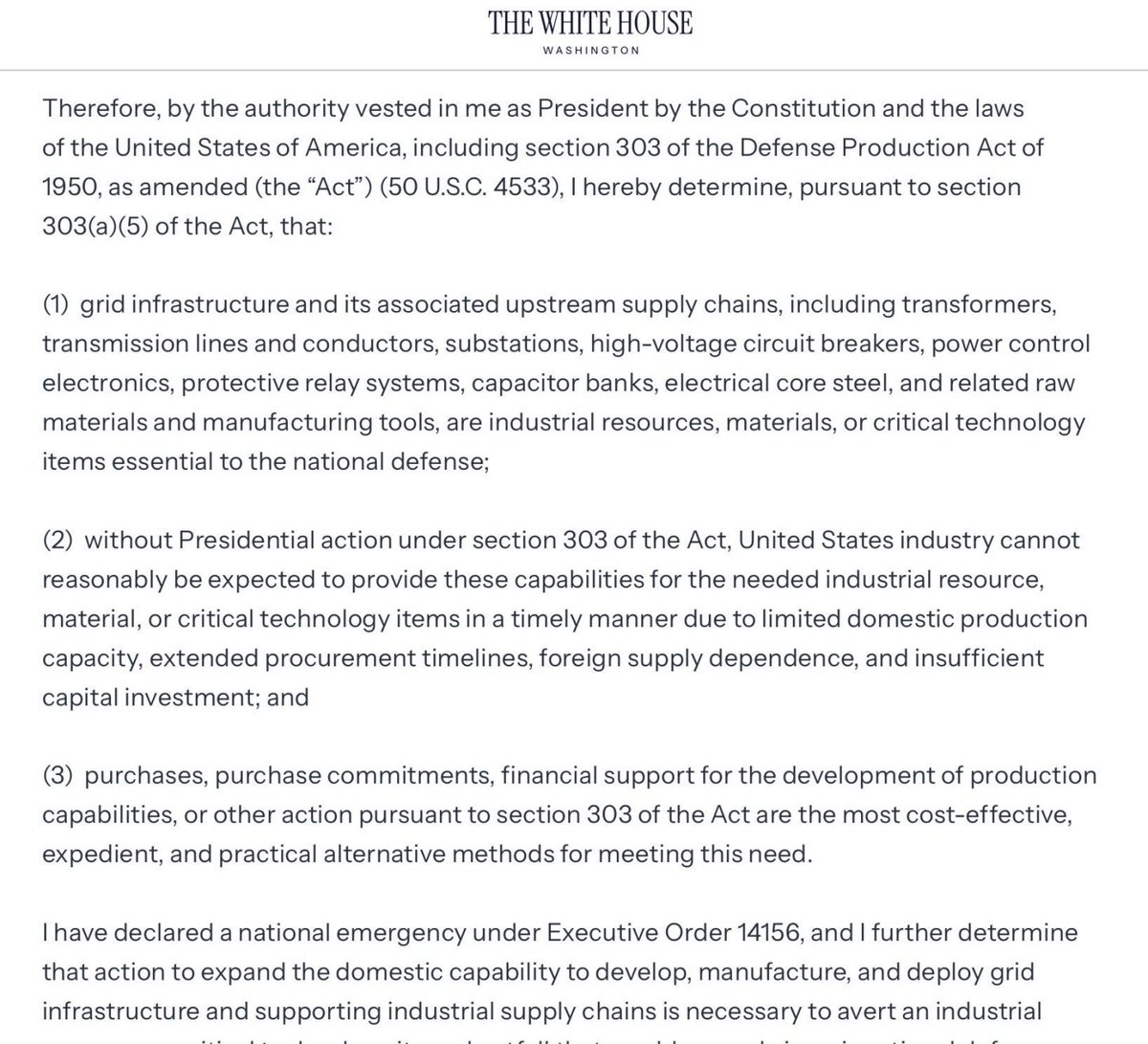

Defence Production Act Cheat Sheet.

3 major hurdles the government is stepping in to solve are Limited Domestic Capacity, Extended Procurement Timelines and Insufficient Capital Investment.

Tickers:

$CLF $X $GEV $SMERY $SPXC $PWR $HUBB $ETN $EMR $ENPH $SEDG

Cheers.

There is one factory in America that produces the magnetic steel inside large power transformers.

Cleveland-Cliffs. Butler Works. Butler County, Pennsylvania.

That steel — Grain-Oriented Electrical Steel (GOES) — represents roughly 25% of a large transformer's manufacturing cost.

Current lead times for large power transformers: 1 to 4 years, averaging 128 weeks. Historical baseline: 6 to 12 months. Price inflation since 2019: +77%.

Hyperscalers have stopped waiting. They're funding private HVDC networks and vertically integrated suppliers that can deliver equipment in 12 to 36 weeks.

The AI buildout isn't constrained by chips right now.

It's constrained by steel. One factory. One state.

$MIAX is the kind of business that could be a legitimate multi-bagger from here over a 5 or 10 year time horizon. Best in class economic characteristics that are very similar to a royalty. Also vetted and owned by some of the best minds in the game, Horizon Kinetics.

Just a reminder: $MIAX has a hidden optionality you currently get for free.

Bloomberg reported today that $HOOD is routing some of its World Cup bets through Rothera instead of Kalshi. And Rothera is the former MIAXdx, MIAX sold it at the end of 2025 but kept a 10% stake.

Meaning: MIAX offloaded the risk but held onto a piece of the upside.

And the timing fits: Robinhood has already processed more event contracts in 2026 than in all of 2025. The World Cup starting June 11 will be the next catalyst.

While everyone sells on irrational perpetual-futures fears, a prediction-market stake is quietly growing in the background

https://t.co/bET3YwUuKB

The selloff in the high moat, compounder names is getting ridiculous. The irrs I get for some of these co's as long as they don't royally shit the bed are pretty attractive. Stuff like $SPGI, $MA, $V, $BR and now add $CME, $CBOE and $ICE with their recent selloff. Steadily adding

$ILYDA.gr cheapest software stock at all universe?

✅Trading at 10 P/E on 2025 results with 30% growth,if you adjust for differed revenue the real growth is 45%

I think will growth at least 25-30% at 2026 with another op leverage, so 7 P/E on 2026 results

Big optionality also on international expansion which can double share price overnight if succeed

Owner operator workaholic who take market share from Epislon and Entersoft

Not recommendation to act

$brun guiding to FCF margin of 20% with arr at least tripling. $470MM ARR contracted for 2026, likely to exit closer to $800M. If they grow 2x next year (implying much slower growth ie conservative), the stock is like 10x FCF on 2027 exit rate.

Stock going much higher. Bought more today. $100 by year end seems realistic $200 next year

@burningbushcap

One of the most overlooked chokepoints in the quantum computing supply chain sits inside a £300M UK small-cap that almost nobody discussing quantum stocks owns.

Gooch & Housego (LSE: GHH)

While investors chase companies promising to build quantum computers, Gooch & Housego supplies many of the optical components that make several leading quantum architectures possible in the first place.

The company is not betting on a single qubit modality.

Instead, it sits upstream of the ecosystem, supplying precision photonics, crystal technologies, acousto-optic devices, and RF-integrated optical systems required across trapped-ion, neutral-atom, scientific, defense, and advanced laser applications.

The Bottleneck:

Quantum computers are ultimately physics machines.

Trapped-ion systems require highly precise laser control. Neutral-atom systems rely on optical tweezers, beam steering, modulation, frequency shifting, and atomic manipulation at extraordinary levels of precision.

Many of these functions are enabled by acousto-optic devices built around highly specialized tellurium dioxide (TeO₂) crystals.

Gooch & Housego is one of the few companies in the world capable of growing, processing, and integrating these crystals at the performance levels demanded by advanced quantum systems. The company controls the entire manufacturing chain, from crystal growth through polishing, coating, transducer bonding, and final RF integration.

This vertical integration is difficult to replicate and creates meaningful barriers to entry for potential competitors.

Each new generation requires more optical control channels, more modulation, more beam steering, and increasingly sophisticated photonic architectures.

Why It Matters:

One of the largest bottlenecks in neutral-atom quantum computing is moving atoms throughout a quantum processor without degrading qubit fidelity.

Gooch & Housego sits directly inside that challenge.

The company is participating in the development of Acousto-Optic Lens (AOL) systems designed to enable high-performance 3D atom shuttling. These systems require specialized ultra-flat TeO₂ crystals and advanced RF control architectures that few suppliers can manufacture.

The company is also developing blue-wavelength fiberized optical switching technology designed to replace bulky free-space optical setups that currently limit scalability in trapped-ion systems. If successful, this could help move quantum hardware from laboratory-scale deployments toward more automated and manufacturable architectures.

Financials:

• ~£297M market capitalization

• ~£150M annualized revenue

• Positive net income

• Dividend-paying business

• Trading at roughly 2x sales versus dramatically higher multiples across many quantum pure-plays

• H1 2025 revenue grew 11.4% year-over-year to £70.9M

Catalysts:

• Scaling of trapped-ion quantum systems

• Scaling of neutral-atom architectures

• Blue-wavelength optical switching commercialization

• Growth in defense photonics demand

• Integration of Phoenix Optical Technologies and Global Photonics acquisitions

• Expansion toward higher-margin subsystem offerings

Risks:

• Quantum commercialization may take longer than expected

• Exposure to industrial and semiconductor spending cycles

• Competitive pressure in certain photonics markets

• Tariff and geopolitical supply-chain risks

The Setup:

Most quantum investors focus on who will build the winning quantum computer.

Far fewer focus on who supplies the physical control layer required by multiple quantum architectures simultaneously.

Gooch & Housego doesn’t need to predict which qubit modality wins.

Its bet is simpler: if trapped-ion and neutral-atom systems continue scaling, demand for the optical infrastructure controlling them may scale alongside them.

A profitable photonics company quietly sitting upstream of one of the most technically demanding industries in the world.

$GHH

Not financial advice. Do your own due diligence

The SMR optionality for $KSB is more concrete than just a CEO statement. In January 2025, KSB signed a letter of intent with the Swedish developer Blykalla to develop specialised pumps for its lead-cooled SEALER reactor (55 MWe) pumps are considered one of the most critical components in liquid-metal-cooled reactors, meaning reactors that use a hot, liquid metal instead of water as coolant. Notably, KSB is not starting from scratch here: its own technical lexicon documents concrete design knowledge for sodium pumps (free fluid surface with inert-gas protection, liquid-metal-lubricated hydrostatic bearing, rated for 580°C) a legacy of Germany’s historical fast-reactor programmes. Together with its canned-motor technology and the sealless wet-rotor RUV, KSB thus holds a rare competence base covering both liquid metals (lead and sodium).

The chain becomes interesting through the second link: in September 2025, Blykalla entered a strategic partnership with the US SMR developer $OKLO expanded in March 2026 to a planned US investment of $100-200 million, including a joint search for suppliers of “reactor-agnostic” equipment. Since KSB is Blykalla’s pump partner and holds both lead and sodium competence, this creates a logical, if early, path into the most prominent US SMR story. Oklo, long chaired by Sam Altman, is one of the most visible vehicles of the AI-driven nuclear renaissance and holds a power purchase agreement with Meta. Both reactor developers explicitly target hyperscalers and data centers. Blykalla’s investor base includes Japanese data-center operator KDDI as well as the co-founders of AI cloud hyperscaler CoreWeave. Through the Blykalla-Oklo axis, KSB thus moves a step closer to a direct SMR-data-center connection, rather than participating in the AI boom only indirectly via the four capex pillars, though this optionality should be assessed on a multi-year horizon.

But for now, it’s just optionality.