$SPGI, $CME, and $ICE are three very high-quality companies that the market has been punishing lately. The market seems to generally dislike financial infrastructure companies at the moment. The reasons why this sector is out of favor are multifaceted. Fears of increased competition, AI disruption risk, and a rotational shift away from the sector all seem to be playing a role.

I don’t find these reasons convincing. These companies benefit from very strong network effects that create what I consider to be some of the strongest moats in the world. Trading on exchanges relies on having a lot of buyers and sellers in order to create liquidity and reduce bid-ask spreads. Once an exchange becomes the clear leader in a particular market, there is little incentive for someone to use a different exchange. Even if a competitor charges lower fees, the cost savings can be more than eaten up by higher spreads, meaning the leading exchanges remain the lowest cost option. This explains why $CME and $ICE have such strong moats.

Network effects also play a big role in credit ratings. S&P and Moody’s are the most widely accepted benchmarks for credit ratings, meaning some debt investors will only consider buying debt if it is rated by one of those two. More potential buyers drive down the cost of issuing debt, meaning issuers have a major financial incentive to use one of them. Even if other credit rating agencies offer lower fees, S&P and Moody’s remain the low-cost leader when considering the total cost of issuing debt, not just the fees to the credit rating agency but also the interest rate the issuer has to pay on the debt. Regulatory mandates benefit those two as well.

Indexes also rely on network effects. The S&P 500 is the most well-known index for the United States stock market. Network effects benefit it in two ways. First, the more the media, investors, and others refer to the S&P 500, the more people know about it and generally associate it as the index for the United States stock market. This leads to many people picking a fund that tracks the S&P 500 because it is the benchmark they hear and read about most often. Similarly, because so many people invest in S&P 500 index funds, there is immense competition between fund issuers, and this competition drives down costs. Also, massive economies of scale allow for the cost of operating the funds to be spread out among a wide base. The result is that numerous index funds are available that track the S&P 500 that have incredibly low management fees. These low fees add another incentive for people to choose them.

The market is overly discounting the strength of these companies’ moats. Leading exchanges, credit ratings, and indexes are very hard to disrupt. It isn’t impossible, but I find it unlikely and currently don’t see any sign of them being disrupted.

This is not financial advice. This is just my opinion.

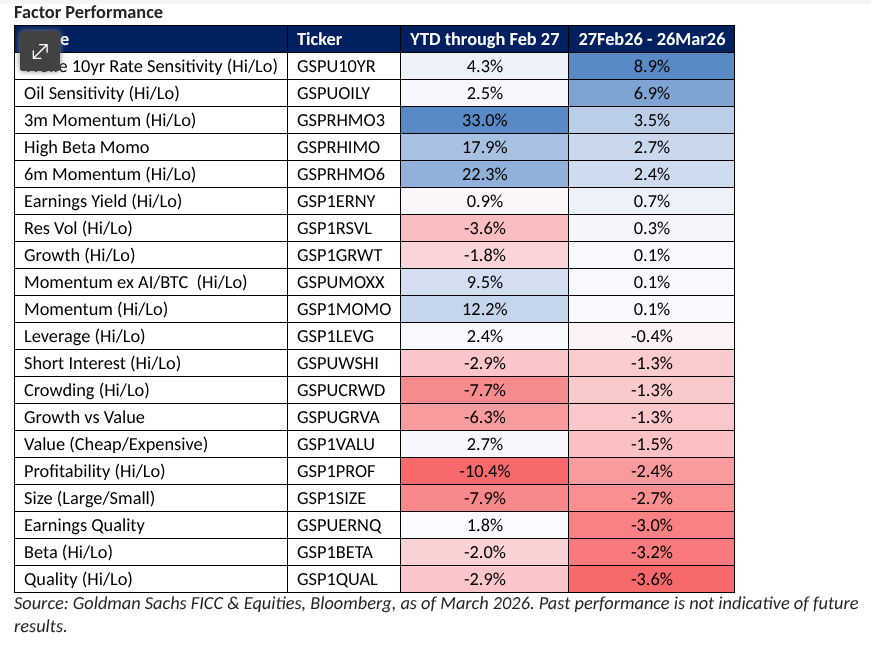

Not a new observation but journaling it here. In the tech bubble sucked capital from every corner of the market and eventually when it reversed it went back; lot of value hedge funds made their careers then (Einhorn etc). You see the same dynamic out there in today's market.

No idea if it reverses or when but there's lots of inconsistencies out there, prime one that comes to mind is the massive debt financing coming to fund the buildout and yet $MCO and $SPGI trade inversely to the AI factor basket.

every job will turn into explaining your intentions to ai

explaining what you want to ai is surpringly time consuming, coders already spend 80% of their time doing it, and this will be true for everyone

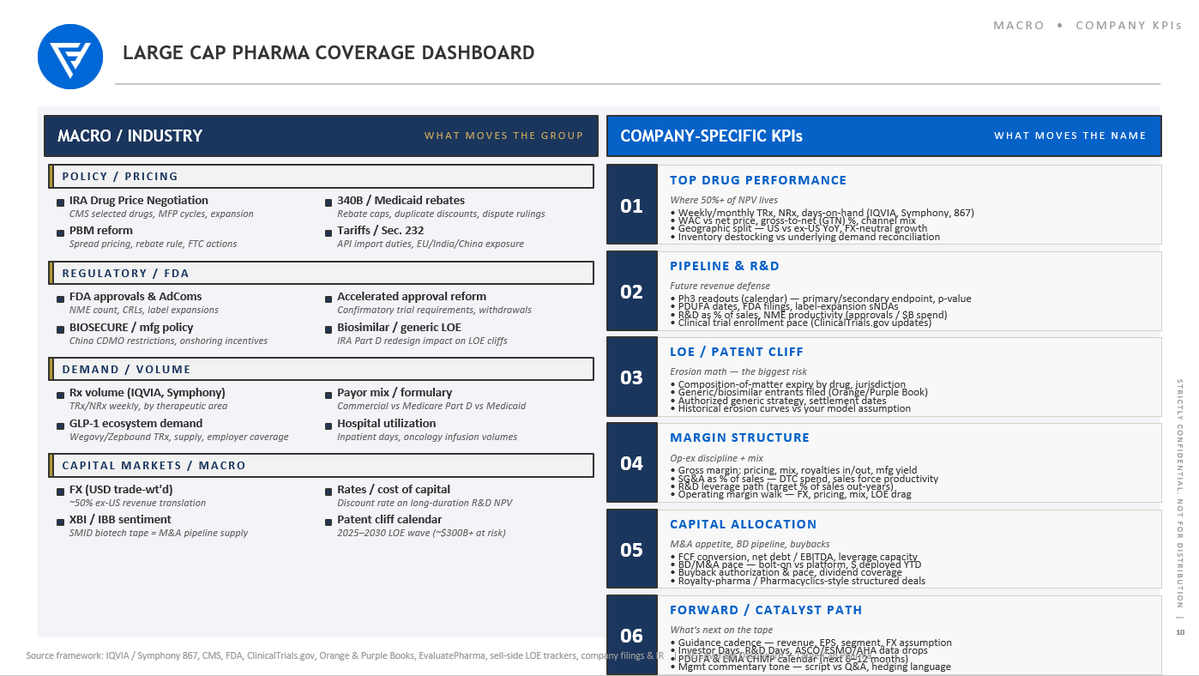

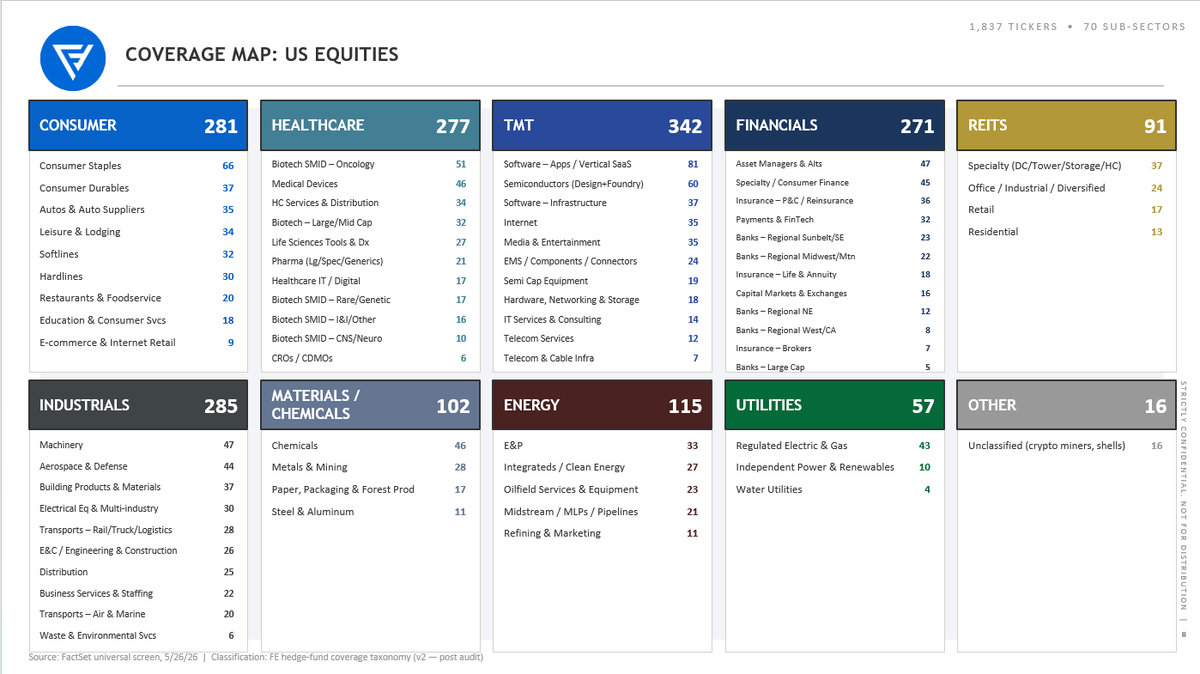

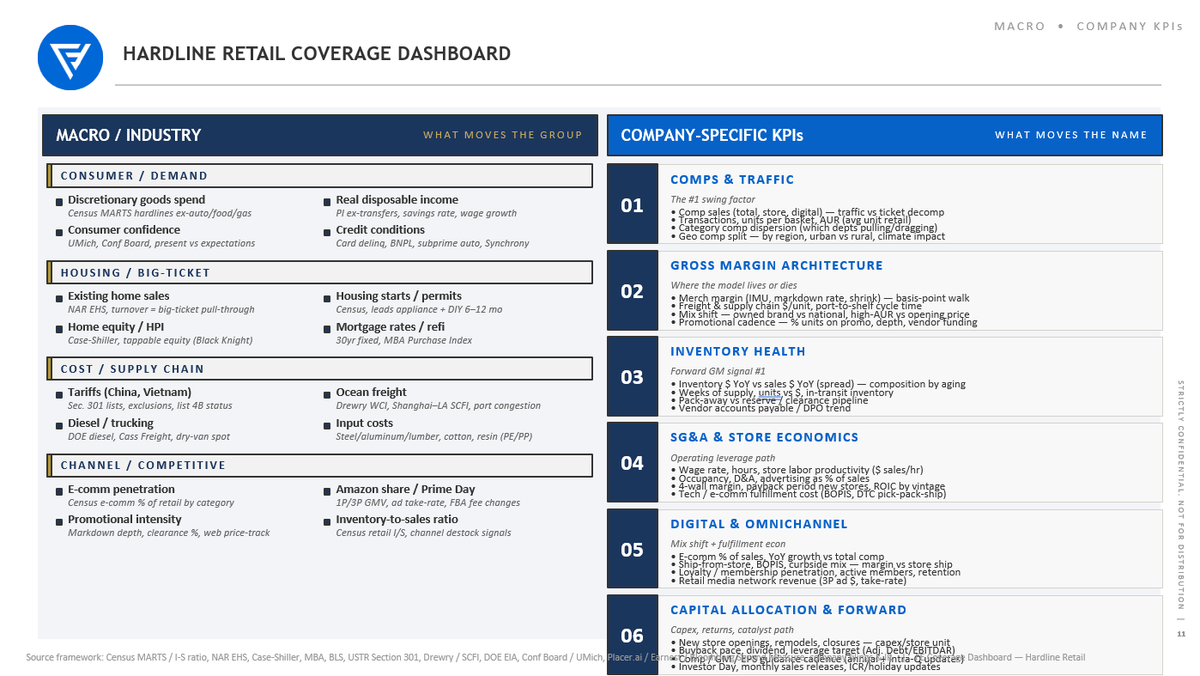

Sharing a few screenshots from one of the more ambitious projects I'm working on right now with respect to agents & investment process: creating coverage dashboard prototypes for all 70 US equity sub-sectors, breaking dashboards into "What Moves the Group" and "What Moves the Name".

I think most technologists don't quite comprehend the investment process differences between a SMID biotech pod analyst vs. a long only midstream MLP analyst vs. an Asian financials Tiger Cub analyst. Public equity investment process is highly heterogeneous and the combinatorial complexity (~a dozen different investors archetypes in ~70 different sub-sectors) hasn't lent itself to easy augmentation with chatbots. Mass customization from a pool of universal process primitives with Agents is a key unlock and I'm wondering how much pre-configuration will happen vs. a thousand flowers blooming from blank agentic workspaces...

My belief: if internal AI teams or vendors can pre-configure coverage dashboards to be immediately value added to the investment process, this forces the agentic "aha moment", accelerates diffusion of agents into investment process, and requires approximately zero time & focus from the investment team (the leverage happens on the back end). Also, if the user interface is configurable, the path to customization from this starting point is immensely easier than solving the blank page problem.

This is VERY conceptual on "what to build" and weak on "how to build", but I'm at the stage on some of this where I am beginning to explore both partnerships with builders and co-development with investment firms.

Please reach out via DM if this resonates.

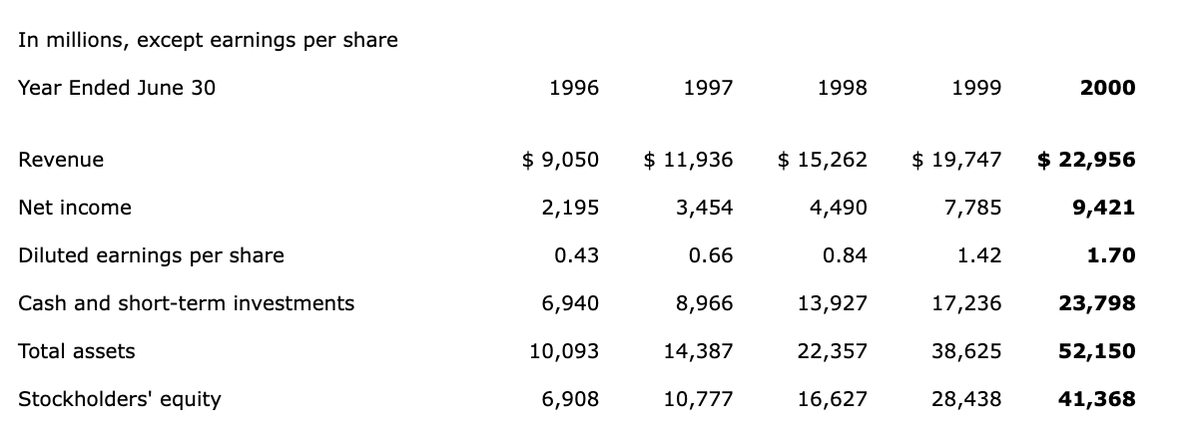

One of the biggest myths concerning differences between today's tech rally and the '90s version is the belief that today's companies are "real" whereas similar companies in the 90s were all fugazi. That is simply not true:

- $CSCO revs ($19,928) +55% and net income + 32% in fiscal 2000

- $MSFT revs ($22,956) +16% net income +21%

- Lucent revs +12%

- SunMicro revs ($15,721) +33% and oper inc +57%

- $ORCL revs +15% net income +380%

- $QCOM revs +12% EPS + 31%

- $EBAY revs +92% net income +400%

- $YHOO revs +88% net income +48%

- $DELL revs +38% net income +14%

- $IBM revs +1% net income +5%

- $INTC revs +15% net income +44%

- $AAPL revs +30% net income +31%

*-This is from annual reports. I'm not accounting for any mergers or other adjustments that may or may not have occurred during the year. Its sunday.

Of course, we know about the many companies that were not making money. https://t.co/BdXj8gXMT5, https://t.co/OJ3UsKjigG and Webvan lost money (even though revs were up 1,200%); even $AMZN lost money.

This is not to say today's companies (i.e. $META, $GOOGL, $AAPL, $SNDK, $VRT, etc) are not comparatively "better" companies because they probably are. I would simply argue companies at the top of the index in 1999/2000 were very much "real" and should not be dismissed simply because of what ensued.

@DivesTech@michaelsantoli@carlquintanilla@RiskReversal@GuyAdami@lisaabramowicz1@Chartfest1@dmoses34

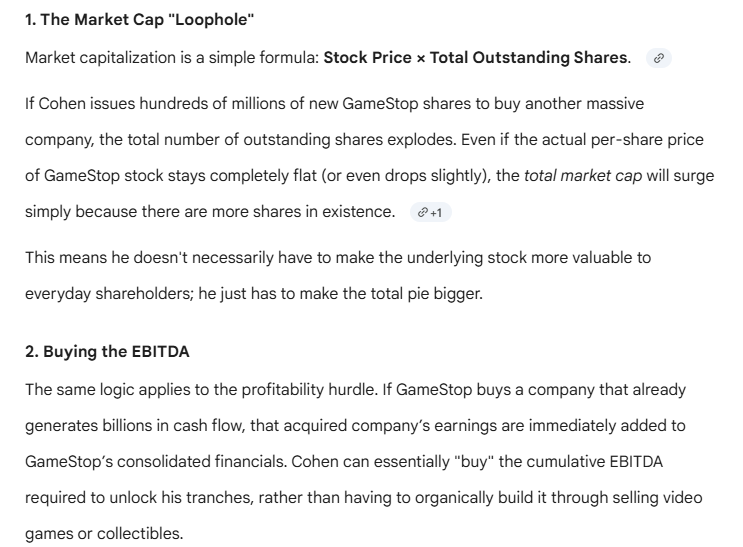

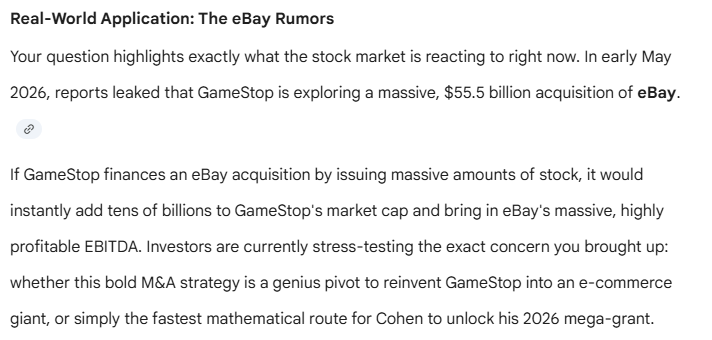

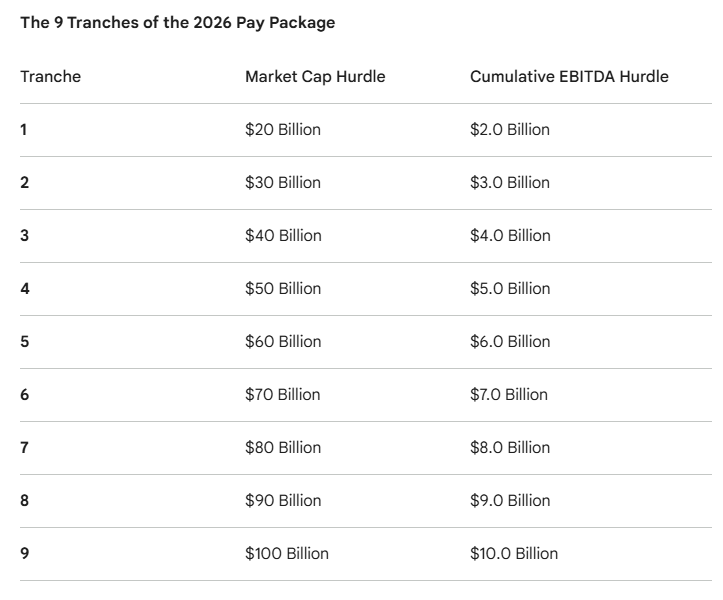

The $GME situation is wild.

The CEO Ryan Cohen has an options package for 171m shares that he can earn if he hits certain market cap and EBITDA hurdles.

The crazy thing is that this is not adjusted for dilution. He needs the market cap to be $20b to get the first tranche but he can just issue a crapload of shares!

This is why he wants to buy $EBAY.

Must read from @akramsrazor

The market has completely given up on trying to figure out who wins from AI. It will only buy the inputs. But:

"If you can't make money in every software, adtech, media, info services biz, and hyperscaler, then why are you buying lasers and cables? The picks-and-shovels trade isn’t insulated from the demand/return question, it's a levered bet on it."

People are surprised that $MU is down on stellar tripled yoy revenues. But they are quiet about the fact price is up like seven fold in the same period. Imagine when shortages are resolved and there is a glut, these stocks will drop 75% $SNDK $MU $WDC $STX

$WMT is disappointed in results from OpenAI partnership, whereby Walmart users are allowed to shop via ChatGPT and OpenAI would receive a commission on these purchases

“Conversion rates—the percentage of users following through with a purchase of an item shown to them by ChatGPT—have been three times lower for the selection sold directly inside the chatbot than those that require clicking out, according to Daniel Danker, who oversees design and product for Walmart.

Put simply, Instant Checkout has been a flop.” -- Wired

OpenAI on a heater recently in the news….

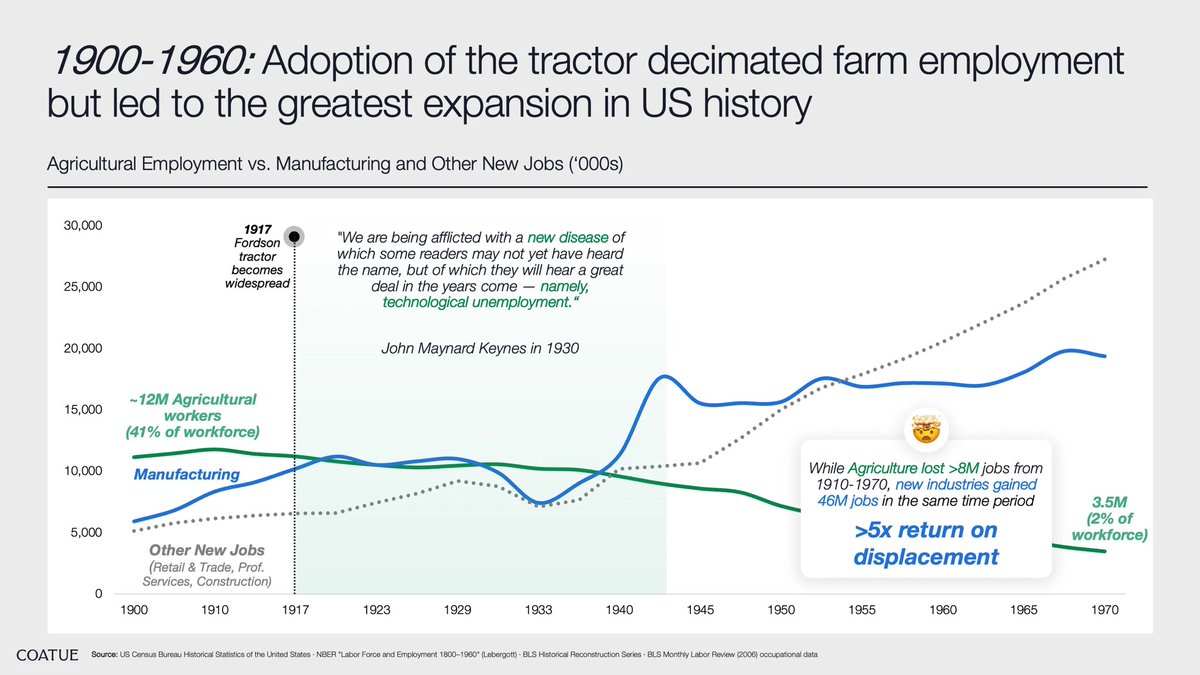

‘Will AI Lead to Mass Unemployment?’

Latest from Coatue..

‘AI will undoubtedly eliminate some tasks, but history suggests it will also create entirely new opportunities.

We looked past the AI “doomer” headlines to examine the history of creative destruction. From 1910 to 1970, the agriculture segment shed more than 8m jobs, while employment in newer industries grew by 46m over the same period.’

‘In fact, 60% of the jobs that exist today did not exist in 1940 — not in spite of technological change, but because of it.’

https://t.co/gQ39nenLSh